Transformation Turmoil: Dealers Navigate Policy-Driven Changes in 2024

03/26 2025

03/26 2025

666

666

Introduction

Driven by both policy initiatives and market forces, auto dealers are grappling with a transformative landscape.

In 2024, China's automotive industry finds itself in the midst of an unprecedented transformation. Amidst the wave of the new energy revolution, shifting policy environments, and intensifying market competition, the sector has embarked on a profound period of adjustment.

The recently released "2024 Automobile Dealer Survival Condition Survey Report" by the China Automobile Dealers Association offers a nuanced picture of this transitional period. Despite the boost provided by the nation's "two new policies" — namely, subsidies for new energy vehicle purchases and trade-in incentives — the survival status of dealer groups has shown marked differentiation.

On one hand, new energy brands have leveraged technological innovation and policy support to achieve countertrend growth, with sales and market share continually rising. Conversely, traditional fuel vehicle brands find themselves mired in price wars, with profit margins drastically squeezed and operational pressures multiplying.

Moreover, the structural conflicts within the manufacturer-dealer relationship have become increasingly prominent, posing a significant bottleneck to further industry development. Concerted efforts from all stakeholders are urgently needed to chart a path forward.

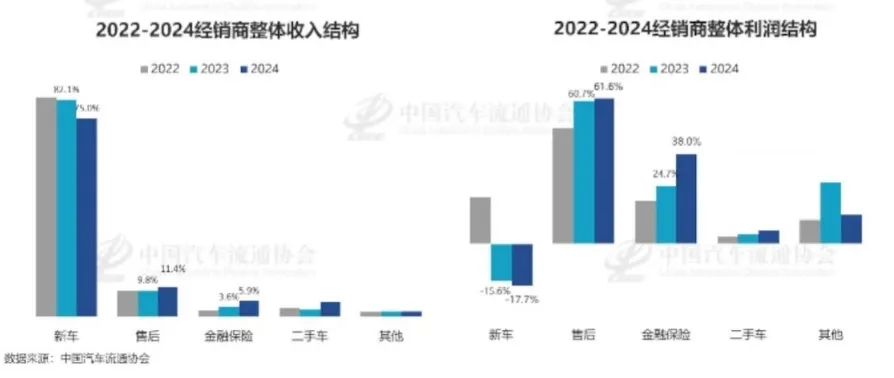

01 Differentiation in Revenue and Profit Structure

Within the traditional automobile dealership sector, core revenue streams are undergoing disruptive reconfiguration. For traditional brands, the proportion of new vehicle sales revenue has exhibited a clear downward trend, dipping from 82.1% in 2023 to 75.0% in 2024. Price wars have further contributed to a decline in profit per vehicle.

In stark contrast, new energy brands boast a new vehicle sales revenue proportion as high as 82.1%, accompanied by a substantial gross margin advantage. This disparity is primarily attributed to the premium associated with the direct sales model and technological barriers in new energy vehicle models, such as the high adoption rate of intelligent driving configurations, which directly elevates terminal prices.

However, beneath this imbalance in profit structure lies underlying contradictions. Traditional brands overly rely on after-sales business, with profits accounting for 61.6%. Nevertheless, the number of vehicle entries has decreased by 12% year-on-year, and parts inventory turnover days have extended to 45 days, exacerbating capital occupation pressure. While new energy brands enjoy a broader profit base, with 50% of dealers achieving profitability, their after-sales systems remain relatively weak.

A dealer from a new force brand revealed that its parts and service absorption rate stands at only 24.7%, with a customer return rate less than one-third that of traditional brands. The primary reasons cited are the high technical threshold for battery maintenance and the diversion of customers towards third-party services.

Additionally, price wars seem to have reached an intractable stalemate in the traditional automobile market. In 2024, over 80% of dealers encountered price inversions for new vehicles, with luxury brands particularly hard-hit.

Simultaneously, the after-sales business is contracting. The growth rate of after-sales revenue in traditional 4S stores has significantly declined, with some stores even compelled to rent out after-sales workstations to new energy brands to alleviate cost pressures.

New energy brands, too, face challenges, as insufficient after-sales loyalty represents a major issue. New energy users tend to rely more on official brand services, but the density of maintenance outlets is low, and waiting times are long, averaging 7 days, leading to substantial customer churn.

Moreover, the risk of policy dependence cannot be overlooked. The new energy vehicle purchase tax exemption policy is set to expire at the end of 2025. If not extended, it may trigger a precipitous demand drop. Dealer surveys indicate that 65% of new energy stores pin their profitability hopes on policy extensions.

Relevant personnel suggest that traditional brands explore "oil-electric synergy" by leveraging existing channel resources to introduce authorizations for new energy vehicle models, thereby reducing marginal costs. New energy brands, on the other hand, need to address their after-sales shortcomings by collaborating with third-party service providers to establish battery maintenance centers and introducing value-added services such as "lifetime free basic maintenance" to enhance customer loyalty.

02 Limited Improvement in Manufacturer-Dealer Relationships

In 2024, dealer satisfaction improved overall, reaching 75.6 points, yet this does not signify that the industry's structural contradictions have been fundamentally resolved.

Currently, dealers continue to grapple with numerous challenges. On one hand, issues such as price inversion and the bundling of unsold models are prominent. A dealer from an independent brand reported that the proportion of manufacturers forcibly bundling unsold models stands at a high 20%, extending the inventory turnover cycle to 90 days and placing immense pressure on the dealer's capital chain.

On the other hand, the rebate mechanism remains complex and unreasonable. The rebate realization cycle is elongated, and some dealers encounter deductions due to "vague clauses," resulting in the actual rebate received being lower than the promised value.

From a business segment perspective, satisfaction levels vary significantly. Satisfaction with the new vehicle business is relatively low, at only 67.8 points, primarily due to excessively ambitious task targets.

In contrast, satisfaction with financial and insurance services is higher, at 79.9 points, attributed to manufacturer discount policies. For instance, a brand launched a "0 down payment + 2-year interest-free" campaign, boosting financial penetration.

Furthermore, new energy vehicle insurance poses numerous challenges. 10.2% of new energy dealers encounter refusals to renew insurance. This is primarily due to excessively high loss ratios for some new energy vehicle models. For example, the average annual accident rate of a certain pure electric model is 1.8 times, far exceeding the 0.9 times of fuel vehicles. Additionally, insurance companies impose restrictions on vehicles used for online ride-hailing, further exacerbating this contradiction.

Simultaneously, the used car business also grapples with a lack of support. Manufacturers' investment in used car source inspection and data sharing is insufficient, leading to a high rate of misjudgment of vehicle conditions by dealers, which directly reduces transaction efficiency.

To enhance manufacturer-dealer relationships, relevant personnel propose a shift from "management" to "empowerment." Manufacturers should establish a transparent rebate system allowing dealers to query rebate progress in real-time and reduce human intervention. Additionally, opening historical data interfaces for used cars can aid dealers in setting accurate prices.

From a policy perspective, collaborative innovation is essential. Promoting a tiered pricing mechanism for new energy vehicle insurance, offering premium discounts for low-risk vehicle models such as household cars, is crucial. Moreover, extending trade-in subsidies to 2026 and expanding vehicle model coverage can propel the market towards healthy development.

Dealers generally anticipate that by 2025, the penetration rate of new energy vehicles will reach 50%-60%. However, this substantial growth is heavily reliant on policy dividends. Once subsidy policies are phased out, there may be a demand contraction in the mid-to-low-end market. Therefore, automakers must accelerate the pace of technology cost reduction, such as promoting the large-scale application of lithium iron phosphate batteries, to solidify the market foundation and ensure the industry's sustainable development.

2024 marks a pivotal juncture for the transformation of China's automobile dealers. While the rise of new energy brands has injected new vitality into the industry, the survival anxiety of traditional brands and the entrenched contradictions within the manufacturer-dealer relationship still necessitate a systematic solution. Moving forward, only by abandoning the zero-sum game mindset and prioritizing data transparency, policy coordination, and service innovation to foster a "symbiotic and win-win" ecosystem can the Chinese automobile circulation industry advance towards a new era of high-quality and sustainable development.

Editor in charge: Yang Jing, Editor: Chen Xinnan

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving