The More Popular OpenClaw Is, The Happier MiniMax and Its Peers Are

03/03 2026

03/03 2026

468

468

"We are firmly not building a general-purpose personal assistant for mobile." said Yan Junjie.

Author I He Jian

Editor I Wang Bin

Cover I MiniMax Official Website

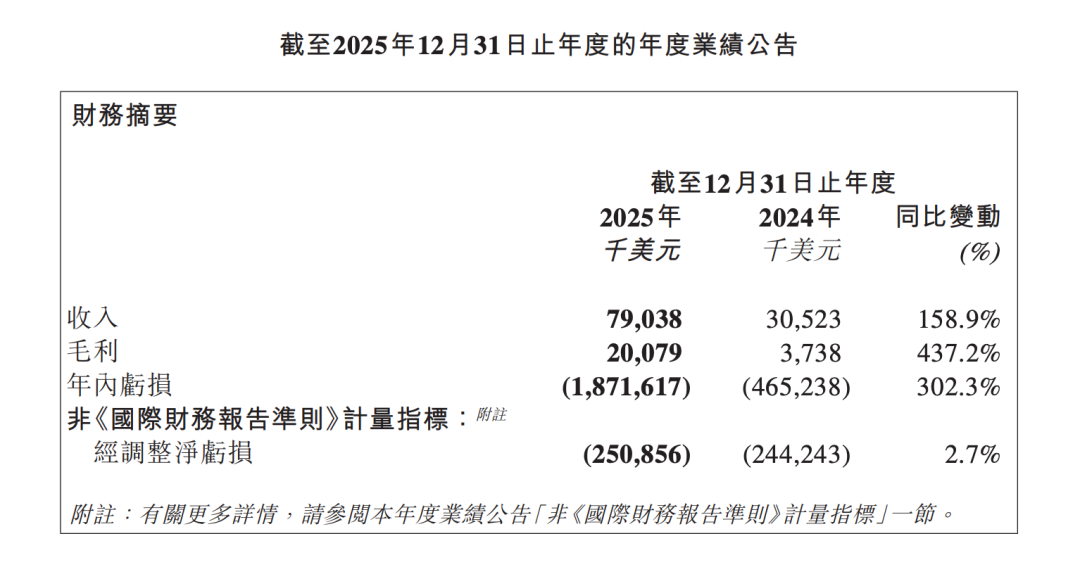

Chinese large model company MiniMax disclosed its full-year 2025 financial results on March 2, marking its first annual report since going public.

The financial report showed that MiniMax's 2025 revenue increased by 158.9% YoY to $79.038 million, with gross profit rising by 437.2% YoY to $20.079 million. However, MiniMax also saw a significant increase in losses during the same period, recording a loss of approximately $1.872 billion for the year, a 302.3% YoY expansion.

MiniMax 2025 Annual Financial Report

The enlarged loss primarily stemmed from fair value losses on financial liabilities. In 2024, the company recorded a loss of $214 million in this category, but it surged to $1.59 billion in 2025. MiniMax stated that the change was mainly due to the continuous increase in the company's valuation, resulting in significant remeasurement losses on preferred shares.

Setting aside these noisy accounting metrics and measuring by adjusted net loss, MiniMax's adjusted net loss in 2025 was $250 million, roughly in line with the previous year's $244 million.

During the first post-IPO earnings call, MiniMax founder and CEO Yan Junjie continued to project confidence. He offered three predictions for 2026: further advancement in the intelligence level of AI programming, a significant increase in the penetration of AI agents in the office sector, and the emergence of multimodal creation capable of directly producing deliverable medium-to-long-form content.

The underlying message of these predictions is that market demand for Tokens will experience exponential growth—Yan's exact words were "growth of one to two orders of magnitude." A substantial increase in Token consumption implies a continuous surge in MiniMax's revenue. Yan stated that MiniMax will transition from a large model company to a platform company in the AI era.

On January 9 of this year, MiniMax went public on the Hong Kong Stock Exchange's main board, becoming one of only two listed large model companies in the Hong Kong market. Its stock price has repeatedly climbed, accumulating approximately 140% growth since listing.

Following yesterday's financial report release, MiniMax's stock price reached a high of over HK$905 today, at one point surpassing Kuaishou and Ctrip, and approaching JD.com in market capitalization.

Beneficiary of Global Token Consumption Surge

The financial reports of large model companies are perhaps the most straightforward and easy-to-understand in the market, as their business models are simple and operations uncomplicated. As long as the model capabilities are strong enough and the user base sufficiently large, the company's revenue and profits can sustain continuous growth.

Like most large model startups, MiniMax has maintained high revenue growth rates over the past few years, though the pace has begun to slow. The company commenced commercialization in 2023, with revenue soaring by 782.2% YoY in 2024, but slowing to 158.9% YoY in 2025.

