Who Killed the Profits of Automakers?

07/16 2026

07/16 2026

343

343

Automakers Reduced to Wage Earners

Author|Wang Lei

Editor|Qin Zhangyong

In the summer of 2026, the automotive industry staged an absurd drama.

GAC Group, Seres, BAIC BluePark, and JAC Motors all reported losses, with Great Wall, the once most profitable automaker, seeing its profit margin plunge by 60%.

Many of these automakers are players with annual sales in the millions.

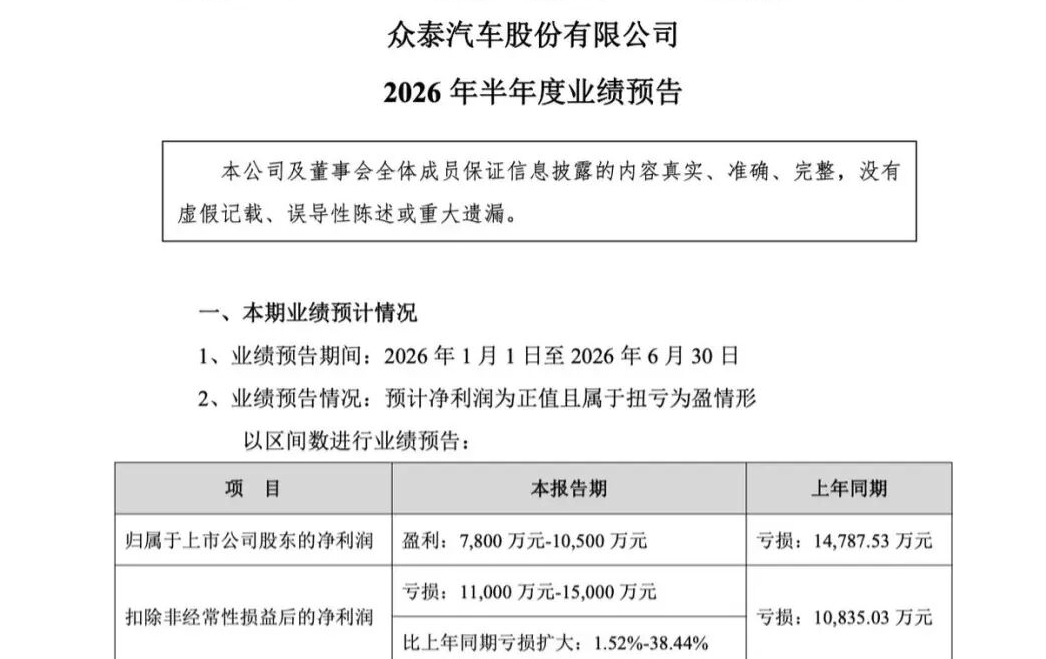

Even more surreal is another set of data: Zotye Auto, the once-ridiculed "tape measure department" known for copying Porsche and ultimately going bankrupt and restructuring, turned a profit in the first half of 2026.

You read that right—Zotye is making money, with an estimated net profit of 78 million to 105 million yuan for the first half of the year.

Giants producing hundreds of thousands of vehicles are bleeding money, while an automotive outsider is profitable.

This is the most authentic snapshot of China's automotive industry in 2026. Data just released by the China Association of Automobile Manufacturers (CAAM) shows that the profit margin for vehicle manufacturing has dropped to 1.5%, the lowest in a decade.

What does that mean? Selling a 200,000-yuan car earns the automaker just 3,000 yuan—not enough for a decent battery pack or even a high-end chip.

Where did all the money go?

01 Four Automakers Project Losses Exceeding 8 Billion

Based on performance forecasts disclosed by various automakers, their situations vary widely.

