Baidu: Is the Kunlun Chip the 'Life-Saving Straw' Amidst a Protracted Advertising Winter?

03/02 2026

03/02 2026

615

615

Baidu's fourth-quarter results were released after the market close on the Hong Kong Stock Exchange on February 26, 2026. Overall, Q4 performance was mediocre. However, given the prolonged recent adjustment + support from repurchases and dividends + upcoming narratives such as the listing of Kunlun Chip and its inclusion in stock connect programs within the year, the market is not expected to impose excessive sustained penalties.

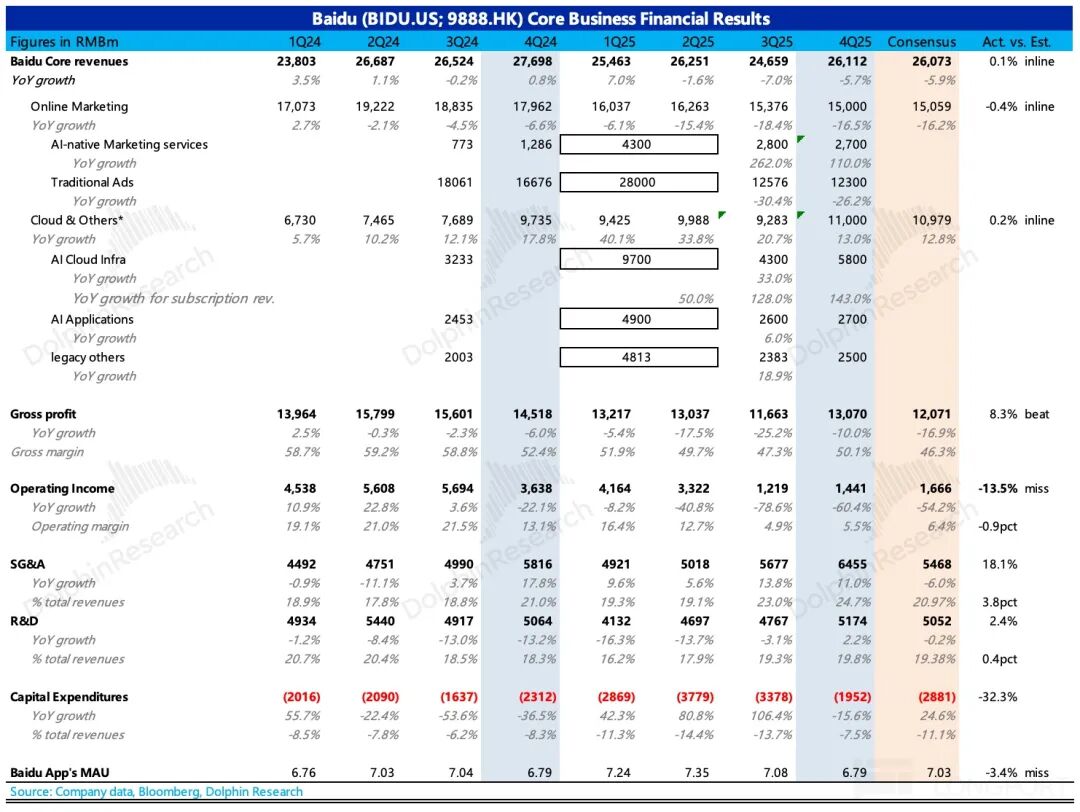

This quarter, Baidu formally adopted a new structure for performance disclosure, dividing it into two parts: AI business and other traditional businesses. The AI business includes AI infrastructure, AI applications, and AI-native marketing. As institutions still set expectations based on the original structure, Dolphin Research will attempt to restore the old disclosure method for comparative analysis and will continue to focus on Baidu's portion, excluding iQIYI.

