Mid-Game Battle of Chinese Automakers: Collective Overseas Expansion for Growth? | Halftime Whistle ②

07/16 2026

07/16 2026

377

377

By Yang Xuejian Source / Node Auto

The year 2026 is set to become a pivotal turning point for the Chinese auto market.

In the first half of this year, China's automobile production and sales stood at 14.993 million and 15.017 million units, respectively, down 4% and 4.1% year-on-year (data from the China Association of Automobile Manufacturers, CAAM). When focusing specifically on passenger vehicles, the decline was even more alarming: from January to June 2026, passenger vehicle production and sales reached 12.721 million and 12.72 million units, respectively, down 5.9% and 6% year-on-year (CAAM data). After a decade of rapid growth, the automotive market is clearly showing signs of leveling off, with the curve experiencing an inflection point.

However, exports continue to surge.

According to CAAM statistics, China's complete vehicle (complete vehicle) exports reached 5.096 million units from January to June 2026, up 65.3% year-on-year. Passenger vehicles have become the absolute mainstay of China's automotive exports, with 4.432 million units exported in the first half, up 71.7% year-on-year, including 2.302 million new energy passenger vehicles, a 1.3-fold increase.

Equally important as sales are financial results. Selling more while incurring heavier losses is not a sustainable path. Unlike new-force automakers that prioritize vehicle sales first, traditional self-owned brand giants like BYD, Geely, Chery, and Great Wall face greater challenges in balancing the terminal market with the capital market, domestic and international markets, and products with technology.

In this critical year for elimination, as described by industry leaders, traditional self-owned brands have shown different strategic directions in the first half of 2026.

1. BYD: Making a Strong Push Overseas

BYD's first-half data could be described as "divided."

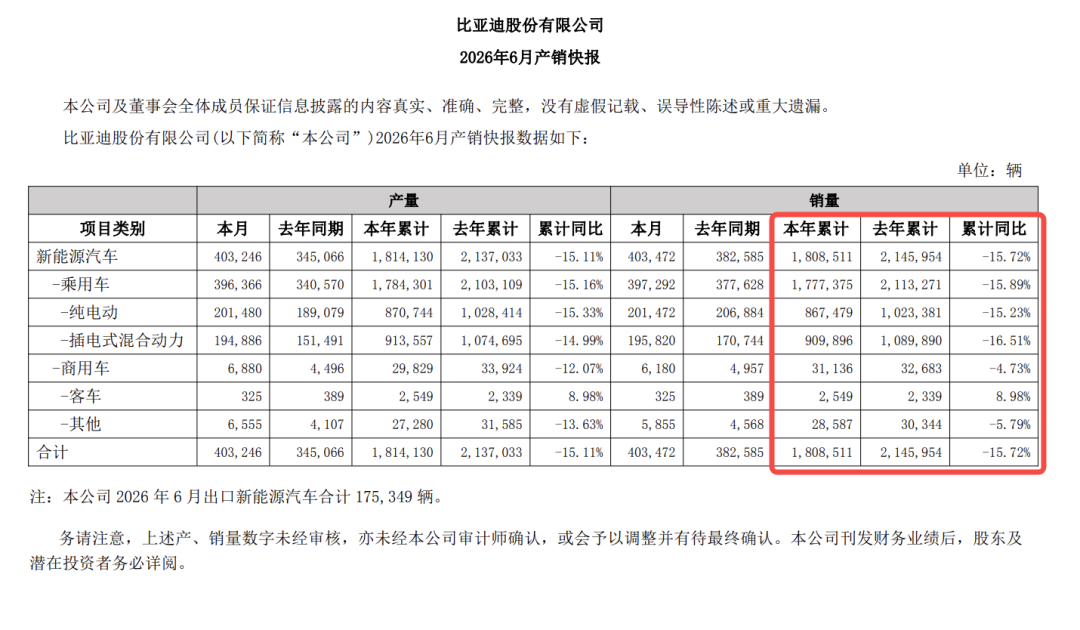

Cumulative sales from January to June reached 1.8085 million units, but year-on-year growth declined by 15.72%. Even more "divided" is that, among BYD's segmented vehicle statistics, only buses saw year-on-year growth, while all other segments declined. Such data is rare in BYD's recent years of rapid growth.