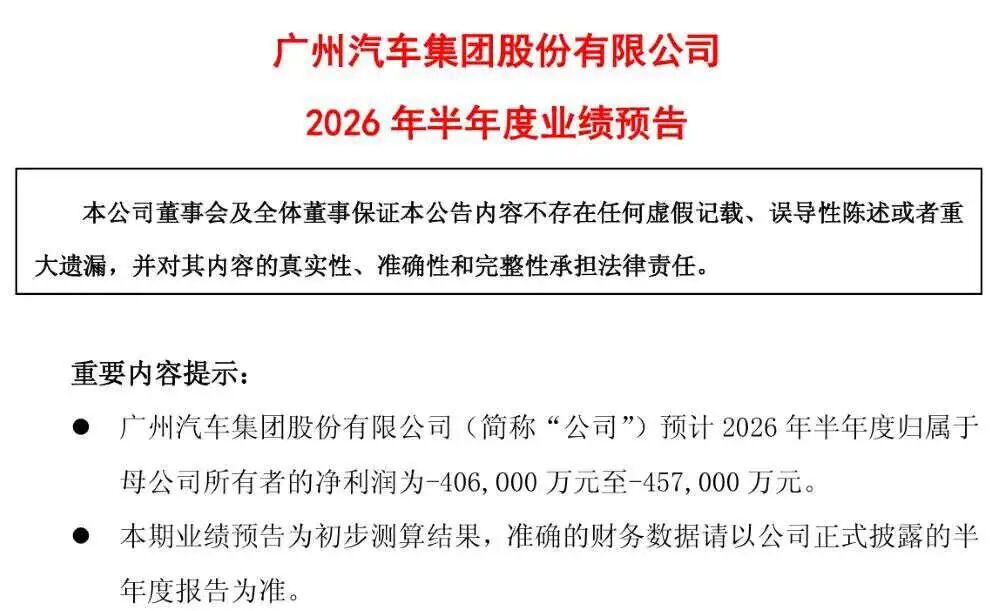

In terms of sheer loss magnitude, GAC Group fared the worst. Announcements show that GAC Group expects a net loss attributable to the parent company's owners of 4.06 billion to 4.57 billion yuan for the first half of 2026, with a net loss after non-recurring items of 4.8 billion to 5.6 billion yuan.

Compared to the net loss attributable to the parent company's owners of 2.538 billion yuan in the same period last year, GAC Group expects its net loss for the first half of 2026 to increase by 1.522 billion to 2.032 billion yuan, a year-on-year expansion of 59.97% to 80.06%—far from insignificant.

The reasons for the profit pressure, as explained in GAC's performance forecast, can be summarized in two points.

First, intensified domestic market competition and rising upstream raw material costs led to a year-on-year decline in profits for its self-owned brands, while joint-venture brands suffered from declining terminal sales. Second, exchange rate fluctuations resulted in foreign exchange losses, further squeezing profit margins.

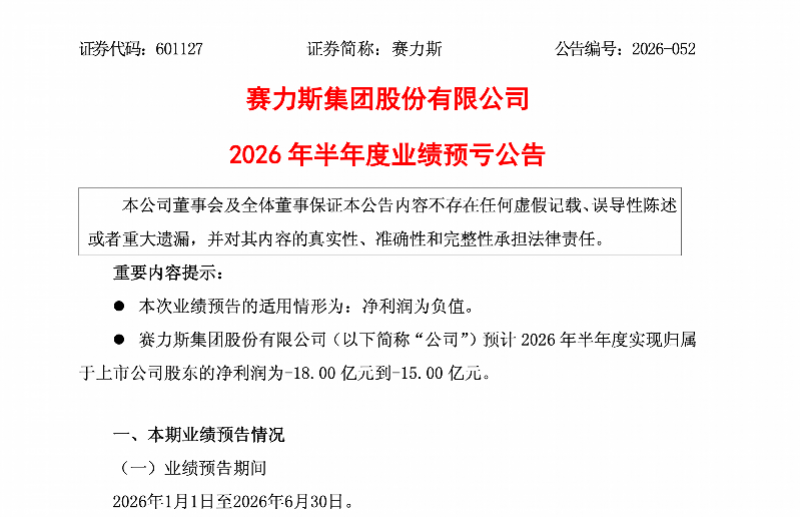

Next is Seres. Although its loss scale is far smaller than GAC Group's, its shift from profit to loss—due to its outstanding performance in the same period last year and its high degree of integration with Huawei—has made it the most talked-about case.