Specific observations:

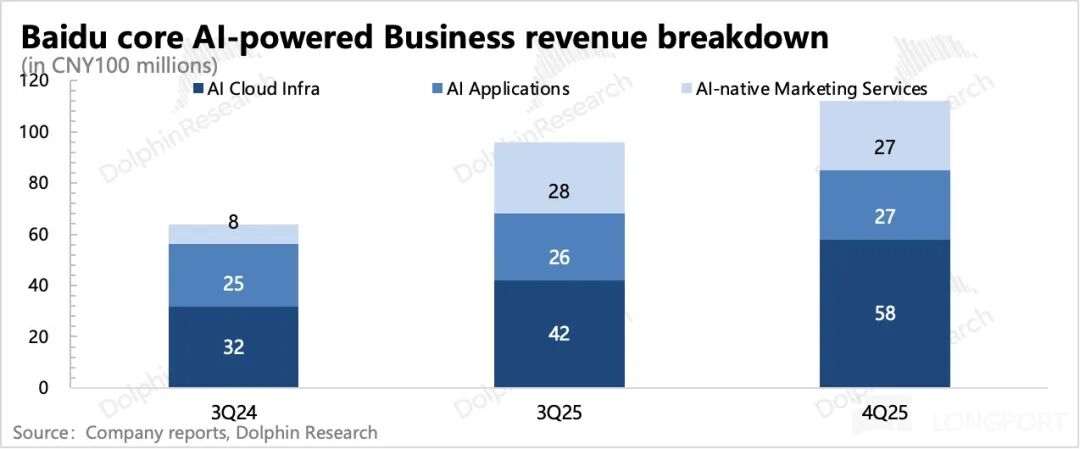

1. AI content continues to rise to 43%: In the fourth quarter, AI-related revenue reached RMB 11.3 billion, accounting for 43% of total revenue, up from 39% in the third quarter. Among them:

(1) AI cloud infrastructure (including cloud services, large model APIs, and computing power leasing) accounted for half, with a quarter-on-quarter growth rate of 35%. This reflects Baidu's advantage in providing comprehensive solutions and cost-effectiveness from computing power to full-stack AI large models, representing one of the few bright spots in this earnings report.

(2) AI applications (including products such as Baidu Wenku, Baidu Netdisk, and digital employees): Remained flat quarter-on-quarter, with the Netdisk business likely still dragging.

(3) AI-native marketing (Agents and digital humans): Slightly declined quarter-on-quarter. Considering industry trends, this may have been influenced by competition. Further details can be gleaned from the earnings call to determine if seasonal or other objective factors played a role.

