After a "superficial harmony" with OpenAI, is Microsoft still attractive?

10/31 2025

10/31 2025

711

711

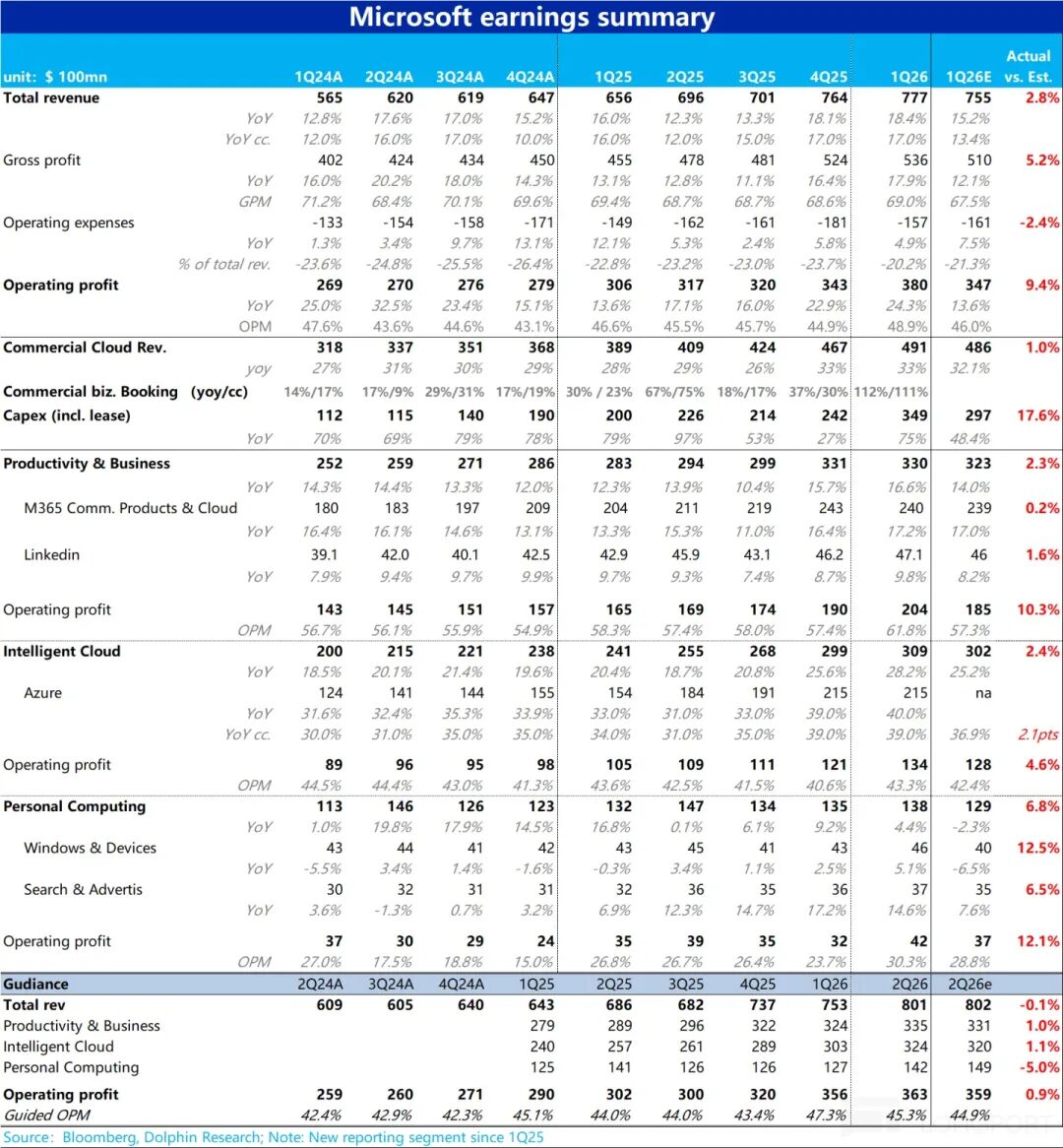

After the market closed on October 30th (Beijing Time), $Microsoft (MSFT.US)$ released its financial report for the first quarter of fiscal year 2026 ending in September. Overall, Microsoft performed well this quarter with almost no flaws, and various indicators generally exceeded expectations.

The issue lies in the fact that as the most consistently bullish target, the market has extremely high expectations for Microsoft. It can be said that a significant exceedance of expectations is required to once again surprise the market. Moreover, the core Azure growth rate this quarter did not outperform buyer expectations, resulting in a muted market reaction to Microsoft's performance this quarter.

1. No pleasant surprises from Azure: The most closely watched Azure business saw a 40% year-over-year revenue increase this quarter, or 39% excluding the impact of exchange rates, consistent with the growth rate of the previous quarter on a constant currency basis.

Although this is better than the company's guidance of approximately 37% growth on a constant currency basis, the pre-earnings sell-side expectations for Azure's growth rate had been raised to 39%-40%, while more optimistic buyer expectations were even 1-2 percentage points higher. Therefore, Azure's performance this quarter cannot be considered unexpectedly strong.

Considering that the significant exceedance of expectations for Azure in the previous two quarters was largely due to the "abnormally" strong pull from non-AI demand, and combining views from some sell-side reports, it is indeed plausible for non-AI demand to continue to rise on this basis. At the same time, the degree of binding between OpenAI and Azure has decreased, potentially weakening the pulling effect on Azure AI-related revenue. Both factors may contribute to the lack of pleasant surprises from Azure.

2. Price increases drive solid growth in the Office business: The main Office business in the productivity segment, including enterprise and consumer versions of Office 365, relied on price per unit increases to offset the slowdown in user growth this quarter, maintaining solid growth.

Specifically, the revenue from commercial Microsoft 365 cloud services, the second most important segment, increased by 17% this quarter, slightly narrowing by 1 percentage point compared to the previous quarter on both variable and constant currency bases, showing stable performance. The number of subscription seats increased by 7% year-over-year, remaining flat compared to the previous quarter. Meanwhile, the average price per unit increased by over 10% year-over-year.

Similarly, the consumer M365 business, benefiting from the first price increase for the consumer version of Office in 12 years in January this year (with an increase of approximately 30%-50%), also saw revenue growth accelerate to 28% despite the slowdown in user growth.

3. Capex surges again: Microsoft's Capex (including leasing) expenditures reached $34.9 billion this quarter, increasing by over $10 billion from the previous quarter and reaching a new all-time high. Although the market generally expected Microsoft's Capex expenditures to increase again this quarter, with expectations around $30 billion, the actual figure still significantly exceeded expectations.

In terms of structure, the company stated that nearly half of this quarter's Capex was invested in short-lifecycle equipment such as GPUs and CPUs, indicating that Microsoft has entered a peak period for chip procurement. Additionally, leasing capital expenditures were also high at $11.1 billion, a 71% year-over-year increase. For long-lifecycle assets such as data centers, Microsoft has increasingly opted for external leasing rather than self-construction.

This is a positive signal (and validation) for upstream chip companies and service providers offering data center leasing.

4. Overall revenue and profit exceed expectations: Summarizing the performance of each segment, Microsoft's total revenue for the quarter was $77.7 billion, a 18% year-over-year increase, showing a generally stable trend with a slight acceleration compared to the previous quarter. Although there were no major surprises, it significantly exceeded both the company's guidance and sell-side consensus expectations.

Profit performance was even more outstanding, with efficiency improvements and cost controls offsetting the decline in gross profit margin due to depreciation. Microsoft's overall operating profit margin increased by 2.3 percentage points year-over-year this quarter. The final operating profit was $38 billion, a 24% year-over-year increase, significantly outpacing revenue growth.

5. Leading indicators surge, but may contain "bubbles": In addition to solid quarterly performance, leading indicators showed a significant year-over-year increase of 112% in the value of newly signed enterprise contracts this quarter, driving the growth rate of the backlog of enterprise contracts to be fulfilled to 51%, an increase of $24 billion from the previous quarter.

However, although the forward-looking indicators appear very strong, this is mainly attributed to the large commitment contracts signed between OpenAI and Azure (excluding the $250 billion commitment signed a few days ago).

Considering that OpenAI has been signing large framework orders everywhere but currently has limited self-generated revenue capabilities, Dolphin remains cautious about whether these orders can be fully converted in the medium to long term and does not "take them too seriously."

6. Price increases, efficiency improvements, and cost controls jointly drive margin improvements: Despite the continuous increase in Capex, Microsoft's profit margins exceeded expectations and increased this quarter. This is attributed to recent price increases in multiple business lines, improved operational efficiency across the company with the help of AI, and effective cost controls.

