DELL: Can AI with Twofold Growth Alleviate Concerns Over 'Storage Shortage'?

03/02 2026

03/02 2026

622

622

Dell Technologies (DELL.N) released its fourth-quarter financial report for FY2026 (ending January 2026) after the U.S. market closed on the early morning of February 27 (Beijing Time):

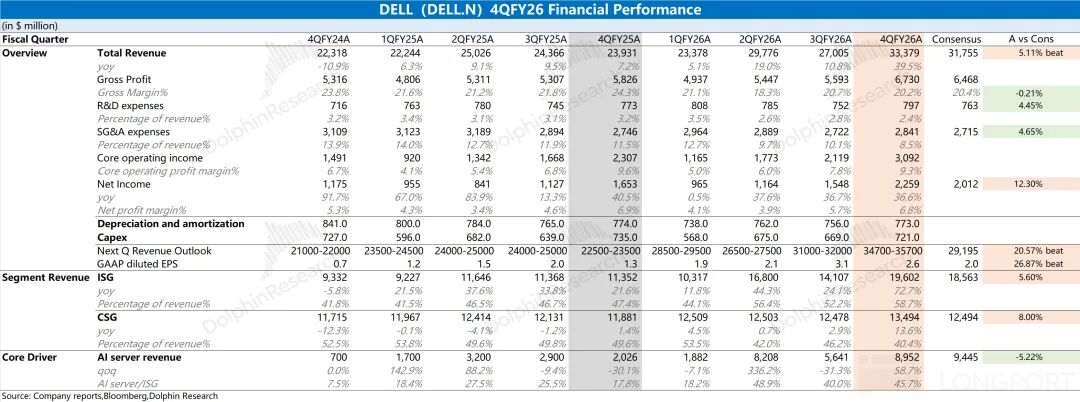

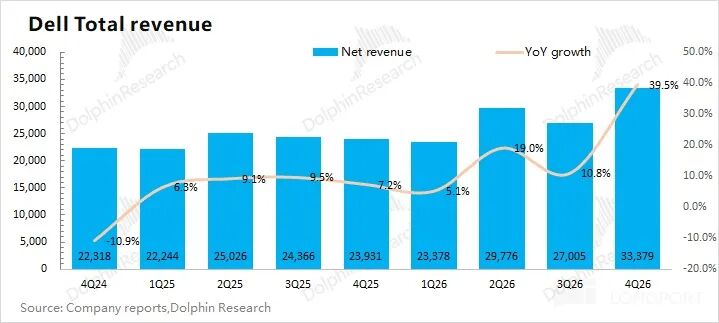

1. Core Performance: DELL's revenue for the quarter was $33.4 billion, up 39.5% year-over-year, surpassing market expectations ($31.8 billion). The company's sequential revenue increased by $6.4 billion this quarter, primarily due to contributions from AI server shipments.

The company's gross margin for the quarter was 20.2%, down 0.5 percentage points sequentially and slightly below market expectations (20.4%). Compared to service revenue, products such as AI servers have relatively lower gross margins. As revenue from AI server-related products increases, it structurally pulls down the overall gross margin.

2. ISG Business (Infrastructure Solutions Group): Revenue for the quarter was $19.6 billion, up $5.5 billion sequentially, exceeding market expectations ($18.6 billion). The sequential increase was driven by AI servers.

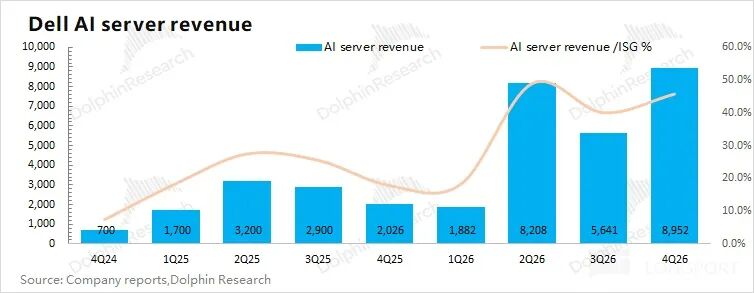

① AI Server Segment: The company's AI server revenue for the quarter was approximately $8.95 billion, falling short of market expectations ($9.4 billion).

