No one dares to bet big on Seres' financial report

07/15 2026

07/15 2026

337

337

Before the financial report was even released, Seres was locked in a daily limit at 53.91 yuan by 3 PM on July 13th.

Market sentiment stemmed from the previous night's performance forecast. Net profit attributable to shareholders for the first half was projected to lose 1.5 to 1.8 billion yuan, with core net profit losing 2.2 to 2.5 billion yuan after non-recurring items.

A year earlier during the same period, these figures stood at profits of 2.941 billion and 2.474 billion yuan respectively. In just one year, nearly 5 billion yuan in profits vanished.

Market analysts raised two key issues. First, the performance forecast only shows profit results—the true operational health lies in cash flow, balance sheets, and segmented business data within the full report. Profit figures are superficial; these internal metrics reveal genuine operational strength.

However, the corporate announcement already identified two culprits: rising raw material costs increasing production expenses, and asset impairment from technological upgrades. The former tests supply chain control, while the latter exposes product rhythm and asset management—both core operational indicators.

Signs of deteriorating profits appeared in Q1's results, where core net profit plummeted 74% year-on-year to just 103 million yuan.

The second issue: Huawei is devouring Seres' profits.

The numbers are striking. In 2025, Seres paid Huawei subsidiary HiLink Intelligent 22.335 billion yuan in related procurement fees—3.75 times its annual net profit of 5.96 billion yuan.

But this doesn't fully explain why Seres still reported 6 billion yuan in annual net profit for 2025. Other automakers collaborating with Huawei haven't been crushed by similar revenue-sharing models.

Huawei isn't the root cause but rather an amplifier, exposing Seres' weaknesses in cost control, product rhythm, and channel efficiency. The flaws remain Seres' own.

On the night of the daily limit, founder Zhang Xinghai acted swiftly. Controlling shareholder Sokon Holdings announced plans to increase stakes by 150-300 million yuan within six months, complementing a previously announced 1-2 billion yuan share buyback and cancellation scheme—a full display of market defense.

But deeper issues remain unresolved. How could an automaker selling nearly 500,000 vehicles annually with a 27% gross margin have profits so thin that market fluctuations could easily wipe them out?

Market and corporate views sharply diverge on the causes of losses.

In its announcement, Seres attributed financial collapse to two factors: rising raw material costs and asset impairment.

Seres isn't alone in facing these challenges.

Since 2026, automotive-grade chip capacity has been squeezed by global AI computing demand, causing memory chip prices to surge from 20 yuan per unit to nearly 100 yuan—a 5x increase. Industrial metal price hikes have raised vehicle production costs, with lithium carbonate prices jumping from 80,000 to 180,000 yuan per ton (+125%), directly elevating battery system cost floors.

Consequently, each Aito vehicle faces 15,000-20,000 yuan in cost increases. Memory chips and lithium carbonate alone add 3,000-5,000 yuan per vehicle.

Based on ~160,000 deliveries in H1, this 15,000-20,000 yuan per-unit cost hike consumed 2.4-3.2 billion yuan in profit margins—roughly matching Seres' 2.941 billion yuan net profit in H1 2025.

Rising raw material costs have nearly erased Seres' entire profit margin, but the root issue remains its razor-thin profits.

In 2025, Seres reported 165.05 billion yuan in revenue and 5.96 billion yuan in net profit, but its net profit margin was just 3.6%.

For each 400,000-yuan Aito vehicle sold, Seres only kept ~14,400 yuan in profit after costs. At this margin, any minor external shock—raw material price hikes, escalating price wars, or asset impairment—could prove fatal.

In Q1 2026, Seres' net profit attributable to shareholders grew just 0.89% year-on-year to 754 million yuan, barely maintaining status quo.

Profit deterioration accelerated since year-start, with Q2's collapse pushing the downward trajectory deeper.

Additionally, Seres paid Huawei subsidiary Shenzhen HiLink Intelligent Technology 22.335 billion yuan in related procurement fees in 2025—nearly four times its 5.96 billion yuan net profit that year.

This means Seres paid Huawei nearly 4 yuan in procurement fees for every 1 yuan in profit earned.

During industry upcycles, this model benefited both sides. Huawei secured crucial cash flow and technology deployment scenarios for its smart vehicle business, while Seres transformed from an underdog to a market contender.

The problem lies in Huawei's rigid revenue-sharing model, which covers chips, intelligent driving software licensing, and in-store sales, leaving Seres little room to maneuver.

Seres now faces pressure from rising upstream raw material costs and downstream pricing constraints, while payments to Huawei remain unchanged. This triple squeeze has inevitably crushed profit margins.

If one symbol best represents Seres' predicament, it's not Huawei or lithium carbonate but the Aito M8.

Launched in April 2025 as a 400,000-yuan mid-to-large SUV, the M8 secured 80,000 orders in its debut month and delivered over 20,000 units in 45 days.

By its first anniversary in April 2026, cumulative deliveries surpassed 170,000 units, making it the best-selling 400,000-yuan SUV of the year.

Huawei Executive Director Yu Chengdong proudly announced the results exceeded expectations, while Seres Group Vice President Kang Bo hailed it as a benchmark for 400,000-yuan segment sales.

The M8 served as Seres' 2025 profit pillar, forming a dual-vehicle strategy with the flagship M9—M8 for volume and M9 for branding—covering the 400,000-600,000 yuan core profit range. In 2025, Seres achieved ~9,936 yuan in per-vehicle profit, leading Chinese NEV automakers, thanks largely to M8 and M9's high margins.

However, M8 sales collapsed in 2026.

Seres' H1 performance forecast and production reports explicitly noted the M8 as the model with the sharpest decline across the lineup. While Aito averaged over 35,000 monthly deliveries in 2025, this fell to ~27,000 in H1 2026 (-22.5%). All models—M7, M8, and M9—declined, with M8 suffering most.

As the industry enters rapid new-model iteration cycles, consumer expectations for new vehicles soar. The one-year-old M8 already appears outdated.

A bigger issue lies in internal product cannibalization.

Seres planned the Aito lineup with M5, M6, M7, M8, and M9 covering the 230,000-600,000 yuan range, aiming for each model to dominate its price tier and collectively capture the entire premium SUV market.

In reality, the ~360,000 yuan starting price of the M8 positioned it between the top-spec M7 and base-spec M9, siphoning sales from both. The top-spec M7 lost appeal, while M9 volumes were diverted.

By Q2 2026, the situation worsened. The all-new M9 launched on May 27th, creating a delivery gap for the old M9—just 3,000+ units in April and nearly halved in May.

Meanwhile, the 259,800-yuan starting Aito M6 gained significant volume, delivering over 30,000 units in 54 days and breaking 20,000 units in its first month.

In its performance forecast, Seres stated it adjusted book values for certain inventory assets (existing assets) with limited adaptability due to technological upgrades and model replacements, based on prudent principles.

In simpler terms, molds, production lines, and previous-generation intelligent driving hardware for old models became obsolete due to rapid new-model launches, resulting in one-time write-downs.

Behind this lies Seres' breakneck technological iteration—ADS upgraded from 3.0 to 4.0 to 5.0, with smart driving hardware receiving major updates annually. Each upgrade rendered previous R&D investments partially sunk costs.

While this rapid innovation drove Seres' market competitiveness, it now traps the company in a profit dilemma: creating hits through speed while eroding its own asset base at the same pace.

On July 13th—the day Seres hit the daily limit—another crisis erupted simultaneously.

SAIC Motor's 2024 annual report provided detailed explanations for its performance decline, impairment provisions, bases, and amounts:

"Due to declining fuel vehicle market share and escalating price wars, the company's sales revenue and gross margins decreased... Some models' expected future cash flows fell below book value, leading to asset impairment provisions based on test results... Estimated to reduce net profit by approximately 7.874 billion yuan in total."

However, Seres didn't disclose impairment amounts or their revenue proportion in its announcement.

According to the SSE Listing Rules, only when impairment provisions exceed 10% of the most recent audited net profit AND surpass 1 million yuan must disclosure occur. For Seres, this threshold is ~600 million yuan. Its failure to disclose suggests impairment below 600 million yuan, but this opacity deepens market distrust.

The deeper question: Seres' time window is visibly shrinking.

In 2026, the 1 millionth Aito vehicle rolled off the line. Zhang Xinghai vowed: "The first million took 5 years; the next million will take 2."

This implies annual sales of 500,000 units in 2026-2027, requiring 46,700 monthly deliveries over the following 18 months.

Yet H1 2026 saw Aito average just ~27,000 monthly deliveries, with worsening trends. Q1 still grew 43.9% year-on-year, but by June, monthly sales plummeted 30.19% year-on-year, with Seres' overall NEV sales dropping 26.94%.

Closing the gap from 27,000 to 46,700 monthly units requires nearly doubling sales. Meanwhile, Main vehicle models (main models) M7 and M8 are losing momentum. While the new M6 drives volume, it depresses profits, and the newly launched M9 needs time to scale.

Aito's competitors are entering rapidly. In September 2026, Xiaomi's first extended-range SUV, Pengcheng, will debut. The mass production (mass-produced) N90 positions as a mid-to-large flagship extended-range SUV, covering multiple price tiers from 200,000-450,000 yuan.

Viewed against 2026's NEV industry backdrop, Seres' predicament (predicament) reflects broader sector challenges.

In May 2026, domestic NEV retail penetration reached 63%. NEVs have entered the mainstream inventory (existing) market, with shrinking space to Excavate (tap) new demand through price cuts.

Industry competition logic is fundamentally shifting. Blunt price wars and sales volume races are ending, with product, technology, and brand-driven value competition becoming dominant.

Against this backdrop, over 10 mainstream automakers collectively raised terminal prices. Brands like BYD, Tesla, NIO, and Xiaomi implemented 2,000-20,000 yuan increases, marking the end of the two-year price war.

Seres sits awkwardly at this transition point, having failed to build cost and scale advantages during the price war before being pushed into value competition.

Seres isn't blind to these issues.

In February 2026, Seres made a strategic move: it spun off its Blue Electric brand assets, bringing in Chongqing Shapingba District Government and CATL as shareholders to establish independent company Saido Technology, which then launched the new AI car brand AIVA.

This calculated maneuver shed a loss-making asset from the listed company while planting seeds outside Huawei's ecosystem to seek growth. Globally, AITO's three global models target the Middle East and Europe, aiming for 30% overseas sales.

Simultaneously, Seres is entering new sectors. On June 15th, the humanoid robot Xiaosai debuted publicly.

The subtext: Seres is transforming from a Huawei contract manufacturer into a globally competitive premium automaker with full-stack capabilities.

But time may not be on Seres' side. Amid pressure on its core business, long-cycle investments in robotics and overseas expansion won't yield profits soon, while its main Aito business faces triple pressures of costs, competition, and product cannibalization.

Seres once won with speed, covering the path that traditional automakers took two decades to travel in just five years. But now, the management needs to answer whether Seres can learn to slow down and truly convert scale into efficiency?

-

AI's Richest Person Revealed: A Native of Zhanjiang!

-

No one dares to bet big on Seres' financial report

-

Standing at a Distance, Behind Xiaomi's Phone Slowdown and Layoffs", "Xiaomi Phone, Declining Sales, Offline Stores, Product Strategy, Comprehensive Ecosystem of People, Vehicles, and Homes", "Accordi

-

![]()

ByteDance Enters Physical AI, Igniting the Second Wave of 'Feast'?

-

![]()

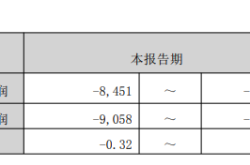

Phoenix Optics Forecasts a Nearly 70% Drop in First-Half Net Profit, Yet Optical Business Profit Shows Growth!

-

![]()

A Staggering 50.16% Reduction in Losses Projected! COST's Interim Report Signals a Pivotal Moment

-

![]()

Nearly 19% of National Total! Guangdong Boasts 164 Registered Large Models as New AI Personification Regulations Take Effect

-

![]()

BYD’s Baosha, Sought After by Australians, Makes a Triumphant Return to China