Sino-US Autonomous Driving Divergence: Overseas Authoritative Index Reveals True Track Gaps

06/26 2026

06/26 2026

454

454

【Introduction】The latest four real-time indices from Road to Autonomy reveal Waymo slightly leading in the passenger-carrying Robotaxi track, while Chinese companies achieve global dominance in the unmanned delivery RoboVan track. Neolix tops the delivery robot rankings, with Meituan firmly positioned at the forefront, earning overseas institutional recognition for their commercialization capabilities. However, behind the impressive deployment data, structural gaps in foundational technologies, long-term R&D, and global rule-making influence cannot be overlooked.

The autonomous driving industry has long lacked a neutral, dynamic evaluation system based on real operational data. Companies primarily focus on test mileage and demo videos in their external communications, while hardcore metrics like commercial orders, cross-regional operations, and safety compliance are rarely benchmarked horizontally, leaving the industry comparison rife with information gaps.

In June 2026, U.S. industry research institute Autnmy AI updated its full suite of real-time Road to Autonomy indices. Developed by Grayson Brulte, proponent of the 'Autonomous Economy' theory, with data accounting (calculation) by S&P Dow Jones, these indices update every 12 hours. Scores rely solely on regulatory disclosures, corporate financial reports, and compliance records, excluding manufacturer self-reported materials. Bloomberg, TechCrunch, and other overseas media regularly cite these rankings as industrial benchmarks.

The indices are divided into four tracks: passenger Robotaxi, last-mile unmanned delivery RoboVan, mainline heavy trucks, and intelligent driving software licensing. The rankings reveal a clear differentiation: the U.S. maintains a comprehensive scoring advantage in Robotaxi and mainline heavy trucks; last-mile unmanned delivery becomes China's sole global leader, with Neolix and Meituan both ranking top-tier; the intelligent driving licensing track sees Sino-US firms evenly matched.

On one hand, Chinese companies leverage domestic markets to achieve scaled commercialization; on the other, U.S. giants hold foundational general-purpose technologies and long-term R&D funding. Competition between these two approaches has entered a substantive divergence phase.

Why This Index Holds Industrial Reference Value

Before dissecting the rankings, we must clarify the index's uniqueness—the core reason for its objective conclusions. First, it is one of the few global commercialization-oriented quantitative rankings for autonomous driving. Most industry rankings emphasize laboratory technical parameters, whereas Road to Autonomy's four indices primarily assess real-world deployment capabilities: fleet scale, paid order volume, cross-city operational licenses, commercial partnership ecosystems, and long-term safety incident records, better reflecting true industrial competitiveness.

Second, it boasts official financial institution endorsement with high data credibility. In 2023, the index partnered with S&P Dow Jones for unified data validation and distribution, becoming a core indicator for Wall Street institutions tracking the autonomous driving industrial chain (supply chain). This is not a niche self-media ranking.

Third, it comprehensively covers all autonomous domains, aligning with the Autonomy Economy theoretical framework. Founder Grayson Brulte argues that autonomous driving merely pioneers the autonomous economy, with last-mile delivery, mainline freight, and industrial autonomous equipment forming the long-term industrial core. The four sub-rankings fully cover mobility and logistics—two central scenarios—enabling a complete reflection of Sino-US industrial landscapes.

China's Strength Lies in Last-Mile Urban Delivery, While Robotaxi Still Slightly Lags

1. Robotaxi: Waymo Ranks First Overall, Chinese Firms Lead Second Tier

Latest top five scores: Waymo 81.2, Baidu Apollo Go 78.1, Pony.ai 61.8, WeRide 54.3, Tesla 42.6. Among 16 ranked companies, six are Chinese, including Baidu, Pony.ai, WeRide, Caocao Chuxing, Didi, and XPeng.

Waymo's slight lead stems from over a decade of native L4 technology accumulation. Its self-developed full-stack perception hardware, long-term global road safety database, and balanced commercialization across multiple U.S. cities yield higher scores in unrestricted general autonomous driving dimensions.

However, Chinese frontrunners are closing the gap rapidly. Baidu trails Waymo by just 3.1 points, with rankings susceptible to real-time changes. Baidu Apollo Go accumulated millions of fully driverless trips in Q1 2026, peaking at 350,000 weekly orders in March, with a 3,500-vehicle fleet covering 11 domestic cities and 300 million accident-free kilometers. It recently secured L4 operational licenses in Abu Dhabi and Switzerland, becoming the only L4 firm with multi-regional commercialization across Asia, the Middle East, and Europe. Pony.ai advances further in commercial profitability, achieving positive per-vehicle daily cash flow in Guangzhou and Shenzhen fleets, targeting 3,000 global vehicles by year-end, with regular Robotaxi services launched in Croatia and Qatar. WeRide diversifies into passenger transport and logistics, using multi-channel monetization to hedge against single-track cyclical fluctuations.

Overall, Chinese Robotaxi firms excel in large-scale urban deployments, supply chain cost control, and emerging market expansion speed. Future global competition hinges on achieving replicable profit loops at the lowest compliance costs, rapid scaled deployments, and building risk-resistant global operational networks.

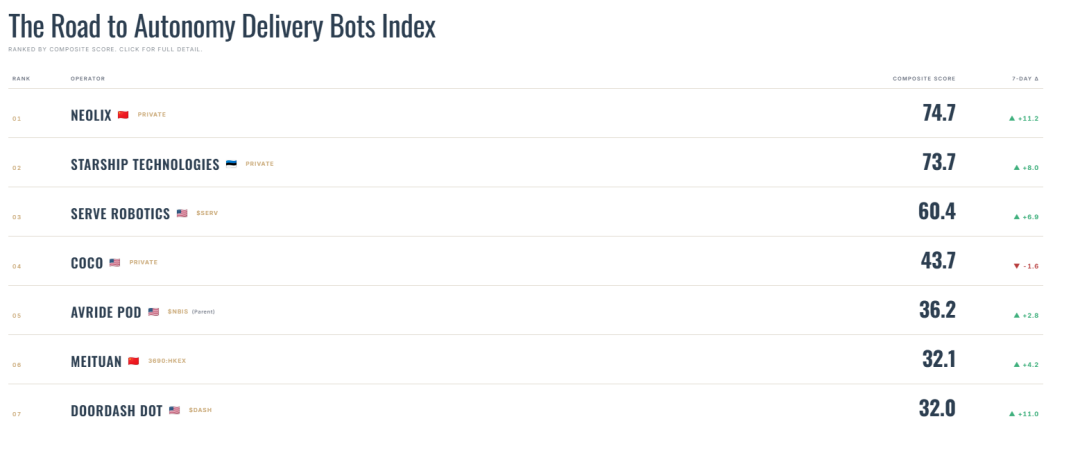

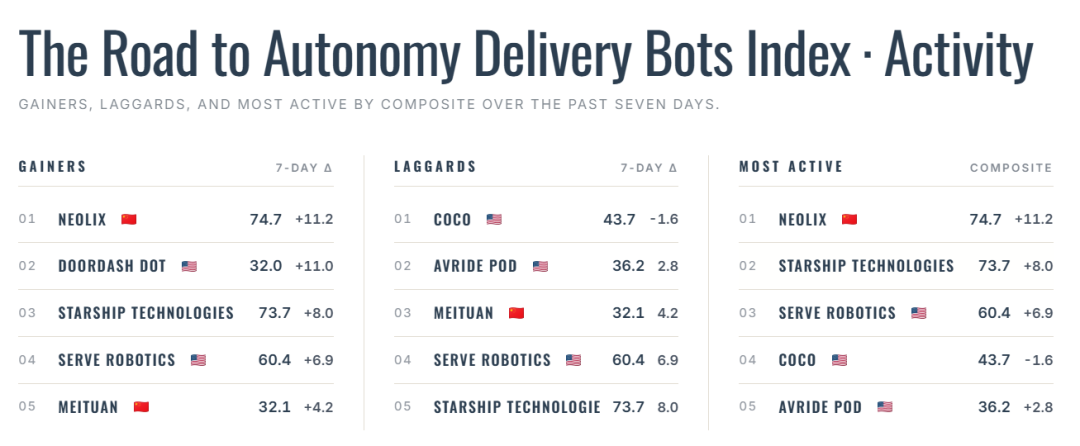

2. Unmanned Delivery: Chinese Firms Lead, Neolix Dominates Globally

This index highlights China's strongest industrial advantage. Full top-seven rankings: Neolix 74.7, Starship 73.7, Serve Robotics 60.4, Coco 43.7, Avride Pod 36.2, Meituan 32.1, DoorDash Dot 32.

Neolix's weekly score surged 11.2 points—the highest increase (increase) in the rankings—creating a clear lead over second-place Starship and rewriting global unmanned delivery competition. Hard data shows Neolix's L4 delivery vehicles surpassing 160 million cumulative kilometers, operating in nearly 20 countries and over 300 cities. In 2025, domestic unmanned urban delivery vehicle sales reached 22,000 units, with Neolix commanding over 51% market share. Commercially, while the industry adopts one-time vehicle sales, Neolix pioneered RaaS (Robots-as-a-Service) subscription models, providing on-demand delivery capacity and significantly lowering barriers for retailers and couriers. This stable recurring revenue drove its score surge. Recent global expansions include securing the Middle East's first unmanned delivery commercial license, planning 10,000 vehicle deployments in the UAE by 2026, and partnering with Singapore's QuikBot in June to launch the world's first 'public road-to-building delivery' end-to-end solution, addressing last-mile gaps. Its go overseas (overseas expansion) strategy synchronously leverages domestic cloud computing, in-vehicle mapping, and charging infrastructure chains for efficient localized adaptation, far outpacing Western rivals.

Meituan ranks sixth globally with 32.1 points, the only platform deploying both ground autonomous vehicles and low-altitude drones. Leveraging China's vast instant retail order pool, it minimizes vehicle idle rates, with regular operations in dozens of domestic cities, 53 commercial drone routes, and Dubai drone BVLOS (Beyond Visual Line of Sight) operational qualification , forming a multi-regional presence across mainland China, Hong Kong, and the Middle East. Unlike pure hardware firms, Meituan coordinates autonomous delivery with human riders, achieving superior commercial efficiency compared to overseas rivals like DoorDash.

Conversely, overseas players like Starship remain confined to campus closed areas, while Serve and Coco lag in fleet scale and open-road operational mileage versus Neolix. Backed by China's RMB1 trillion-scale instant retail market and low-cost supply chains, last-mile delivery has become China's benchmark autonomous driving export sector.

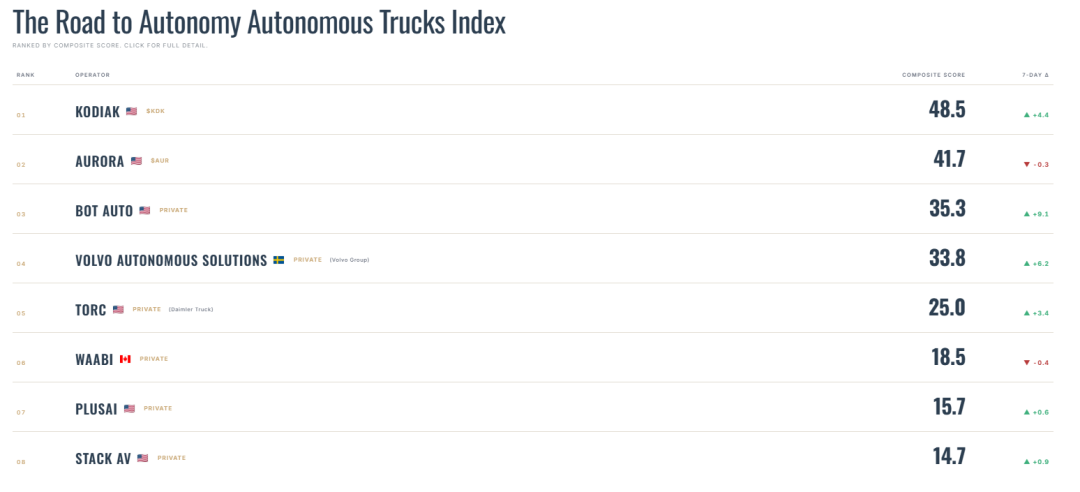

3. Mainline Autonomous Heavy Trucks: U.S. Firms Maintain Absolute Lead

The mainline heavy truck index ranks Kodiak and Aurora first and second. North America's mature long-haul freight market, standardized highway conditions, and sustained capital investments enable U.S. firms to achieve profitability first—the most pronounced Sino-US gap among the four tracks.

