Leapmotor Surges Ahead, Second-Tier Brands Lock Horns in Fierce Competition

07/16 2026

07/16 2026

547

547

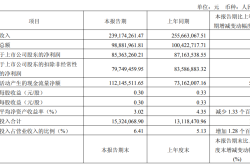

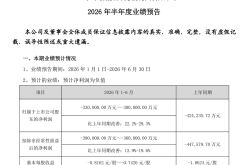

Over the past six months, the competitive landscape in China's domestic new energy vehicle (NEV) market has intensified, leading to a further divergence among NEV startups. Notably, Leapmotor emerged as the frontrunner, with cumulative sales reaching 356,487 units in the first half of the year, making it the sole brand to exceed 350,000 units. Li Auto and NIO followed closely, with 193,472 and 191,123 units sold, respectively, in a tight battle for second and third place. Xiaomi Motors saw its cumulative sales surpass 180,000 units in the first half, marking a significant jump from over 150,000 units during the same period last year. Meanwhile, XPeng Motors ranked fifth, with cumulative sales of 165,977 units, reflecting a 15.83% year-on-year decline. Overall, the rankings among NEV startups are in constant flux, with intensifying competition at the top and a rapidly evolving market landscape.

Leapmotor: 356,487 units

In the first half of 2026, Leapmotor maintained its robust growth trajectory, achieving cumulative sales of 356,487 units, a 60.82% year-on-year increase. It became the only NEV startup to surpass 300,000 units in sales during the first half of the year, leading its nearest competitor by approximately 160,000 units and showcasing a significant competitive edge. Since the start of 2026, Leapmotor's monthly sales have consistently climbed, securing the top spot in NEV sales for five consecutive months, demonstrating remarkable market performance. According to its first-quarter financial report, Leapmotor generated revenue of RMB 10.82 billion, an 8% year-on-year increase, marking a record high for the first quarter. It delivered 110,155 units globally, with overseas sales exceeding 40,000 units, opening up new growth avenues in international markets.

Over the past two years, Leapmotor's product portfolio has continuously expanded. The Leapmotor B-series and C-series have become the cornerstone of its sales. Key models such as the new A10 and C10 have consistently contributed to sales, collectively accounting for nearly half of Leapmotor's total sales. Looking ahead, while continuing to refine the B and C series, Leapmotor will accelerate the development of its A and D series, further enhancing its product matrix and driving sales growth. If it can sustain monthly sales growth exceeding 70,000, 80,000, and 90,000 units, and capitalize on new product launches and overseas market expansion, Leapmotor may have a greater chance of achieving its annual sales target of 1 million units.

Li Auto: 193,472 units

In the first half of 2026, Li Auto achieved cumulative sales of 193,472 units, a 5.13% year-on-year decrease, ranking second among NEV startups in terms of sales volume. Financial reports indicate that in the first quarter of this year, Li Auto generated revenue of RMB 25.93 billion, providing financial support for subsequent product development and new product launches.

Currently, Li Auto's strength lies primarily in the family SUV market, with models L6, L7, L8, and L9 covering the price range of RMB 200,000 to RMB 500,000. Notably, the Li Auto i6 has performed exceptionally well, with an average monthly sales volume exceeding 20,000 units, accounting for nearly 60% of Li Auto's total sales and becoming a key driver of its current sales growth. In contrast, the contribution of the Li Auto L series has waned, with models L8 and L9 underperforming in the market, each accounting for approximately 10% of monthly sales. As competition in the extended-range SUV market intensifies and similar competitors continue to emerge, the price and configuration advantages of the L8 and L9 are gradually diminishing, naturally facing greater pressure for sales growth.

In the second half of the year, Li Auto will introduce the next-generation Li Auto L6, initiate the delivery of the all-new Li Auto L8, and sequentially launch new products such as the all-new L7 and the flagship battery electric SUV, the Li Auto i9, further refining its product lineup.

NIO: 191,123 units

In the first half of 2026, NIO achieved cumulative deliveries of 191,123 new vehicles, a 67.43% year-on-year increase. Among them, the NIO brand delivered 119,488 units, the Onvo brand delivered 42,463 units, and the Firefly brand delivered 29,172 units. The combined efforts of the three brands supported NIO's overall sales volume. From a sales structure perspective, the NIO brand remains the main contributor to sales, with the NIO ES8 serving as the brand's sales leader, accounting for approximately 70% of average monthly sales. Models such as the ES6 and ET5T maintained stable deliveries; the Onvo brand contributed an average of approximately 7,000 units in monthly sales; and the Firefly brand contributed an average of approximately 5,000 units in monthly sales, further enriching NIO's product lineup.

