The First Year of Robots 'Soaring': Hot Money, Tales, and a Future at Risk of Overextension

03/09 2026

03/09 2026

675

675

Author | Yugu

Disclaimer | The featured image is sourced from the internet. This original article by Jingzhe Institute cannot be reproduced without prior application and approval.

When robots from four Chinese companies made a concerted appearance on the stage of the 2026 Spring Festival Gala, it was evident that the tech world would be enthralled by the 'humanoid robots' trend throughout the year.

Since the start of the year, numerous robotics companies have swiftly announced financing news, with valuations of humanoid robot firms skyrocketing. Meanwhile, 'robot dances' have become a regular feature at offline events such as Spring Festival temple fairs and shopping mall openings. It appears that robots are rapidly transitioning from laboratories to factories, shopping malls, and public spaces.

However, does the superficial excitement equate to genuine industry prosperity? Are the soaring financing figures and growing order volumes indicators of technological maturity, or merely the result of temporary emotional fervor? As capital pours in, companies intensify their strategic layouts, and public discourse continues to heat up, perhaps we need to pause and pose some critical questions: Is the robotics industry truly at a turning point of robust growth?

Capital Influx Propels Humanoid Robots to the Forefront of Investments

As the saying goes, 'The duck knows first when the spring river warms up.' Even before the Spring Festival Gala became a 'robot conference,' the capital market had already 'predicted' the sustained explosion of the robotics sector.

Industry statistics reveal that from the start of 2026 to February 11, the domestic embodied intelligence sector witnessed 19 financing events in just 42 days, averaging one financing every 2.3 days, with disclosed funding exceeding 7.6 billion yuan. The high exposure from the Spring Festival Gala further bolstered capital confidence in the sector.

On March 2, Songyan Dynamics and Galaxy General, which had successfully debuted on the Spring Festival Gala stage, disclosed their financing progress on the same day. Among them, Songyan Dynamics completed a nearly 1 billion yuan Series B financing, while Galaxy General's new round of financing reached 2.5 billion yuan. On the same day, UniX AI also announced the completion of a new round of equity financing worth nearly 300 million yuan.

*Songyan Dynamics robot in the Spring Festival Gala sketch 'Grandma's Favorite'

According to third-party data, as of March 4, 2026, a total of 88 financing events had been disclosed in China's embodied intelligence sector, averaging about 1.4 financings per day, with a combined funding amount exceeding 20 billion yuan.

A closer look at this financing wave reveals that investors in robotics companies include not only leading VC firms, industrial capital, and state-owned funds but also frontline institutions such as Sequoia China, Hillhouse Capital, Yunfeng Capital, and Baidu Ventures. Even the National Artificial Intelligence Industry Investment Fund and multiple local state-owned platforms have made significant entries, heavily betting on leading enterprises and rapidly driving up the valuations of many star companies.

During a search of public reports, Jingzhe Institute found that as of March 5, 2026, there were already nine companies in the domestic embodied intelligence sector valued at over 10 billion yuan, including Unitree Technology, Zhiyuan Robotics, Zhipingfang, Xinghaitu, Lingxin Qiaoshou, Shenji Technology, Qianxun Intelligence, Galaxy General, and Xingdong Era. Among them, Shenji Technology, Qianxun Intelligence, Galaxy General, and Xingdong Era all joined the 'unicorn' ranks after accepting new rounds of financing since February.

Additionally, many startups less than a year old have smoothly completed angel and Pre-A round financings, easily securing hundreds of millions of yuan—a financing speed and scale extremely rare in other hard tech sectors, reminiscent of the investment frenzy under the 'Mass Entrepreneurship and Innovation' slogan a decade ago.

In fact, capital fervor stems from the fundamental logic of technological investment and boundless imagination about the industry's future. Currently, humanoid robots are widely seen as the next disruptive hardware terminal after smartphones. Optimistically, it is believed that humanoid robots will eventually penetrate vast scenarios such as industrial production, household services, commercial reception, and special operations. Based on this grand vision, the future industrial scale of humanoid robots is expected to surpass trillions of yuan.

Meanwhile, the simultaneous boom in the AI sector and ongoing technological iterations have made embodied intelligence a crucial pivot and carrier for AI industry implementation. The accelerated pace of tech giants investing in the AI arms race has also stimulated market FOMO (Fear of Missing Out), leading to heavy investments in humanoid robots as the 'ultimate form of AI,' even if profitability remains distant. The goal is to secure a high-priced 'ticket' for a chance to win in the future.

However, capital revelry often obscures the industry's fundamental issues. While everyone discusses the future and envisions prospects, few pay attention to the core contradiction: Have these robotics companies with massive financing achieved large-scale commercial implementation? Have they mastered stable and sustainable profit models? As the saying goes, 'A minute on stage takes ten years of practice offstage.' Beyond the national exposure from the Spring Festival Gala and the lofty expectations from the capital market, how much genuine capability do humanoid robots possess?

Profitable Robots 'Don't Look Human'

If capital's blind fervor remains harmless to ordinary people, the 'collective deviation' in the robotics sector is somewhat puzzling—guided by the halo of the popular new concept of embodied intelligence, many companies have rushed headlong into the 'humanoid robot' direction. Yet, the ones truly achieving large-scale mass production, stable profitability, and creating tangible industrial value are non-humanoid robots.

According to the International Federation of Robotics (IFR)'s 'World Robotics Report 2025,' China retained its position as the world's largest industrial robot market in 2024, accounting for 54% of global new installations. China not only installed 295,000 new industrial robots, setting an annual record, but Chinese manufacturers also surpassed foreign suppliers in domestic market sales for the first time. National Bureau of Statistics data shows that in 2025, industrial robot output in scale-above industries reached 773,000 units, up 28% year-on-year.

Long before humanoid robots became Spring Festival Gala stars, non-humanoid products like handling robotic arms, welding robots, palletizing robots, and AGVs had already achieved bulk implementation and commercial closure in core fields such as automotive manufacturing, 3C electronics, logistics warehousing, and new energy production, becoming the cornerstone of manufacturing transformation and upgrading.

In contrast, highly touted humanoid robots in public reports seem concentrated in demonstration-heavy scenarios like scientific research, education, or exhibition halls. This raises two profound questions: What tangible value do humanoid robots bring? Must robots be human-shaped to be considered cutting-edge?

First, it must be clarified that the strategic direction of humanoid robots is sound.

Since the Ministry of Industry and Information Technology released the 'Guidelines on Innovative Development of Humanoid Robots' in 2023, explicitly pursuing the 'large model + robot' approach, humanoid robots have become another hot tech sector parallel to AI. By 2024, OpenAI's collaboration with Figure to launch Figure 1, a humanoid robot equipped with a large model, captured global attention.

In 2025, embodied intelligence was written into the government work report for the first time, becoming a core sector of the country's future industries. During the same period, the entry of the National Integrated Circuit Industry Investment Fund explicitly endorsed embodied intelligence as a new strategic-level productive force at the national level, marking the sector's formal transition from 'frontier exploration' to national-level strategic deployment and large-scale implementation.

However, after humanoid robots broke into the mainstream via the Spring Festival Gala and became a national topic, the waters of embodied intelligence grew murky.

Amid cries of 'AI materialization' and 'next-generation productivity revolution,' opportunistic companies emerged, focusing on making prototypes, seeking attention, and riding the hype. This speculative chaos resembles the 'hundred-model battle' in China's large model sector after ChatGPT's explosion in 2023.

Recently, Fu Sheng, Chairman and CEO of Cheetah Mobile, mentioned in an interview that the robotics startup craze is fueled by two factors: easy access to financing and low technical barriers. According to him, within Shenzhen's mature supply chain, investing 2 million yuan suffices to customize a basic walking humanoid robot prototype, slap on a proprietary brand logo, and declare entry into the humanoid robot sector—all to pitch to capital for financing.

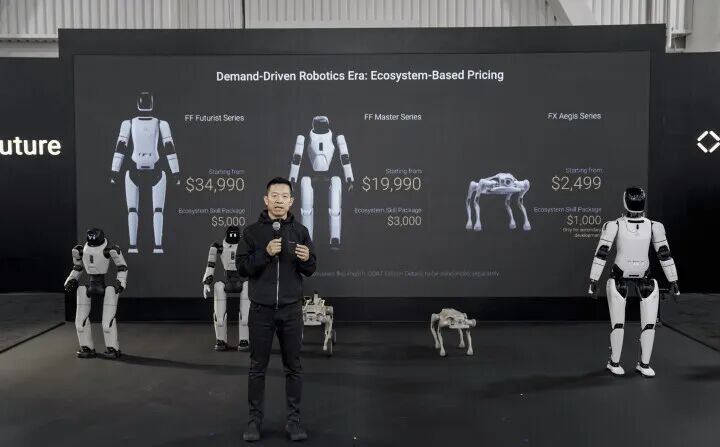

Similarly, in February this year, Faraday Future founder Jia Yueting high-profiled launched a so-called 'self-developed humanoid robot.' However, the entire event showcased only a 20-second video of basic walking, with no disclosure of core technical parameters, mass production timelines, or practical application scenarios.

After the event, multiple tech media outlets compared and found that Jia Yueting's Master series humanoid robot closely resembled Zhiyuan Robotics' previously released Lingxi X2, with nearly identical core parameters. This raised doubts that his true aim was not technological R&D but leveraging the hype for financing and shifting debt pressures, replicating the old path of 'PPT car-making.'

*Image source: Faraday Future official website

Some netizens humorously pointed out that Faraday Future's wholly-owned robotics subsidiary was only established in January, yet it unveiled three robot products on February 5. The intervening month was likely spent not on technical development or testing but waiting for humanoid robots shipped from Shenzhen while 'self-developing' the PPT. One netizen quipped: 'Going from PPT to product in a month is the limit of express logistics, not embodied intelligence.'

Narrative 'Front-Running' Creates Industry Bubbles

In reality, another underlying reason for the robotics startup craze is that on the 'large model + humanoid robot' embodied intelligence tech route, compared to the high barriers of large model R&D requiring massive computational power, long-term training, and rigorous evaluation, the 'assembly-style entrepreneurship' shortcut in humanoid robots is too obvious, artificially lowering the speculative threshold and leading to chaos.

Additionally, current public discourse on robots has deviated from the industry's technical realities. Many overlook a core fact: Robots are not single hardware products but complex engineering systems integrating mechanical engineering, electronics, AI embodied intelligence algorithms, high-precision sensors, power systems, precision control, and other multidisciplinary technologies.

At the industrial level, large-scale implementation of humanoid robots requires a complete industrial chain, including core component self-research, mature mass production processes, cost reductions, and scenario adaptations—not simply assembling a prototype that can walk a few steps without falling.

Miao Rentao, Associate Dean, Professor, and PhD supervisor at the School of Labor Economics, Capital University of Economics and Business, pointed out that China's intelligent robots still lag behind international giants in core technologies like motion control algorithms, precision reducers, and high-precision sensors. The per-unit cost of humanoid robots remains in the hundreds of thousands of yuan, with over 40% of core components still imported, severely hindering large-scale adoption.

From industrial design and practical perspectives, humanoid (especially bipedal) forms are not currently optimal for robots.

Bipedal walking demands extremely high requirements for balance control algorithms, high-precision joints, servo motors, and power systems. However, in confined indoor or uncomplicated public spaces, bipedal walking can easily be replaced by wheeled movement. Moreover, the cost of an ordinary humanoid robot prototype ranges from hundreds of thousands to millions of yuan, making civilian popularization difficult. In contrast, non-humanoid robots customized for specific scenarios feature simpler structures, higher operational efficiency, and controllable costs, quickly addressing real production and living needs.

Yet the 'illusion' created by current capital and public discourse suggests that humanoid robots will soon enter households to 'work' for humans, and only humanoid robots represent the 'future.' This severe disconnect between technological progress and societal expectations directly fuels a bubble of 'excessive attention and blind hype,' diverting many companies from core R&D to focusing on hype and financing—a complete inversion of priorities.

Capital fervor can quickly create hype but cannot sustain long-term industry health; public adulation can attract short-term attention but cannot hide technological shortcomings and implementation challenges.

The capital market's fervor and the public's fascination with humanoid robots largely originate from the boundless imagination sparked by embodied intelligence. However, the rationality of practical applications and their timeline for realization remain to be proven by time and concrete evidence. Blindly following the trend merely because "robots are the in-thing" is tantamount to contributing to the creation of an industry bubble.

By 2026, the humanoid robot sector has witnessed rapid progress in a short span, fueled by widespread attention and robust capital support. Nevertheless, as a domain of hard technology, humanoid robots have arrived at a pivotal juncture where they must revert to rationality, discard the bubble mentality, and concentrate on pragmatic development.

Any technological product necessitates a lengthy cycle, spanning from technological breakthroughs and mass production to market penetration (popularization). It is improbable for such products to skyrocket in popularity and profitability akin to internet products in the near term. Frankly speaking, humanoid robots undoubtedly represent the pinnacle of future intelligence, but they still require time to overcome technological limitations and implementation hurdles. Until then, adhering to the technological core and prioritizing commercial implementation are imperative for the robotics industry to truly mature and yield sustainable value.

Undeniably, the current humanoid robot sector has spawned numerous "star" companies. However, the future of embodied intelligence cannot be realized through mere "showmanship."

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once