The loss forecast announcement shows an expected net loss attributable to the parent company's owners of 1.5 billion to 1.8 billion yuan for the first half of 2026, compared to a profit of 2.941 billion yuan in the same period last year—a staggering swing of over 80%. Seres also mentioned in the announcement that its core subsidiary, Aito Automotive, reported a net loss attributable to the parent company of 1.05 billion to 1.3 billion yuan for the first half of 2026.

The problem is, Seres didn't sell fewer vehicles—its sales even grew. In the first half of 2026, Seres' new energy vehicle sales totaled 178,800 units, up 3.87% year-on-year; among them, Seres Aito series sales reached 160,800 units, up 5.60% year-on-year.

It's worth noting that GAC also didn't sell fewer vehicles, with 773,100 units sold in the first half, up 2.35% year-on-year, and exports surging by 132%. More sales, but even bigger losses.

As for why they fell into the trap of "selling more, losing more," Seres also clarified two factors in its announcement: rising costs due to price increases in major raw materials such as memory chips, industrial metals, and lithium carbonate, and adjustments to the book value of certain inventory assets (existing assets) with limited adaptability due to technological iterations and model updates.

Two other automakers also issued loss forecasts: BAIC BluePark and JAC Motors. The former expects a net loss attributable to shareholders of listed companies of 1.77 billion to 1.97 billion yuan for the first half, a narrowing of about 340 million to 540 million yuan compared to the same period in 2025.

The latter expects a net loss attributable to the parent company's owners of about 740 million yuan for the first half, a reduction of about 33 million yuan compared to the 773 million yuan loss in the same period last year, a year-on-year narrowing of about 4.25%.

While both are still in the red, at least their losses aren't widening further.

02 Two Automakers Earn 5.1 Billion Less in Half a Year

But don't assume that automakers still in the black are faring well.

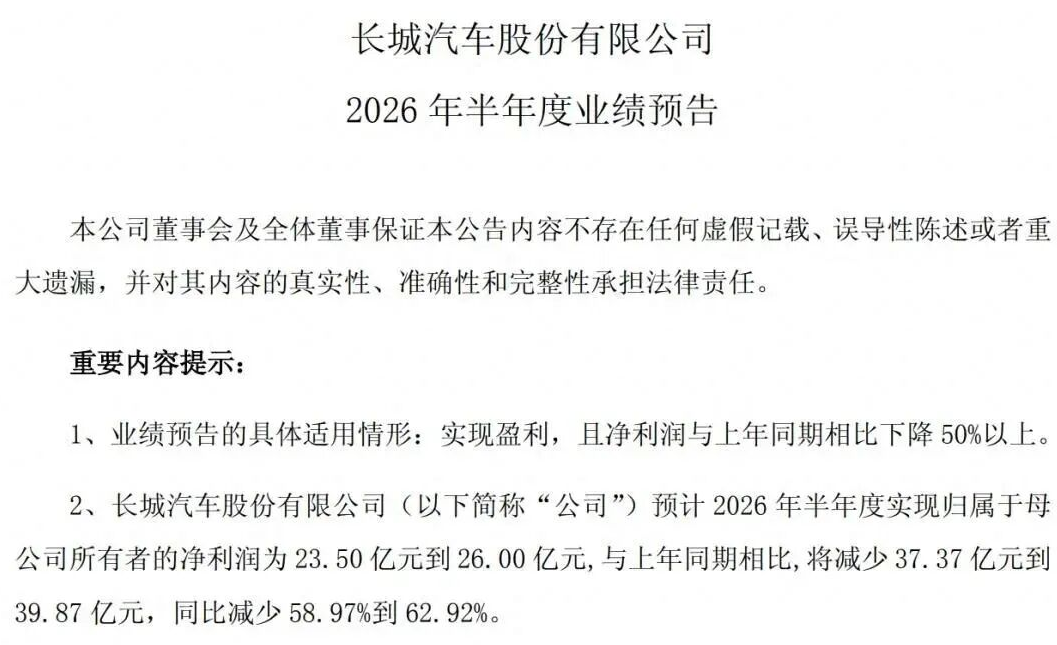

Performance forecasts disclosed during the same period also include Great Wall Motors and Changan Automobile. While they haven't slipped into losses, their profitability has severely declined.

