Large Model Suffers 360% Loss, Yet MiniMax Remains a 'Hot Pick'?

03/03 2026

03/03 2026

462

462

The Old Guard Fades, New Stars Shine! Today, Minimax, a Hong Kong-listed 'hot pick' and China's independent model provider, unveiled its 2025 full-year results! However, in contrast to its stock price soaring 4.5 times in two months, its Q4 performance fell short. Here are the key highlights:

I. Revenue: C-side Growth Slows, B-side Surges—Is the Structure Improving?

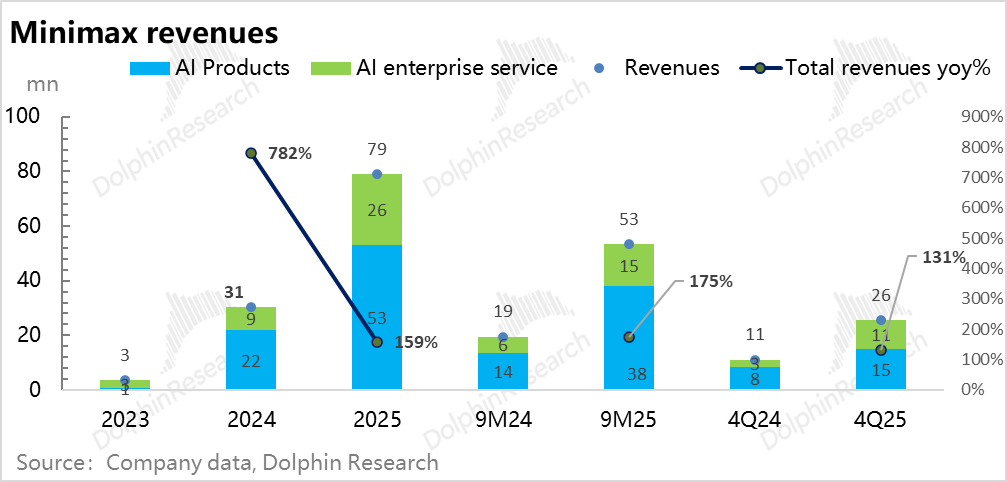

1) Revenue Growth Moderates:

The 2025 revenue reached $79 million, marking a nearly 160% YoY increase, which still appears robust. However, given that Q1-Q3 revenue was already disclosed, Q4 revenue stood at approximately $26 million, with growth decelerating from 175% in H1 to 130%, indicating a clear slowdown.

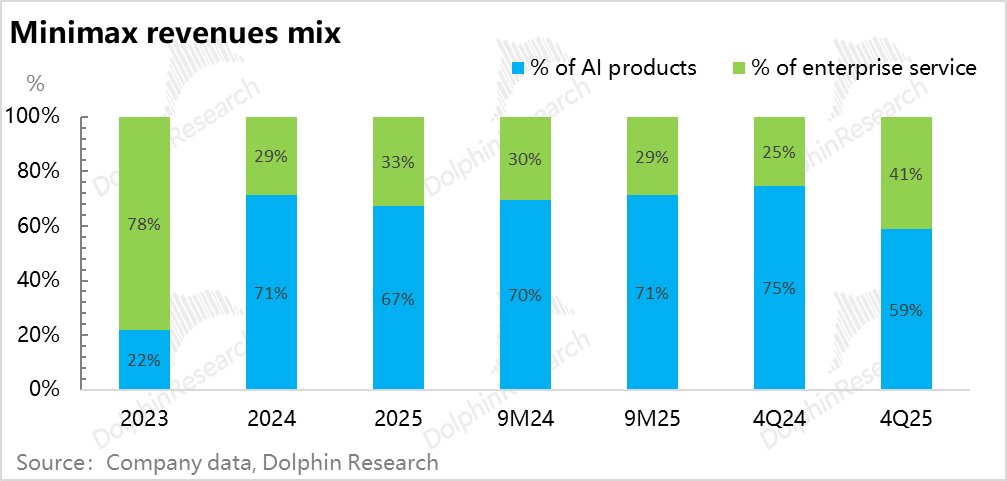

2) C-side Declines, B-side Rises: Is the 'Models-as-Revenue' Strategy Working?

