Industry Insight Notes 1 | Categorization of AI Computing Power and Its Industrial Ecosystem

10/13 2025

10/13 2025

610

610

01 Computing Power and Its Categorization

AI Computing Power

Computing power denotes the capacity to perform computations. Typically, we refer to the computational prowess of chips like CPUs (Central Processing Units) and GPUs (Graphics Processing Units) as narrow computing power. Memory and hard disk storage technologies are termed storage power, while software technologies such as operating systems, databases, middleware, and applications are classified as algorithms. Broad computing power encompasses narrow computing power, storage power, and algorithms.

The essence of computing power lies in its ability to accomplish computational tasks. Systems and program software, including computers, mobile phones, servers, and data centers, rely on countless computational tasks for their operation, making computing power the driving force behind the seamless functioning of hardware systems and program software.

Computing power is a key determinant of the digital economy's growth rate and the extent of societal intelligence. According to data jointly released by IDC, Inspur Information, and Tsinghua University's Global Industry Research Institute, a one-point increase in the computing power index results in a 3.5‰ and 1.8‰ growth in the digital economy and GDP, respectively.

Computing power is quantified in FLOPS (floating-point operations per second). High-performance gaming graphics cards and AI training servers commonly use TFLOPS (trillion operations per second), supercomputers employ PFLOPS (quadrillion operations per second), and national computing power statistics are measured in EFLOPS (hundred billion billion operations per second).

Based on computational precision, ranging from low to high, computing power can be categorized into general-purpose computing power, intelligent computing power/AI computing power, and supercomputing power/high-performance computing. These correspond to data centers categorized as general-purpose data centers, intelligent computing centers, and supercomputing centers. General-purpose computing power primarily leverages the computational output of CPUs for everyday tasks like web browsing and data queries. AI computing power harnesses the computational capabilities of AI chips such as GPUs, FPGAs (Field-Programmable Gate Arrays), NPUs (Neural Processing Units), and TPUs (Tensor Processing Units) for AI training, inference, and deep learning. Supercomputing power is derived from the computational output of supercomputers, comprising tens of thousands or even millions of CPUs and GPUs, utilized in cutting-edge scientific research, national defense, and the military industry.

Based on service type, computing power can be classified into public cloud computing power, private cloud computing power, hybrid cloud computing power, and edge computing power. Public cloud computing power is accessible to the public via the internet. Private cloud computing power is typically constructed and utilized by specific organizations, such as governments, banks, and large enterprises. Hybrid cloud computing power combines public and private clouds, often placing non-core businesses on the public cloud to reduce costs and core sensitive businesses on the private cloud for enhanced security. Edge computing power deploys computing resources near the data generation source to achieve low latency and localized processing.

02 Computing Power Industrial Ecosystem and Market Scale

AI Computing Power

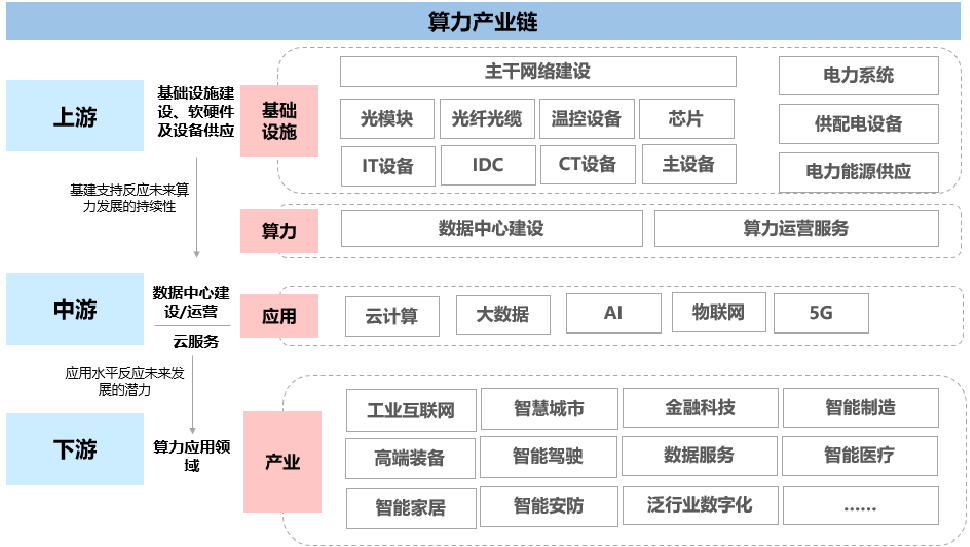

The upstream of the computing power industrial ecosystem primarily comprises IT hardware and software equipment. This includes hardware such as CPUs, GPUs, memory chips, and network devices like servers, routers, switches, and optical modules, as well as software like operating systems, databases, and middleware. Additionally, power supply and distribution facilities, including power distribution cabinets, transformers, and uninterruptible power supplies, along with cooling systems like air and liquid cooling, are vital supporting components.

The midstream encompasses computing power networks and platforms, including various data centers and operational services, cloud services, and security services based on these data centers.

The downstream comprises diverse application scenarios, such as the internet, finance, government affairs, transportation, education, industry, healthcare, and energy.

Figure: Computing Power Industrial Ecosystem

Note: The figure is sourced from the Founder Securities Research Institute.

According to data from the China Academy of Information and Communications Technology, IDC, and others, the global market size for computing power is witnessing rapid growth, expanding continuously from 232 EFLOPS in 2018 to 1,397 EFLOPS in 2023, with a CAGR of approximately 43%. It is anticipated that by 2030, the global computing power scale will exceed 16,000 EFLOPS, with a CAGR surpassing 42%. Furthermore, the global market size for computing power is projected to exceed $420 billion by 2025 and reach $1.2 trillion by 2030, with a CAGR of 16.3%. The United States and China lead the market, accounting for 32% and 26% of the global computing power market, respectively. They are followed by Japan, Germany, the United Kingdom, and Canada, with computing power shares of 5%, 4%, 3%, and 3%, respectively.

From a domestic market perspective, according to a report jointly released by IDC and Inspur Information, China's AI computing power scale reached 725.3 EFLOPS in 2024, marking a year-on-year increase of 74.1%, with a market size of $19 billion, a year-on-year increase of 86.9%. It is expected that by 2025, the AI computing power scale will reach 1,037.3 EFLOPS, a year-on-year increase of 43%, with a market size of $25.9 billion, a year-on-year increase of 36.2%. Overall, the five-year CAGR for China's AI computing power scale and general-purpose computing power scale from 2023 to 2028 is projected to reach 46.2% and 18.8%, respectively. AI computing power already constitutes 66.5% of domestic computing power, becoming the core driver of computing power growth.

END

// The editor's opinion is for reference only //

-

![]()

Enflame Tech's IPO Journey: Navigating Over 5.9 Billion Yuan in Losses and Soaring Debt in Q1 This Year

-

![]()

Trillion-Yuan Giant Li Shufu 'Streamlines': Could Levc Be the Casualty?

-

![]()

AI Competes for Electricity and Generates Power in the Gobi Desert

-

![]()

The First Batch of Victims of the AI Bubble: Programmers

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'