Looking ahead to the second half of the year, NIO will continue to focus on product development. With the launch of the all-new ES8 and the subsequent addition of models such as the all-new ES7 and ES6 to its product lineup, NIO will have new opportunities for sales growth. It is reported that NIO's sales target for 2026 is 450,000 to 490,000 units. Whether this target can be achieved will depend on NIO's overall sales performance and whether its new models can generate significant incremental sales.

Xiaomi Motors: 180,000 units

In the first half of this year, Xiaomi Motors achieved cumulative sales of approximately 180,000 units. From a sales structure perspective, the Xiaomi SU7 and YU7 have formed a "dual-model strategy," covering the sedan and SUV segments and jointly supporting Xiaomi Motors' sales growth.

However, as competition in the NEV market intensifies, relying solely on the SU7 and YU7 models is no longer sufficient to support Xiaomi Motors in achieving greater sales breakthroughs. Meanwhile, competitors such as the Qijing GT7, Shangjie Z7, and Zhijie EHX are set to enter the market, further increasing the competitive pressure on Xiaomi Motors.

In the second half of the year, the first model of Xiaomi Motors' second product series, the Pengcheng N90, will officially launch in August. According to its plans, Xiaomi Motors has raised its annual sales target for 2026 to 550,000 units. To achieve this target, not only do the SU7 and YU7 need to maintain stable deliveries in the second half of the year, but the Pengcheng N90 must also quickly gain market traction to contribute new sales increments.

Whether the Pengcheng N90 can stand out will largely depend on whether its pricing can attract consumers.

XPeng Motors: 165,977 units

In the first half of 2026, XPeng Motors achieved cumulative sales of 165,977 units, a 15.83% year-on-year decrease. Financial reports indicate that in the first quarter of this year, XPeng Motors' gross margin for complete vehicles was 12.1%, with R&D investment reaching RMB 2.91 billion. Going forward, XPeng must not only launch new products to sustain sales growth but also convert its order backlog into stable deliveries.

From a sales structure perspective, the MONA M03 remains the main contributor to XPeng's brand sales, accounting for over 40% of total brand sales, with the P7+ also maintaining a stable contribution. However, XPeng's sales still rely heavily on a single model. In the second half of the year, XPeng will launch a new wave of products. With the pre-sale of the XPeng MONA L03, the upcoming launch of the MONA L05, and the sequential introduction of new models such as the all-new G9L and a large five-seat extended-range SUV, XPeng aims to boost its sales in the second half of the year.

According to its plans, XPeng's sales target for 2026 is 550,000 to 600,000 units. Whether this target can be achieved will depend on whether the G series models can sustain sales growth, whether the MONA L03 can gain market traction, and whether new products can contribute significant incremental sales. Additionally, the contribution from overseas markets will also be worth watching.

Summary

Overall, in the first half of 2026, NEV startups underwent a new round of reshuffling. Leapmotor secured the top spot with 356,000 units delivered; brands such as Li Auto, NIO, Xiaomi, and XPeng intensely competed for positions in the second tier, with market rankings still subject to constant adjustment.

As we move into the second half of the year, major NEV startups will focus on launching multiple new models, which are expected to further drive sales recovery upon their market introduction. However, it is also evident that competition in the NEV market remains fierce, with ongoing intense competition for market share among automakers.

(Image source: Internet. Rights reserved for deletion in case of infringement.)

-

![]()

Is Tencent AI Heading in the Right Direction?

-

Latest Update! Jinding Optics’ GEM IPO Review Now “Under Inquiry”

-

![]()

VOYAH’s CBO Sets Ambitious Target: Secure Top 3 Spot in Luxury BEV Market Within Two Years, Launch 4 New Models to Cover All BEV Segments

-

![]()

Sehwa Technology Invests 740 Million Yuan, Eyeing the Lucrative Optical Film Market!

-

![]()

150 Million Users, $40 Million ARR: AIShige Technology Enters the Final Round of AI Video Competition

-

![]()

StepOn Star Forays into Smartphone Manufacturing: A Rationally Sound Yet High-Risk Endeavor

-

![]()

TCL Zhonghuan: Embracing a New Story Despite Anticipated Losses

-

![]()

Forty Years On: From Volkswagen’s State-Backed Entry into China to BYD’s Hiring of a Former European Foreign Minister