Did Advertising Fail? Is AI the Savior? Li Yanhong and Baidu's 'Breaking and Building'

03/03 2026

03/03 2026

505

505

By He Ying

Edited by Zhang Xiao

The term BAT, a relic of the past, is rarely mentioned seriously anymore.

Tencent remains rock-solid with its WeChat ecosystem, Alibaba is restructuring under e-commerce pressure, and ByteDance has quietly become the new overlord of Chinese internet with Douyin and Doubao. Baidu, once a company that defined internet order through search, has spent the past five years mostly 'losing': losing young users, losing advertiser budgets, losing market value, and losing presence in the public eye.

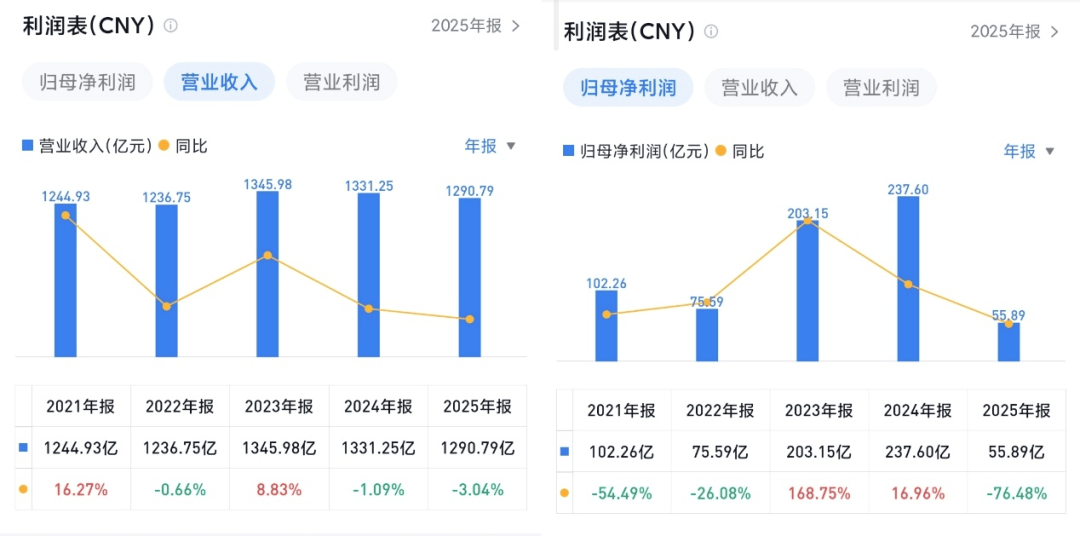

On February 26, Baidu released its 2025 financial report. The overall performance was not particularly impressive. Annual operating revenue was 129.1 billion yuan, down 3% year-on-year, marking Baidu's third consecutive year of stagnant or declining revenue.

At the profit level, net income attributable to the parent company under GAAP fell 76.5% year-on-year, primarily due to a one-time impairment charge of approximately 16.2 billion yuan in Q3 for outdated infrastructure no longer suited for AI needs. Excluding this impact, Non-GAAP net profit was 18.94 billion yuan, still down 30% year-on-year.

Chart via Snowball App

Chart via Snowball App

Core business revenue continues to decline, with Baidu App's MAU dropping to 679 million. As a typically B2C company, its presence on the consumer side keeps weakening—a fact that needs no emotional embellishment.

But changes are happening on another front. In 2025, AI-related revenue reached 40 billion yuan, accounting for 43% of Baidu's core business in Q4; AI cloud infrastructure generated approximately 20 billion yuan for the year, up 34% year-on-year—the biggest highlight in this report.

The problem is that Baidu's AI gains are happening more on the enterprise side than the consumer side. As its gateway influence weakens, the company, which originally rose on user traffic, is shifting its growth focus to the B2B sector.

Baidu hasn't collapsed, but it's changing how it operates. The question is: How far is this new path from rewriting the company's trajectory?

01

The Traditional Advertising Story is Nearing Its End

Try to recall: When was the last time you opened a traditional search engine on your phone—not to find strategies on Xiaohongshu, not using WeChat Search, not asking Doubao or DeepSeek directly, but honestly typing in Baidu's search box and waiting for that familiar list of blue links?

Most people can't remember.

This reality is harsher than any financial report number.

Starting in Q4, Baidu adopted a new disclosure framework, clearly dividing into three segments: core AI business, traditional business, and others. Traditional business includes search, information feeds, and traditional advertising services.

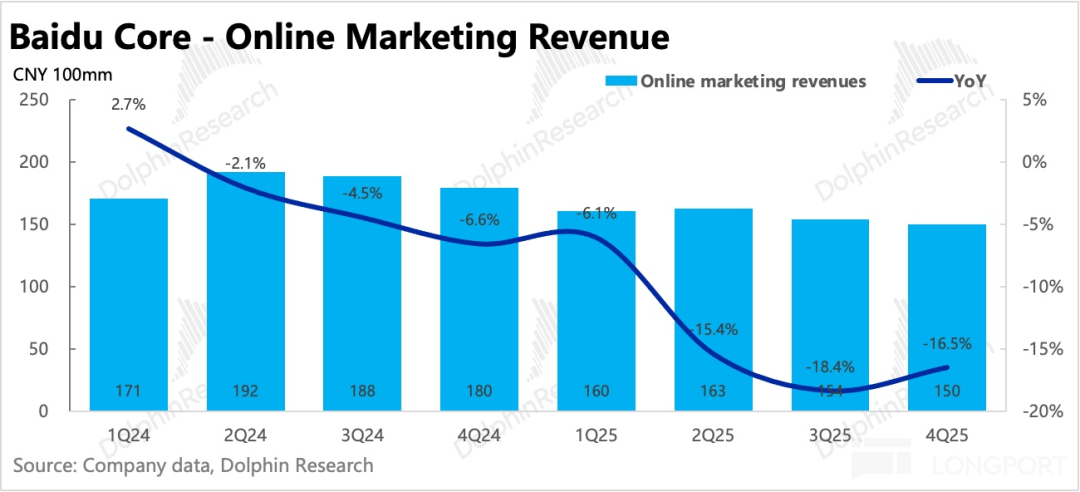

In 2025, Baidu's mobile app MAU fell to 679 million, declining for two consecutive quarters. According to Dolphin Research, traditional search ad revenue dropped 26% year-on-year in Q4. While this was an improvement from Q3's 30% decline, it's hard to tell whether this was due to Q3's low base or genuine recovery—uncertainty remains about when positive growth will resume.

Chart via Dolphin Research

Chart via Dolphin Research

Full-year advertising revenue remained under pressure, though this business was once Baidu's highest-margin core asset—search ads historically maintained high gross margins, serving as the ballast for the company's profitability. As it declines, Baidu's profit margins are being passively squeezed.

Baidu has long understood the competitive landscape of traffic diversification. Xiaohongshu captures strategy searches, Douyin captures video searches, WeChat Search captures instant queries—encroachment from outside competitors has been ongoing for years.

But what truly changed the market landscape in 2025 was the rise of AI-native search.

DeepSeek's breakthrough during Chinese New Year was a watershed moment, making ordinary users aware for the first time that 'asking questions' could completely bypass search engines. Doubao's MAU keeps climbing, while domestic alternatives to Kimi and ChatGPT continue to penetrate the market. These products aren't just taking Baidu's ad share—they're taking something more fundamental: the very nature of search is undergoing qualitative change.

In the past, users searched to find a link and jump to another page; now, users increasingly expect direct answers.

Baidu certainly recognizes this issue. After embedding AI into Baidu Search, Wenxin Assistant's MAU surpassed 200 million in December last year—no small number. AI search API calls grew over 110% quarter-on-quarter. Management sounded confident on the earnings call, saying they're 'evolving from information synchronization to solution provision.'

At Baidu World 2024 last November, Li Yanhong revealed that most Baidu search results are now AI-generated, with rich media coverage for top results reaching 70%.

Chart via Baidu's official WeChat

Chart via Baidu's official WeChat

This is good for user experience but amounts to Baidu directly disrupting its own advertising foundation.

The logic of traditional search ads relies on 'clicks.'

Users search, see ad links, click through, and advertisers pay. Every click represents real money. But when AI provides answers directly, users no longer need to click—ad inventory shrinks, and bidding space narrows.

While Baidu uses AI to save its search business, it's also accelerating the decomposition of its monetization model.

This creates an awkward dilemma: Baidu embraces AI to avoid being disrupted by it, but the cost of embracing AI is accelerating the erosion of its advertising revenue—its lifeblood. Not transforming means certain death; transforming means faster bleeding.

Worse, there's no clear Hemostasis point (point to stop the bleeding). Nothing needs fixing because nothing is broken—the era has simply moved forward.

Can Wenxin Assistant's 200 million MAU catch this falling foundation?

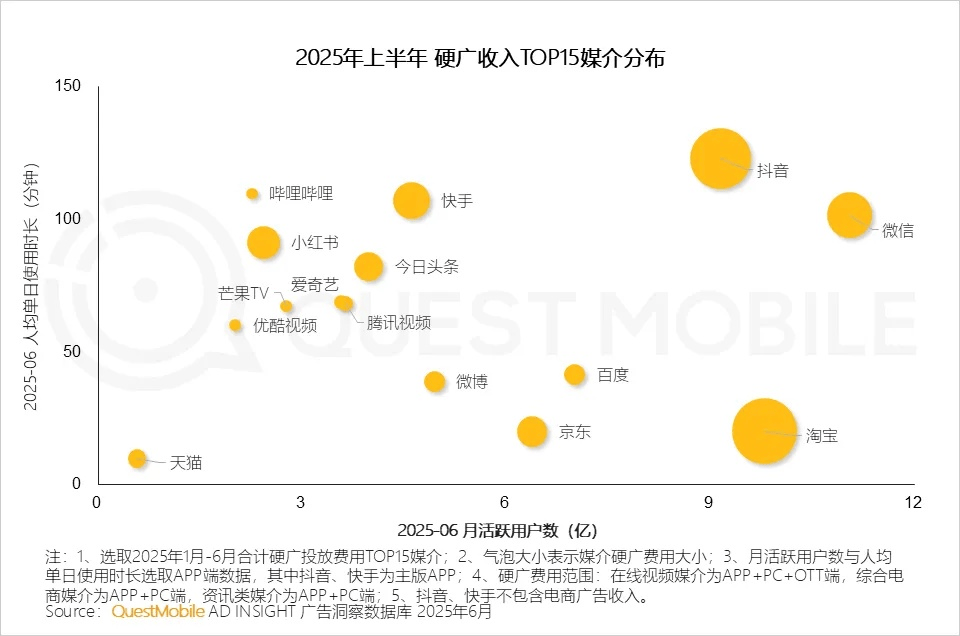

Not currently. According to QuestMobile, Baidu lagged far behind other media platforms in internet advertising revenue rankings in H1 2025.

Chart via QuestMobile

Chart via QuestMobile

The 200 million figure also needs scrutiny: Wenxin Assistant isn't an independent app but primarily embedded within Baidu Mobile, which has over 600 million MAU. How many of those are genuine high-frequency users versus forced 'penetration' pushes?

A truly user-centric AI product should be proactively opened and renewed—qualitatively different from users acquired through spontaneous viral spread.

More critically, while AI-native marketing services (digital humans + intelligent agents) saw 110% growth in Q4, their scale remains limited—far from enough to fill the gap left by declining traditional ads.

Simply put, Baidu is losing high-margin ad revenue while gaining low-base AI marketing revenue, with an unbridgeable gap between the two lines that no one knows if it can be closed.

This isn't just Baidu's problem—it's a historic question facing all traditional search advertisers:

When AI-native interactions become mainstream, how much is 'search' still worth? Google is conducting the same experiment with AI Overview, facing similar risks to its ad monetization model, though Google's scale and computing reserves give it more buffer time. Baidu lacks that luxury.

Advertising can no longer support the entire company. Baidu needs another leg to stand on.

02

The B2B Deep End: How Baidu Earned Its 40 Billion in AI

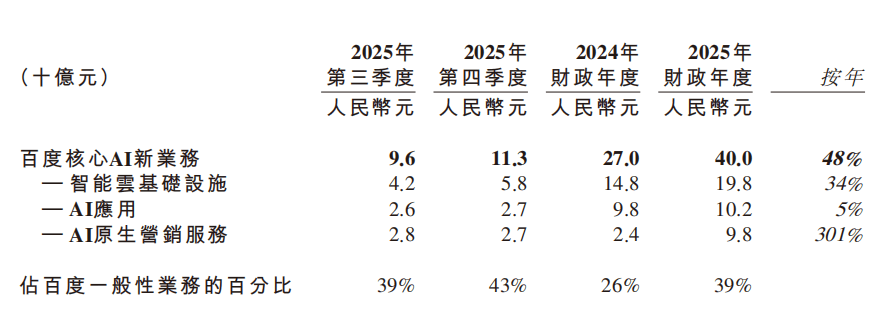

In 2025, Baidu's AI-related revenue hit 40 billion yuan. Q4 AI revenue was 11.3 billion yuan, accounting for 43% of core business—nearly half. Where is this money coming from?

Not from AI search.

In public discourse, Wenxin's presence remains low, overshadowed by Doubao and Yuanbao. The Chinese New Year traffic boom didn't land on Baidu. For most ordinary users, Baidu's AI hasn't become a must-use independent gateway.

But what truly supports AI revenue in the financials lies elsewhere.

In 2025, about 30 billion yuan of Baidu's core AI business revenue came from AI cloud, including approximately 20 billion yuan from AI cloud infrastructure (up 34% year-on-year, outpacing industry averages) and about 10 billion yuan from AI applications (products like Baidu Wenku and Baidu Netdisk). Another 10 billion yuan came from AI-native marketing—helping enterprises create digital humans and intelligent agents.

Chart via Baidu's financial report

Chart via Baidu's financial report

Among these 40 billion yuan, the portion closest to ordinary users' daily experience is actually the smallest. The AI cloud truly driving this number operates far from public view: helping enterprises 'integrate' AI capabilities into their systems.

What does Baidu's AI cloud sell?

An enterprise wanting to use AI needs more than just a large model. It requires computing power to run models, storage for data, interfaces to embed AI into existing systems, and maintenance when things go wrong. Baidu AI Cloud sells this entire packaged solution (also available in layers).

Baidu repeatedly emphasizes one word on earnings calls: 'full-stack.' This means: self-developed Kunlunxin chips provide computing power at the bottom layer, Baidu Intelligent Cloud serves as infrastructure, Wenxin large models deliver AI capabilities, and top-layer applications and intelligent agents target specific business scenarios. Baidu provides all four layers.

The commercial value: clients don't need to source chips, cloud services, large models, and application development from four different vendors. One negotiation, lower integration difficulty, and clearer accountability when issues arise. For industries like finance, telecommunications, and energy—with strict data security requirements and accelerating import substitution—this logic holds real appeal.

But the truly noteworthy number in this report isn't the total but the growth structure.

Within AI cloud infrastructure, subscription revenue from AI accelerator infrastructure grew 143% year-on-year in Q4, accelerating from Q3's 128%.

AI accelerator infrastructure means enterprises purchase computing power from Baidu long-term for model training and operation—not one-time equipment purchases but ongoing service subscriptions. As long as enterprises run models, they use computing power, and bills continue. Unlike project-based revenue, subscriptions are stable and increase client dependency and migration costs.

For years, Baidu's presence in the cloud market seemed weak— Alibaba Cloud (Alibaba Cloud) and Huawei Cloud (Huawei Cloud) dominated public discourse. But this financial report shows AI cloud has become Baidu's most stable growth source. Management repeatedly emphasized subscription models and recurring revenue on the call, clearly signaling to the market: this will be a long-term business.

The other 10 billion yuan from AI-native marketing represents a harder-to-quantify opportunity.

Digital humans and enterprise intelligent agents are the main forms here—AI-generated virtual avatars for live commerce, online customer service, brand endorsements, etc. Financial data shows the number of digital humans live-streaming on Baidu's platform grew nearly 200% year-on-year in December 2025, while production costs for hyper-realistic digital humans dropped to about 1/3 of previous levels. Clients include JD.com, Zuoyebang, and TikTok.

This direction reflects real market demand—MCN agencies and brands are investing heavily in digital humans for cost reduction and efficiency gains.

But this capability is also rapidly commoditizing, with Kuaishou, ByteDance, and SenseTime offering similar product lines. Baidu's current competitive edge comes from Wenxin's generation quality and its existing enterprise client base. How deep this moat runs remains unclear at this stage.

Viewed together, a clear structural shift emerges.

Baidu is gradually shifting its revenue focus from traffic-driven to computing power-driven. The former risks user behavior changes; the latter risks capital intensity and competitive dynamics. Advertising is an asset-light, high-margin business; computing power is asset-heavy with longer payback periods. Their profit curves differ.

With 40 billion yuan in AI revenue accounting for 43% of Baidu's core business, its AI transformation on the B2B side is indeed happening. Baidu is earning money in the deep end but hasn't yet surfaced.

03

Kunlunxin: A Chip and the Calculus Behind It

If AI cloud is Baidu's transformation cash flow source, Kunlunxin resembles a strategic asset.

Management spoke cautiously about Kunlunxin on the earnings call. Positioned at the bottom of 'full-stack capabilities,' it was described as stable in performance, compatible, and already deployed at scale in finance, telecommunications, and energy. But the real focus isn't technical details—it's capital moves.

Baidu is advancing Kunlunxin's spin-off and listing.

Kunlunxin is Baidu's self-developed AI chip, with development spanning over a decade. Internally, it serves as the computing power foundation for Baidu's entire AI cloud system, supporting Wenxin model training and inference, and forms one of the base layers for Baidu's full-stack AI services to enterprises.

Against a backdrop of restricted NVIDIA GPU supplies and surging demand for domestic alternatives, Kunlunxin's strategic value has been revalued.

The logic for spinning it off, as management explained on the call, is straightforward: to give Kunlunxin an independent market valuation while unlocking asset value for Baidu.

This timing sends a notable signal. Baidu currently holds about 294.1 billion yuan in cash (total cash and investments)—sufficient scale, but its core advertising business keeps shrinking. Spinning off Kunlunxin not only prices its AI infrastructure business separately but also cashs in on asset valuation before cash flow pressures emerge.

Whether Kunlunxin can sustain an independent company's valuation remains uncertain.

In China's domestic AI chip track (sector), Huawei's Ascend has an earlier start and more complete ecosystem; Cambricon has been listed for years. Kunlunxin's advantage lies in its usage scenarios backed by Baidu's cloud and model businesses, but once operating independently, its ability to expand external clients beyond Baidu's ecosystem hangs as a question mark over this valuation logic.

04

Luobo Kuaipao: Baidu's Slowest-Growing Curve May Also Be the One That Goes the Farthest

Compared to Kunlunxin, Luobo Kuaipao is more tangible and easier for the public to understand.

By 2025, Luobo Kuaipao will have delivered over 10 million orders annually, with 3.4 million orders in the fourth quarter alone, representing a year-on-year increase of over 200%. Wuhan has achieved break-even for single-vehicle single-operation, making it one of the few players globally to reach this milestone in the Robotaxi sector.

The story of Luobo Kuaipao actually occupies only a small portion of this financial report, with a relatively small scale but a clear trend.

Globally, Robotaxi is a track (translated as 'sector' for context) heavily bet on by capital but also one where many players have been eliminated. Uber has exited, Lyft has exited, and Cruise suspended operations at the end of 2023 due to accidents. The main survivors globally are Waymo and Luobo Kuaipao. After Waymo completed a new round of financing in early February, its valuation once reached $126 billion, but it continues to incur losses; Luobo Kuaipao does not have an independent valuation, but its single-vehicle economics in Wuhan have broken even.

Figure/Luobo Kuaipao

Figure/Luobo Kuaipao

Cost is key. Baidu's self-developed RT6 model has a per-vehicle cost of less than $30,000, making it one of the lowest-cost solutions among globally mass-produced Robotaxis. The significance of this figure lies in the fact that lower costs reduce the financial threshold for scale expansion and bring the profitability inflection point closer.

In 2025, Luobo Kuaipao's international expansion accelerated significantly, covering 26 cities globally, including plans to launch in London in partnership with Uber, obtaining fully autonomous driving test permits in Dubai, entering the Seoul metropolitan area in South Korea, and expanding testing in Hong Kong. The advancement in these markets relies on an asset-light model of cooperation with local mobility platforms, where Baidu provides technology and vehicles, while Uber and Lyft provide order entry points and local operational experience.

These figures are sufficient to demonstrate that Luobo Kuaipao has become a scaled business.

But scale does not equal profit.

Autonomous driving is a typical capital-intensive path. Vehicles, operations, testing, and compliance all require capital at every step. Even if break-even is achieved in a single city, overall expansion still relies on continuous investment. The cumulative AI investment in the financial report exceeds 100 billion yuan, and investment intensity will continue in the future.

A more critical issue lies in the pace. Has the Robotaxi industry truly reached the commercialization inflection point? Waymo's high valuation gives the market room for imagination, but the industry is still in the verification stage. Baidu has advantages in technology and cost, but whether the industry's overall valuation can support long-term investment remains to be seen.

During the earnings call, management was asked whether they would consider spinning off Luobo Kuaipao as a separate entity, similar to Kunlunxin. The response was, 'We will remain flexible and evaluate the best path to maximize shareholder returns'—neither confirming nor denying.

Luobo Kuaipao and Kunlunxin share a commonality: both are businesses that Baidu has quietly invested in for over a decade, outside the public eye. Both also face the same issue: before reaching a sufficient scale, it is difficult for outsiders to provide an accurate valuation, and Baidu's overall market recognition has been consistently suppressed as a result.

This may be the most accurate description of Baidu's current situation: its presence on the consumer side continues to shrink, but the sectors it has bet on have not yet reached a point where winners and losers can be determined. The decline in advertising is a fact, the growth of AI cloud is a fact, and the undervaluation of Kunlunxin and Luobo Kuaipao is probably also a fact.

The question is no longer whether Baidu has a future, but whether the market is willing to wait and how long it will take for that future to materialize.

Header Image/Baidu Official Weibo

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once