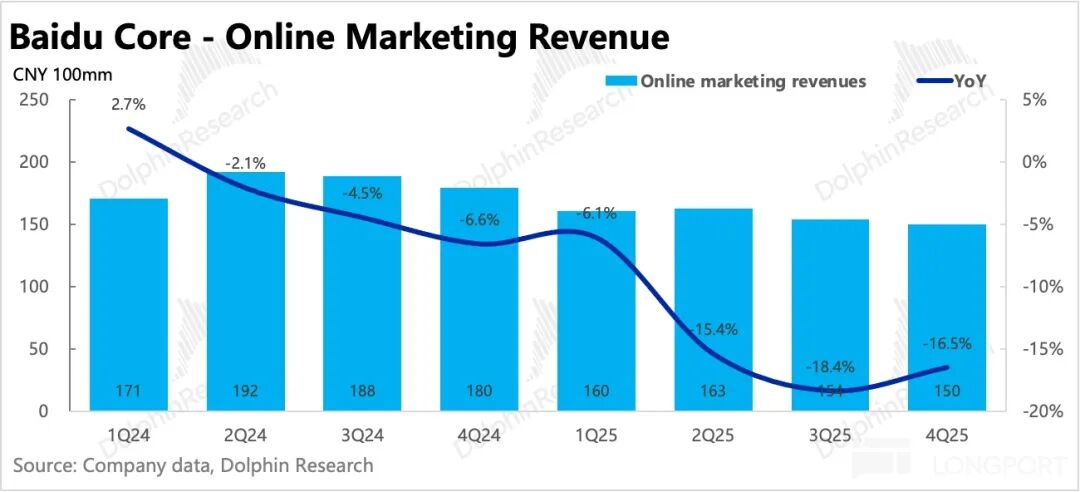

2. Traditional advertising continues to struggle: The separated traditional advertising (search, information feed ads, etc.) saw a 26% year-on-year decline. Although this was slower than the 30% decline in the previous quarter, it is uncertain how much of this was due to a low base effect, whether there is a genuine recovery trend, and the pace of subsequent return to positive growth remains difficult to determine.

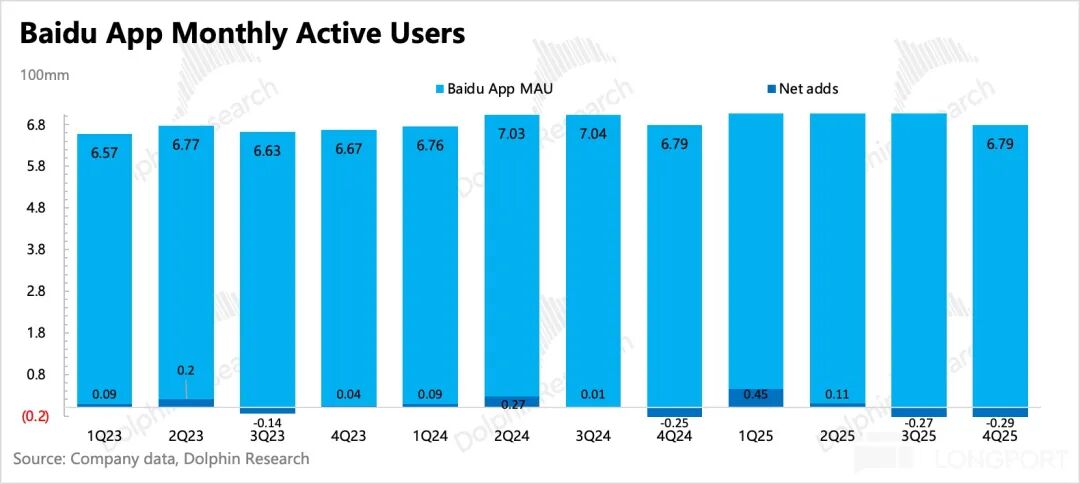

Dolphin Research leans toward the view that traditional advertising is still struggling at the bottom, given that Baidu's traditional advertising is affected by the macro environment and competition both within and outside the industry. In the fourth quarter, Baidu Mobile continued to lose users, with MAU dropping to 679 million. Despite seasonal influences, the continuous decline over two quarters makes it difficult to ignore the impact of competition, especially from new-generation AI chatbots.

Currently, Baidu's AI chatbot, ERNIE Bot, has a standalone app called Wenxiaoyan, but user penetration is primarily through its integration within the Baidu App. The company disclosed that ERNIE Bot has reached 200 million MAU in penetration users, equivalent to nearly 30% penetration within Baidu Mobile.

3. Autonomous driving and others: Revenue from this segment reached RMB 2.5 billion in the fourth quarter, showing quarter-on-quarter growth. In the second half of last year, Apollo focused on expanding into international markets, conducting tests in the Middle East, UK, South Korea, and other international markets through partnerships with Uber and Lyft. To date, Apollo has covered 26 cities globally.

4. Depreciation cost optimization and organizational efficiency: Operating profit under GAAP fell short of expectations due to nearly RMB 700 million in severance compensation and provisions for bad debts.

However, after excluding these factors, adjusted operating profit slightly exceeded expectations due to reduced amortization and depreciation (partial traditional equipment underwent one-time impairment in the previous quarter) and overall efficiency gains from personnel optimization (SBC expenses decreased by 32% quarter-on-quarter with a similar market capitalization at the end of the period).