Microsoft's gross profit margin was 69% this quarter, a 0.4 percentage point year-over-year decrease but 1.5 percentage points higher than Bloomberg's expectations.

At the same time, the total year-over-year increase in operating expenses was only 4.9%, continuing to narrow from 5.8% in the previous quarter and far lower than the approximately 18% growth in revenue and gross profit, resulting in a 2 percentage point year-over-year dilution in the expense-to-revenue ratio.

Dolphin's View:

1. Almost no flaws in quarterly performance

In summary, Microsoft's quarterly performance had almost no flaws. Although it can be said that there were no particularly unexpected surprises, both revenue and profit growth exceeded sell-side consensus expectations, and profit margins increased instead of decreasing, driving profit growth to outpace revenue growth.

In core businesses, Azure growth continued to accelerate slightly, while the M365 business maintained solid growth by relying on price increases to offset the slowdown in user growth. Although the forward-looking indicators contain some "water" from OpenAI, the strong growth in newly signed orders and backlog is also an objective fact.

From any perspective, Microsoft's quarterly performance had no significant flaws and still demonstrated first-class and stable delivery capabilities.

2. Steady guidance for the next quarter

Regarding performance in the next quarter, Microsoft's guidance maintains a consistently robust (steady and even somewhat conservative) attitude:

1) In terms of revenue, the company's guidance for total revenue midpoint is a 15% year-over-year increase, roughly in line with the guidance provided in the previous quarter. The guidance for growth rates in the three major segments is also generally close to the previous quarter's guidance. In other words, the company expects subsequent business growth trends to at least remain stable compared to the current situation.

2) In terms of profit margins, the company's guidance for the operating profit margin in the next quarter is 45.3%. Even according to Microsoft's conservative expectations, the operating profit margin will only narrow by 0.2 percentage points compared to the same period last year. This likely means that the actual profit margin in the next quarter will still increase year-over-year. In other words, the performance trend in the next quarter for Microsoft is likely to still involve steady revenue growth and continued outperformance in profits.

3. Forward-looking developments

1) In recent days, negotiations between OpenAI and Microsoft, a partnership with significant potential impact on the entire AI industry, have achieved important interim results. To summarize, with the cooling of relations between OpenAI and Microsoft and the absence of exclusive support from OAI, Microsoft may need to rely more on its own R&D capabilities in AI-related functions or services, similar to Google, Meta, and Amazon.

This implies that Microsoft's currently absolute leading position in the AI field for its cloud business may be shaken. This could be a somewhat negative medium to long-term signal.

Due to the extensive content involved, it is inconvenient to include all details in the summary. Please refer to the first paragraph of the main text for more information.

2) Another development affecting medium to short-term performance is that starting from the fourth quarter of fiscal year 2025 (second quarter of the calendar year), Microsoft has generally increased prices for multiple businesses by around 10%-20%. This includes PowerBI under the productivity process segment, M365 on-prem, and Dynamic 365, to offset the impact of the slowdown in seat growth for businesses like M365.

Additionally, starting in November, Microsoft has reduced the price discounts it offers to cloud business partners/distributors, which is expected to be equivalent to a double-digit percentage price increase. In other words, before the end of the price increase Dividend period (at least one year), there will be support for the growth of Microsoft's cloud computing and productivity process segments.

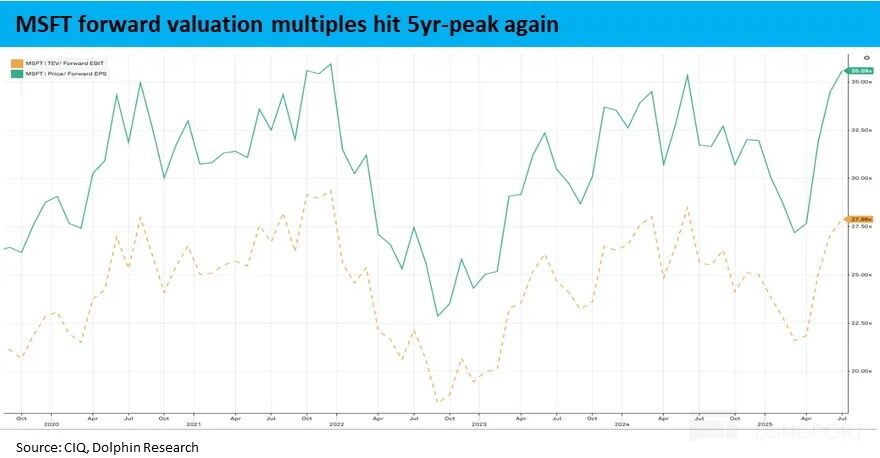

4. Valuation perspective: As seen from the chart below, over the past five-plus years, Microsoft's valuation range for forward earnings per share has fluctuated within approximately 25x-35x. During this period, overall macro sentiment, market optimism towards AI, and Microsoft's performance trends have all influenced valuation fluctuations within this range.

