Unitree Robotics IPO: The Journey of a Talented Yet Focused Player Going Public

03/25 2026

03/25 2026

459

459

By Liang Tian

Source / Node AI

At the 2017 Wuzhen Internet Conference, Wang Xingxing, a recent graduate, introduced Unitree Robotics to the world. At that time, both Unitree Robotics and Wang Xingxing were relatively inexperienced. Nine years on, Unitree Robotics has made headlines with two appearances at the Spring Festival Gala and is now racing towards an IPO, claiming the title of the world's leading supplier of humanoid robots.

The numbers certainly look impressive.

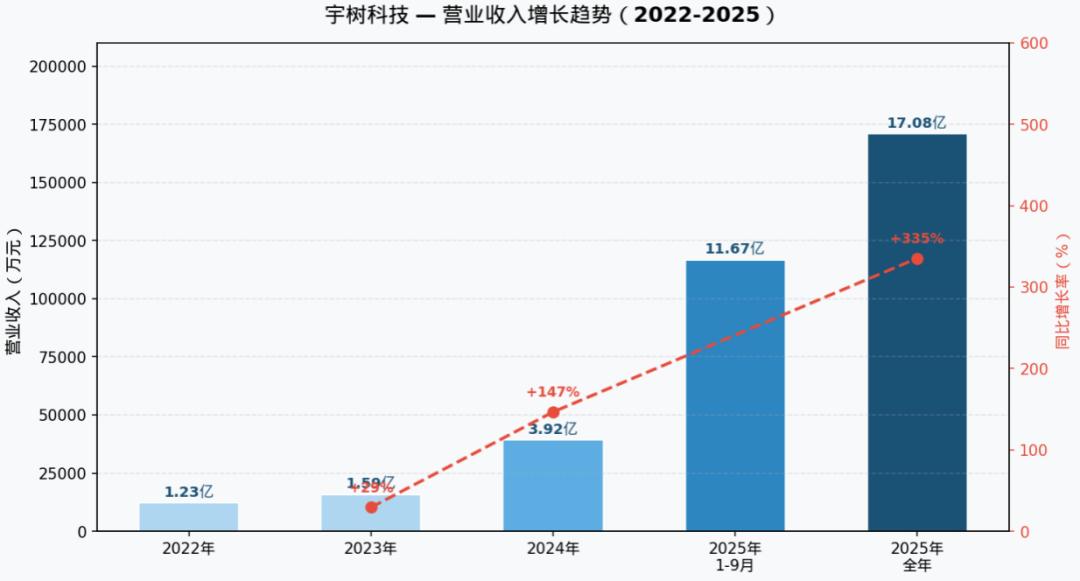

According to the prospectus data, the company reported an operating revenue of RMB 1.708 billion in 2025, marking a year-on-year increase of 335.36%. During the reporting period from January to September 2025, revenue from the humanoid robot business reached RMB 590 million, a staggering 456.78% increase compared to the entire previous year. In 2025, the company's shipments of humanoid robots exceeded 5,500 units (purely humanoid, excluding wheeled dual-arm robots).

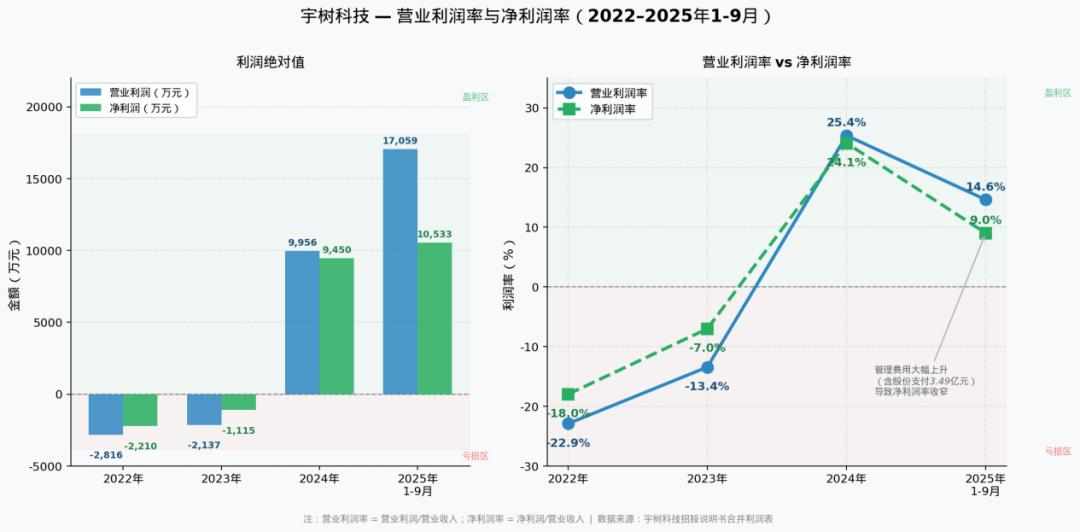

The profits are noteworthy. In 2025, the gross margin of Unitree Robotics' main business reached 60%, with non-recurring net profits of RMB 600 million and a net profit margin of around 35%. It is one of the few companies in the embodied intelligence field capable of achieving large-scale profitability. In contrast, Hong Kong-listed UBTECH had a gross margin of around 30% and incurred a loss of RMB 1.16 billion in 2024 alone.