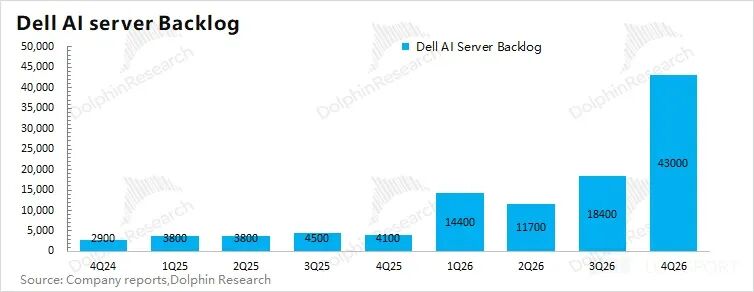

However, the company's new AI orders for the quarter reached $34.1 billion, far exceeding market expectations ($11 billion), with a backlog of $43 billion at the end of the quarter. Dolphin Tab estimates that the company's AI server revenue will exceed $13 billion next quarter, significantly surpassing original market expectations ($7.5 billion), contributing the primary increment for the next quarter.

② Other Segments: Apart from AI servers, performance remained relatively stable. Traditional server-related businesses contributed approximately $5.85 billion in revenue, up 27% year-over-year; storage business contributed around $4.8 billion in revenue, up 2% year-over-year.

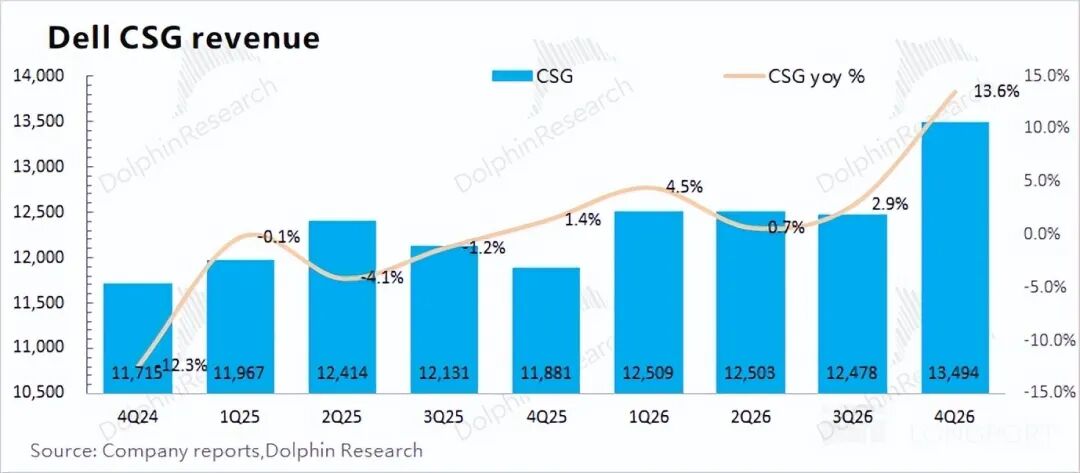

3. CSG Business (Client Solutions Group): Revenue for the quarter was $13.5 billion, up 13.6% year-over-year, exceeding market expectations ($12.5 billion). Specifically, DELL's client business remains primarily focused on commercial customers. Revenue from commercial clients was $11.6 billion, up 16% year-over-year; while revenue from individual consumers was only $1.9 billion, remaining roughly flat year-over-year.

4. Next Quarter Guidance: The company expects revenue for the first quarter of FY2027 to be between $34.7 billion and $35.7 billion, significantly exceeding market expectations ($29.2 billion). Considering the company's backlog of nearly $43 billion this quarter, the upward revision in guidance is primarily driven by the AI business (estimated sequential increase of around $2 billion). The company's EPS (GAAP) for the next quarter is $2.55, better than market expectations ($2).

Dolphin Tab's Overall View: 'Explosive' AI Orders Accelerate Growth

DELL's performance this time was quite strong, with sequential revenue increasing by $6.3 billion. The company's growth this quarter was primarily driven by ISG business (server) shipments.

① The company achieved $8.95 billion in AI business revenue this quarter, up $3.3 billion sequentially. New AI orders for the quarter reached a record $34.1 billion, far exceeding market expectations ($10-11 billion). The backlog at the end of the quarter increased to $43 billion, laying the foundation for the company's future high growth.

② Compared to this quarter's data, the company's guidance was even more 'surprising.' The company expects revenue for the next quarter to reach $34.7-35.7 billion, with the midpoint of the range representing a sequential increase of $2 billion, significantly better than market expectations ($31.8 billion). Considering the backlog of orders, Dolphin Tab estimates that the company's AI revenue for the next quarter could exceed $13 billion, with a sequential increase of over $4 billion, which is the main reason for the upward revision in revenue guidance.

Previously, the company's management raised long-term guidance (7-9% compound annual growth rate in revenue for 2026-2030), and the stock price once reached $165. Subsequently, the stock price declined again, primarily due to concerns in the following areas:

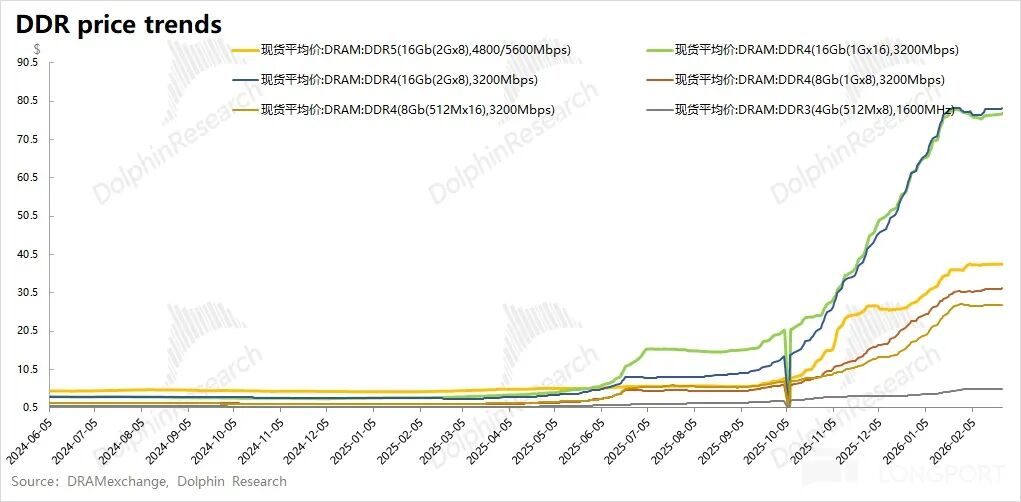

a) Tighter Storage Market: Driven by demand for AI servers, storage prices began to 'surge' in the second half of 2025. Since PCs are one of the main end-use scenarios for storage, the 'sustained rise in storage prices' directly impacts the performance of the company's traditional PC business.

Combining views from manufacturers like Qualcomm, the current storage issue has escalated from 'price hikes' to 'shortages.' This means that even if manufacturers 'pay more,' they may not necessarily receive goods, leading to relatively cautious outlooks for the PC market.

During this round of storage price hikes, the company's traditional CSG business (client solutions) will continue to face pressure.

b) AI Servers: With traditional businesses under pressure, AI progress is the company's biggest highlight.

Recently, major cloud service providers have raised their capital expenditure outlooks. Dolphin Tab estimates that the combined capital expenditure of the four core cloud providers (Google, Meta, Microsoft, and Amazon) in 2026 could exceed $660 billion, with a year-over-year growth rate of 62%.

If DELL's management does not subsequently raise AI guidance, considering previous guidance (20-25% compound annual growth rate for AI business in 2026-2030), it implies two possibilities: ① Capital expenditure growth will significantly slow down thereafter; ② DELL's share in AI Capex will decline.

On the other hand, NVIDIA is a core partner for DELL's AI servers. As the focus of large models shifts from 'training to inference,' products like ASICs will pose challenges to NVIDIA's GPUs. If NVIDIA's competitiveness declines, the market will also worry about the growth performance of DELL's AI servers.

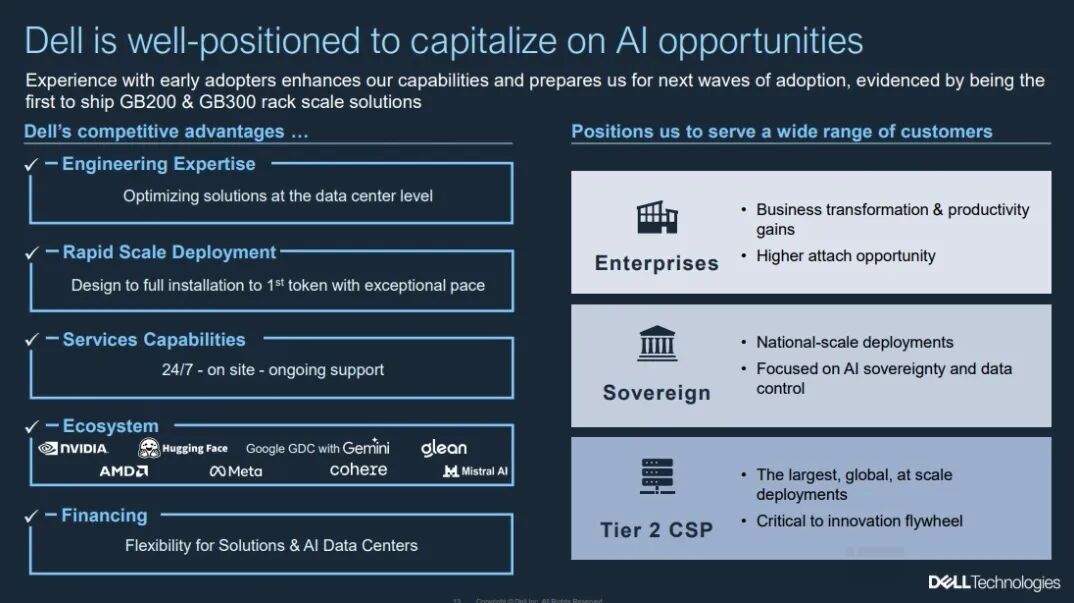

Since the company's business is relatively more focused on enterprise and sovereign/government clients, it helps the company achieve steady growth in its AI business.

DELL's current market capitalization is $80.5 billion, corresponding to approximately 9x PE for core operating profit after tax in FY2027 (assuming revenue growth of 29%, gross margin of 19.5%, and tax rate of 18.5%).

Given the current situation of 'rising prices and even shortages' in storage, outlooks for the PC market in the industry are relatively cautious, which will also continue to put pressure on the company's traditional business.

With traditional businesses under pressure being 'unavoidable,' the company's biggest highlight is its AI business. This quarter, the company reported $34.1 billion in new AI server orders, significantly exceeding market expectations ($11 billion). The backlog at the end of the quarter reached $43 billion, laying the foundation for high growth in the company's AI business.

The company's management also provided full-year guidance for FY2027, with full-year revenue expected to reach $138-142 billion, including $50 billion in AI revenue, doubling year-over-year and far exceeding market expectations ($35-40 billion). Driven by the doubling growth in AI business, the company's overall performance will also accelerate.

A more detailed value analysis has been published in the article with the same name in the 'Dynamic-Depth (Research)' section of the Changqiao App.

The following is a detailed analysis:

I. DELL's Overall Performance

1.1 Revenue

DELL achieved revenue of $33.38 billion in the fourth quarter of FY2026 (25Q4), up 39.5% year-over-year, surpassing market expectations ($31.8 billion). The company's sequential revenue increased by $6.4 billion this quarter, driven by both the ISG business (Infrastructure Solutions Group) and the CSG business (Client Solutions Group), with AI revenue increasing by $3.3 billion sequentially.

1.2 Gross Profit

DELL achieved a gross profit of $6.73 billion in the fourth quarter of FY2026 (25Q4), up 15.5% year-over-year.

The company's gross margin for the quarter was 20.2%, down 0.5 percentage points sequentially and slightly below market expectations (20.4%). The increase in the proportion of the ISG business, which has a relatively lower gross margin, has a structural dilutive effect on the overall gross margin.

1.3 Operating Expenses

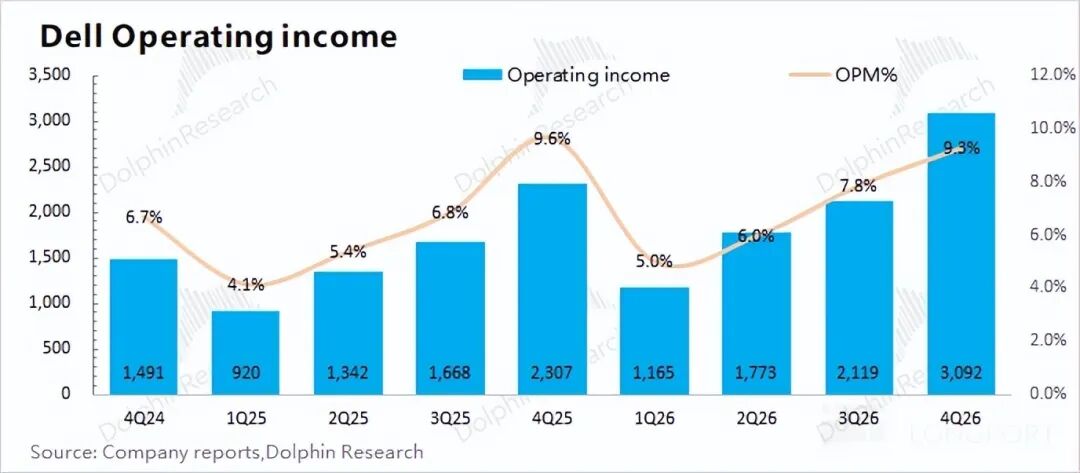

DELL's operating expenses for the fourth quarter of FY2026 (25Q4) were $3.64 billion, up 3% year-over-year. Due to scale effects, the operating expense ratio decreased to 10.9% this quarter.

Among them: 1) R&D expenses: The company's R&D expenses for the quarter were $800 million, up 3% year-over-year, with the company maintaining a growth trend in R&D expenses; 2) Sales and administrative expenses: The company's sales and administrative expenses for the quarter were $2.84 billion, up 3% year-over-year.

1.4 Net Profit

DELL achieved core operating profit of $3.1 billion in the fourth quarter of FY2026 (25Q4), up 34% year-over-year, with the core profit margin increasing to 9.3% this quarter. The growth in profit this quarter was primarily driven by revenue growth and margin recovery.

II. DELL's Core Business Performance

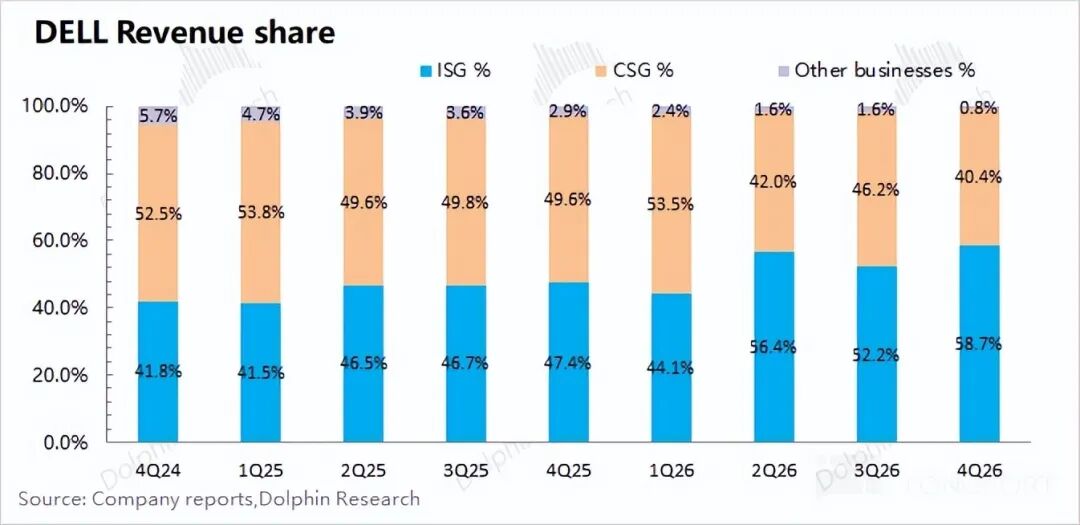

From the perspective of DELL's business segments, driven by the growth of AI servers, the company's ISG business (Infrastructure Solutions Group) showed an upward trend, accounting for 58.7% this quarter.

Combining the company's previous growth guidance, the compound annual growth rate of the ISG business (11-14%) for FY2026-FY2030 will be significantly higher than that of the CSG business (2-3%), and the proportion of the ISG business will continue to rise.

The ISG business is the most important part of the company, with specific breakdowns as follows:

2.1 ISG Business (Infrastructure Solutions Group)

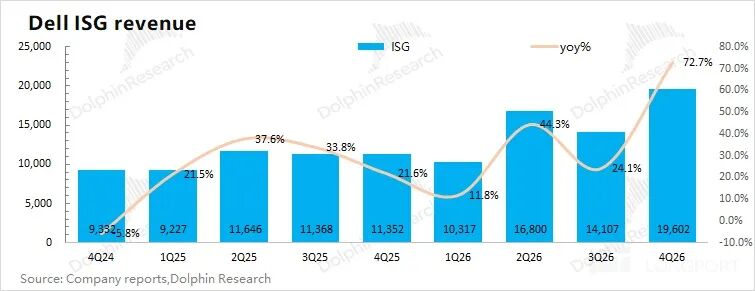

DELL's ISG business achieved revenue of $19.6 billion in the fourth quarter of FY2026 (25Q4), up 72.7% year-over-year, exceeding market expectations ($18.6 billion).

Specifically: ① The AI server business achieved revenue of approximately $8.95 billion this quarter, up $3.3 billion sequentially, contributing the primary increment to the company's ISG business this quarter; ② Traditional server-related businesses achieved revenue of $5.85 billion this quarter, up 27% year-over-year; ② The storage business achieved revenue of $4.8 billion this quarter, up 2% year-over-year.

The growth of the ISG business this quarter was driven by AI servers, with the current proportion of AI business in the ISG business exceeding 40%.

In addition to AI revenue for this quarter, the company's management also provided information on new AI orders and backlog, which are forward-looking indicators. The company secured $34.1 billion in new AI orders this quarter, significantly exceeding market expectations ($11 billion). The backlog at the end of this quarter reached $43 billion, laying the foundation for high growth in the company's AI business in FY2027.

Given the core partnership between NVIDIA and Dell, there have been market concerns about the impact of ASICs on Dell's AI servers within NVIDIA's supply chain. However, judging by the progress of the company's AI business this quarter, Dell's AI business continues to perform well. The company has even provided guidance of $50 billion in AI revenue for FY2027, implying a doubling of Dell's AI business and injecting clearer 'AI confidence' into the market.

2.2 CSG Business (Client Solutions Group)

Dell's CSG business achieved revenue of $13.5 billion in Q4 FY2026 (i.e., Q4 2025), up 13.6% year-over-year, outperforming market expectations ($12.5 billion).

Specifically, Dell's client business remains predominantly focused on commercial customers. Revenue from commercial clients reached $11.6 billion this quarter, up 16% year-over-year, while revenue from individual consumers remained roughly flat at $1.9 billion.

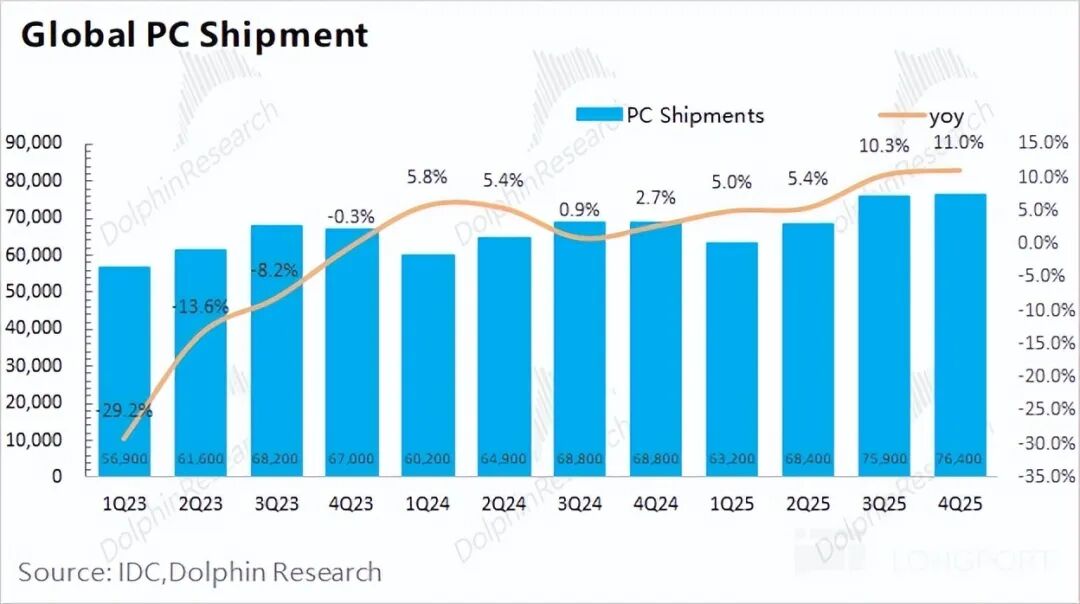

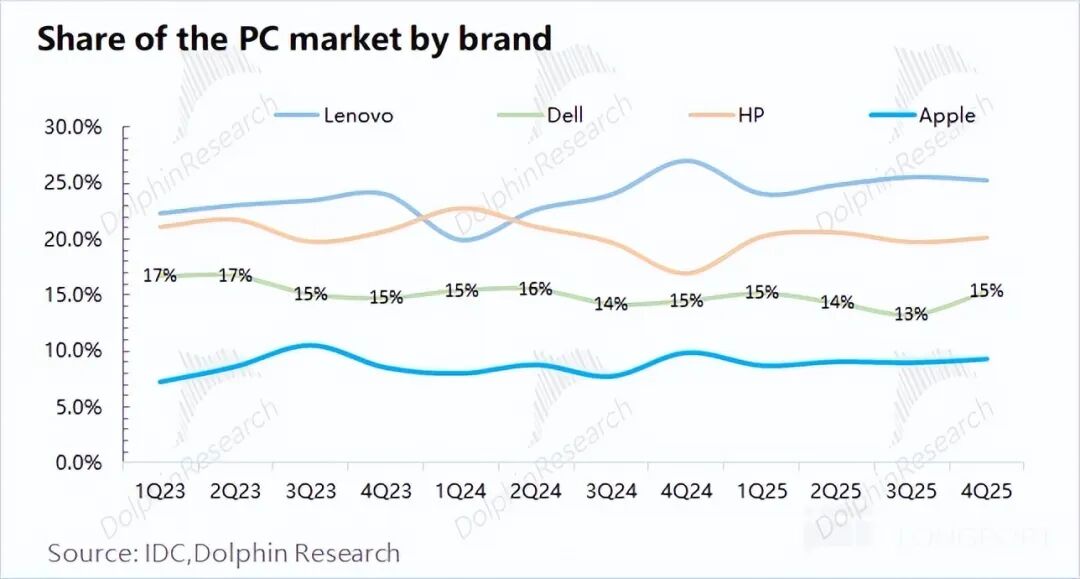

According to global PC market data, global PC shipments reached 76.4 million units in Q4 2025, up 11% year-over-year, showing a rebound. Dell's shipments amounted to 11.7 million units, up 17% year-over-year, outperforming the industry average and increasing the company's market share in the PC segment to 15%.

Based on discussions with vendors like Qualcomm, the current issue with memory has escalated from 'price hikes' to 'shortages.' This means that even if vendors are willing to pay more, they may not be able to secure supplies. Projections for the PC market remain relatively cautious.

Under these circumstances, Dell's PC products will, on one hand, pass on some cost pressures to the downstream market through price increases (unified price adjustment already implemented on January 6, 2026). On the other hand, the company will strive to secure more memory products to ensure supply chain security.

The former will affect end-user demand, while the latter highlights supply-side uncertainties. In the environment of 'memory shortages,' the company's CSG business will continue to face pressure.

- END -

// Reprint Authorization

This article is an original piece from Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated entities. It does not take into account the specific investment objectives, product preferences, risk tolerance, financial situation, or particular needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are provided for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell or a solicitation to buy securities, nor do they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to or use by individuals or residents of jurisdictions where such distribution, publication, provision, or use would conflict with applicable laws or regulations or subject Dolphin Research and/or its subsidiaries or affiliates to registration or licensing requirements in those jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and its copyright is solely owned by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual may (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once