Directly basing on performance in fiscal year 2027 two years later and according to Dolphin's relatively optimistic profit expectations (approximately 10% higher than market consensus expectations), Microsoft's pre-performance market capitalization corresponds to approximately 30x PE. Even from this perspective, Microsoft's valuation cannot be considered cheap and undoubtedly includes a premium given by the market for Microsoft's certainty of benefiting from this round of the AI wave.

Dolphin does not intend to judge the reasonableness of this valuation level and premium; investors should consider it based on their own risk preferences. Dolphin's view is that in the medium term, Microsoft undoubtedly remains one of the companies with the highest certainty and execution capabilities in the U.S. AI industry chain.

Although its revenue and profit growth are not extremely high, they excel in being sufficiently stable and rarely disappointing in terms of delivery capabilities.

As mentioned earlier, although its original first-mover and leading advantages in the AI field obtained through OAI may diminish, at its not-low valuation, it may not be able to deliver significant outperformance compared to the market. However, for investors seeking more stability and the average return of the overall AI industry, Microsoft can still be considered one of the optimal choices.

The following is a detailed review of the financial report

I. OpenAI and Microsoft

1. What changes have been made to the new cooperation terms?

First, briefly summarize the main content and changes in the newly signed cooperation relationship between OpenAI (OAI) and Microsoft:

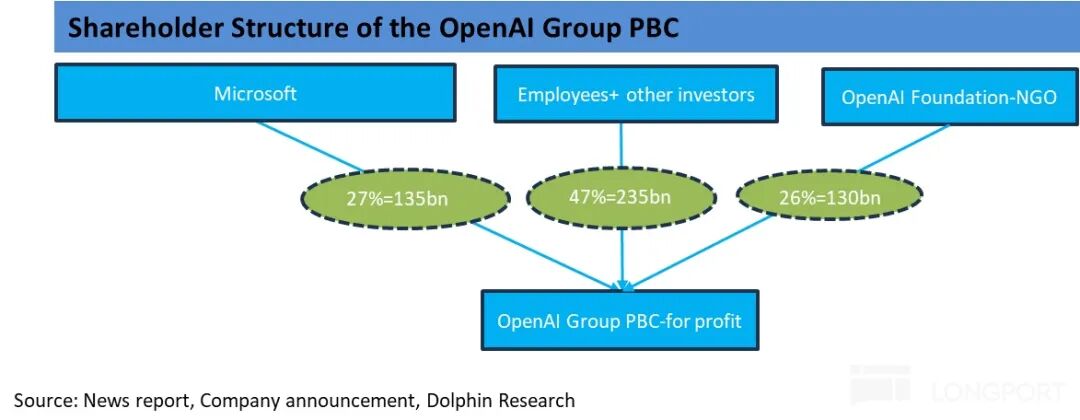

1) After transforming OpenAI's operating entity from a "limited profit" model to a for-profit public company, Microsoft holds approximately 27% of the new entity. Based on OAI's latest valuation of approximately $500 billion in the latest funding round, Microsoft has acquired shares worth approximately $135 billion and a 27% profit/loss attribution right to OAI's operating entity.

This means that under the "limited profit" model, the previous cap on the profit Microsoft could obtain from OAI, set at 8x its total investment (over $14 billion), has been lifted.

2) Microsoft's usage rights for OpenAI models have been extended to 2032, and this right will not be revoked even after the realization of AGI (Artificial General Intelligence). Under the previous contract, Microsoft did not unconditionally possess the usage rights for OAI models after the realization of AGI.

3) Both Microsoft and OAI have the right to independently or in cooperation with other third parties conduct research and development on AGI and other areas.

4) Any API functions developed by OpenAI can still only be exclusively provided on the Azure cloud platform.