Minimax is the sole Chinese large model company with a strong C-side presence but a relatively weaker B-side footprint. Critics argue that its 'models-as-products' competitiveness is underwhelming. Yet, the Q4 results demonstrate that with robust core model capabilities, monetization on both B and C sides can be achieved!

a. Minimax's AI product suite (including Minimax, video-gen Conch AI, audio-gen Minimax Audio, and Talkie—primarily driven by Talkie and Conch AI) generated just over $15 million in revenue, with growth halving from ~150% in H1 to 82%, the main contributor to the slowdown.

b. Meanwhile, enterprise services (APIs, etc.) accelerated from 160% growth in H1 to 278% in Q4, surpassing $10.55 million in a single quarter. Given no acceleration in overseas revenue, it's reasonable to deduce that both domestic and international enterprise clients are increasing their API usage.

As API revenue essentially monetizes 'models-as-revenue,' its growth signals that enterprises are validating the model's 'cost-performance' as a standalone product.

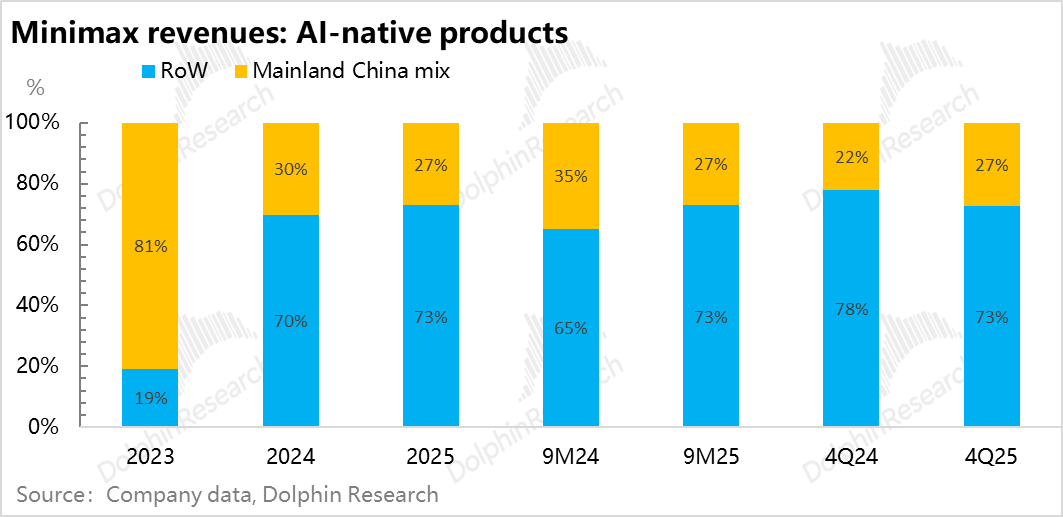

3) Overseas Revenue Remains Stable at 73%:

MiniMax's overseas revenue (from the U.S., Singapore, and other regions) is evenly distributed. After rising to 73% in H1, driven by Conch AI, it held steady—no further increase.

Nonetheless, both API call volumes on OpenRouter and actual revenue (73% overseas) confirm MiniMax as a successful Chinese model exporter.

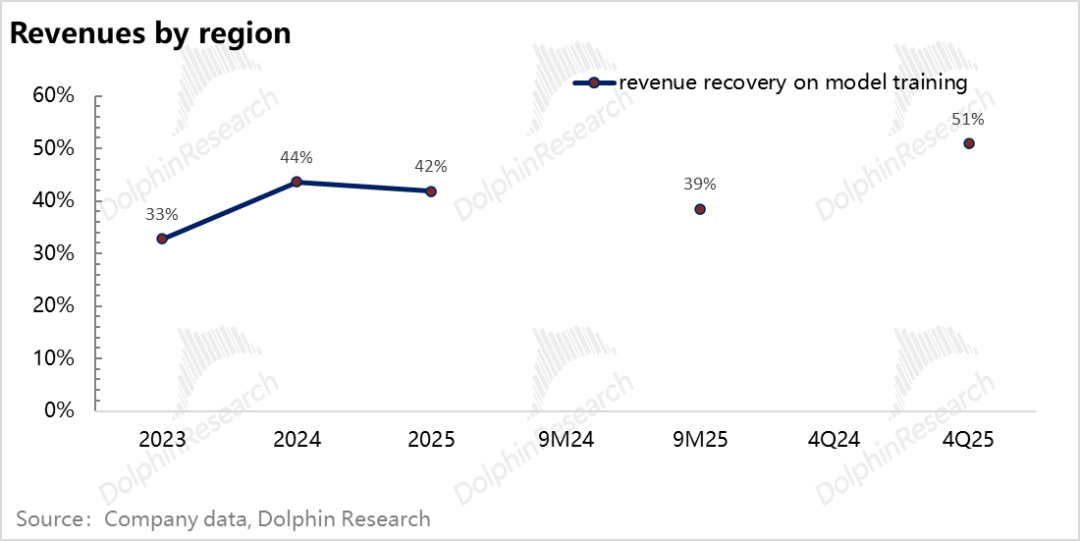

4) Can Revenue Cover Prior Model Training Costs?