5. Shareholder returns become more 'generous': Although the core cash flow business—advertising—has declined, the accumulated cash remains substantial. By the end of 2025, Baidu had RMB 115.3 billion in cash + short-term investments, offset by short-term loans of RMB 22.4 billion, leaving nearly RMB 93 billion (approximately USD 13.5 billion).

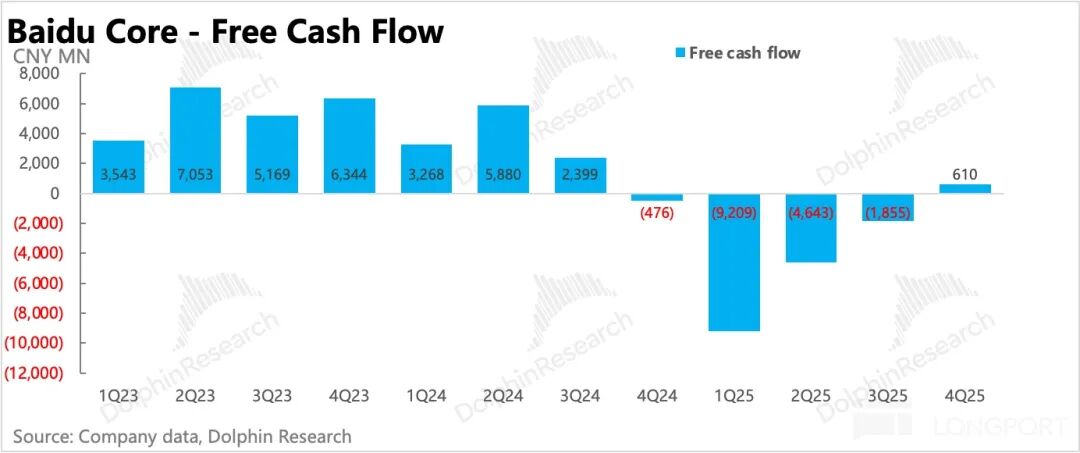

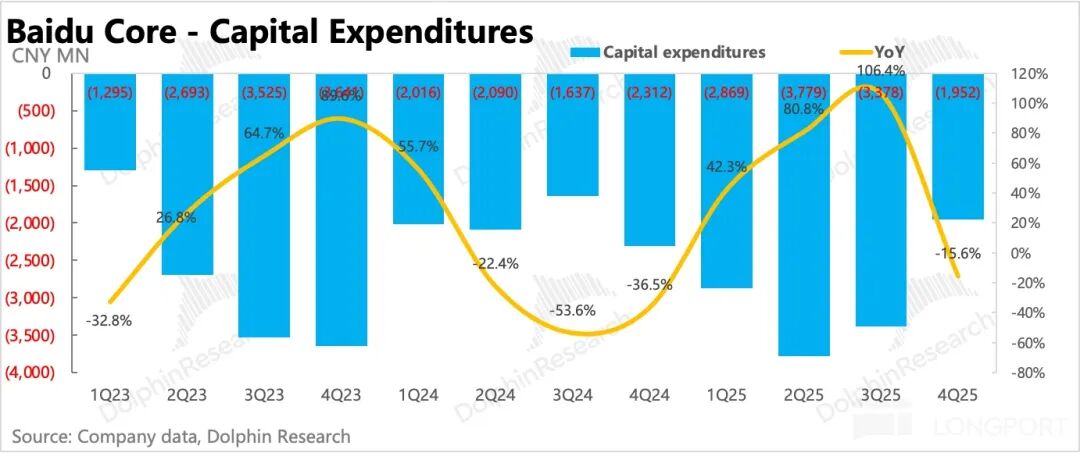

With improved profits in the fourth quarter, quarterly free cash flow appeared to turn positive for the first time in a year. However, Capex fell to less than RMB 2 billion this quarter, which Dolphin Research believes is not the norm. Therefore, if restored to normal growth, actual free cash flow may still be negative.