5) OAI is allowed to purchase computing power from other cloud service providers, and Microsoft no longer has the right of first supply for computing power. However, OpenAI has signed a cloud service contract with Microsoft worth approximately $250 billion (duration unknown). In other words, OAI will not fully transfer its computing power demand away from Azure.

6) According to media reports, Microsoft's share of OpenAI's total revenue may have decreased from the original 20% to less than 10%. (All the aforementioned percentages are based on media reports and have not been officially confirmed)

2. What are the reasons and impacts for the "drifting apart" between Microsoft and OAI?

Expanding on this, there are two main clues behind the recent back-and-forth negotiations between OpenAI and Microsoft and the signing of this new contract: 1) OpenAI itself has the appeal (demand) to transform its operating entity from the original public welfare/non-profit organizational structure to a for-profit organization. This would facilitate subsequent financing and even going public, as well as bring more wealth benefits to its shareholders, management, and employees.

2) Dolphin believes that another reason behind the "drifting apart" between OAI and Microsoft from their previously close cooperation is the significant divergence between OpenAI and Microsoft regarding the scale and pace of computing power construction in the medium to long term.

Microsoft is not as willing to cooperate with OAI's "aggressive and optimistic" vision by extensively building the computing power facilities it needs and undertaking overly heavy Capex expenditures for OAI. (The total volume of OAI's various collaborations may exceed 30GW).

From OAI's perspective, it may criticize Microsoft for the slow pace of computing power deployment, which has become a bottleneck and drag on OAI's development. Therefore, OAI has bypassed Microsoft and directly collaborated with a series of cloud service or chip companies such as Oracle, AMD, Coreweave, Nvidia, and Broadcom, signing a series of computing power supply contracts.

With both parties having their own "hidden agendas" and mutual dissatisfaction, it is not surprising but rather expected that they are drifting apart.

3. What are the impacts of signing the new cooperation agreement?

The most obvious impact is undoubtedly that the binding between OpenAI and Microsoft is no longer as strong. Originally, OpenAI was the largest single customer for Azure AI revenue, and its subsequent contribution to Azure's revenue growth may decrease. Correspondingly, Microsoft's subsequent growth in AI-related revenue will rely more on its own capabilities, including its various Copilot businesses and the exploration of enterprise AI cloud computing demand outside of OAI.

From OAI's perspective, according to news reports, in exchange for ceding part of its interests to Microsoft, the revenue sharing ratio that OAI needs to pay to Microsoft is likely to decrease, helping OAI save a significant amount of cash flow, reportedly possibly up to $50 billion. For OAI, which has signed contracts worth hundreds of billions of dollars everywhere and is in great need of funds, this is also highly important.

4. Where is OpenAI's impact on Microsoft's financial report?

The last question is, in what ways and to what extent has the collaboration with OpenAI affected Microsoft's financial report? Let's look at it from two perspectives:

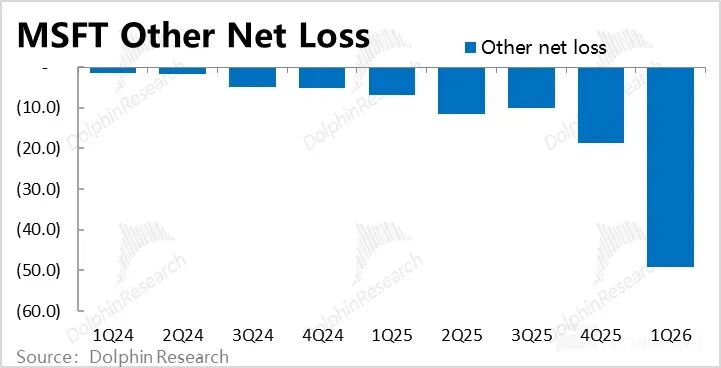

1) As one of the major shareholders of OpenAI, Microsoft should recognize the profits/losses generated by OpenAI in proportion to its shareholding. This portion is recognized in Microsoft's other gains and losses items.

After excluding the portion of other gains and losses from investment/interest gains and losses, the remaining portion saw a significant increase from a loss of just over 100 million in the two-year period from F1Q24 to 1Q26 to a quarterly loss of approximately 4.9 billion. This reflects the rapid expansion of Microsoft's recognition of OAI's losses, which has increasingly dragged down Microsoft's overall net profit.

Given that Microsoft held approximately 30% to 40% of OAI's shares at that time, it can be inferred that OAI's quarterly losses may have approached $15 billion, and are expected to continue to expand.

2) From the perspective of revenue, OpenAI's impact on Microsoft is even more complex. Firstly, the inference costs generated by OAI are recorded in Azure's revenue. The training costs of OAI are capitalized and recorded in the intangible assets on Microsoft's balance sheet, affecting Microsoft's revenue statement in the form of amortization and depreciation.

Additionally, due to the revenue-sharing agreement between OAI and Microsoft, a portion (reportedly originally 20%, which may decrease after the new contract) of all OAI's revenue is also recorded in Microsoft's revenue.

Combining external estimates, the total annualized revenue from OAI inference for Azure plus the revenue share for Microsoft (excluding Azure's own sales of OpenAI API and Copilot-related revenue) is approximately $10 billion, accounting for half or more of Microsoft's overall AI-related revenue (not just Azure AI).

It can be seen that OAI has a moderate impact on Microsoft's performance from the perspectives of revenue and profit/loss. Currently, with the relaxation of the binding between OAI and Microsoft, one of the main driving forces for Microsoft's subsequent AI-related growth, especially Azure's growth, is expected to weaken.

At the same time, the losses recorded in Microsoft's other gains due to OAI are likely to continue to increase. However, it should also be remembered that the total amount of losses recognized by Microsoft from OAI is limited to the amount of funds it has invested in OpenAI. According to previous reports, the upper limit of recognized losses may be $14 billion or more.

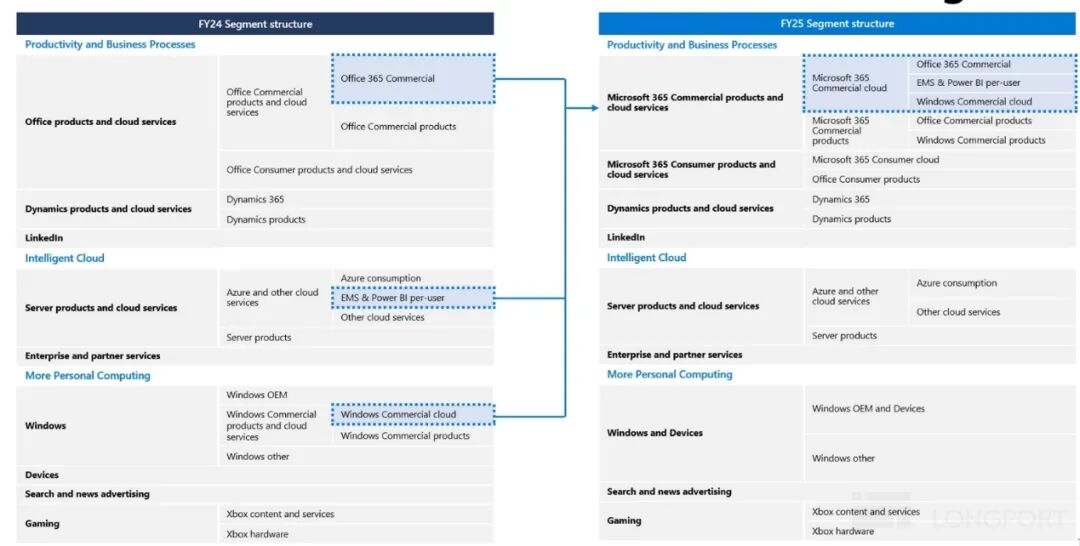

II. Overview of Changes in Financial Report Disclosure Scope

At the beginning of Fiscal Year 25, Microsoft made significant adjustments to the departmental structure of its financial report disclosures. The overall adjustment approach is to move all enterprise-oriented 365 services, including Commercial Office 365, Windows 365, and Security 365, from their original segments to the large segment of Productivity & Processes (PBP).

When the first adjustment was made in the new Fiscal Year 25, Dolphin Research provided a relatively detailed interpretation, so we won't repeat it in every financial report. The following figure briefly summarizes the changes in this adjustment. For more detailed views on the scope adjustment, please refer to the review of 1Q25.

-

![]()

Enflame Tech's IPO Journey: Navigating Over 5.9 Billion Yuan in Losses and Soaring Debt in Q1 This Year

-

![]()

Trillion-Yuan Giant Li Shufu 'Streamlines': Could Levc Be the Casualty?

-

![]()

AI Competes for Electricity and Generates Power in the Gobi Desert

-

![]()

The First Batch of Victims of the AI Bubble: Programmers

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'