Base models are updated annually, meaning a model trained over a year has just a one-year service life. Thus, model economics can be partially assessed by comparing its direct/indirect revenue against the prior year's training investment.

For MiniMax, despite rapid revenue growth, the 2025 revenue coverage of 2024's training costs actually declined. Clearly, until models reach maturity, competition remains fierce.

Of course, financing can bridge gaps, but future model deployment and monetization capabilities will become increasingly critical. Model providers must generate revenue faster and more stably than their peers to prove their value.

Assuming a Q4 revenue base of $26 million and quarterly growth of $8 million (Dolphin Research's estimate), 2026 revenue could exceed $130 million, maintaining ~50% coverage of 2025's $250 million R&D investment—similar to Q4's ratio.

II. Enterprise Services: Price Cuts to Capture Market Share?

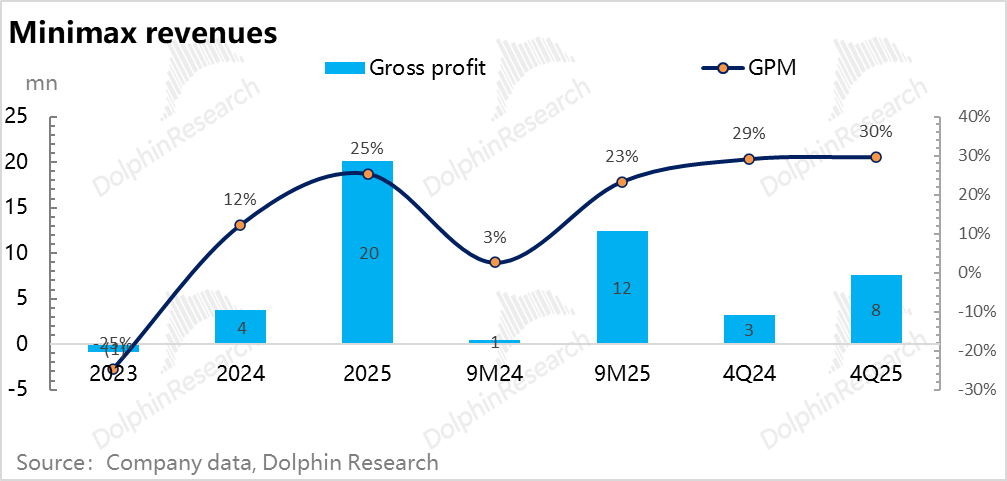

Enterprise services boast higher gross margins (Token inference cloud costs vs. Minimax's Token pricing), with API clients typically paying, yielding margins >60% (nearly 70% in H1).

However, Q4's overall gross margin only rose to 30% from 23% in H1, despite enterprise services' rising share. The full-year margin was 25% on $20 million revenue.

Assuming C-side margins improved from 4.7% to 5% with rising pay rates, enterprise margins likely fell to ~65%.

This decline suggests MiniMax is commercializing API services post-IPO, aiming to balance B and C-side growth.

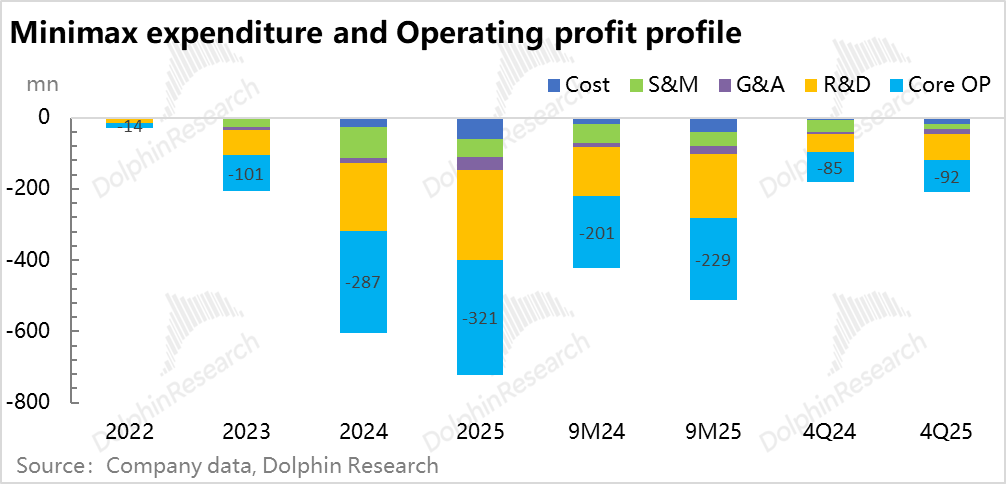

III. $26M Revenue, $92M Loss: Still Among the Least Unprofitable

Large models appear decent on gross margin, but training—the biggest cost—is buried in R&D expenses (3-5x revenue). As long as models iterate rapidly via training, profitability is unlikely (click for reasons). Q4 R&D spending (mostly training) hit $72.5 million, 2.8x quarterly revenue.