Great Wall Motors expects a net profit of 2.35-2.6 billion yuan for the first half of 2026, compared to 6.337 billion yuan in the same period last year—a year-on-year decline of 58.97%-62.92%.

Great Wall Motors attributed the profit decline to two factors: delayed receipt of overseas tax policy subsidy benefits and exchange rate fluctuations.

The financials bear this out. In the first half of last year, Great Wall Motors received a 2.274 billion yuan overseas tax policy subsidy. This year, that subsidy failed to arrive on schedule, evaporating nearly 2.3 billion yuan in profit alone.

Additionally, in the first half of this year, Great Wall Motors incurred comprehensive foreign exchange losses of about 266 million yuan, compared to foreign exchange gains of 1.493 billion yuan in the same period last year—a year-on-year reduction in foreign exchange gains of about 1.759 billion yuan.

Combined, these two non-recurring factors account for exactly 4 billion yuan. This means that nearly all of Great Wall Motors' decline in net profit for the first half can be explained by these two factors.

On the same day, Wei Jianjun also posted on social media, not shying away from the profit decline but stating, "While surface numbers are important, we care more about the healthy development of the enterprise, especially in the current complex and fiercely competitive market environment."

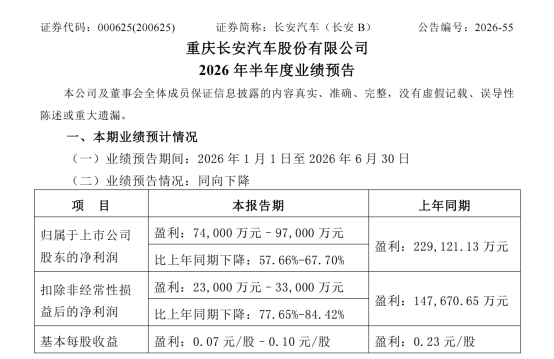

Changan Automobile, another automaker escaping the trap of selling vehicles at razor-thin margins, expects a net profit attributable to shareholders of listed companies of 740 million to 970 million yuan for the first half of 2026, a year-on-year decline of 57% to 67% from 2.291 billion yuan in the same period last year—effectively halving overall profits.

After excluding non-recurring items, only 230 million to 330 million yuan remains, a year-on-year decline of 77% to 84% from 1.477 billion yuan in the same period last year.

In response, Changan Automobile provided clear official attribution, all stemming from operational pressures brought by external market conditions. Exchange rate fluctuations causing foreign exchange losses were a major reason for the profit shrinkage, as Changan Automobile's overseas sales reached 454,700 units in the first half of this year, surging by 51.87% year-on-year.

The rising share of overseas business revenue has also made exchange rate fluctuations increasingly significant in impacting corporate profits.

Another core reason is the sustained rise in raw material costs, continuously driving up vehicle manufacturing costs. However, Changan Automobile stated that it has already implemented a series of improvement measures, such as cost reduction, expenditure control, and technological optimization, to mitigate the impact of rising raw material costs.

03 A Profit Margin of 1.5%

While the reasons cited by each automaker vary, there are quite a few (many) commonalities, such as rising raw material costs and intensified domestic market competition.

In June of this year, Zhang Xinghai, Chairman of Seres Group, pointed out at the 2026 China Automotive Chongqing Forum that the unit price of memory chips had risen from 20 yuan to nearly 100 yuan, a fivefold increase; lithium carbonate prices had surged from 80,000 yuan/ton in the same period last year to 180,000 yuan/ton. The average manufacturing cost per Aito vehicle had increased by 15,000 to 20,000 yuan.

Keep in mind that a bicycle (per-vehicle) cost increase of around 20,000 yuan is enough to offset the bicycle (per-vehicle) profit or even gross profit of most automakers.

