Off-season Challenge! February Auto Market Dynamics Shift Again: SAIC and Geely Maintain Leads, BYD's Exports Surge, New Forces Face Intense Reshuffle

03/03 2026

03/03 2026

522

522

As March begins, major automakers have started releasing their February sales figures. This month, coinciding with the 'longest-ever Chinese New Year holiday,' had only 16 effective working days, compounded by the early release of pre-holiday consumer demand. China's auto market faced a genuine off-season stress test.

As expected, most automakers saw month-on-month sales declines, but market differentiation became more pronounced: Among established players, SAIC, Geely, and BYD held the top three positions. Geely achieved slight year-on-year growth against the trend, while BYD opened up new growth space through exports.

The new forces sector witnessed a major reshuffle. HiMode continued to lead, Leapmotor surpassed Xiaomi to rank second, and XPeng's sales nearly halved year-on-year, placing it at the bottom. The 20,000+ sales mark has become the survival threshold for new forces.

The contrasting performances in February's auto market not only validated the industry rule of 'true strength revealed in off-seasons' but also foreshadowed even fiercer competition in China's auto market in 2026.

Established Automakers Maintain Top Positions: Geely Grows Against Trend, BYD's Exports Surpass Domestic Sales

Despite the Spring Festival slowdown, the ranking of leading auto groups remained consistent with January. SAIC, Geely, and BYD secured the top three sales positions, though each demonstrated unique growth highlights, with overseas markets serving as a common growth engine.

SAIC Group reported February sales of 269,465 units, down 8.6% year-on-year, but its overseas performance remained strong with 99,024 exports, surging 46.1% year-on-year, consolidating its global layout advantages.

For January-February results, SAIC's self-owned brands sold 401,000 units, up 14% year-on-year, accounting for 67.2% of group sales—a 4.3 percentage point increase from last year. SAIC Passenger Vehicles sold 139,000 units (+44.8% YoY), SAIC Maxus sold 33,000 units (+4.4% YoY), and SAIC-GM-Wuling sold 206,000 units, maintaining growth momentum.

Geely Automobile became the only top-tier group to achieve positive year-on-year growth, selling 206,160 units in February (+0.6% YoY), demonstrating strong resilience during the slowdown. Its new energy segment performed exceptionally well with 117,488 units sold (+19% YoY), while overseas exports doubled to 60,879 units. Strong performance from its premium brands drove Geely's growth: Zeekr delivered 23,867 units in February, achieving both year-on-year and month-on-month growth (+70% YoY); Lynk & Co sold 27,359 units (-5.3% MoM but +58.7% YoY). Together, these brands propelled Zeekr Technology's growth by over 60% year-on-year, solidifying their position in Geely's brand matrix.

More importantly, Geely Automobile Group maintained its lead over BYD in February, increasing the likelihood that Geely will claim China's auto market leadership in 2026.

BYD sold 190,190 units in February (-35.8% YoY, -9% MoM), though it maintained significant scale advantages with 187,782 passenger vehicles sold. BYD's standout performance came from overseas markets: passenger vehicle and pickup exports reached 100,151 units (+41.4% YoY), surpassing domestic sales for the first time and demonstrating the effectiveness of its globalization strategy. Meanwhile, its premium brand lineup continued to gain traction: Fangchengbao sold 17,036 units (+244.7% YoY), and Yangwang sold 232 units (+121% YoY), progressively implementing its premium strategy.

Additionally, other automakers like Chery and Great Wall also performed variably during the slowdown. Chery Group sold 160,765 units in February, with exports accounting for over 70% (124,929 units, +41.5% YoY). Great Wall Motor sold 72,594 units total, with 42,675 overseas units (+37.4% YoY), and its WEY brand grew 54.1% YoY, becoming a standout performer.

Among joint-venture brands, GAC Toyota, Dongfeng Honda, and Zhengzhou Nissan achieved positive year-on-year growth against the trend. Zhengzhou Nissan sold 4,531 units in February (+57.5% YoY), with 1,535 new energy vehicles sold (+95.5% MoM), performing exceptionally well.

New Forces Sector Sees Major Reshuffle: Leapmotor Overtakes Xiaomi, XPeng Finishes Last

Compared to the steady changes among established automakers, the new forces sector underwent dramatic restructuring in February. Month-on-month declines became widespread, but year-on-year performances varied sharply, intensifying differentiation. HiMode, Leapmotor, and Li Auto ranked top three, while Xiaomi's sales nearly halved and XPeng became the only new force with significant year-on-year decline.

HiMode continued to dominate new force sales rankings, delivering approximately 18,000 units in February (+20% YoY) based on stable Aito series performance, maintaining steady growth during the slowdown and leading the new forces sector.

Leapmotor achieved counter-trend growth, delivering 28,067 units in February (-12.5% MoM but +11% YoY), surpassing Xiaomi to rank second among new forces and becoming the most resilient new force brand during the slowdown. Its cost advantages from full-domain self-research and balanced product matrix covering the mainstream 100,000-yuan market stabilized orders far better than peers.

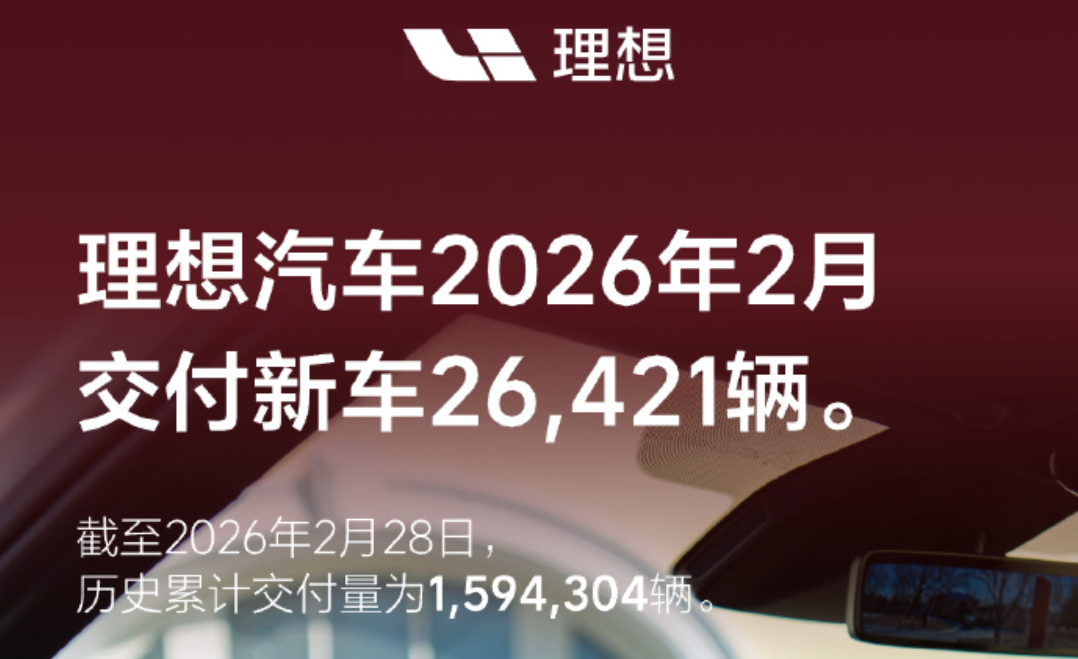

Li Auto maintained its consistent robust (robust) style, delivering 26,421 units in February (-4.5% MoM but +0.6% YoY become a full-time employee ), experiencing the smallest month-on-month decline among top new forces. Its product barriers built around family users and continuously improving charging network layout maintained strong market competitiveness during the slowdown. The upcoming L9 Livis model is expected to further enhance its technological attributes and boost sales to new heights.

NIO emerged as the year-on-year growth 'dark horse' among new forces in February, delivering 20,797 new vehicles (-23.5% MoM but +57.6% YoY). The blockbuster performance of the new ES8 served as the core driver, contributing 54% of sales. Combined with the gradual activation of NIO, Ledo, and Firefly's multi-brand matrix, NIO's product cycle is reaching an upward inflection point.

In stark contrast, Xiaomi Auto and XPeng Motors performed poorly. Xiaomi Auto delivered over 20,000 units in February, nearly halving from January's over 39,000 units (-48.7% MoM), sliding from second to fifth among new forces. Lei Jun previously explained that with only the YU7 model currently available (as the new SU7 awaits launch), product transition combined with the Spring Festival slowdown caused the sales plunge. The new SU7's market performance will directly determine Xiaomi's future trajectory.

XPeng Motors became the 'laggard' among new forces in February, delivering only 15,256 new vehicles (-49.9% YoY, -23.8% MoM), ranking last and becoming the only mainstream new force with significant year-on-year decline. Product gaps from main model iterations and delayed order conversions are core issues, but with the X9 pure electric version and VLA intelligent driving system launching in early March, XPeng's product and technology cycles are expected to shift, potentially repair (recovering) sales.

February Auto Market Reflects Industry Trends: Exports and Product Strength Become Core Competitiveness

The February 2026 off-season exam for the auto market not only revealed automakers' true capabilities but also reflected three key development trends in China's auto industry:

First, overseas markets have become automakers' second growth engine, with export volumes directly determining risk resilience during slowdowns. BYD's exports surpassing domestic sales, along with significant export growth for SAIC, Geely, and Chery, proves that globalization has become essential. Automakers that seize overseas opportunities will gain competitive initiative.

Second, product strength and product cycles have become key sales drivers. Geely Zeekr and NIO's growth stemmed from blockbuster models' sustained performance, while Xiaomi and XPeng's declines resulted from product transition gaps. In an increasingly competitive market, only by continuously building strong product strength and managing iteration rhythms can automakers maintain growth.

Finally, the industry's survival-of-the-fittest competition is intensifying, with concentration at the top becoming more pronounced. Among established automakers, SAIC, Geely, and BYD's lead continues to widen. In the new forces sector, the 20,000+ sales mark has become a clear survival threshold. Automakers below this level face immense pressure, while top new forces leverage scale advantages and brand barriers to capture market share, further accentuating the Matthew effect.

From January's shifting dynamics to February's off-season exam, competition in China's 2026 auto market has reached white-hot intensity. BYD no longer dominates alone as Geely, SAIC, and other established players continue to gain momentum, while the new forces sector faces intense reshuffling. No company can rest on its laurels. In this fierce competition, only those focusing on product strength and globalization while continuously innovating can gain a foothold and win the future in the rapidly evolving auto market.

-

![]()

Buying Jimeng and Getting Doubao for Free? Decoding the Pricing Strategy of ByteDance's AI Services

-

![]()

Robot Sets New Human Record in Half Marathon: Honor’s AI Ecosystem Strategy Hits Milestone

-

![]()

Who are the key players in the WiFi6 chip market, both visible and behind the scenes?

-

![]()

Doubao to Start Charging: Without Transparent Pricing, How Can There Be Competition?

-

![]()

What is the recovery timeline for Microsoft after the breakup?

-

![]()

Who is Most Panicked by Doubao's Charging Model?

-

![]()

OpenAI Surprises Apple: Doubao Phone Emerges as the 'Trailblazer'

-

![]()

There's No Such Thing as a Truly Free Doubao