Even with sales expenses plunging (-63% YoY—management recognizes AI growth hinges on model strength, not mobile-era user acquisition) and low admin costs (assuming modest growth excluding IPO-related stock compensation), operating losses reached $92 million, 3.6x revenue.

Full-year operating losses hit $320 million, or $290 million excluding stock compensation and IPO costs—still a 370% loss ratio, though an improvement from 429% in H1.

By our tracking, this is exceptional cost control among Chinese large models.

Media-reported ~$1.9 billion net loss is noise, driven by $1.6 billion in non-cash losses from convertible debt conversion at inflated valuations during IPO. Ignore it.

Dolphin Research's View: Still a Long-Term 'Hot Pick'!

After doubling on IPO (Jan 9, 2026), surging another 60% by February (Chinese New Year season), MiniMax's stock is now 4.5 times its IPO price in under a quarter.

Based solely on Q4 2025 results—compared to IPO filings' H1 data—there’s no 'wow' factor.

The structural bright spot is enterprise services (APIs, etc.). As a C-side-heavy AI company, MiniMax is now doubling down on B-side growth. While this involved pricing concessions, rapid B-side growth proves its 'models-as-products' offer sufficient 'cost-performance' to attract enterprises amid fierce competition.

The growth slowdown stems from AI product revenue deceleration. With no operating metrics disclosed, we infer that AI-native C-side products like Talkie relied on model iterations and virality for user growth, not marketing budgets. But Q4 lacked base model upgrades, so user pay rates didn’t spike.

