For Seres, Losses Aren't the Toughest Challenge

07/14 2026

07/14 2026

357

357

Post-AITO Brand Elevation: Strategies to Convert Scale into Profitability

Author|Ding Shan

Editor|Xiaobai

Cover Image|AI Generated

Produced by|Qiangdiao Next

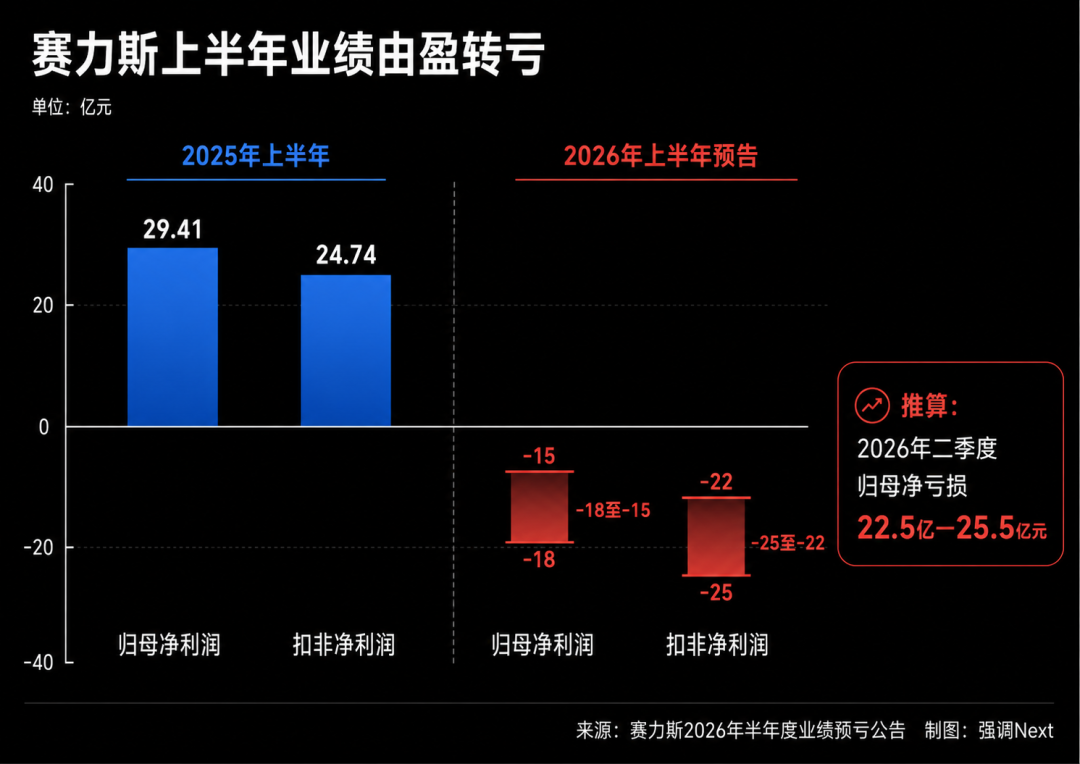

On July 12, Seres issued a performance forecast, projecting a net loss attributable to the parent company ranging from 1.5 billion to 1.8 billion yuan for the first half of 2026, in stark contrast to the 2.941 billion yuan profit recorded during the same period last year.

Given that the company still reported a profit of 754 million yuan in the first quarter, it is estimated that the net loss attributable to the parent company in the second quarter alone amounted to between 2.254 billion and 2.554 billion yuan. The core subsidiary, AITO, is expected to incur a loss ranging from 1.9 billion to 2.15 billion yuan in the second quarter. Seres attributed these losses to escalating prices of memory chips, industrial metals, and lithium carbonate, as well as adjustments to the book value of certain existing assets due to technological advancements and model upgrades.