In Q4 2025 specifically, based on a simple calculation of revenue from the first three quarters as disclosed in MiniMax's prospectus, MiniMax's Q4 revenue reached $25.601 million, up approximately 131.3% YoY. While this growth rate marked a clear slowdown from the roughly 175% YoY increase in the first three quarters of 2025, it still exceeded market expectations.

The primary reason for the revenue growth slowdown was a deceleration in subscription revenue growth from MiniMax's consumer (C)-end business, which has a larger base and accounts for a greater share of annual revenue.

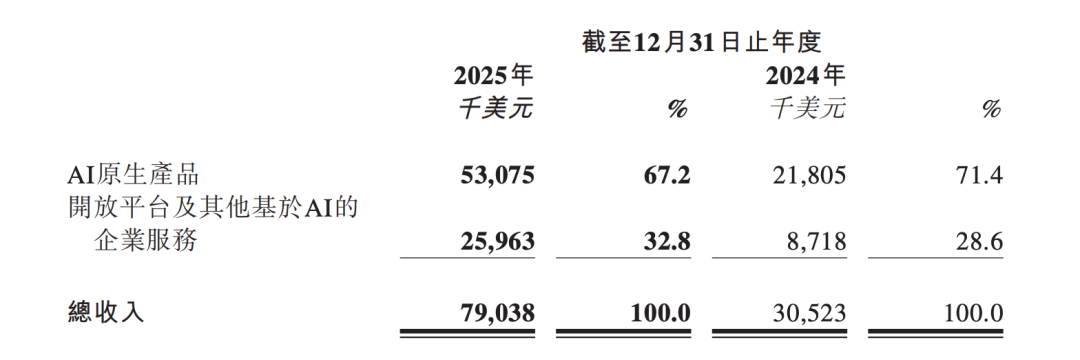

MiniMax categorizes its revenue sources into two main segments: "AI-native products" and "open platform and other AI-based enterprise services," corresponding to the C-end and B-end, respectively. "AI-native products" include subscription services for AI-native applications such as MiniMax, MiniMax Voice, Conch AI, and Talkie/Xingye, while "open platform and other AI-based enterprise services" primarily consist of API interface revenue calculated based on Token usage.

MiniMax 2025 Annual Financial Report

In Q4 2025, MiniMax's revenue from AI-native products was $15.055 million, up approximately 81.9% YoY, compared to an approximately 181% YoY increase in the first three quarters of the year. In contrast, API interface revenue calculated based on Token usage grew faster, reaching $10.546 million in Q4 2025, up approximately 277.6% YoY, compared to a 160.2% YoY increase in the first three quarters.

On an annual basis, MiniMax's subscription revenue from the C-end increased by 143.4% YoY to $53.1 million in 2025, while API interface revenue from the B-end rose by 197.8% YoY to $26 million. The C-end revenue share decreased by 4.2 percentage points YoY to 67.2%, with the B-end revenue share exceeding 30% at 32.8%.

The increase in Token consumption to some extent represents market recognition of the model's capabilities. In Q4 last year, MiniMax's large language model M-series, video model Conch series, and voice model Speech series all received updates.

In February this year, MiniMax released its latest flagship model, M2.5, claiming it achieves global top-tier performance in productivity scenarios such as programming, tool invocation, and office applications. MiniMax stated that the average daily Token consumption of the M2-series text model in February this year increased more than sixfold compared to December 2025, with Token consumption from programming packages surging over tenfold. Yan said MiniMax's ARR (Annual Recurring Revenue) exceeded $150 million in February this year.

MiniMax's M2.5 model still has a slight performance gap compared to top overseas models but comes at a lower cost. MiniMax stated that under the condition of outputting 100 Tokens per second, M2.5 requires only $1 for one hour of continuous operation, and only $0.3 for outputting 50 Tokens per second.

Low Token prices have long been an advantage for Chinese open-source models, especially following the rise of the OpenClaw trend earlier this year. Yan introduced during the earnings call that on the AI model API aggregation platform OpenRouter website, M2.5 has topped the charts for two consecutive weeks since its release. Additionally, API call volumes for models including Moonshot AI's Kimi K2.5, Zhipu's GLM-5, DeepSeek-V3.2, and Alibaba's QianWen series have all surged.

MiniMax Launches MaxClaw

During the earnings call, Yan specifically mentioned the popularity of the OpenClaw project, noting that well before OpenClaw became a hit, its founder Peter Steinberger had highly praised MiniMax's models, considering them his top choice for the best open-source models.

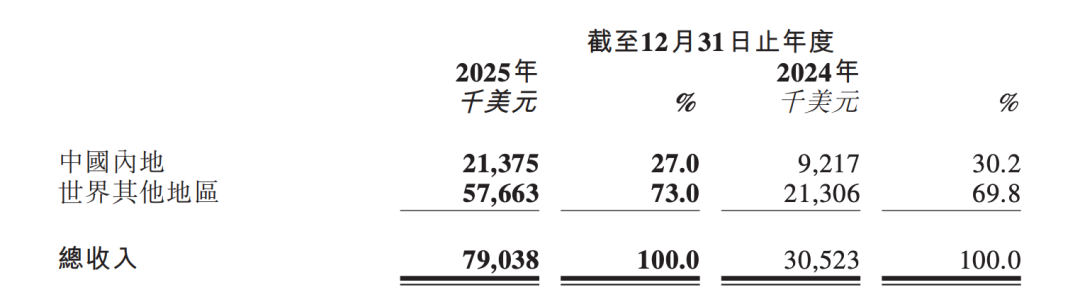

MiniMax Revenue Share from Mainland China and Overseas

Throughout 2025, MiniMax's share of overseas revenue further increased, rising from 69.8% in 2024 to 73%, while revenue from mainland China decreased from 30.2% to 27%.

Aspiring to Become a Platform Company in the AI Era

MiniMax and Zhipu are currently the only two large model companies listed in the capital markets. Even though both companies faced criticism for their substantial losses when they first disclosed their prospectus data, the capital markets remain highly optimistic about the prospects and future of large model companies.

Since their listings, both MiniMax and Zhipu have seen their stock prices soar. As of noon on March 3, MiniMax's stock price had accumulated approximately 140% growth, while Zhipu's had risen by about 300%.

During the earnings call, Yan projected that the intelligence level of models will continue to improve in 2026.

First, the programming field will see the emergence of L4 to L5-level intelligence, transitioning from tools to collaborative partners. Second, the office sector will replicate the rapid progress seen in programming last year, with AI agents significantly enhancing their delivery capabilities and penetration rates in office applications. Third, multimodal creation will move toward directly producing deliverable medium-to-long-form content, even approaching more stream-like, real-time output forms.

Yan stated that this means market demand for MiniMax will further amplify, with Token volumes likely experiencing growth of one to two orders of magnitude.

Building on this, Yan proposed a new positioning, stating that MiniMax is advancing from a large model company to a platform company in the AI era.

"Platform companies in the internet era served as entry points for traffic, whereas platform companies in the AI era, we believe, are organizations that define and drive new intelligence paradigms while enjoying paradigm-related benefits in products and commerce. This will depend on the ability to define intelligence paradigms, innovate in technology and products, and possess scalable infrastructure and efficient Token throughput capabilities."

"The value of a platform company in the AI era can be simply estimated as the density of intelligence provided multiplied by Token throughput. When both are sufficiently strong, the platform's value will naturally emerge," Yan said.

Analysts expressed skepticism about Yan's new company positioning, especially considering that numerous internet giants are also heavily investing in AI. They questioned how MiniMax, as a startup, has the opportunity to grow into a platform company.

Yan responded that AI is not currently a market defined by Stock game (existing market competition), as annual growth far exceeds the existing market size. Additionally, AI is not a winner-takes-all market; as long as a company has its own innovations and uniqueness, it will have opportunities.

Yan believes MiniMax holds significant differentiated advantages over competitors. For example, from its inception, the company bet on multimodal models, continuously enhancing the models' intelligence density and boundaries to create unique value, and then developing products and businesses around that unique value.

Yan said they "choose what to do and what not to do." For instance, in 2023, they firmly decided not to develop a general-purpose personal AI assistant for mobile or dialogue products similar to Doubao or ChatGPT, as they believed they could not create unique value in such products.

Like most large model companies, MiniMax remains in the red. Excluding substantial losses caused by non-operational items, MiniMax's adjusted loss in 2025 was $250 million, roughly in line with the previous year's $244 million, representing a roughly 2.7% YoY increase in losses. During the same period, MiniMax's gross margin improved from 12.2% in 2024 to 25.4% in 2025.

Large model companies primarily allocate their expenditures to R&D. Last year, MiniMax's development expenses increased by 33.8% YoY to $253 million. MiniMax emphasized in its financial report, "Our YoY increase in R&D expenses was far lower than the 158.9% revenue growth rate, proving that our R&D efficiency has improved."

However, MiniMax's asset-liability ratio continues to rise. The asset-liability ratio, calculated by dividing total liabilities by total assets at period-end, measures a company's leverage level and solvency risk. As of December 31, 2025, MiniMax's asset-liability ratio stood at 343.3%, compared to 187.8% at the end of the previous year.

© All rights reserved by Shanshang. No reproduction without authorization.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once