Growth Illusion and Undercurrents: Behind the 66% Growth, Insta360's 'Prosperity Dilemma'丨A-Share Avoidance Guide

07/01 2026

07/01 2026

461

461

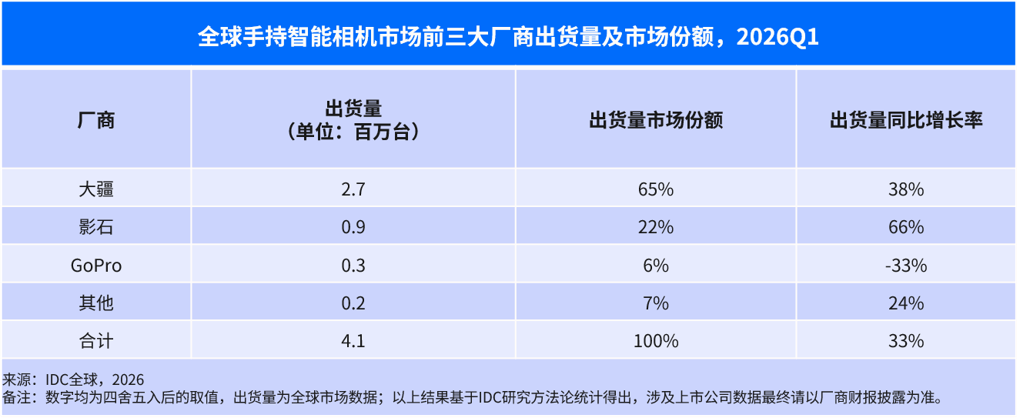

On June 25, 2026, IDC released data that briefly excited investors in Insta360 (688775.SH): In the global handheld smart camera market in Q1 2026, Insta360's shipments grew by 66% year-on-year, the highest growth rate in the industry, securing a solid second place with a 22% share. However, flipping this 'report card' revealed another set of numbers—DJI held a 65% share, Insta360 22%, and GoPro 6%, with DJI's shipments three times those of Insta360. While Insta360's revenue in Q1 2026 surged by 83% year-on-year, net profit attributable to the parent company plunged by 52%, leaving a net profit margin of just 1.31%.

Over the past year, DJI and Insta360 have shifted from 'niche competition' to 'full-scale confrontation.' Insta360's foundational segments of panoramic and thumb cameras were targeted by DJI's Osmo 360 and Osmo Nano, each delivering a costly blow. Insta360's counterattacks in drones and gimbals clashed with DJI's cash cows and flight control strongholds, cultivated over eight years. This is an asymmetric war, and Insta360 is sliding from a 'high-growth star' to a 'revenue-growing but profit-shrinking commodity.'

01

The Base Illusion of 66% Growth: The Gap Between Second and First Place Is a Chasm

IDC's latest 'Global Handheld Smart Camera Market Tracker Report for Q1 2026' reveals that Insta360's 66% year-on-year growth in Q1 2026 was indeed the highest among the top three, with its share increasing by 4 percentage points to 22%. However, examining absolute values paints a different picture: DJI shipped 2.7 million units, capturing a 65% share (+38% year-on-year); Insta360 shipped 900,000 units, holding a 22% share (+66% year-on-year); and GoPro shipped 300,000 units, securing a 6% share (-33% year-on-year).

While Insta360's growth rate exceeded DJI's by 28 percentage points, its absolute shipments were just one-third of DJI's. More critically, the product mix—IDC disclosed that Q1 2026 shipments of detachable action cameras (i.e., 'thumb cameras') surged by 350% year-on-year, over 20 times the growth of non-detachable models (Ace Pro 2's category, +16%). In this booming segment, DJI's Osmo Nano became a bestseller after its launch, capturing over 50% of the market share in Q1 2026 and reaching the top spot in less than two quarters.

In other words, Insta360's 66% growth stemmed from two moderate-growth segments: panoramic cameras (its core business) and the Ace Pro 2 street photography kit (non-detachable action cameras, 17% share, +7 percentage points year-on-year). Meanwhile, the industry's primary growth drivers—thumb cameras (+350%) and gimbals (dominated by DJI)—either saw Insta360 suppressed by DJI (thumb cameras) or entering as a latecomer (Luna Ultra gimbal).

02

Revenue Growth Without Profit: 83% Revenue Surge Fails to Boost Profits

If market share can be excused by 'youth and rapid growth,' financial data is harder to gloss over.

Insta360's 2025 annual report and Q1 2026 earnings release painted a grim picture for the market:

Metrics

2025

YoY

2026Q1

YoY

Revenue

RMB 9.741 billion

+74.76%

RMB 2.481 billion

+83.11%

Net Profit Attributable to Parent

RMB 929 million

-6.62%

RMB 84.6 million

-52.02%

Core Net Profit Attributable to Parent

RMB 850 million

-10.09%

RMB 62 million

-61.27%

Gross Profit Margin

45.74%

-6.46 percentage points

45.20%

-7.73 percentage points

Net Profit Margin

9.10%

-8.75 percentage points

1.31%

-11.7 percentage points

Data Source: Wind

While Insta360's Q1 2026 revenue doubled (+83%), net profit attributable to the parent company halved (-52%), with core profits plummeting even further (-61%). The gross profit margin collapsed from 52.93% to 45.20%, a 7.73-percentage-point drop indicative of a 'price war bloodbath' in consumer electronics. The company attributed this to 'rising storage component costs, intensified market competition, and increased R&D investment,' but a closer look reveals starker issues.

• Costs: Q1 2026 operating costs surged by 113.18% year-on-year to RMB 1.36 billion, far outpacing revenue growth (83%). Direct materials' share of imaging equipment costs rose by 2.78 percentage points year-on-year.

• R&D: Full-year 2025 R&D investment reached RMB 1.649 billion (~17% of revenue), with Q1 2026 R&D expenses doubling year-on-year to RMB 465 million.

• Pricing: To counter DJI's Osmo 360, Insta360 slashed the X5's price by RMB 500 to RMB 3,298 in April 2026, squeezing profit margins from both ends.

Insta360's shareholder letter blamed profit declines on 'aggressive R&D investment'—a half-truth. While R&D is offensive, the 7.73-percentage-point quarterly drop in gross profit margin reflects defensive failures. DJI's Osmo 360 priced at RMB 2,999 (RMB 800 cheaper than the X5) and Osmo Nano at RMB 1,998 (RMB 1,698 after subsidies, nearly RMB 1,000 cheaper than the GO Ultra) forced Insta360 to choose between price cuts or market share losses—both paths erode margins.

Insta360's Q1 2026 net profit margin of 1.31% means that for every RMB 100 in sales, just RMB 1.3 reaches shareholders. For context, mature consumer electronics firms typically maintain net profit margins of 15–25%, rarely dipping below 5% during aggressive expansion. At 1.31%, this is no longer a 'growth-phase trait' but a 'price war meat grinder.'

03

Moats Being Breached: Panoramic, Thumb, and Gimbal Segments Under Siege

Insta360's decade-long story is clear—it rose on panoramic cameras (global leader), defined the thumb camera category with its GO series, entered traditional action cameras via the Ace series, and ventured into gimbals with the Luna series. However, over the past 12 months, DJI has pried open these moats using product, pricing, and accessory ecosystem strategies.

Panoramic Cameras: 'Paper-Stable' 68% Share

Insta360 held over 68% of the panoramic camera market in Q1 2026, up from 2025, appearing stable. But DJI's Osmo 360, launched in July 2025 and priced at RMB 2,999 (vs. the X5's RMB 3,798), forced Insta360 to cut the X5's price by RMB 500 to RMB 3,298 in April. Critically, DJI equipped the Osmo 360 with a custom square sensor, offering nearly 70% more usable pixels than the X5—a supply chain and component-level advantage that software stitching algorithms cannot match.

Insta360's 68% panoramic share relies on the X4/X5 generations, but if DJI refines the 'custom sensor + ecosystem' combo, further share gains are questionable.

Thumb Cameras: Insta360's Pioneered Category, DJI's Nano Raids

Thumb cameras (detachable action cameras), nurtured by Insta360's GO series, surged by 350% globally in Q1 2026—the fastest growth among all segments. Yet DJI's Osmo Nano captured over 50% of this market in Q1 2026, dominating Insta360's GO Ultra.

DJI's strike was precise:

• Pricing: Nano priced at RMB 1,998 (RMB 1,698 after subsidies) vs. the GO Ultra's HKD 2,339/TWD 13,980 (~RMB 2,100+), nearly double the price.

• Accessories: Nano compatible with Action series accessories, while Insta360's 'per-generation interface changes' force new accessory purchases—DJI exploited this 'accessory tax' model via ecosystem binding.

• Specs: Nano (1/1.3") vs. GO Ultra (1/1.28") sensors are similar, but the Nano offers 10-bit color output and horizon correction, delivering sharper image quality.

• Weakness: The Nano overheats after 20 minutes (vs. the GO Ultra's minimal overheating), but its pricing makes heat tolerance a negotiable flaw.

Insta360 pioneered the thumb camera category, but pioneers don't always defend it. DJI's 'Action ecosystem reuse + 30% price cut' combo propelled the Nano to over 50% market share in Q1 2026—the first substantive reversal in Insta360's foundational segments (panoramic + thumb).

Gimbals: Luna's Counterattack Clashes with DJI's 8-Year Cash Cow

Insta360 launched the Luna Ultra gimbal in June 2026 to challenge DJI's Pocket series, offering 8K Leica dual cameras, modularity, and an AI Cameraman concept. DJI retaliated five days later with the Pocket 4P, priced RMB 200 lower than the Luna at RMB 3,799, engaging in head-to-head competition.

DJI's Pocket series, cultivated over eight years with over 10 million units shipped, is no battleground Insta360 can dislodge with a single Luna model. Critically, Insta360 seeks gimbals for 'new growth,' while DJI defends them as 'cash cows'—their investment urgency differs in magnitude.

Drones: Yingling's Breakout or Bleeding?

Insta360 launched the 'Yingling Antigravity' panoramic drone in July 2025, its boldest counterattack against DJI—directly infiltrating DJI founder Frank Wang's nearly two-decade-old flight control and imaging stronghold. In March 2026, DJI sued Insta360 in Shenzhen Intermediate Court, alleging that six drone patents (flight control, airframe structure, image processing) were Service invention (work-for-hire inventions) by former employees and thus owned by DJI.

This move is harsher than product competition: if valid, Yingling's core patents belong to DJI.

04

Insta360's Gamble: Trading Profits for Territory on DJI's Chessboard

Insta360's current predicament unfolds as follows:

• Impressive Growth but Small Base: 66% growth built on 900,000 units/quarter, suppressed by DJI's 2.7 million units in the same segment.

• Accelerating Financial Bleeding: Q1 2026 net profit margin of 1.31%, a 7.73-percentage-point quarterly drop in gross profit margin, burned by R&D, storage costs, and price wars.

• Segmental Moats Breached: Panoramic cameras face Osmo 360's sensor-level disruption; thumb cameras ceded to Nano's pricing and ecosystem (50%+ share); gimbals clash with DJI's 8-year Pocket dominance.

• Asymmetric Counterattacks: Insta360's forays into DJI's core domains (drones, gimbals) play to DJI's home-field advantage, while DJI targets Insta360's cash flow segments (panoramic, thumb, action cameras).

IDC projects global handheld smart camera shipments to reach 40 million units by 2030, with a 5-year CAGR of 18%—the market is fine, but growth ≠ universal prosperity. In the same IDC report, DJI + Insta360's combined share hit 87%, up 13 percentage points, carved from GoPro and smaller players. Once GoPro is exhausted, the next 13 percentage points will come from Insta360.

Insta360's shareholder letter attributes profit declines to 'aggressive R&D'—a narrative the market temporarily buys (2025 R&D: RMB 1.649 billion; Ace series revenue quadrupled in a year; Luna and Yingling newly launched). But at 1.31% net profit margin, the company has no margin for error: any further misstep could shift profits from 'halved' to 'loss-making.'

Insta360's real danger isn't being eliminated but being systematically dismantled by DJI's full-category layout (layout), supply chain cost resilience, and patent thickness. DJI copies Insta360's foundational segments one by one while using patent litigation to block Insta360's sole breakthrough direction (drones). Under this strategy, 'second place' is riskier than 'third'—the leader won't ally with you, and GoPro (the third) lacks the energy to bite you, but GoPro's today could be your tomorrow.

'Handheld smart camera penetration remains low, with promising future growth'—true for all players, but for Insta360, 'growth space' and 'how much you capture' are two different questions. DJI's 65% share, full-industry-chain migration capability, and Osmo Nano's 50%+ quarterly flash strike in the thumb segment have split 'growth' and 'market share' into separate realities: the industry may grow 33%, but you can grow 66% while your net profit margin collapses to 1.31%.

This is the question Insta360 must answer behind Q1 2026's 'impressive data.'

- END -

-

![]()

Avita Reapplies for Listing: Reports 25.6 Billion Yuan in Revenue and 3.49 Billion Yuan in Net Loss for the Previous Year, with 182 Million Yuan in Dividends from Yinwang | MIRROR Pro

-

![]()

DataStory's Controversial Hong Kong IPO: 5 Billion Valuation Hangs in the Balance Amid 866 Million Debt Pressure

-

![]()

Apple’s Prices Skyrocket Up to 3,500 Yuan! Who Empowered Cook to Hike Prices?

-

![]()

ByteDance Executives Go Viral!

-

![]()

ByteDance Executives Dominate Headlines!

-

![]()

Perspective | An Ke Cashes Out from the Computing Power Support Sector Under His Flagship, Jin Jing New Energy Faces Four Real Challenges in Its HK$2.5 Billion Acquisition

-

![]()

Selling Cars No Longer Profitable: Guanghui Transforms into a 'Landlord'

-

![]()

Anchoring Physical AI, Momenta Passes Public Verification