While profit certainty is a positive sign, a deeper analysis reveals that Unitree Robotics excels in the physical design and 'cerebellum' (basic motor functions) but has yet to achieve outstanding results in the increasingly critical 'brain' level—the field of embodied large models.

The AI industry is evolving rapidly, and the focal point of competition in this sector is now centered on enabling robots to truly perform work. It can be said that Unitree's prospectus only reflects its past achievements and cannot predict the future. How to make breakthroughs at the 'brain' level will be the true test for Wang Xingxing.

Behind the high-profit margins, does Unitree's robot lack a 'brain'?

Unitree Robotics' high gross margins and net profits can be attributed to a focused player reaping brand dividends from an emerging sector.

Quadruped robots and humanoid robots are Unitree's two main revenue streams. As of the first three quarters of 2025, revenue from quadruped robots was RMB 488 million, accounting for 42.25%, while revenue from humanoid robots was RMB 595 million, accounting for 51.53%.

As the largest revenue source, humanoid robots have seen astonishing growth. In 2023, they were almost negligible, with annual revenue of only RMB 2.97 million. However, by the first three quarters of 2025, it had surged to RMB 595 million.

The reason is straightforward: the fame gained from two consecutive appearances at the Spring Festival Gala has made Unitree Robotics almost synonymous with robots. This influence has made Unitree Robotics a household name, allowing it to spend virtually nothing on marketing. In the first three quarters of 2025, sales expenses were only RMB 76 million, accounting for 6.51% of revenue, with advertising expenses of only RMB 22.57 million.

Not all brands can capitalize on high sales volumes. Unitree Robotics, after a decade of refinement, has accumulated significant expertise in hardware and supply chain management, greatly contributing to cost control.

It is important to note that as one of the earliest robot companies in China, Unitree has leveraged the systemic opportunities of the Chinese industrial chain and established its own factories early on. By 2020, Unitree already had a small workshop in Hangzhou. The self-research of core components has transformed Unitree's upstream suppliers from component suppliers to material suppliers, eliminating a layer of markup. Its self-developed molds for producing non-standardized components have solved mass production issues, making it easier for Unitree to control costs as sales volumes rise.

Unitree Robotics excels in the physical design and 'cerebellum' but is a true focused player when it comes to the 'brain' level, which is responsible for cognition, decision-making, and environmental understanding. This area is the most capital-intensive, and Unitree has not heavily invested in it. This choice inherently carries risks in terms of technical approach.

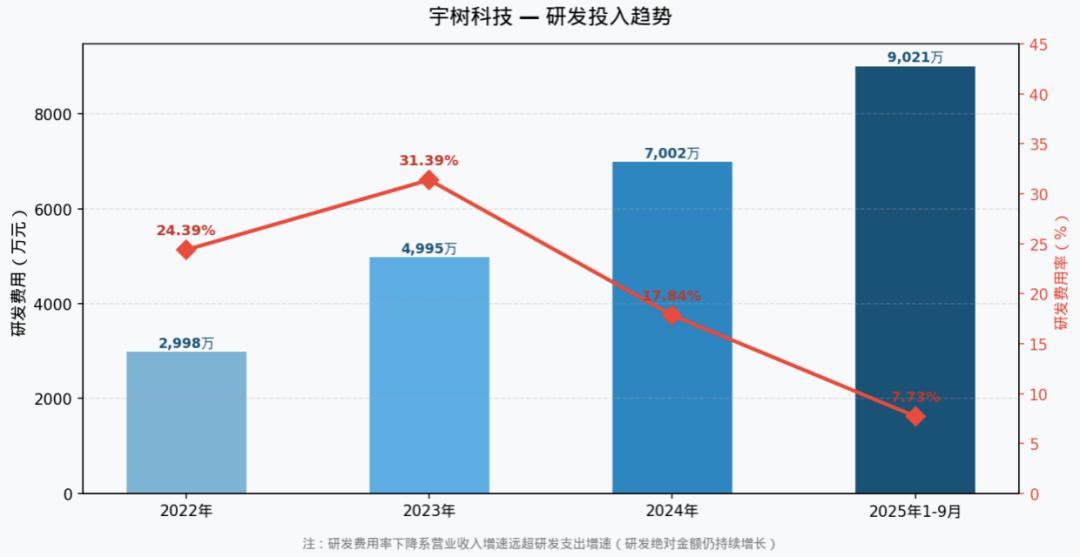

The data speaks for itself: in the first three quarters of 2025, Unitree Robotics' R&D expense ratio was only 7.73%. In contrast, UBTECH, which released the multimodal large model Thinker with 10 billion parameters in 2025, has an R&D expense ratio of around 40% year-round.

