Why Are They Still Heavily Investing in Humanoid Robots in 2026?

03/12 2026

03/12 2026

672

672

Looking back from March 2026, the financing fervor in the humanoid robot sector not only remains undiminished but has accelerated at an astonishing pace.

According to incomplete statistics from The Paper, in the first two months of 2026 alone, the humanoid robot industry (including components) has completed at least 18 financing rounds, with total funding exceeding 13 billion yuan. IT Juzi data shows that since the beginning of 2026, China's embodied intelligence sector has disclosed a total of 88 financing events, with a combined funding amount surpassing 20 billion yuan.

▲ Since 2026, the humanoid robot industry (including components) has completed at least 18 financing rounds. Image source: The Paper

This raises curiosity: Is the humanoid robot sector truly promising, or is capital blindly following the trend? What exactly is driving this wave of heavy investment?

【Robots in the Spotlight: Financing Kicks Off the Year in Full Swing】

On March 2, Galaxy General Robotics completed a new round of financing worth 2.5 billion yuan. This figure not only sets a new record for single-round financing in China's embodied intelligence sector but also propels the company, founded less than three years ago, to a valuation exceeding 20 billion yuan.

On the same day, another company named Songyan Power announced a cumulative Series B financing of nearly 1 billion yuan.

The 28-year-old founder, Jiang Zheyuan, was early inspired by Unitree Technology's robotic dog in the lab and began 'handcrafting' his own robot prototypes. By the end of 2023, Songyan Power secured seed funding and completed nine financing rounds within two and a half years, with a dense (frequent) pace that forces a reevaluation of the sector's heat.

Interestingly, both companies recently 'broke through' on the stage of the Horse Year Spring Festival Gala: Galaxy General's humanoid robot shared the stage with Shen Teng and Ma Li, showcasing skills like walnut cracking, glass shard picking, and sausage skewering;

while Songyan Power's bionic robot starred alongside Cai Ming in the sketch 'Grandma's Favorite,' with its 1:1 replica of Cai Ming leaving a deep impression on many viewers.

▲ Image source: CCTV News

From the Spring Festival Gala stage to financing announcements, the interval was just two weeks. Perhaps someone wonders: Is capital chasing the spotlight of the Spring Festival Gala, or the emerging commercial value of these robots?

Let's shift our gaze back to February: Zhipingfang announced in late February the completion of a Series B financing exceeding 1 billion yuan, with its valuation surpassing 10 billion yuan, becoming Shenzhen's first unicorn in embodied intelligence in the Year of the Horse. Qianxun Intelligence secured nearly 2 billion yuan across two consecutive funding rounds, also joining the '10 billion yuan club.' Component companies like Zibianliang Robotics, Intime Robotics, and Lingxin Qiaoshou also completed financing rounds worth hundreds of millions of yuan, marking capital's expansion from complete machines to every key link in the industrial chain.

Even calculated at the highest annual financing amount of 44.5 billion yuan in 2025, the financing in the first two months of this year already approaches one-third of last year's total. This means the Spring Festival Gala's traffic merely 'fanned the flames,' as the humanoid robot sector, after experiencing the 'mass production the first year ' in 2025, not only failed to cool but instead showed stronger momentum.

However, the truly intriguing aspect is not the financing figures themselves but the faces behind them.

On Galaxy General's 2.5 billion yuan financing list, the National Artificial Intelligence Industry Investment Fund, Sinopec, and CITIC Group are prominent. Notably, the National Artificial Intelligence Industry Investment Fund, established under the leadership of the Ministry of Industry and Information Technology and the Ministry of Finance, made its fourth public investment and first foray into the embodied intelligence sector.

When the 'national team,' wielding national strategic resources and industrial leverage, begins betting real money, it signals that the humanoid robot sector is no longer a 'hype bubble' for capital but a tangible cornerstone in China's manufacturing transformation and upgrading. This is perhaps the confidence many investors have in placing their bets.

【From 'Showcasing Skills' to 'Getting the Job Done': Factories as the Litmus Test】

In the past, capital invested in robots based on backflips and plum blossom pile walking—a logic of 'showcasing skills.' From 2025 to 2026, the most significant shift in the humanoid robot sector is the evaluation system switching from 'athletic ability' to 'labor value.' This shift is most evident in robots that truly enter production lines.

For example, in factories of CATL, Bosch, Toyota, SAIC Motor, and others, Galaxy General's industrial heavy-duty robot Galbot S1 has become a 'regular employee,' with dual arms capable of handling loads up to 50 kg and operating stably under complex conditions like dust, vibration, and temperature fluctuations. At workstations that may be tedious or strenuous for humans, they achieve fully autonomous and normalized operations.

Similarly, UBTECH has gained 'factory access.' In 2025, the company's humanoid robots secured cumulative orders exceeding 1.4 billion yuan, with over 500 units delivered to customers in aviation, automotive, smart logistics, and other industries domestically and abroad.

In its Shenzhen factory, UBTECH's third-generation robot Walker S2 has learned new skills: when its battery level drops below 20%, it locates the nearest battery swap station through a 'swarm brain' network, swaps batteries in three minutes, and returns to work. This means it can operate continuously for 24 hours like a true industrial worker.

▲ UBTECH's Walker S2 achieves autonomous battery swapping. Image source: ifeng.com

If factory robots compete on efficiency and endurance, those in service scenarios are tested more on their ability to handle complex realities.

At this year's National People's Congress, Shenzhen-based Dobot's humanoid robot Atom made its debut as an interview assistant. Facing the complex dynamic environment of the NPC, Atom interacted calmly with journalists and interviewees, even serving popcorn to attendees—its 'original profession.'

Previously, at Shenzhen's K11 cinema, Dobot's humanoid robot had already been stationed at the popcorn counter for some time, working continuously for 14 hours a day, producing and selling over 1,000 cups of popcorn daily without a single error.

But the path to this role was not smooth. According to Liu Peichao, founder of Dobot, the robot encountered numerous issues early in the project, such as crushing paper cups by gripping too hard, spilling popcorn during filling, or even 'striking' when customers moved their cups.

These problems made the R&D team realize that for humanoid robots to truly 'work,' they must pass the test of real-world scenarios. After Repeated debugging (repeated debugging) of fingertip pressure sensors and simulating over 20 emergency scenarios, the robot learned to autonomously diagnose deviations and replan movements, resulting in today's Atom, which can calmly handle various situations at the counter.

▲ Dobot's humanoid robot Atom serves popcorn at the National People's Congress. Image source: Shenzhen News Network

Notably, Wang He, founder of Galaxy General, once calculated: A 24-hour pharmacy robot priced at 500,000-600,000 yuan replaces two- or three-shift workers and can recoup costs within three years.

Clearly, beyond the 'national team' leading the way, these unfolding scenarios may also explain why capital dares to pour billions into the robot sector. People finally see that humanoid robots are beginning to truly integrate into human production and service sectors, with an industrial chain mature enough to calculate every cost, making capital's return on investment yearning (anticipatable) and predictable.

【AI Era Positioning Battle: China Is Determined to Win】

If industrial scenario deployments clarify the 'present' for capital, the Sino-US competitive landscape prompts them to bet on the 'future.'

In the AI era, large models serve as the 'brain,' while humanoid robots act as the 'body.' Currently, China, with the world's most complete manufacturing supply chain, Ultimate cost reduction capability (unparalleled cost-reduction capabilities), and vast industrial scenarios, has the potential to occupy the core ecological niche in defining the 'body.'

This strategic positioning is no accident but the result of a carefully designed combination punch (combination of strategies).

From a national standpoint, the 2025 Government Work Report included 'embodied intelligence' in the list of future industries for priority cultivation for the first time. In February 2026, the first full industrial chain standard system for humanoid robots was implemented. Policies are not just slogans but systematic moves, unifying previously fragmented software interfaces and hardware routes into a coordinated roadmap for mass production, testing, and global expansion.

▲ Image source: CCTV News

From public perception, multiple domestic robots made collective appearances at the 2026 Spring Festival Gala, with related topics exceeding 100 million views on Douyin. Overnight, humanoid robots transformed from niche tech terms into national conversations, igniting public curiosity and acceptance. This perceptual foundation is invaluable for future robot products entering households and daily life.

From an industrial base perspective, three major industrial clusters have formed in the Yangtze River Delta, Pearl River Delta, and Beijing-Tianjin-Hebei region: In Hubei, the humanoid robot industrial chain reaches 85% completeness, covering 31 key components. In Jiangsu, the coverage rate exceeds 93.8%. In Shenzhen's 'Robot Valley,' nestled between the southern foothills of Yangtai Mountain and Tanglang Mountain, nearly half of the core components can be sourced within 10 kilometers, with 80% of suppliers located within 40 kilometers.

Meanwhile, the cost of core robotic joint motors has dropped from 50,000-60,000 yuan to 500-600 yuan, while high-precision tactile sensor prices have fallen from the 100,000 yuan range to the thousand or even hundred yuan level. This full-chain matching (support) and Extreme cost reduction (extreme cost-reduction) capability is the cornerstone of domestic robots' scalable deployment.

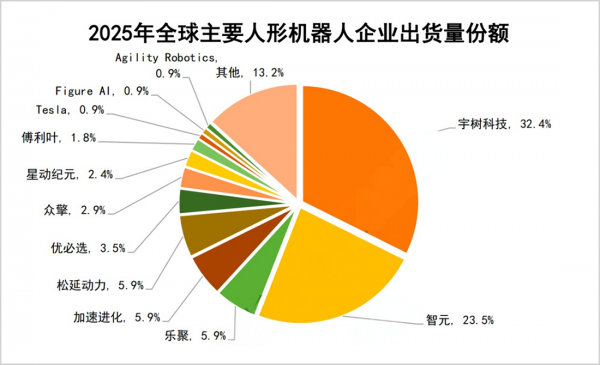

Thus, we see that as of Q3 2025, Tesla's Optimus had a trial production scale of less than 1,000 units, while Figure AI shipped only about 150 units annually, primarily for internal testing and technical verification. In contrast, Chinese companies dominated the top six in global humanoid robot shipments, collectively accounting for 74.1% of the market. Among them, Unitree Technology shipped over 5,500 units, representing 32.4% of the global market and ranking first in both shipments and market share.

▲ Image source: '2025 Humanoid Robot Market Research Report'

Moreover, in terms of benchmark enterprises' capabilities, Unitree Technology achieved 100% localization of core components like motors, reducers, controllers, and underlying algorithms, developing a high-burst electro-mechanical drive integrated joint module that fills domestic gaps. Zhiyuan built an 'integrated three intelligences' architecture and launched the industry's first general-purpose embodied foundation model, 'Zhiyuan Qiyuan Large Model.' Xingdong Era self-developed the end-to-end VLA embodied brain ERA-42, with over 95% hardware self-research rate, serving nine of the top 10 global tech giants by market value...

As Jiang Lei, deputy director of the Standards Committee and chief scientist at Humanoid Robot (Shanghai) Co., Ltd., said, humanoid robots have progressed from 0 to 1, and the next step is to advance from 1 to 10.

Therefore, the current wave of capital investment is not just in a few robot companies but in China's strategic ticket to transition from a 'follower' to a 'definer' in the future global tech division of labor.

Perhaps for humanoid robot companies, 2026 is not only the 'commercialization the first year ' but also the 'elimination round the first year .' The money is already on the table; now, it's about who can complete this marathon with factory order volumes and household penetration rates.

Disclaimer

The content related to listed companies in this article is based on the author's personal analysis and judgments derived from information publicly disclosed by the companies in accordance with their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms). The information or opinions herein do not constitute any investment or other business advice, and Market Value Observer assumes no responsibility for any actions taken based on this article.

——END——

-

![]()

Xiaomi Auto Reports a Substantial Q1 Loss of 3.1 Billion Yuan, Yet Lei Jun Remains Unperturbed

-

![]()

"3D Vision Pioneer" Grapples with Internal Strife: $120 Million in Share Reductions Offset by $147 Million Private Placement

-

![]()

The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

-

![]()

Five Brands Team Up with Huawei: Will Dongfeng Still Pursue Independent R&D?

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One