Similarly, GAC Group also forecasts a net loss attributable to the parent company between 4.06 billion and 4.57 billion yuan for the first half of 2026. Having already reported a loss of 656 million yuan in the first quarter, GAC's estimated loss for the second quarter alone is approximately between 3.4 billion and 3.9 billion yuan. GAC cited similar factors, including rising raw material prices, increased sales investments, and shifts in product mix, coupled with declining sales of joint venture brands, reduced investment income, and exchange losses.

The automotive industry is currently grappling with profit squeezes due to escalating costs and intense price competition. Seres' losses cannot be solely attributed to its cooperation model with Huawei, nor can they be simply interpreted as a loss of operational control.

However, compared to GAC, Seres' distinctiveness lies in its previously industry-leading gross margins and robust product pricing power, yet it swiftly transitioned from profitability to losses within a single quarter. The issue is not merely the magnitude of external shocks but, more critically, how Seres can transform its acquired brand, sales volume, and high gross margins into a profit model less susceptible to cost fluctuations after AITO's rapid growth.

01. High Gross Margin, Yet Low Net Profit

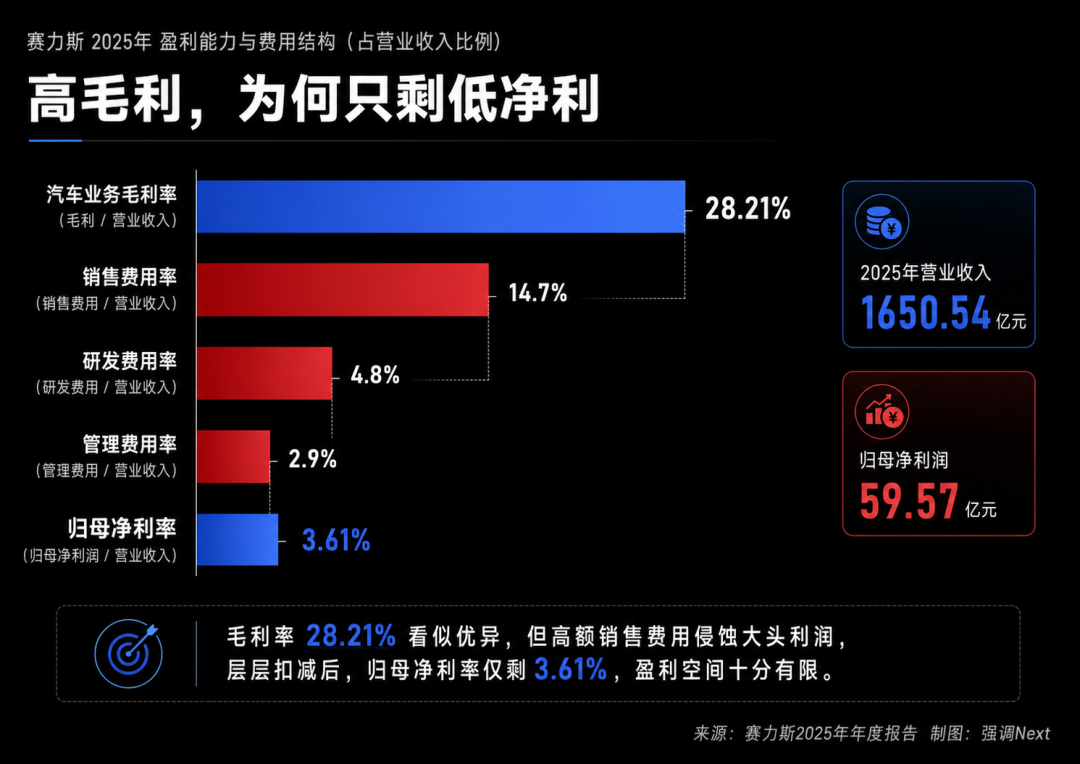

In 2025, Seres achieved an operating revenue of 164.888 billion yuan with a gross margin of 26.88%, nearing 30% in the third quarter. However, its net profit attributable to the parent company was only 5.957 billion yuan, corresponding to a net profit margin of approximately 3.61%. Non-recurring profit and loss net profit stood at 5.136 billion yuan, with a non-recurring net profit margin of about 3.11%.