Wang Xingxing once said in an interview, 'To be honest, our investment in machine AI in China is relatively small compared to others. After all, our financial and human resources are limited. AI is too expensive—we can't even afford the GPU computing power. If we invest too much, it's easy to fall into an imbalance between profits and losses.'

Taking the Spring Festival Gala's 'Wu Bot' as an example, according to public information, the martial arts movements of Unitree's robots were not the result of the robots generating 'self-thinking' but rather a combination of pre-programming and advanced AI algorithms.

In other words, the robots were executing carefully choreographed movement sequences rather than creating them independently after understanding the meaning of 'martial arts.' This means that in real-world applications requiring robots to face open environments and understand them in real-time, the current technological architecture is far from sufficient.

Humanoid robots have not yet truly been deployed on a large scale, but Unitree has already turned 'robots' into a brand and a symbol of the times.

What are the future challenges?

A new trend has emerged in the robotics industry—as seen from the direction of primary market investments, the industry's focus is shifting from hardware to the 'brain.' In layman's terms, future competition among robot companies may revolve around who can develop the Android operating system for the robot era and who can build a hardware ecosystem on top of it.

Competitors are rapidly catching up in hardware and 'cerebellum' capabilities while launching attacks on the 'brain' level.

More and more companies are quickly closing the gap in motion intelligence, leaving the 'brain' as the only missing piece of the puzzle. The primary market is voting with its feet, with the 'brain' faction gaining more supporters.

According to AI Technology Review, if we roughly divide leading companies into camps based on motion control and 'brain' capabilities, among the 11 complete machine companies with valuations exceeding RMB 5 billion, except for Unitree and Zhongqing, the rest are focusing on the development of embodied large models like VLA.

Some companies have already achieved certain success. Recently, the Galaxy General team, known for its powerful 'brain,' released the algorithm Latent, contributing the 'brain' that enabled Unitree's robots to learn to play tennis in real-time.

This is not meant to deliberately downplay the industry leader; it is a consensus among investors and Wang Xingxing.

Some investors have bluntly stated that the ceiling in the robotics field is definitely in developing the 'brain' because it is directly linked to downstream applications. The value of motion control companies remains unclear, depending on whether the future physical form will be bipedal. Some estimate that a 'wheeled + dual-arm' configuration is more likely because embodied intelligence cannot survive solely on dancing and performing, which would put humanoid robots in an awkward position.

Wang Xingxing himself acknowledged in previous interviews that as AI technology becomes more mature, demand for hardware will decrease. When the AI of future humanoid robots truly breaks through, one could find a few joint motors from a trash heap, assemble them into a human-like form, and it would be able to walk and even do some work on its own. Moreover, Wang Xingxing admitted that his biggest regret in the past was not investing in AI.

Discussing these points does not mean that Unitree Robotics does not value embodied large models. It is fair to point out that when Unitree Robotics was founded in 2016, AI technology was still in a relatively early stage, and large models had not yet reached the 'ChatGPT' moment. Embodied intelligence also did not see significant breakthroughs until DeepSeek gained prominence in 2025.

This does not directly imply that Unitree will inevitably fall behind in the 'brain' level in the future, as it will join the ranks of companies tackling the 'brain' challenge after this IPO.

In the prospectus, Unitree Robotics stated that the company places great importance on independent innovation and technological R&D and will continue to increase investment in R&D for embodied large models through this fundraising project.

Unitree also specifically mentioned that if the company fails to accurately grasp industry technology trends, makes incorrect decisions in technological R&D and product development, or fails to achieve breakthroughs in key technologies or meet performance expectations, resulting in its products falling behind industry technology, it will adversely affect its sustained competitive advantage and operating performance.

However, with the technological approach for embodied large models still far from converging and competition around the 'brain' intensifying, R&D is not something that can be accomplished overnight. A key question is: After the IPO fundraising, how much capital does Unitree plan to invest in large model R&D? The size of this figure will directly determine the market's judgment on Unitree's sincerity in 'catching up.'

Has the inflection point for commercialization arrived?

After discussing the technological approaches that have not yet converged, we must admit that the large-scale commercialization of humanoid robots still faces uncertainties and risks of falling short of expectations.

Unitree Robotics also pointed out in the prospectus that on the demand side, except for specific application scenarios, the consumer market for general-purpose robots has not yet formed a rigid demand, and the process of building an application ecosystem and cultivating the market is lengthy. Additionally, factors such as regulatory policies, industry standards, and social acceptance may also constrain the commercialization process. If progress in technological breakthroughs, cost control, and market cultivation does not meet expectations, the commercial promotion of general-purpose robots will face substantial delays.

In summary, Unitree Robotics has a clear leading advantage and is virtually unmatched in brand recognition. Its decade-long supply chain accumulation is also a significant moat. However, it also has shortcomings that need to be addressed. The unpredictable nature of the industry and the future direction of technology and approaches will be key.

*The featured image was generated by AI.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?