In early February, the company announced a two-year share repurchase program of up to USD 5 billion, and its first dividend plan was approved by the board of directors. The specific amount was not disclosed this time and is expected to be announced and implemented this year.

Excluding dividends, if the repurchase is executed at the upper limit, overall shareholder returns will increase to the 5-6% range (compared to the current market capitalization of RMB 45.6 billion). This represents an improvement from the previous 2% return rate, enhancing bottom support during market corrections.

6. Detailed financial data overview

Dolphin Research's Viewpoint

Since the third quarter of last year, Baidu's valuation sentiment has significantly improved compared to the past. The initial rally was driven by expectations from new 'narratives'—domestic substitution in computing power + spin-off and listing of innovative businesses + increased shareholder returns + inclusion in stock connect programs after dual-primary listing. The subsequent decline since the beginning of the year, in line with the overall Hong Kong stock market, reflects a narrative shift towards AI disruption theories.

As of now, regarding these narratives:

(1) Hype around domestic substitution in computing power occasionally resurfaces. The spin-off and listing of Kunlun Chip are in progress, and the USD 5 billion repurchase program has been officially announced. Future catalysts include the potential spin-off and listing of autonomous driving (Apollo Go) and inclusion in stock connect programs after dual-primary listing.

In other words, half of the short-term positives have already been priced in, while the other half still has expectation gaps, though the market is somewhat aware of them. Optimistic funds may have already priced in some of these factors. This suggests that significant rallies can only occur under specific conditions (valuation corrections + near realization).

(2) The impact of negative narratives seems to persist, with tightening liquidity expectations and the siphoning effect from ByteDance exerting some pressure on short-term sentiment.

At this juncture, the current market capitalization of USD 45.6 billion aligns with Dolphin Research's neutral valuation expectation updated in 'Kunlun Chip's Accelerated Listing: Baidu's 'Google Moment'?' (Some institutions are more optimistic about Baidu's valuation due to higher pricing of Kunlun Chip).

The difference is that with significantly improved shareholder returns, subsequent valuations may find some support if they continue to decline. However, upward movement requires positive expectation gaps in fundamentals—such as significantly stronger-than-expected cloud revenue or a bottoming-out and recovery in traditional advertising.

Regarding fourth-quarter performance, Dolphin Research believes that while the cloud business exceeded expectations, the drag from traditional advertising and the moderate growth trend of other AI businesses make the fundamentals insufficient to drive valuation upwards as a strong catalyst.

In other words, unless valuations correct to offer more attractive opportunities, upward recovery will likely depend on short-term 'narratives': such as new progress in the listing timeline of Kunlun Chip (expected mid-year), potential listing and financing plans for Apollo Go, and the promotion of dual-primary listing and inclusion in stock connect programs (expected in the second half of the year), which could bring about a meaningful new round of recovery.

Detailed analysis follows:

I. Business Structure

Baidu is relatively rare among internet companies in detailed performance breakdown:

1. Baidu Core: Covers traditional advertising (search/information feed ads), innovative businesses (smart cloud/DuerOS Xiaodu smart speakers/Apollo, etc.), and AI-related revenue, including AI infrastructure (cloud, large model APIs, computing power leasing), AI applications (including products such as Baidu Wenku, Baidu Netdisk, and digital employees), and AI-native marketing (Agents and digital humans);

2. iQIYI Business: Membership, advertising, and copyright sublicensing, among others.

The separation of these two businesses is clear-cut, and with iQIYI as an independently listed company providing detailed data, Dolphin Research will also provide a detailed breakdown of these two businesses. Given that there are approximately 1% (between RMB 200-400 million) of eliminations between the two major businesses, the breakdown of Baidu Core by Dolphin Research may slightly differ from the actual reported figures, but this does not hinder trend judgment.