In simpler terms, for every 100 yuan in revenue, nearly 27 yuan in gross profit was generated, but only about 3 yuan ultimately remained for shareholders.

The primary expenditures were sales, R&D, and administrative expenses. In 2025, Seres' sales expenses reached 24.194 billion yuan, accounting for approximately 14.7% of revenue. R&D expenses were 7.954 billion yuan, a year-on-year increase of 42.4%. Administrative expenses amounted to 4.787 billion yuan. Including capitalized portions, total R&D investment for the year reached 12.512 billion yuan.

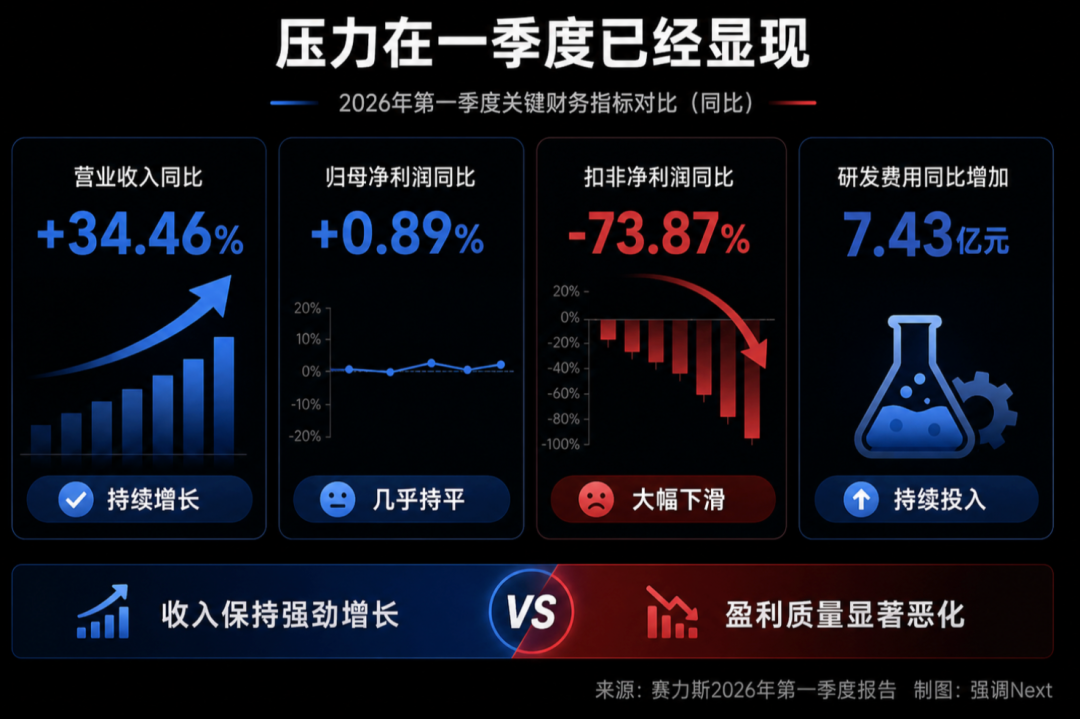

Pressure was already evident in the first quarter of this year. While Seres' revenue increased by 34.46% year-on-year, net profit attributable to the parent company grew by only 0.89%, and non-recurring profit and loss net profit decreased by 73.87%. The company explained that one of the main reasons was a 743 million yuan year-on-year increase in R&D expenses.

Financial data reveals that Seres' issue lies in high sales investments, high R&D investments, and high collaboration costs behind its high gross margins. The narrow net profit margin of only three to four percentage points can quickly be eroded by rising raw material prices, product transitions, and asset impairments.