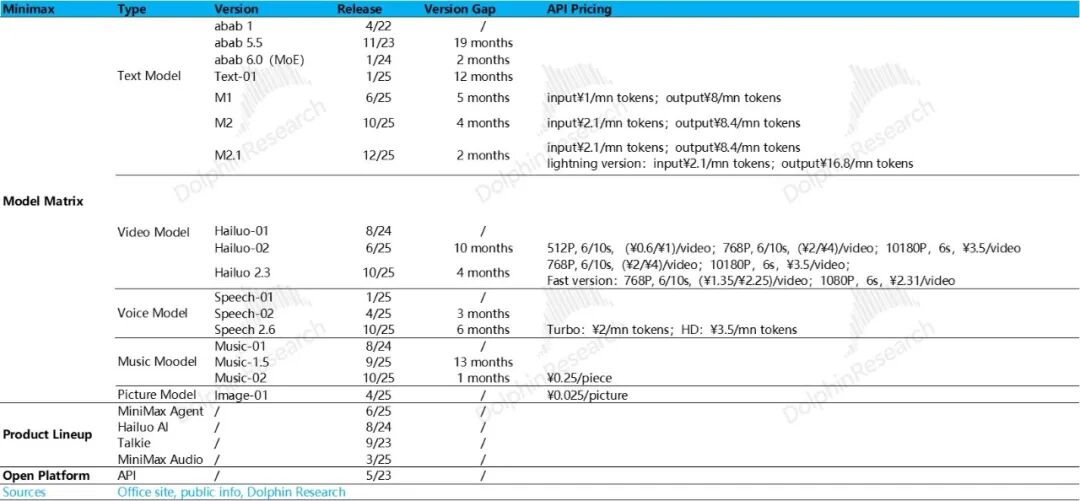

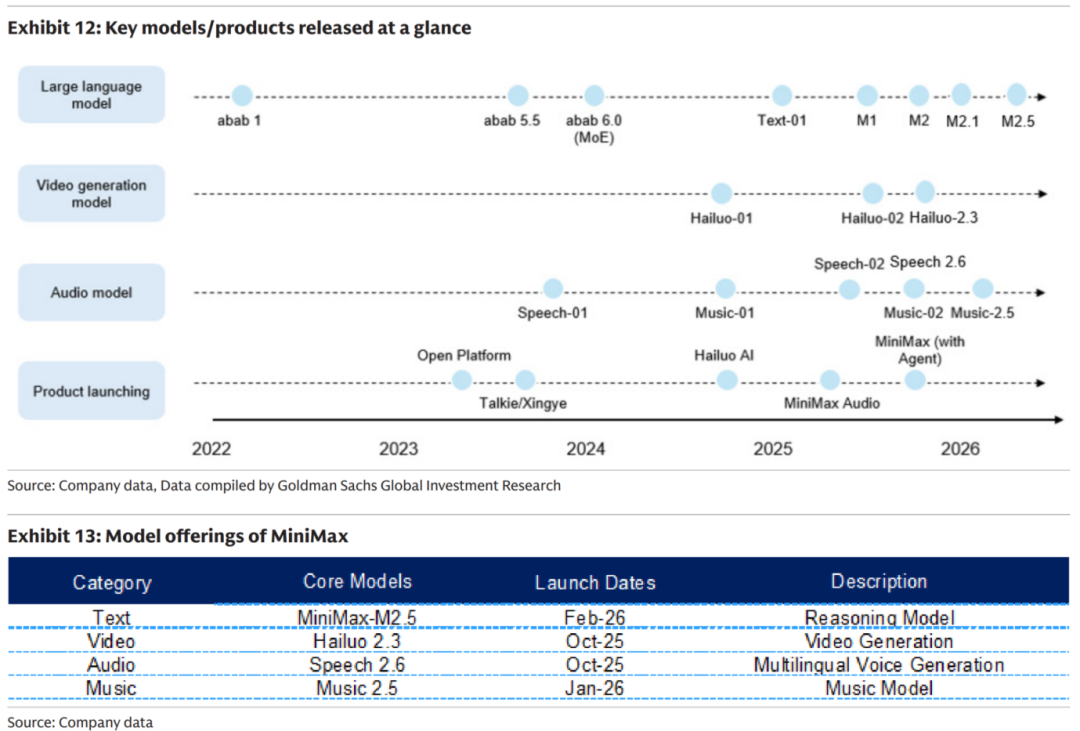

From a model roadmap perspective, Q4 results no longer reflect fundamentals:

Since Q4 2025, all modalities have iterated rapidly, culminating in the February 2026 M2.5 base model, which introduces Agent capabilities for coding, tool integration, and office scenarios—aiming to transform AI from 'assistant' to 'AI colleague.'

Meanwhile, MiniMax integrated OpenClaw (a hot Agent platform), driving Token usage sharply higher. Latest data:

a. MiniMax M2 text model's daily Token consumption in February 2026 is 6 times December 2025's level.

b. Coding Plan Token usage surged 10 times MoM.

The February 2026 rally primarily reflects M2.5 adoption expectations, with 6 times MoM Token growth proving its success.

Short-term, MiniMax's stock may correct post-model launch, especially as open-source rival DeepSeek prepares a new base model (likely focusing on coding/Agents). MiniMax could face selling pressure amid this offset leadership.

In the long run, beyond model intelligence, independent model providers must compete on R&D efficiency, cash resilience, and product execution.

First, cash reserves: The $700 million IPO raise left MiniMax with ~$1 billion in cash/equivalents by Q4 2025. Even if next-gen models require higher investment than 2025's $250 million, funding is secure.

In 2025, MiniMax generated ~$80 million in revenue with 428 employees and $250 million in training costs—a globally leading model with outstanding efficiency. It’s among the few Chinese providers excelling in model iteration, monetization, and execution.

- END -

// Reprint Policy

This article is original to Dolphin Research. Reprints require authorization.

// Disclaimer and General Disclosure

This report is for general data reference only, intended for users of Dolphin Research and its affiliates. It does not consider individual investment objectives, product preferences, risk tolerance, financial status, or special needs. Investors must consult independent professionals before acting on this report. Any investment decisions based on this report are at your own risk. Dolphin Research disclaims liability for direct/indirect losses from using this report's data. Information is based on public sources and provided 'as is' without guarantees of reliability, accuracy, or completeness.

Nothing herein constitutes an offer to sell or solicitation to buy securities in any jurisdiction, nor investment advice, bids, or recommendations. This report's data, tools, and materials are not intended for distribution in jurisdictions where such distribution would violate applicable laws or require Dolphin Research/its affiliates to register or obtain licenses. Residents of such jurisdictions must comply with local regulations.

This report reflects the personal views, insights, and analytical methods of its authors, not the stance of Dolphin Research or its affiliates.

Produced by Dolphin Research. Copyright reserved. No entity or individual may (i) reproduce, copy, duplicate, reprint, forward, or create derivatives in any form, or (ii) redistribute/transfer to unauthorized parties without Dolphin Research's prior written consent. All rights reserved.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once