II. AI Content Continues to Rise to 43%

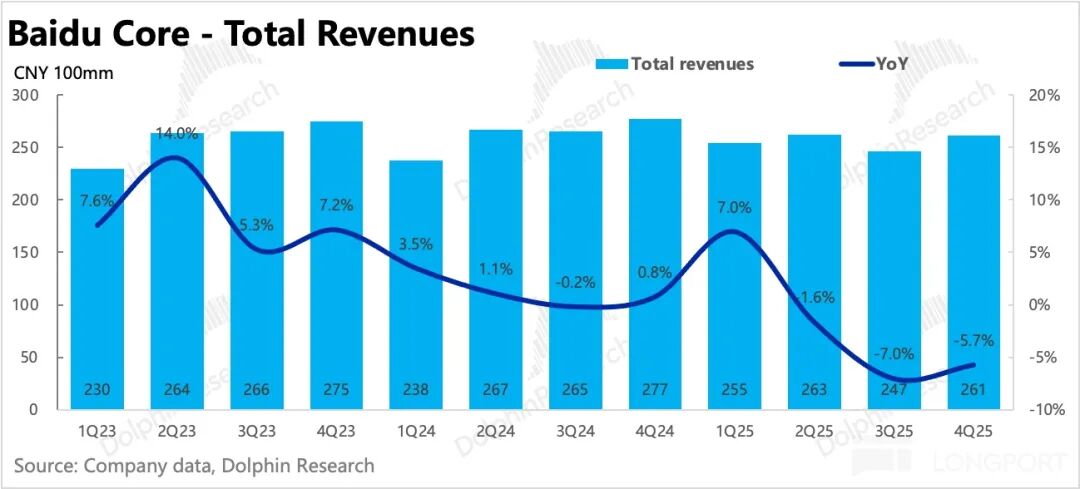

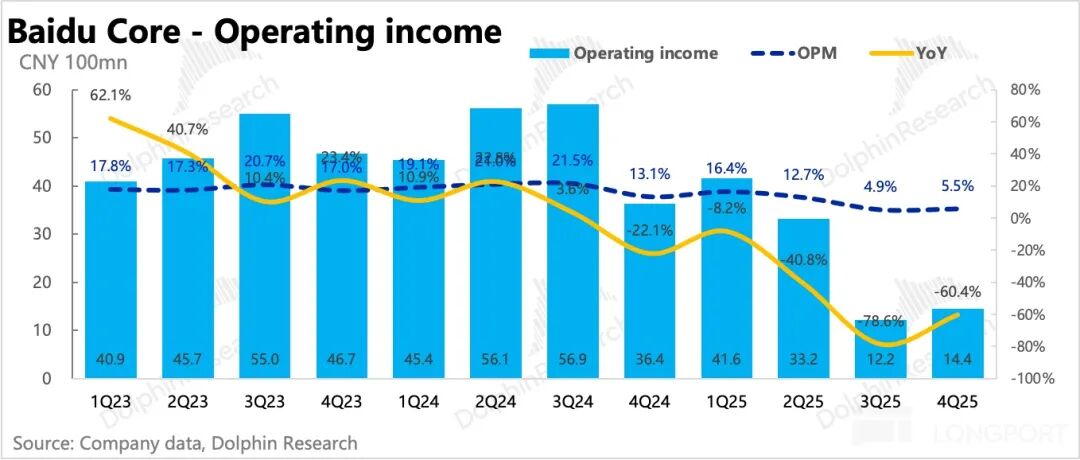

Baidu Core's total revenue was RMB 26.1 billion, a 6% year-on-year decline, primarily dragged down by traditional advertising such as search and information feeds. AI-related revenue, however, experienced high growth, reaching RMB 11.3 billion in the current period, accounting for 43% of total revenue, partially mitigating the impact of the decline in traditional advertising.

Dolphin Research restores the old disclosure structure for specific comparisons:

(1) Advertising: Overall, a 16.5% year-on-year decline, with traditional advertising down 26%. The turning point for recovery remains unclear. Baidu Mobile's MAU was 679 million, with continued seasonal user loss quarter-on-quarter.

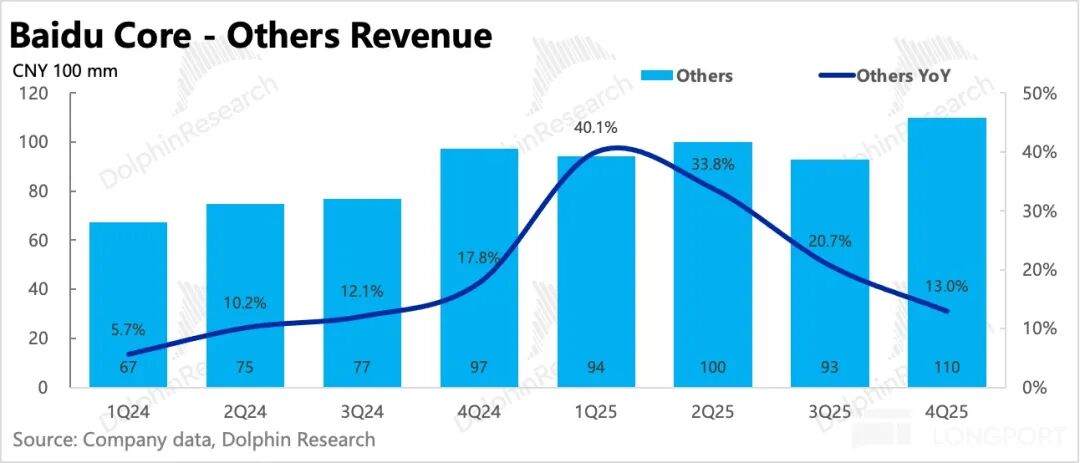

(2) Cloud and other revenues: Overall growth of 13%, with a significant slowdown due to a high base in the previous year (project clustering), meeting market expectations. However, further breakdown shows that cloud infrastructure service revenue performed better than capital expectations.

III. Revenue Under Pressure, Profitability Sustained Through Efficiency Gains

The restructured organization around the AI theme, through optimization of personnel redundancies in old businesses and cross-departmental resource coordination, has brought some effects to the profit side, alleviating overall profitability pressure caused by the decline in high-margin advertising.

In November last year, two new large model R&D departments were established, one continuing to advance general-purpose LLMs and the other responsible for fine-tuning specialized models for application scenario demands. In January this year, along with team adjustments, Baidu merged its original Netdisk and Wenku services.

Dolphin Research believes this mainly involves adjustments to Baidu Netdisk, especially personnel optimization in response to competition from Kuake Netdisk. Meanwhile, Baidu Wenku has performed well under AI empowerment, and since Netdisk's cloud storage function aligns with the same demand chain, they can be bundled together.

Now, let's look at the actual Q4 profitability:

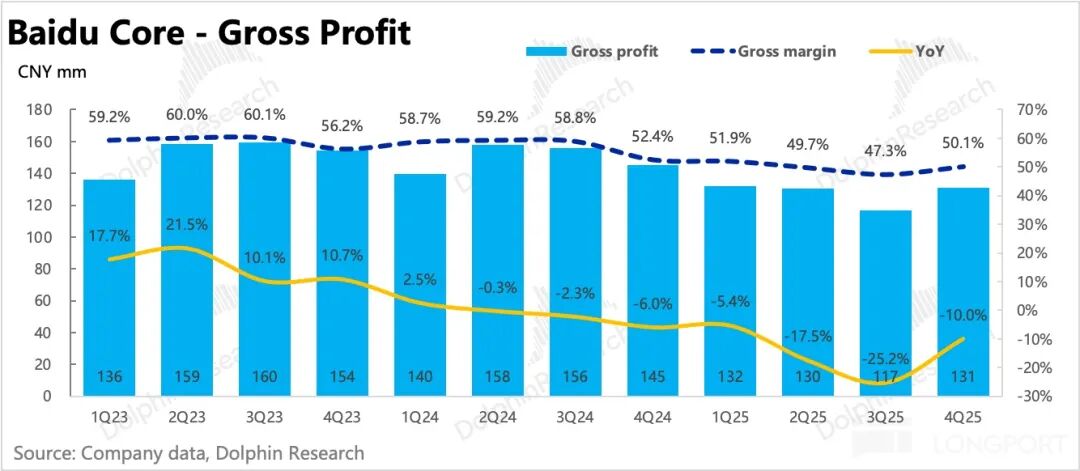

(1) Core gross margin rebounded quarter-on-quarter despite advertising pressure, mainly due to one-time impairment of partial traditional equipment in the previous quarter, leading to significant optimization of depreciation and amortization costs starting from Q4: Total depreciation and amortization in Q4 was RMB 1.7 billion, compared to RMB 2.2 billion in Q3.

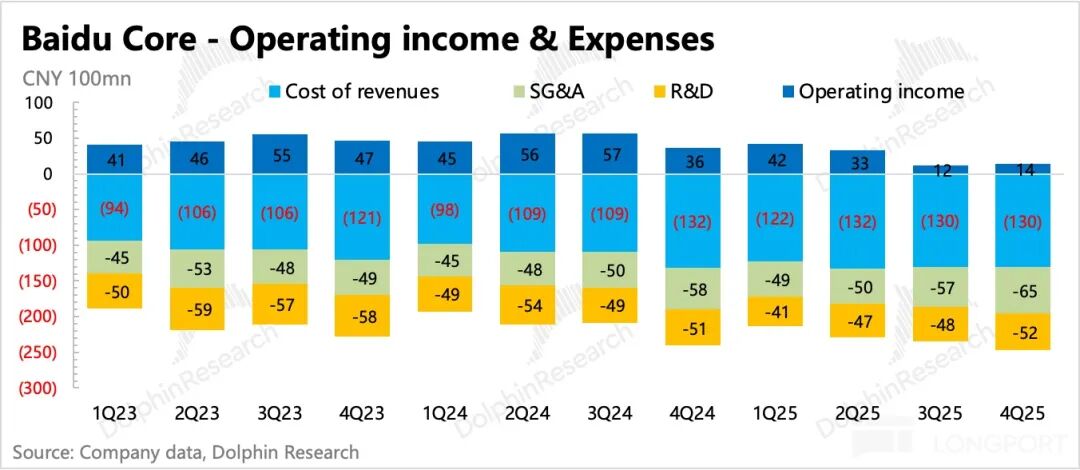

(2) Core operating profit was RMB 1.4 billion, with a profit margin of 5.5%, both increasing quarter-on-quarter. However, this was lower than market expectations, primarily due to RMB 700 million in severance compensation and partial bad debt impairments. Excluding these factors and other non-recurring changes such as SBC, Non-GAAP operating profit was RMB 2.84 billion, actually exceeding consensus expectations (RMB 2.54 billion).

IV. Capital Expenditure May Only Be Temporarily Contracted

With improved profits in the fourth quarter, quarterly free cash flow appeared to turn positive for the first time in a year. However, Capex fell to less than RMB 2 billion this quarter, which Dolphin Research believes is not the norm. Therefore, if restored to normal growth, actual free cash flow may still be negative.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referring to the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information mentioned or the opinions expressed in this report shall not be considered or deemed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor shall they constitute advice, inquiry, recommendation, etc., regarding the relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or for use by, any person or entity in any jurisdiction or country where such distribution, publication, availability, or use would be contrary to applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliated companies to any registration or licensing requirements in such jurisdiction.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create copies or reproductions in any form by any means, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once