More critically, Geely is rapidly catching up to BYD in the domestic market, attempting to end BYD's lead in the new energy vehicle (NEV) market. If BYD heavily invests in the domestic market, it will continue to be bogged down in the "price war." Therefore,

Looking at BYD's June data, monthly sales reached 403,472 units, up 5.5% year-on-year and 5.2% month-on-month, returning to an upward trajectory. Where did this growth come from? None other than overseas markets.

Data shows that BYD's cumulative overseas sales in the first half of 2026 reached 789,400 units, a staggering 70.65% year-on-year increase, with exports accounting for 43.8% of total sales. In June alone, overseas exports exceeded 175,000 units, up 95% year-on-year, continuously breaking historical records.

Image Source: BYD

The place that has attracted the most global attention in the past month is undoubtedly Mexico, the United States, and Canada. These three countries are jointly hosting the 2026 FIFA World Cup, and BYD has launched a significant marketing campaign in Mexico, including sponsoring domestic broadcast programs and collaborating with local Chinese youth football teams for exhibition hall and stadium viewing events, leveraging the World Cup's massive IP to play a strong sports marketing card in one of the host countries.

The reason for such heavy investment is that Mexico is one of BYD's key overseas export markets. Having entered the local market in 2023, in just under three years, BYD has become the leader in Mexico's new energy vehicle market. For example, in 2025, BYD sold nearly 80,000 electric and plug-in hybrid vehicles in Mexico, capturing about 70% of the segment. In May 2026, there were also reports that BYD, Geely, GAC, and other domestic companies were bidding for Nissan's Mexican factory.

In

2. Geely: A Representative of Accumulated Strength

Image Source: China Passenger Car Association (CPCA)

In the CPCA's ranking of narrow passenger vehicle manufacturers' retail sales from January to June 2026, despite a 16.7% year-on-year decline in cumulative sales, Geely ranked first with over 1.02 million units and an 11.7% market share, about 30,000 units more than second-place BYD. It was also the only self-owned brand to exceed one million units in sales in the first half.

As mentioned earlier, Geely is rapidly catching up to BYD in the domestic market. Based solely on domestic industry statistics, Geely has occasionally surpassed BYD since late 2025.

In the battle for domestic market leadership, Geely seems determined to win.

On the morning of July 15, Geely Holding Group officially released its statistical data, reporting total sales of 1.935 million units in the first half, including over 1.1 million new energy vehicles, with an NEV penetration rate nearing 57%.

As Geely Holding's core automotive segment, Geely Auto (including Geely, Lynk & Co, and Zeekr brands) reported total sales of 1.423 million units in the first half, with NEV sales approaching 800,000 units, up 10% year-on-year. In terms of overseas sales, a relatively weaker area for Geely, the company shipped 474,000 units in the first half, surpassing its total exports for all of 2025, though still lagging behind BYD.

Within Geely Auto's portfolio, each sub-brand has shown steady progress. Specifically, Geely's China Star series sold 581,000 units in the first half, leading self-owned brands in the fuel vehicle market; Geely Galaxy, focused on NEVs, sold 520,000 units; Lynk & Co sold 144,000 units, with NEV products now accounting for 65% of its sales. Among premium brands, Zeekr delivered 178,000 units in the first half, up 97% year-on-year.

In terms of overseas expansion, while Geely's overall overseas sales lag behind Chery and BYD, Zeekr is a leader within the Geely system.

In the second half of the year, the Zeekr 8X Thousands of miles and vastness G-ASD H9 variant will be delivered, with its performance in the intelligent sector warranting special attention. Whether Zeekr and Geely as a whole can sustain export growth in the second half will also be a key focus.

