The Humanoid Robot Boom: Abundant Capital, Yet Haste Leads to Waste

03/06 2026

03/06 2026

447

447

Emerging within two or three years and aiming for public listing after raising RMB 3-5 billion—an opportunity that most people may never encounter in their lifetime is now unfolding in batches within the humanoid robot sector.

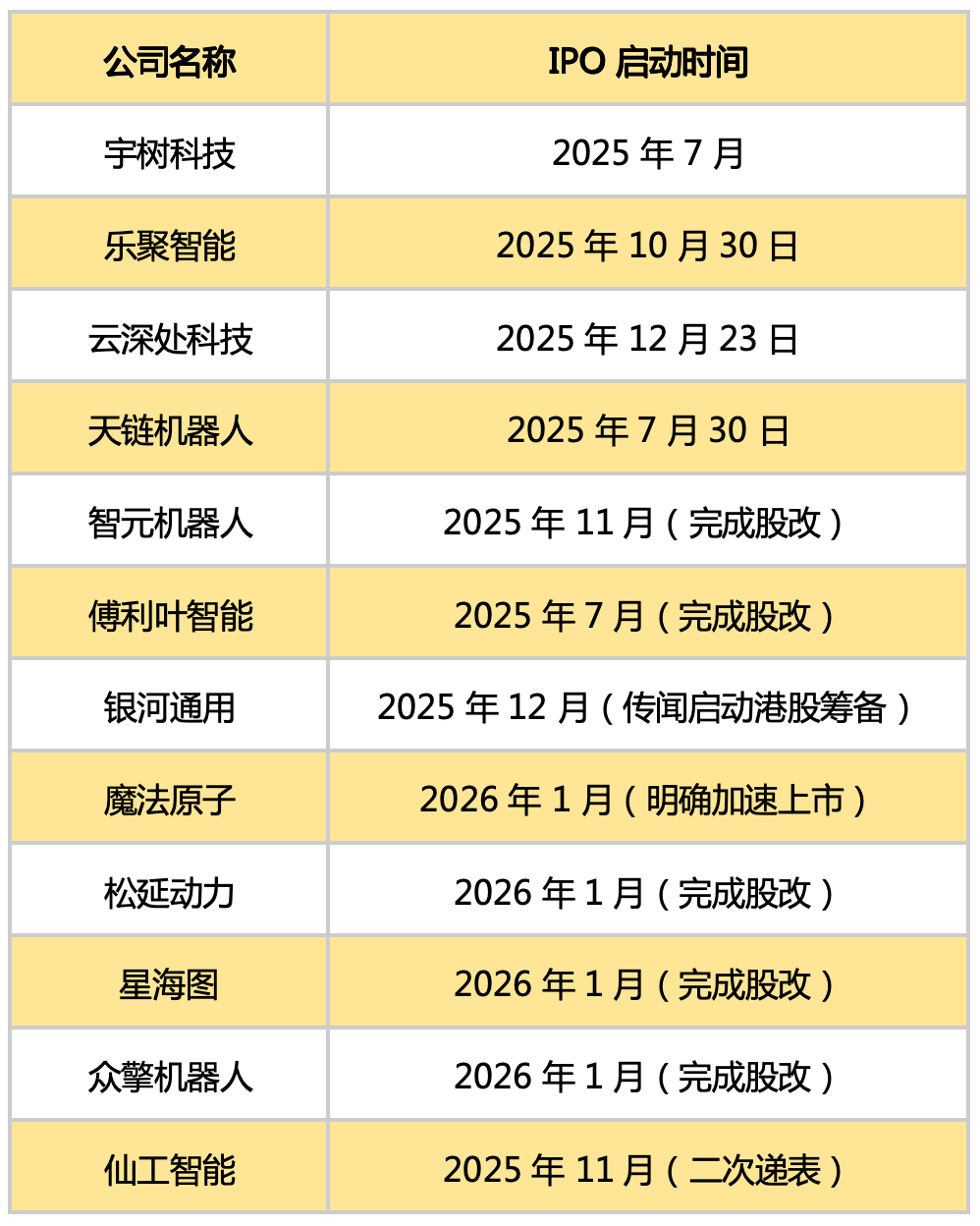

Just in the past week, Zhipingfang and Qianxun Intelligence secured financing almost simultaneously, with one raising RMB 1 billion and the other RMB 2 billion. Moreover, regarding IPOs, at least 10 humanoid robot companies have been preparing to go public in the past six months.

When it comes to financing, an investor who has been closely following this field lamented, "In the past, raising RMB 10 billion might have taken five years. Now, it could be accomplished in just two."

The same can be said for IPOs. Historical records for the "fastest time to go public" may soon be shattered by humanoid robot companies one after another.

No bubble, no opportunity. Behind these frenzied fundraisings, is it the result of collective anxiety or a technological leap?

- 01 -

The Anxiety Driving the Frenzy

Financing for humanoid robots is surging, with capital flowing in faster than ever.

In the past 1-2 months, several young companies, established for just three to five years, have secured financing, typically amounting to billions of yuan.

Zhipingfang, founded three years ago, recently raised RMB 1 billion. Qianxun Intelligence, founded two years ago, raised RMB 2 billion. Zibianliang Robotics, also founded two years ago, raised over a billion yuan.

In this wave, Tsingzhi Capital has also invested in Zhipingfang. Tsingzhi Capital made an early foray into embodied intelligence, with investment projects covering almost all aspects of the industry, such as the brain, cerebellum, and body motion control modules. It has a profound understanding of the current boom.

Zhipingfang's robot at work (Source: Zhipingfang's official WeChat account)

Founding partner Zhang Yu lamented, "Everything in the industry is accelerating. In the past, raising RMB 10 billion might have taken five years. Now, it could be done in just two."

This acceleration is driven by capital anxiety and the desire for quick exits. This is not necessarily a bad thing; it's just normal profit-driven behavior.

Zhang said that over the past year, many embodied intelligence companies have grown tenfold or even more. From an order perspective, the industry has prospects and potential, but it has not yet translated into actual, specific applications or fully replaced human labor.

Nevertheless, everyone is still willing to push forward excessively, which defies normal logic. This indicates that some capital is anxious and hopes to cash out quickly in the short term.

Zhang described a phenomenon to Pencil News.

"Since the pandemic, a significant number of funds are nearing their expiration dates. Many of their invested projects are in a precarious state with long exit cycles. Embodied intelligence companies, however, have shorter listing cycles and faster exits. They hope to use this wave of listings to withdraw their previously invested funds and reinvest in new projects."

The listing cycle for embodied intelligence is indeed short.

Take Zhiyuan Robotics as an example. Founded in 2023, it rapidly secured financing over the next two years. Last July, it acquired the listed company SWancor, completing a backdoor listing—all within just two years and seven months.

Even in the internet era, this record would be considered lightning-fast.

In 2010, Jumei Optimal went public in four years and two months, breaking the internet's shortest listing record. In 2016, Qutoutiao went public in the U.S. in two years and three months, setting a new record.

History never repeats itself simply, but it often rhymes—this scene is now replayed in today's humanoid robot sector.

Zhiyuan Robotics is just the beginning.

Xinghaitu, founded in 2024, completed its shareholding reform in January 2026 and is expected to go public this year; Yinhang General, founded in 2023 with a valuation exceeding RMB 20 billion, is preparing for a Hong Kong listing. Qianxun Intelligence and Zibianliang Robotics, which recently secured financing, are also preparing to go public.

These facts validate the earlier conclusion: Embodied intelligence develops and lists quickly, satisfying capital's need for rapid exits.

Why is this channel so fast? Zhang analyzed that it is a special channel influenced by policy factors. No one knows when these policies will end, so everyone is rushing to cross the bridge before it’s too late, even if the technology isn’t fully ready.

- 02 -

The Financing Race

This financing race has two consequences: one is the anxiety it induces among entrepreneurs due to capital pressure; the other is the Matthew effect.

When capital becomes anxious, entrepreneurs follow suit. "Why? Money is scarce, so you must secure financing quickly. If others raise funds and go public first, you may not be able to list for years."

In this context, enthusiasm surges, leading to a financing race: A planned five-year listing timeline might be compressed to two years. As a result, companies may prepare to go public even without clear application scenarios or validated commercialization capabilities for their products.

Thus, a rare scene in financing history is unfolding today.

In past star sectors, two to three funding rounds per year for leading players were considered impressive. In the humanoid robot sector, leading players can secure seven to eight rounds annually, each exceeding RMB 100 million. And this is not an isolated case but a recurring phenomenon.

In terms of IPOs, Pencil News found through public records that over 10 humanoid robot companies have been preparing for IPOs in the past six months.

Another consequence of the financing race is the Matthew effect, where the strong get stronger, making it harder for new players to secure funding.

Once leading companies emerge, more money flows toward them, propelling them to list quickly. Meanwhile, many smaller companies may be left behind, facing even greater difficulties in securing financing.

Zhang noted that these leading companies often share common traits: They are founded by entrepreneurs from major firms embarking on second ventures.

"Capital trusts these entrepreneurs more because they have already navigated the path and can quickly rise to the top, not just based on technical capabilities."

Zhang told Pencil News that among the dozens of dexterous hand startups in the past six months, very few have secured funding. For the over ten embodied intelligence companies established each month, the success rate in securing financing has dropped significantly.

- 03 -

Rushing to Go Public: Who Will Buy the Products?

Of course, capital anxiety is just one accelerating factor. Zhang Yizhe, founding partner of Yonggui Fund, said that embodied intelligence has not just heated up recently but has been popular for two to three years. However, the current "heat" feels different.

The turning point might be Q3 2025.

"In the first half of last year, people were still excited, with many optimistic visions and high enthusiasm at both primary and secondary levels. But by Q3, everyone gradually calmed down and began to ponder a crucial question: Where are the application scenarios for humanoid robots or embodied intelligence?"

To put it more bluntly, previous capital stories emphasized emotional value, like singing and dancing. Now, it's time to deliver: securing orders and rushing to go public.

Qianxun's robot is already operational at CATL's Zhongzhou base (Source: Qianxun's official WeChat account)

But without orders, how can one go public? Zhang recalled history: Domestically, the earliest humanoid robot companies were not the well-known Unitree Robotics or Zhiyuan Robotics but companies like UBTECH and Fourier.

UBTECH went public on the Hong Kong Stock Exchange in 2023, which was good. However, humanoid robots accounted for less than 1% of its orders, with most revenue coming from non-humanoid products like educational, logistics, and consumer robots.

Fourier has not yet gone public, but the U.S. is reportedly an important market, with overseas orders growing rapidly. This reveals another path for Chinese robot companies.

Without clear historical precedents, where are the orders and listing opportunities for domestic robots today?

Zhang said that as of February 20, 2026, 488 companies are queued for listing on the Hong Kong Stock Exchange, including many robot companies, reflecting a certain industry mentality.

"In this context, if companies rush to capitalize on secondary market enthusiasm and 'exit for the sake of exiting,' it may lead to distorted actions, undermining the industry's steady development and preventing the sector from meeting expectations," Zhang said.

- 04 -

Real Application Scenarios

Steady development is the long-term path, and some domestic companies are exploring real orders for humanoid robots.

Zhang Yu from Tsingzhi Capital observed that companies like Zhipingfang and Qianxun have increasingly clear business models. "For example, they often secure industrial orders from major corporations."

Take Zhipingfang as an example. According to media reports, the company has made two key breakthroughs:

1. Signed a contract with semiconductor display leader HKC to supply over 1,000 robots within three years, potentially exceeding RMB 500 million in value.

2. Its products have been scaled for use in leading companies across industries such as automotive, biotechnology, and semiconductors.

A significant value of humanoid robots lies in industrial applications, which are now nearing reality.

Zhang said three conditions must be met for robots to enter factories:

1. Fine motor skills. Some robots or embodied robotic arms now achieve millimeter-level precision.

2. Long-duration task execution. They can complete end-to-end tasks in a chain rather than following step-by-step commands.

3. Autonomous planning and feedback. Within limited scenarios, they can plan tasks autonomously, correct errors, and provide flexible feedback.

Of course, beyond product technology, there is an economic calculation: cost-effectiveness.

"We generally believe that when a robot's price drops to 1.8 times the annual salary of a human worker, cost-effectiveness is achieved."

How was this 1.8x figure estimated?

Zhang explained that a worker typically works eight hours a day, requires breaks, provides emotional value, and incurs management costs and social security expenses. After accounting for these factors, robot costs become acceptable.

Beyond robot morphology and industrial applications, Zhang also sees potential in specialized scenarios. "For example, power grids, firefighting, and sanitation. These dangerous, polluted, or high-intensity environments unsuitable for humans will likely be the first to be replaced by robots."

Of course, there is no industry-wide consensus on investing in humanoid robots.

Zhang Yizhe from Yonggui Fund admitted that despite the market's fervor, they are not in a hurry to invest.

"We have invested in some embodied intelligence companies, such as Flexiv and Aitun Robotics, both performing well in industrial and service scenarios," Zhang said. "Refining robots' human-like capabilities to solve general tasks is our core investment rationale."

In his view, humanoid robots are not yet a direction for rapid commercialization. However, precisely because they are "not yet mature," the entire supply chain still holds numerous opportunities.

A FA agency that has long focused on robots told Pencil News that for many entrepreneurs, new opportunities in humanoid robots lie in the supply chain rather than in complete machines, such as vision-tactile skin sensors and dexterous hands.

Similar financing cases are not uncommon.

In the vision-tactile sensor field, PaXini secured hundreds of millions of yuan in Series A and A1 funding (2024). Its multi-dimensional tactile sensors are already used in dexterous robot operations.

Additionally, Taishan Tech received strategic investments from Xiaomi and Ledong Robotics, focusing on AI tactile perception chips.

In short, where there is a bubble, there is opportunity. Humanoid robots are currently a hub of opportunities.

This article does not constitute any investment advice.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once