Li Bin once said, "The cost of each NIO ES8 has risen by nearly 20,000 yuan. To maintain the original gross profit, the selling price would need to increase by 30,000 yuan."

Price hikes of 20,000 to 30,000 yuan, when reflected in terminal prices, would inevitably be rejected by consumers. In other words, automakers must absorb these cost increases internally to the greatest extent possible when facing price hikes.

According to data from Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), automotive industry revenue grew by 1.4% year-on-year from January to May 2026, but costs increased by 2.3%—higher than revenue growth—leading to a 20% year-on-year decline in profits.

Correspondingly, upstream companies began reaping huge profits.

For example, China's "memory duo" GigaDevice and Longsys. The former reported a net profit of 6.9 billion yuan in the first half, up 1,099% year-on-year; the latter expects a net profit of 9.2 billion to 11 billion yuan, up at least 622 times year-on-year.

Lithium mining and lithium salt companies fared similarly. Tianqi Lithium reported a net profit of 2.85 billion to 4.25 billion yuan in the first half, up 3,276%-4,935% year-on-year; Ganfeng Lithium's net profit reached 3.65 billion to 4.6 billion yuan, up 787%-965% year-on-year.

Additionally, all automakers do or think the same without prior consulation (in unison) mentioned "intensified market competition," which, in simpler terms, means price wars and internal price competition.

Although many automakers have announced price hikes this year, data from the CPCA shows that the dominant theme in the first half of 2026 was still price cuts. According to Cui Dongshu's statistics, from January to June this year, the average price of new conventional fuel vehicle models undergoing price cuts was 225,000 yuan, with an arithmetic average price cut of 32,000 yuan—a 14.1% reduction. This even led to headlines like "Buying a Land Rover for 160,000 yuan."

Additionally, the average price of new energy vehicle models undergoing price cuts was 247,000 yuan, with an arithmetic average price cut of 30,000 yuan—a 12% reduction.

Under the dual pressures of soaring costs and internal price competition, the "backlash" of price wars arrived prematurely—industry profits evaporated rapidly.

According to industry data disclosed by Chen Shihua, Deputy Secretary-General of the CAAM, the average profit margin for domestic vehicle manufacturing fell to 1.5% in the first half of 2026, a 43% year-on-year decline and the lowest in nearly a decade.

What does that mean?

From January to May 2026, the average revenue profit margin for industrial enterprises above designated size nationwide was 5.56%. Vehicle manufacturers' profit margins are far below this average, and the automotive industry fell from this level to 1.5% in less than three years.

To avoid being left behind by the market, automakers are rushing new products onto the table at an astonishing pace. From January to May, 542 new models were launched domestically. Before the R&D, mold, and production line costs of the previous model are recovered, the next generation is already hitting the market. Marginal profits are being eroded continuously, trapping the automotive industry in a cycle of "increasing competition leading to increasing losses, and increasing losses fueling even fiercer competition."

For consumers, this is indeed a feast—they can buy higher-spec vehicles at lower prices. But when manufacturing profits are compressed to 1.5%, one can guess which way the scale will tilt between "cost reduction" and "quality."

-

![]()

The Dead End of GoPro: Unveiling the Decisive Factors in DJI and Insta360's Competition

-

![]()

The Dead End for GoPro: Unveiling the Key to Victory in DJI and Insta360's Competition

-

DeepSeek Targets A-share IPO Amid RMB 480 Billion Valuation Debate

-

![]()

WPS Meitu XiuXiu: The Threat to Its Market Position from AI Large Models

-

![]()

After Seres Reports Losses, What Is the Capital Market Really Worried About?

-

![]()

Honor, Stepfun, and Nubia Vie for 'Pioneering' Status: The Fierce Contest Among AI-Powered Smartphones

-

![]()

Glory, Stepfun, and Nubia Vie for the Pioneering Position: AI-Powered Smartphones Engage in Intense Competition

-

![]()

Apple AI Gains Approval but Faces Outdated Challenges