3. Chery: The Export Leader's Hidden Worries

After successfully listing on the Hong Kong Stock Exchange in September 2025, Chery has become more active in the automotive market and marketing. Looking back at the first half of 2026, Chery announced plans to develop controlled nuclear fusion ("artificial sun") research, surprising the outside world: Chery, known for its "grassroots hut" spirit and "engineering nerd" image, seemed to have changed.

Focusing back on the automotive business, Chery Group reported cumulative sales of 1.358 million units in the first half, up 7.7% year-on-year. Chery exported 945,000 vehicles in the first half, up 71.5% year-on-year, with exports accounting for nearly 70% of total sales. Combining this with the CPCA's first-half domestic retail statistics, it is clear that Chery's sales rely heavily on overseas markets. Its five brands—Chery, Exeed, Jetour, iCAR, and Luxeed—sold only 413,000 units domestically in the first half, down 36.4% year-on-year.

Chery Group has held the top spot in domestic export sales for 23 consecutive years, covering over 130 countries and regions overseas, with factories in eight countries and KD assembly plants in 16. Undoubtedly, Chery leads domestic automakers in the depth and breadth of its overseas Layout (layout).

However, the 3:7 ratio of domestic to overseas sales in the first half of 2026 reveals Chery's hidden worry: a severe domestic market imbalance.

While overseas markets are Chery's core source of sales and profits, if its domestic market share continues to decline, Chery risks an unstable foundation.

From the CPCA's first-half statistics, Chery's domestic market share was only 4.7%, far behind Geely and BYD. Meanwhile, BYD is growing rapidly overseas. In the first half of 2026, BYD's cumulative overseas sales reached 789,400 units, about 155,000 units less than Chery's, but the gap is narrowing, which should alarm Chery.

BYD's overseas sales target for 2026 is 1.5 million units, with 53% of the target achieved in the first half. Chery has not officially released an export target, but based on its 2025 export performance of 1.344 million units, its 2026 target is likely around 1.5 million units.

If, hypothetically, both BYD and Chery achieve their overseas sales targets, it would represent a successful step for BYD in offsetting its domestic market strategy with strong overseas growth. However, for Chery, it would mean losing ground in both domestic and overseas markets.

Chery urgently needs to reevaluate its domestic market strategy. Currently, Chery's five-brand portfolio is clear and reasonable, with the core Chery brand targeting the mainstream market, Jetour focusing on off-road segments, iCAR on personalized NEVs, and Luxeed in collaboration with Hongmeng Zhixing.

The brand lineup is sound, so where is the problem? In

Using World Cup Asian teams as an analogy, Arsène Wenger, former Arsenal manager and now FIFA's Global Football Development Director, pointedly noted, "The pace of World Cup matches has become so fast that teams must keep up. Asian teams have all been eliminated because they cannot match the intensity and speed, nor do they possess sufficient technical competitiveness."

This assessment applies equally to the auto market. When BYD and Geely set such a fast pace, other automakers risk elimination if they cannot keep up. For Chery, with five brands in hand, the question is how to play them effectively. How can its "engineering nerd" technical advantages be more efficiently integrated with mass-produced products? These are issues that must be resolved quickly.

4. Great Wall: Is Declining Profit No Cause for Concern?

If any automaker has remained relatively "rational and restrained" during the most intense years of price wars in the auto market, it is Great Wall Motors. Over the past few years, Great Wall has insisted on not blindly engaging in "price wars," maintaining stable new vehicle pricing at the terminal level to ensure stable financial results.

Thus, when periodic sales data raises questions about Great Wall's decline, the company has consistently countered with positive financial growth to disprove doubts and validate its strategy.

However, will things change in 2026?

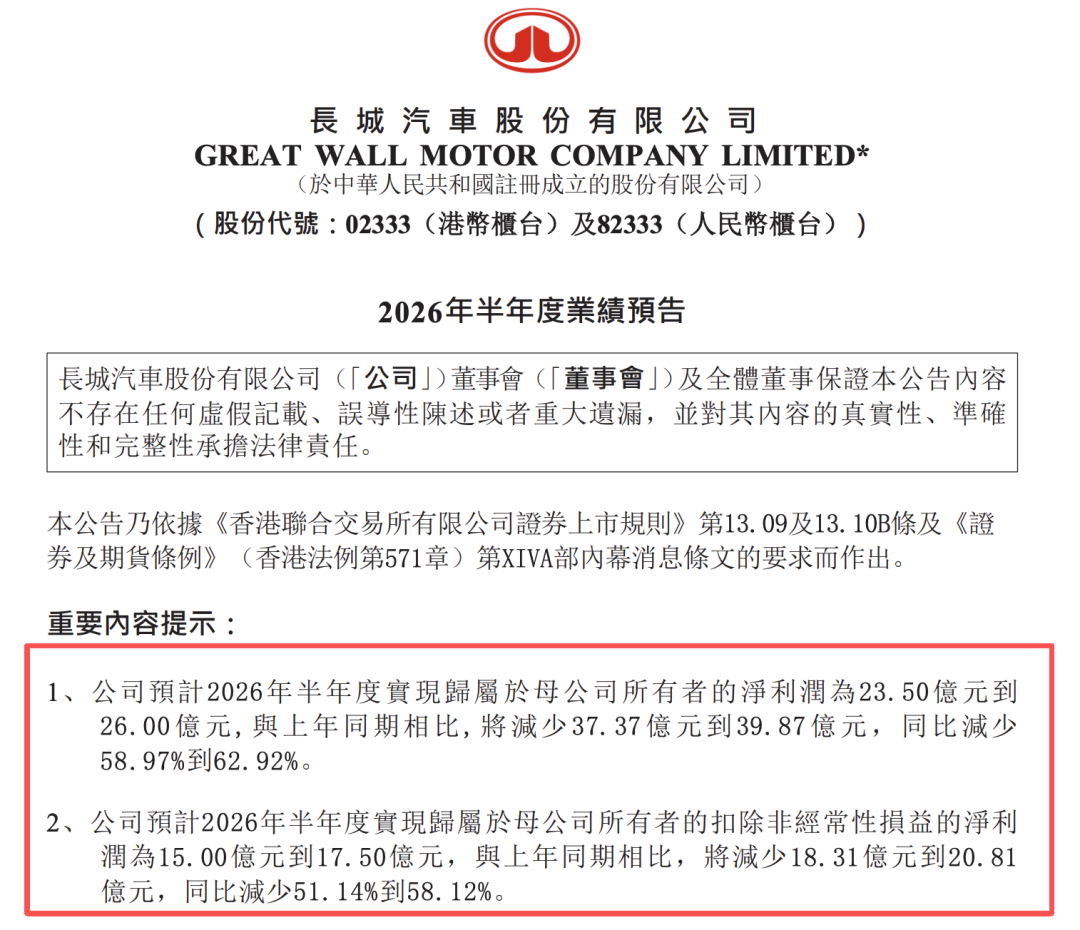

On July 14, 2026, the performance forecast released by Great Wall Motor showed that the net profit attributable to the parent company for the first half of 2026 was expected to be between RMB 2.35 billion and RMB 2.6 billion, a year-on-year decrease of 58.97% to 62.92%, equivalent to a reduction of nearly RMB 4 billion in net profit. The net profit excluding non-recurring gains and losses was expected to be between RMB 1.5 billion and RMB 1.75 billion, a year-on-year decrease of 51% to 58%, representing a reduction of RMB 1.831 billion to RMB 2.081 billion.

Great Wall Motor explained in the announcement that the main reasons for the profit decline were the delayed recovery of overseas tax policy subsidy benefits (RMB 2.274 billion received in the same period last year) and the impact of exchange rate fluctuations, resulting in a comprehensive exchange loss of approximately RMB 266 million in the current period. However, a decline in profits is still a cause for concern.

Wei Jianjun, Chairman of Great Wall Motor, remained 'calm.' In his view, short-term book data is less important than the long-term healthy development of the enterprise. He stated that the company's sales volume and operating revenue increased year-on-year in the first half of the year, with outstanding performance overseas, an increased proportion of high-value models, and continuously enhanced global brand influence.

In other words, Great Wall Motor will not dress up its profit performance just to 'make the financial statements look good.'

Indeed, in terms of sales volume, Great Wall Motor's cumulative sales volume in the first half of 2026 was 583,900 vehicles, a year-on-year increase of 2.48%. Among the performances of the five major sub-brands, Haval, WEY, and ORA all achieved positive growth, while Great Wall Pickup and TANK brands experienced year-on-year declines. The TANK brand delivered a cumulative total of 93,000 vehicles in the first half of the year, a year-on-year decrease of approximately 10%.

In overseas markets, Great Wall Motor sold a cumulative total of 291,000 vehicles in the first half of the year. From the perspective of sales structure, the sales volume ratio of Great Wall Motor's domestic and overseas markets was almost 5:5, indicating that Great Wall Motor can indeed operate on both fronts with a stable and healthy structure without relying solely on the domestic market. Looking back at its performance over the past few years, it is precisely Great Wall Motor's steady progress overseas that has, to a certain extent, offset the pressure of 'involution' in the domestic market, and this momentum continues today.

However, what Great Wall Motor should be wary of is that compared to several other leading independent brands, its competitiveness in terms of overall scale may face further risks of decline.

The good news is that in the second half of the year, Great Wall Motor will launch several heavyweight new models, including the all-new TANK 300, which has already started pre-sales, as well as highly anticipated new models such as the Great Wall H10 and WEY V9X, which will be launched successively.

Looking ahead, in the view of

5. Seres: Temporary Troubles

On July 13, Seres also released its semi-annual performance forecast, expecting a net loss attributable to the parent company of RMB 1.5 billion to RMB 1.8 billion for the first half of 2026, with a net loss excluding non-recurring gains and losses of RMB 2.2 billion to RMB 2.5 billion; its core subsidiary, AITO, is expected to incur a loss of RMB 1.05 billion to RMB 1.3 billion in the first half of the year.

This company, which was one of the most successful automakers in the past few years, faced the dilemma of turning from profit to loss in the first half of 2026.

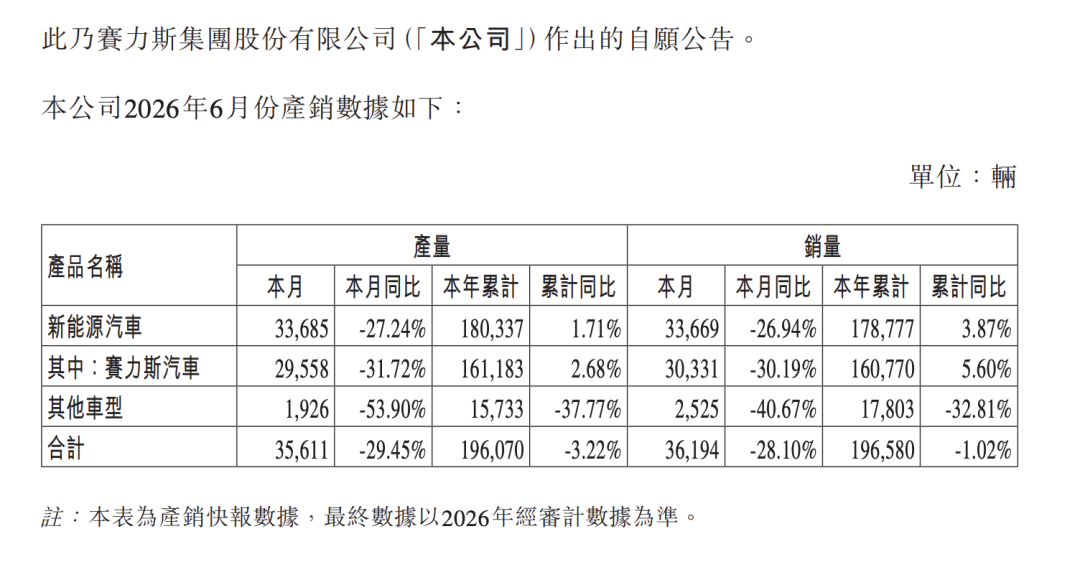

However, if we shift our focus from the financial statements back to sales volume, Seres is one of the few companies in the automotive market that has maintained growth. From January to June this year, Seres' cumulative sales volume of new energy vehicles was 178,800 units, a year-on-year increase of 3.87%; among them, Seres' (AITO brand) sales volume was 160,800 units, a year-on-year increase of 5.6%.

At the product level, Seres continues to make efforts in high-end products. In June, the AITO M9 sold 10,070 units, reclaiming the top spot on the domestic large SUV sales chart and establishing a firm foothold in the market for models priced above RMB 500,000. The sales pillar, the all-new AITO M6, is also rapidly increasing in volume, with cumulative deliveries exceeding 30,000 units in just 54 days since its launch. However, at the same time, the sales volumes of the older models, the M7 and M5, continue to decline, indeed posing certain pressure on overall sales growth.

In fact, within the Hongmeng Intelligent Mobility Alliance, AITO remains an irreplaceable sales pillar. Among the 'Five Brands,' AITO accounts for approximately 60% of the alliance's total sales volume. However, compared to the goal set at the beginning of the year of selling 1 million to 1.3 million vehicles annually under the Hongmeng Intelligent Mobility brand, the completion rate in the first half of the year was only 18.5% to 24%, indicating significant pressure for the second half of the year.

From the performance forecast and sales statistics, it is not difficult to see that Seres is currently facing a classic double dilemma: sales growth and profit losses.

However, in the view of

Therefore, balancing sales volume and profit will be the core challenge that Seres needs to address to the outside world in the second half of the year. In the second half of the year, amid challenges from brands such as NIO, Li Auto, and Zeekr, which are all focusing on the high-end SUV market, whether the AITO M9 can continue to deliver outstanding performance and reflect it on the profit and loss statement is also worth paying attention to.

Finally

In the future, traditional independent brands may present the following competitive landscape: Geely and BYD will continue to vie for the position of 'top dog' in the domestic market, while Chery will focus on overseas markets to counter BYD's relentless advance. However, ultimately, BYD will achieve a greater balance between domestic and overseas markets, while Geely will establish itself overseas with high-end brands such as Zeekr as its core. Great Wall Motor and Chery may find themselves in a defensive battle for domestic market share.

In the second half of the year, traditional mainstream independent automakers will find themselves engaged in two battlegrounds: one is the intense close-quarters combat in the domestic market, and the other is the competition for growth rates and market Layout (which means 'layout' or 'strategic positioning') in overseas markets.

*The featured image is generated by AI.

-

![]()

Breaking Through the US Blockade! Huawei Mobile Phones Now Support 5G Overseas

-

Help! The Price Has Crashed So Badly That I Just Want to Close My Account!

-

Investing in 'old established players' rather than 'new upstarts' is more reliable in the current NEV market

-

![]()

StepFun: A Smartphone You Can't Buy Yet, and a Story That Must Be Told

-

![]()

Mid-Game Battle of Chinese Automakers: Collective Overseas Expansion for Growth? | Halftime Whistle ②

-

![]()

VOYAH CBO Declares: To Ascend to TOP 3 in Luxury BEV Market Within Two Years, Launch 4 New Models Across All BEV Segments | Mingjing Pro

-

![]()

Rising Against the Tide on Lock-Up Expiry Day: Zhipu's Crucial Leap Forward

-

![]()

Fast Charging vs. Slow Charging for Electric Vehicles: Which is Better for Battery Health?