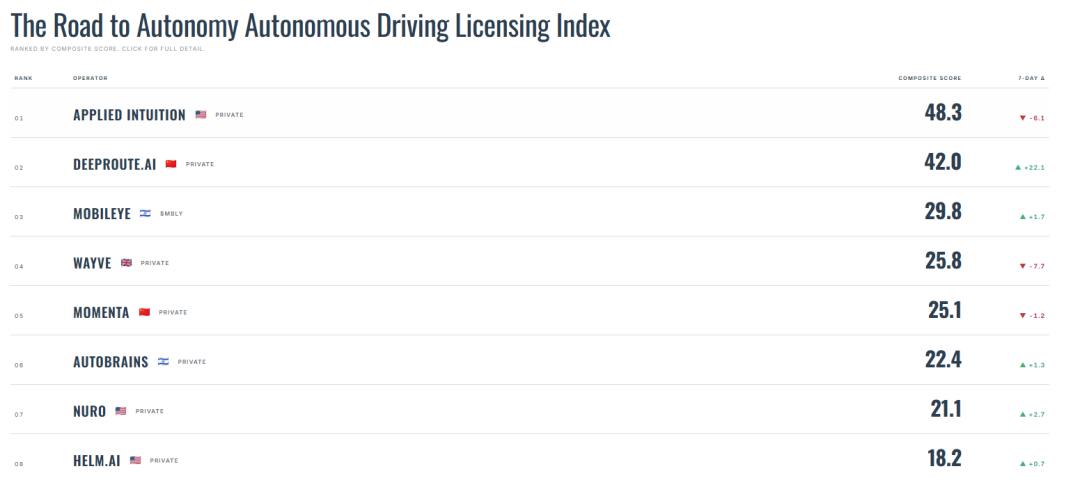

4. Intelligent Driving Software Licensing: Sino-US Evenly Matched

U.S.-based Applied Intuition ranks first, with China's DeepRoute and Momenta placing second and fifth. Domestic intelligent driving solutions have achieved scaled advantages in passenger vehicle mass production, creating differentiated competition with overseas firms.

Beyond Scores: Four Fundamental Sino-US Autonomous Driving Gaps

Rankings reflect only short-term commercialization scale. Over a 5-10 year industrial cycle, U.S. leaders retain first-mover advantages in foundational general-purpose technologies, long-term R&D funding, and global industry influence. However, Chinese firms, leveraging massive real-world scenarios, have formed irreplaceable strengths in scenario-specific technologies, mass production engineering, and multi-sensor fusion solutions—each with distinct pros and cons.

Technology Routes: Generalized Vehicle Intelligence vs. Scenario Adaptation + Mapless Approaches

U.S. firms generally pursue generalized vehicle intelligence, using a single algorithm suite for global road conditions without relying on external infrastructure. Waymo adheres to high-redundancy native L4 hardware with full self-developed perception and computing platforms, ensuring ample safety margins in extreme scenarios. Tesla's pure vision end-to-end route leverages global tens of millions of mass-produced vehicle (mass-produced vehicles) to build a boundaryless data flywheel, with algorithms adaptable to passenger, freight, and delivery scenarios, showcasing generalized capabilities.

Chinese firms explore differentiated routes for high-density cities, focusing on complex scenario adaptation and mass production engineering. Domestic Robotaxi and RoboVan firms are shifting from multi-sensor fusion + high-definition mapping to mapless technologies, leveraging vast real-world data from human-vehicle mixed traffic, narrow roads, and dense non-motorized vehicles to develop world-leading urban perception and decision-making algorithms. Baidu and Pony.ai's self-developed multimodal autonomous driving models simultaneously recognize pedestrians, e-bikes, and irregular obstacles. Neolix and Meituan develop lightweight fusion perception schemes for low-speed urban delivery, reducing hardware costs and accelerating mass production.

This localized technical approach achieves higher deployment efficiency, perfectly fitting Asia's high-density urban road networks—a technological barrier overseas firms struggle to replicate.

Long-Term R&D Funding Disparity

Foundational technology iteration demands sustained massive investments, with significant Sino-US capital gaps. Waymo, backed by Alphabet, maintains annual L4 R&D spending exceeding USD 10 billion. Tesla reinvests vehicle business profits into FSD development, with annual autonomous driving-related investments surpassing USD 5 billion, creating a self-sustaining funding loop. Delivery robot firms like Nuro and Starship secure large-scale specialized financing.

Domestic firms, whether Robotaxi or unmanned delivery players, mostly rely on group funding or Series A/B/C financing. Even with growing commercial orders, short-term revenues barely cover fleet maintenance and local operations. Long-term high-intensity R&D for foundational large models, self-developed vehicle chips, and global simulation platforms remains underfunded versus U.S. giants. However, advantages persist: domestic supply chain cost advantages significantly reduce R&D and deployment expenses, while massive local scenario data continuously feeds algorithm iteration without needing expensive overseas test networks. Meanwhile, Baidu, Meituan, and other groups steadily increase autonomous driving R&D investment, with domestic capital passion (enthusiasm) for RoboVan, Robotaxi, and Robobus sectors rising, gradually improving long-term funding supply.