02. The Next Step in Cooperation with Huawei: Not "Decoupling"

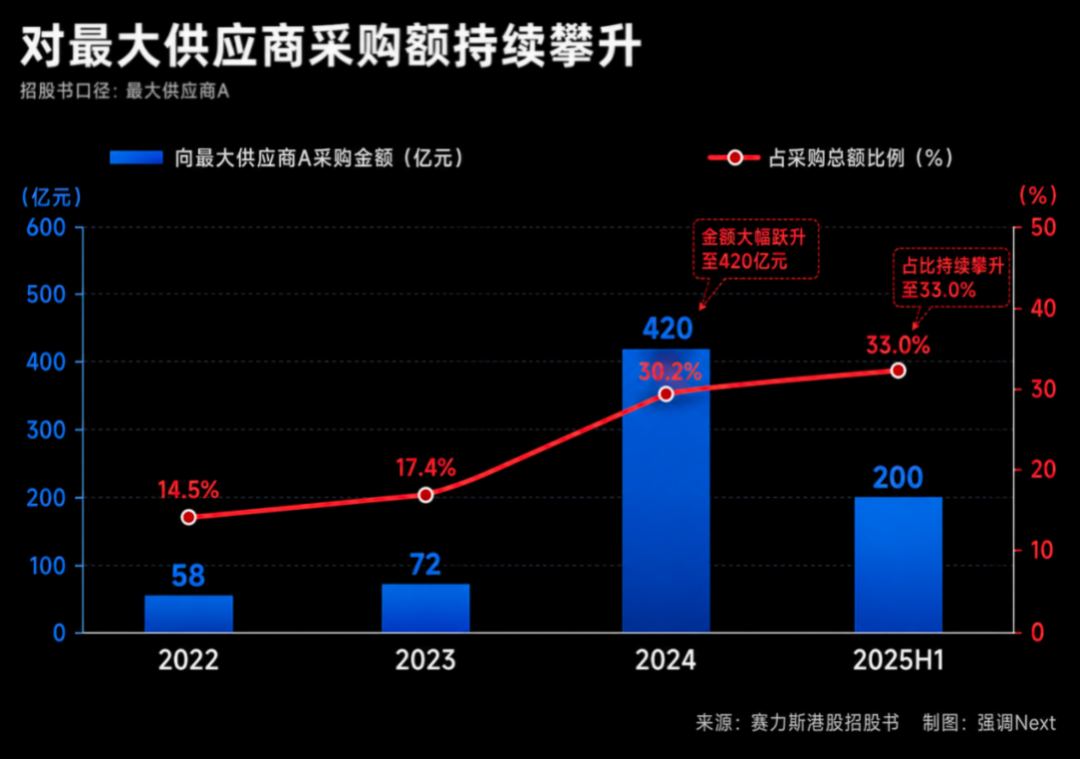

Seres' Hong Kong stock prospectus disclosed that from 2022 to 2024, the company's procurement volume from its largest supplier (the Huawei ecosystem) surged from 5.8 billion yuan to 42 billion yuan, with its share of total company procurement rising from 14.5% to 30.2%. An additional 20 billion yuan was procured in the first half of 2025, further increasing the proportion to 33%, equivalent to nearly 30% of total revenue for the same period (62.36 billion yuan).

Officially, this expenditure covers "procuring components such as smart cockpits and driving assistance systems" and "purchasing development and sales promotion services." Seres also explicitly stated in the prospectus that no profit-sharing arrangements exist. However, multiple industry media outlets estimate, based on vehicle pricing, that under the Smart Selection model, the Huawei ecosystem can generate nearly 10% of revenue from each vehicle's selling price (2% in technology licensing fees + 8% in sales channel service fees). For AITO's main price range of 300,000 to over 400,000 yuan, the revenue flowing to the Huawei ecosystem per vehicle is often estimated at over 100,000 yuan. Based on this, the total fees paid by AITO to the Huawei ecosystem from 2022 to the first half of 2025 are estimated to approach 75 billion yuan.

The rising procurement volume is often cited as evidence of Seres' dependence on Huawei. However, focusing solely on procurement amounts overlooks the value created by this cooperation for Seres.

AITO's rapid acquisition of premium pricing, intelligent capabilities, and nationwide channels would have required more time and potentially higher costs if built entirely from scratch by Seres. Huawei cooperation is not a panacea for Seres' profitability issues but rather a primary reason for its growth in recent years.

What truly needs adjustment is not the cooperation itself but whether Seres can achieve greater economies of scale after the cooperation matures.

As AITO's sales volume expands, advertising, channel, and service expenses should not continue to grow in tandem with revenue over the long term. The intelligence, electronic architecture, and manufacturing platforms of different models also need to be more reusable to avoid large-scale reinvestment and asset write-offs with each model transition.

Seres does not need to replicate BYD's approach of controlling batteries, chips, intelligent driving, and cockpits entirely in-house. This would not align with its existing capabilities and could create new heavy asset burdens. A more realistic path is to concentrate limited R&D resources on areas that can create differentiation, such as vehicle integration, manufacturing, chassis, range-extender systems, and user data.

For Seres, true technological autonomy does not mean producing all components in-house but rather maintaining the ability to define products, control costs, and integrate systems even if it changes partners.

03. AIVA: Not a Replication of AITO

AIVA offers Seres another avenue for growth.

Saidou Technology has introduced investors such as local state-owned assets and CATL, collaborating with Volcano Engine to develop smart cockpits, while autonomous driving is provided by Yuanrong Qixing. Seres' stake has been reduced to 32.96%, meaning it has chosen not to bear all the financial and operational risks of the new brand alone. AIVA's first mass-produced model is planned for launch within the year, targeting the market above 200,000 yuan.

AIVA is easily perceived as Seres' search for a second technology ecosystem outside Huawei, but merely changing partners may not improve profitability.

It should instead serve as an operational model experiment.

Since AITO already occupies the premium market, AIVA does not need to replicate another expensive brand, channel, and service system. It needs to prove whether Seres can launch competitive products in the mainstream market with a leaner organization, fewer upfront investments, and a more open supply chain.

This requires Seres to exercise restraint with AIVA. The number of models should not expand too quickly, R&D and manufacturing platforms should be reused as much as possible with existing systems, and marketing investments should not continue the high-profile approach commonly used for new brands.

Otherwise, AIVA may generate a new round of R&D, sales, and channel expenses before generating revenue. Seres would shift from bearing one high-cost cooperation system to bearing two simultaneously.

04. This Loss: An Opportunity for Adjustment

Seres currently has a solid financial foundation to address short-term losses. By the end of 2025, the company's monetary funds reached 87.287 billion yuan, and its asset-liability ratio declined significantly compared to the previous year. This loss will not immediately undermine the company's ability to continue operations.

This also means Seres does not need to immediately cut all R&D and brand investments for short-term profits. Given the automotive industry's product cycles, abrupt cuts in investment could lead to product gaps in the next two to three years.

A more reasonable adjustment is to re-evaluate which expenditures can be transformed into long-term capabilities and which merely sustain short-term sales volumes.

Investments in vehicle platforms, manufacturing systems, user data, and core integration capabilities are worth continuing. Repeated model development, overly frequent product transitions, and marketing expenditures lacking economies of scale should be reduced.

This is where Seres differs from traditional automakers like GAC. GAC must address multiple issues, such as the decline of joint venture brands, the transformation of autonomous brands, and organizational bloat. Seres' business is relatively concentrated, making its adjustment path clearer.

It does not need to rediscover its brand or prove consumer acceptance of AITO. Its next task is to reduce the sales, R&D, and collaboration costs per vehicle sold.

Therefore, judging whether Seres' profitability can recover should not focus solely on whether it turns a profit in the second half of the year.

More importantly, after AITO's sales recover, will sales expenses continue to grow in tandem? After model transitions end, will asset impairments decline significantly? After AIVA's launch, will it adopt a leaner operational model or add another cost system?

If these changes occur, the losses in the first half of 2026 can be viewed as a stress test caused by rising costs and product transitions.

If revenue resumes growth but expenses continue to rise at a similar or faster pace, then Seres' real challenge will no longer be raw material prices but how to operate an automotive company that has already reached a scale of hundreds of billions in revenue.

- END -

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge