Ford, Renault, and Geely: A Tripartite Strategic Interplay

03/03 2026

03/03 2026

588

588

After incurring a substantial $19.5 billion write-down in its electric vehicle (EV) business, Ford is recalibrating its strategic approach and seeking external platform collaborations. A cross-regional collaborative landscape is gradually taking shape, with potential three-way interactions among Ford, Renault, and Geely coming to the forefront.

Following the $19.5 billion write-down, Ford may appear to be under pressure at first glance. However, its subsequent actions are gradually dispelling the strategic ambiguity surrounding its external collaborations.

On February 10, Ford Motor Company released its financial results for the full year and fourth quarter of fiscal year 2025. The report revealed a net loss of $11.1 billion in the fourth quarter of 2025 and an annual loss of $8.2 billion, with a $19.5 billion asset write-down for its EV business that will span through 2027.

This represents Ford's worst annual loss since the 2008 financial crisis. The $19.5 billion write-down primarily reflects aggressive investments made in recent years in pure electric platform development, vehicle architecture redesign, battery production line construction, and software system development. Between 2021 and 2023, Ford publicly committed to investing over $50 billion in electrification by 2026 and planned to expand annual production capacity to over 2 million units.

Now, this expansion assumption has been forced to undergo a reassessment. In response, Ford has decided to halt production of certain F-150 Lightning variants (which had previously been suspended multiple times due to aluminum plant fires) and redirect capacity originally planned for large pure electric SUVs toward hybrid vehicle production. Some battery factories will be repurposed for energy storage equipment production. These moves indicate that while electrification investments have not been completely halted, their pace and priority have significantly diminished.

Ford CEO Jim Farley stated during the earnings call: "We must strike a balance between electrification investments and profitability realities. This is not abandoning electrification but making a rational adjustment to resource allocation."

Notably, in December 2025, Ford and Renault formally announced a strategic partnership to jointly develop small EVs for Europe based on Renault's pure electric business unit, Ampere, with plans to launch in 2028.

While aggressively writing down losses and proactively seeking external platform collaborations may seem contradictory, they represent two facets of the same strategy: shedding the burden of past high-leverage expansion and leveraging external resources to reduce future development costs and uncertainties.

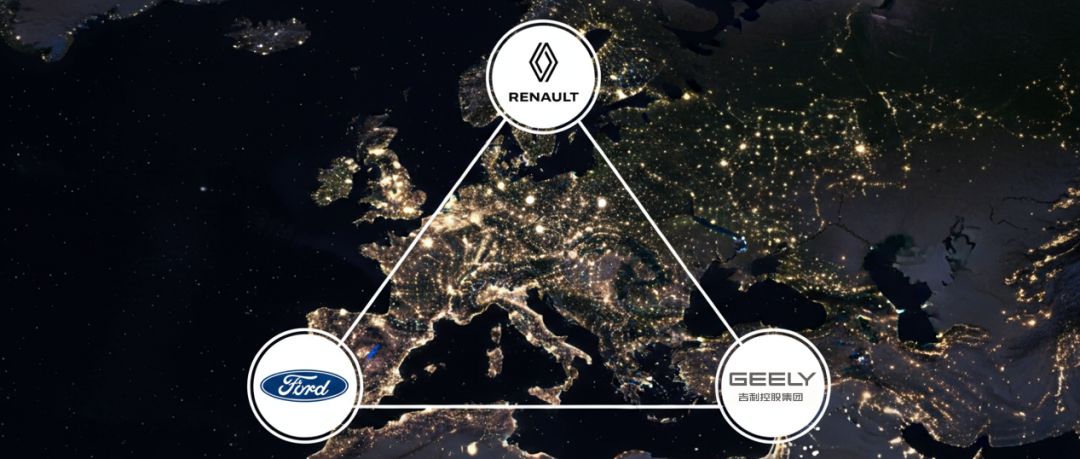

Taking a broader perspective, another underlying thread had already been set in motion. Before Ford's announcement, Renault had completed its internal restructuring, with Chinese automaker Geely playing a deeply involved role behind the scenes.

Ford's $19.5 billion write-down simply brought the already complex relationships among the three parties into the spotlight.

Ford's Strategic Choice: Leveraging External Strengths

To understand why Ford chose to partner with Renault, the perspective must shift back to Europe.

Before the 2035 internal combustion engine (ICE) vehicle ban target was adjusted, Europe had been one of the most aggressive regions globally in promoting electrification. Through stringent carbon emission regulations, clear timelines, and financial subsidy policies, Europe created a highly conducive external environment for the pure electric transition at the institutional level. By 2023, annual EV registrations in Europe approached 3 million, with EV penetration exceeding 50% in some Nordic countries.

Under this policy framework, "full electrification" was not just an industrial direction but a political commitment. Traditional automakers were compelled to cut ICE vehicle R&D budgets and accelerate capital and resource allocation toward pure electric platform development. European automakers universally increased electrification investment intensity, launching a new round of technological competition around battery supply chains, software systems, and platform architectures.

However, the situation changed markedly in 2025. The EU adjusted its 2035 ICE vehicle ban from "100% zero emissions" to "90% reduction," allowing the remaining 10% to be offset through low-carbon fuels, synthetic fuels, or hybrid solutions. While not reversing the decarbonization direction, this modification clearly signaled that the transition pace could be reassessed.

Around the same time, Europe's pure EV market growth began to slow. Consumer-side issues gradually emerged: charging infrastructure lagged behind sales growth, public charging prices rose, used EV residual values fluctuated sharply, purchase costs remained higher than equivalent ICE vehicles, and price sensitivity increased significantly after subsidy reductions. Meanwhile, Chinese brands accelerated their entry into Europe, creating dual price and technological pressures in segments like small EVs and compact SUVs. European automakers, already in transition pain, now faced a more complex competitive landscape.

Against this backdrop, Ford's position in Europe became particularly pragmatic. Its European market share stood at just around 5%, with its EV business yet to turn a profit. Independently developing a pure electric platform for Europe's small vehicle market would require massive R&D expenses, factory retrofitting costs, and marketing investments, with significant uncertainty around expected sales volumes and profitability timelines.

Thus, Ford chose to leverage Renault's Ampere platform. Designed specifically for small pure electric models, this platform has already undergone cost optimization and software ecosystem validation, enabling Ford to rapidly enter the sub-€20,000 price segment with relatively low incremental investment. The core of this move lies in cost-sharing, platform risk mitigation, and accelerated product time-to-market.

This cooperation marks the first link in the chain: Europe has transformed from the most aggressive "vanguard market" for electrification into a hub for cross-border industrial collaboration. Policy relaxation and demand slowdown have instead driven collaboration among traditional automakers and across regions.

Geely's Strategic Layout Behind Renault's Restructuring

Viewing Ford's partnership with Renault at face value might suggest a simple "European and American automakers huddling for warmth." However, Renault's strategic adjustments began well before Ford's involvement, with its internal restructuring logic far more complex than a single bilateral cooperation.

Since 2023, Renault has formally initiated business restructuring, dividing its operations along technological pathways and profit structures: on one hand, spinning off its pure electric business into Ampere to focus on pure electric platform architecture development, software-defined vehicle capabilities, and digital ecosystem construction; on the other, establishing a joint venture with Geely called Horse Powertrain for ICE and hybrid powertrain businesses, covering traditional ICE, hybrid, and even future hydrogen power systems.

Headquartered in London, Horse Powertrain operates 17 factories and 5 R&D centers globally, with an annual production capacity of 5 million powertrain systems. It is not a traditional engine supplier but a platform company providing comprehensive power solutions for the global market. Against the backdrop of temporarily slowed European pure electrification and resurgent hybrid demand, Horse Powertrain has become a crucial profit support and risk buffer for Renault during its transition.

Through this restructuring, Renault achieved risk isolation and structural optimization: separating capital-intensive, long-return-cycle, and highly volatile pure electric businesses from stable cash-flow ICE and hybrid operations, thereby reducing overall group financial volatility. Renault now follows a clear "dual-track strategy"—Ampere continues advancing technological breakthroughs and software capabilities along the pure electric route to maintain technological leadership in long-term electrification competition, while Horse maintains large-scale production and profitability, preserving strategic flexibility amid policy fluctuations and demand changes.

In this structure, Geely plays a pivotal role. Unlike some Chinese brands' export models focused primarily on sales expansion, Geely adopts a deeper "structural integration" approach. By participating in Horse's establishment, Geely directly enters Europe's traditional powertrain system as a core component. Simultaneously, through equity stakes in Renault Brazil and collaborative layouts with Renault's Korean factories, Geely gains manufacturing and channel foundations in South American and Asian emerging markets, further extending its global industrial network. Geely's advantages in hybrid system integration, supply chain scale effects, and cost control make it an indispensable partner in Renault's transition.

This completes the second link in the chain: Geely is no longer just an external competitor in Europe but has transformed into a systemic participant in Europe's power ecosystem, embedding itself at deeper industrial chain nodes.

Ford's Strategic Shift and the Emergence of a Triangular Structure

The dilemma Ford faces is not merely an individual operational fluctuation but broadly representative of the industry. Entering 2025, the U.S. policy environment saw periodic adjustments: some EV tax credit policies were canceled or tightened, and emissions regulation enforcement pace slowed. Against this backdrop, the policy-driven effect on pure EV models weakened, while hybrid and ICE vehicles demonstrated more stable short-term profitability.

However, from a longer-term perspective, the global decarbonization trend remains fundamentally unreversed. Regulatory directions, capital market expectations, and technological evolution paths still point toward low-carbon and electrification. For Ford, the real challenge lies in balancing short-term financial recovery with long-term strategic transformation: achieving "hemorrhage control" through product mix and investment pace adjustments while not losing its future position in electrification competition. Amid this superimposed uncertainty, sharing risks, reducing capital expenditures, and lowering technological trial-and-error costs through external cooperation have become more pragmatic choices.

Against this backdrop, a second critical variable emerges: potential contact between Ford and Geely. Entering 2026, media outlets like Reuters reported that Ford and Geely remain in early-stage discussions, with possible cooperation directions including technology sharing or production capacity collaboration for low-cost EVs, though no formal agreements have been announced.

If such cooperation materializes into substantive outcomes, a relatively complete triangular structure will gradually take shape:

First, between Geely and Renault, deep collaboration already exists in powertrain systems through the Horse Powertrain joint venture, with industrial synergies in Korean and South American (e.g., Brazilian) markets;

Second, between Renault and Ford, cooperation centers on developing small EVs in Europe using Renault's Ampere platform;

Third, if Geely-Ford cooperation materializes, direct links may form in low-cost EV production, core technology module sharing, and supply chain collaboration.

Under this structure, Ford not only indirectly accesses Chinese companies' capabilities in cost control and hybrid technology through Renault but may also establish direct collaborative relationships with Geely, forming a tighter global automotive value chain network. Brand boundaries remain distinct, but relationships among underlying platforms, powertrains, and manufacturing systems will exhibit higher degrees of interweaving.

Thus, the third link in this "interlocking strategy" begins to materialize: industrial cooperation evolves from bilateral models to triangular closed loops. The three companies maintain market competition while achieving resource sharing in technology, production capacity, and supply chains. Cross-regional, cross-factional collaboration deepens further.

What Might a Triangular Closed Loop Imply?

If Ford and Geely ultimately reach substantive cooperation, its impact will extend beyond single models or regional markets, affecting the global automotive industry's value chain landscape. Key implications can be divided into several layers:

First, the loosening of technological boundaries will become one of the most direct changes. If Ford incorporates Geely's systemic capabilities in new energy core platforms or key technology modules, this will substantially impact the long-standing "technological sovereignty" logic dominated by multinational automakers. Traditionally, these automakers emphasized vertical integration and autonomous control, striving for internal closed loops from platform architectures to powertrains. Under the new cooperation framework, cross-enterprise, cross-regional platform co-creation and technology sharing may become the norm. Technology will no longer strictly belong to single brands but become shared resources within multi-party collaborative networks.

Second, the role of European platforms will face reevaluation. Renault's Ampere, originally positioned as the core carrier of Europe's electrification transition, will see its "central" status redefined if it serves both Ford and synergizes with Geely's low-cost manufacturing systems. On one hand, platform utilization rates could significantly rise, amortizing R&D and fixed asset costs; on the other, negotiations around platform pricing power, intellectual property ownership, and revenue distribution mechanisms will become more complex. Platforms will cease to be mere technological carriers but become key nodes for balancing multi-party interests.

Thirdly, price systems may undergo structural downturns. Geely's cost advantages in supply chain integration and large-scale production, once integrated into the systems of mainstream European and American brands, could drive the prices of small electric vehicles (EVs) even lower. This will not only reshape the competitive landscape in the end-market but also influence the bargaining power and profit distribution mechanisms of upstream component suppliers. Consequently, the global small EV market may enter a phase of even fiercer cost competition.

At the same time, the complexity of geopolitical and regulatory environments will increase. Cross-regional cooperation necessitates addressing tariff barriers, local production ratio mandates, data security concerns, subsidy eligibility criteria, and other institutional challenges. To comply with regulatory requirements across different jurisdictions, companies may need to establish more intricate joint venture structures, data isolation protocols, and technology licensing frameworks. This indicates that value chain reconfiguration is not merely a commercial endeavor but also a challenge involving institutional coordination and compliance management.

Finally, Geely's position within the global industrial system will undergo a significant upgrade. Unlike its previous global expansion through capital operations, such as acquiring Volvo and investing in Mercedes-Benz, this move likely signifies a deeper level of technological and systemic integration. Once the triangular closed-loop system is established, the powertrains, platform architectures, and even overall cost structures of certain Ford or Renault models may incorporate Geely's technological contributions and revenue-sharing models. While brand identities will remain distinct under national flags, value creation and profit flows will transcend traditional factional boundaries.

From Factions to Efficiency: A Logical Evolution

Ford's $19.5 billion write-down marks the conclusion of its initial phase in the electrification race. Renault's dual-track restructuring represents a structural self-rescue effort amid uncertain environments. Geely's embedded globalization signifies the transformation of Chinese automakers from mere competitors to systemic participants. These three threads intertwine to form an 'interlocking strategy.' The electrification process has not ended but has shifted from a 'speed race' to a 'cost race.' Over the past decade, the industry has debated who would lead in new energy; in the coming decade, the truly pivotal question may be: who can integrate into more systems and become cross-regional connection nodes.

Amid an environment characterized by policy fluctuations and profit pressures, cooperation has emerged as a more rational choice. Ford is no longer pursuing expansion alone, Renault is no longer solely betting on pure electric vehicles, and Geely is no longer just an external competitor. The global automotive value chain is transitioning from vertical integration to horizontal collaboration, marked by platform sharing and risk sharing.

The sequence of events may have only just begun. Perhaps a fourth party is already observing the right moment to join the fray.

Note: This article was first published in the "Global Perspective" column of the March 2026 issue of Auto Review magazine. Please stay tuned for more updates.

Image: Sourced from the Internet

Article: Auto Review

Layout: Auto Review

-

![]()

Buying Jimeng and Getting Doubao for Free? Decoding the Pricing Strategy of ByteDance's AI Services

-

![]()

Robot Sets New Human Record in Half Marathon: Honor’s AI Ecosystem Strategy Hits Milestone

-

![]()

Who are the key players in the WiFi6 chip market, both visible and behind the scenes?

-

![]()

Doubao to Start Charging: Without Transparent Pricing, How Can There Be Competition?

-

![]()

What is the recovery timeline for Microsoft after the breakup?

-

![]()

Who is Most Panicked by Doubao's Charging Model?

-

![]()

OpenAI Surprises Apple: Doubao Phone Emerges as the 'Trailblazer'

-

![]()

There's No Such Thing as a Truly Free Doubao