Localized Pilot Profitability vs. Global Balanced Profitability

Domestic autonomous firms rely heavily on delivery service revenues, with slow progress in software technology licensing overseas. Their ranking strengths concentrate on fleet size and order volume, but profitability Balance degree (balance) requires improvement.

Neolix achieves positive RaaS revenue in core Chinese cities like Qingdao and Linyi, while Middle East and Singapore overseas pilots remain investment phases. Meituan's domestic drone routes generate slight profits, but Dubai operations sustain losses. Most Baidu and WeRide Robotaxi fleets across cities remain unprofitable. U.S. firms adopt lighter asset models: Starship and Serve achieve balanced cost reductions across multiple North American cities. Tesla secures stable software cash flow through FSD subscriptions. Waymo narrows overall losses through balanced multi-city operations.

However, Chinese companies have innovated business models to open up new profit spaces: Neolix's RaaS (Robotics-as-a-Service) capacity subscription model and Meituan's air-ground collaborative fulfillment system both align with local market demands, offering profit models better suited for emerging markets. Meanwhile, American companies have more diversified revenue structures, with hardware sales, algorithm licensing, and capacity operations all generating revenue simultaneously. There is still room for improvement in the progress of Chinese autonomous driving companies in licensing their software technologies for overseas markets.

Global regulatory environments and upstream industrial chain influence vary significantly.

Waymo and Tesla have been deeply involved in the formulation of autonomous driving regulations by the U.S. NHTSA and California DMV. Many low-speed and high-level autonomous driving rules in European and American countries heavily reference test data from U.S. companies. Overseas manufacturers still dominate core upstream technologies such as in-vehicle computing chips, underlying simulation platforms, and autonomous driving operating systems.

Chinese companies venturing overseas need to adapt to new regulatory rules in each country individually. The global export of Chinese autonomous driving standards is still in its early stages, and there is external dependence on core upstream hardware.

At the same time, China is accelerating its export of autonomous driving technologies. Companies like Neolix, Mogu Vehicle Network, and Baidu are deeply involved in the implementation of autonomous driving projects in the Middle East, Southeast Asia, and Singapore. Domestically produced LiDAR and in-vehicle computing chips have rapidly achieved commercial mass production, and the process of self-sufficiency in the upstream supply chain continues to accelerate, with the potential to gradually narrow the gap in industrial chain influence in the long term.

The industry coexists with differentiated competition, and there is no single winner.

Combining the Autonomy Economy theory behind the Road to Autonomy Index, autonomous driving is merely a precursor to the broader autonomous industry. Long-term competition will hinge on comprehensive capabilities in large-scale deployment, industrial ecosystems, and underlying general-purpose technologies. The Chinese and American approaches will coexist for a long time.

In the short term (3-5 years), China will continue to dominate the commercialization of last-mile unmanned delivery and domestic Robotaxi services. Urban delivery autonomous driving solutions represented by Neolix and Meituan will continue to capture emerging markets in the Middle East, Southeast Asia, and Eastern Europe, with RaaS subscriptions and air-ground collaborative delivery models becoming benchmarks for global short-haul logistics intelligence. Robotaxi companies like Baidu and Pony.ai will continue to narrow the rating gap with Waymo and expand into incremental markets through overseas expansion.

In the medium to long term (5-10 years), the United States will set the upper limits of general-purpose autonomous driving technology. Tesla's pure vision and Waymo's fully redundant hardware approaches will continue to iterate, pushing towards unrestricted L4 autonomous driving across all domains. Domestic scenario-based customized routes are well-suited for high-density Asian cities, but cross-regional, map-free general-purpose autonomous driving technologies still require continuous breakthroughs.

The real-time Road to Autonomy rankings provide an objective fact: at the critical stage of autonomous driving transitioning from laboratories to mass commercialization, the Chinese industry has achieved a phased lead through market and supply chain advantages, becoming the market with the fastest global deployment speed. The overseas expansion and large-scale practices of companies like Baidu, Neolix, Mogu Vehicle Network, and Pony.ai have provided a new "Chinese solution" for global autonomous driving.

However, the rankings cannot conceal the industry's deep-seated shortcomings: gaps in underlying technology, long-term R&D, and global regulatory influence cannot be bridged by short-term fleet scale alone. For the domestic autonomous driving industry, the future requires not only continuing to leverage commercialization and supply chain advantages to consolidate leadership in niche segments but also increasing investment in self-developed underlying algorithms, general-purpose large models, and core hardware to address long-term technological shortcomings. Only then can it form sustainable core competitiveness in the global autonomous economy wave.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving