Former Tencent Scientist Builds Leading Industrial AI Player, SmartMore Rushes Towards IPO with 3-Year Cumulative Loss of 2.2 Billion Yuan

03/30 2026

03/30 2026

551

551

Produced by | Frontline of Entrepreneurship

Art Editor | Xing Jing

Reviewed by | Song Wen

In recent years, AI has begun transitioning from the cloud to manufacturing floors, with industrial intelligence emerging as a hot sector backed by both tech and industrial capital.

Many AI companies, driven by the ambition to "redefine industrial automation," have rushed into this field. SmartMore Inc. (hereinafter referred to as "SmartMore") is one such representative company.

Positioning itself as an AI company with agents as its core product and top-tier manufacturing enterprises as clients, SmartMore has become the domestic market leader in industrial AI agents just six years after its establishment.

However, in stark contrast, the company holds less than 10% market share, has an overall gross margin below 40%, incurred cumulative losses exceeding 2.2 billion yuan over three years, and suffered persistent operating cash outflows exceeding 1.1 billion yuan.

All grand narratives ultimately boil down to financial metrics. Currently, SmartMore's books clearly have not yet found the balance between scale and profitability.

1. Industrial AI Agent Leader Faces Encirclement from Both Sides

Founded in 2019 by Jia Jiaya, a tenured professor in the Department of Computer Science and Engineering at The Chinese University of Hong Kong and former scientist at Tencent's YouTu Lab, SmartMore represents Jia's pivotal shift from academia to industry. Jia, who was recommended for doctoral studies at Hong Kong University of Science and Technology from Fudan University in his youth and later became a professor at The Chinese University of Hong Kong, counts Xu Li, chairman and CEO of SenseTime, among his former students.

Naming the company SmartMore, Jia intended to convey not just intelligence but also foresight.

For this venture, Jia targeted the "cornerstone of human progress"—the industrial sector. With rapid AI technological advancements, the global industrial landscape is undergoing a transformation from automation to AI-driven systems, with industrial AI solutions set to redefine manufacturing paradigms.

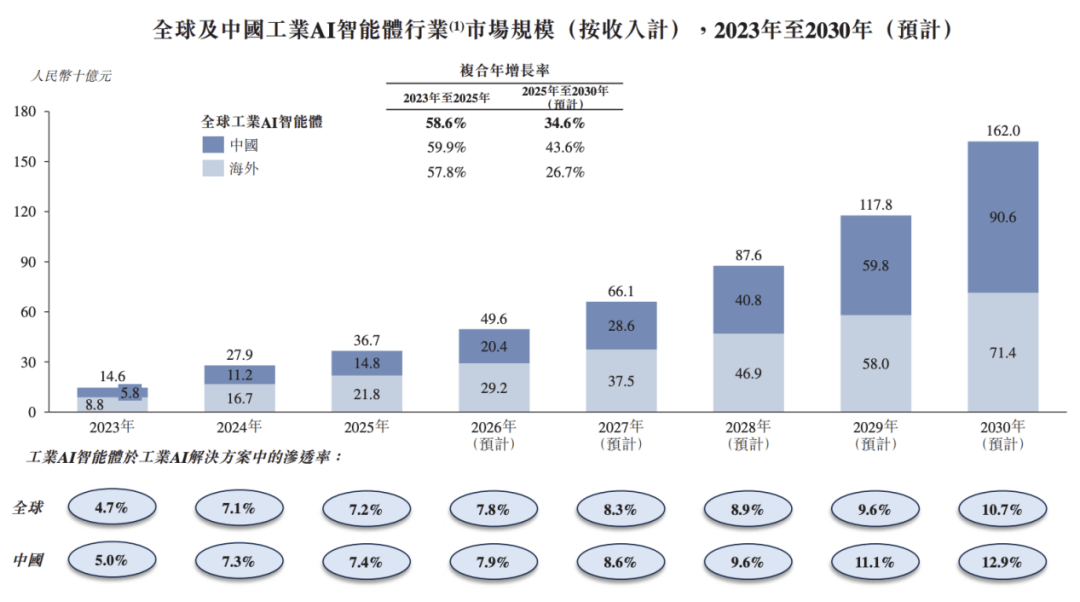

According to a report by China Insights Consultancy, the global market size for industrial AI agents is projected to expand from 14.6 billion yuan in 2023 to 36.7 billion yuan in 2025, representing a compound annual growth rate (CAGR) of 58.6%, and is expected to reach 162 billion yuan by 2030, with a CAGR of 34.6% from 2025 to 2030.

(Figure/Prospectus)

Specifically, the Chinese industrial AI agent market is projected to grow from 5.8 billion yuan in 2023 to 14.8 billion yuan in 2025, with a CAGR of 59.9%, and is expected to reach 90.6 billion yuan by 2030, with a CAGR of 43.6% from 2025 to 2030.

SmartMore was born into this "golden track " (golden track). By 2025, it had become China's largest industrial AI agent provider by revenue, holding a 5.8% market share.

(Figure/Chinese Industrial AI Agent Industry Landscape (Source: Prospectus))

However, the "gold" in this first-place ranking is not as solid as it sounds. SmartMore faces intense competitive pressure, described aptly as "blockades ahead and pursuers behind."

Ahead, SmartMore's core clients may develop in-house solutions. Manufacturing giants like Tesla and Luxshare Precision are both clients and potential future competitors.

After all, as AI capabilities become a core competitive advantage in manufacturing, will these leading firms continue to outsource? In its prospectus, SmartMore admits: "Several of our clients may develop similar products independently."

Notably, Huawei and BYD have already established large-scale in-house AI teams, while Tesla has heavily invested in AI. Should they choose in-house development, SmartMore faces not only order losses but also the emergence of formidable competitors.

Behind, SmartMore is pursued by peers amid intensifying industry competition. International giants like Keyence and Siemens loom large, while domestic newcomers like HuaRay Technology and Weiyi Intelligent Manufacturing are rising rapidly.

The sector remains fragmented and competitive, with no single enterprise achieving absolute dominance. The combined market share of the second- to fifth-ranked firms reaches 17.1%, far exceeding SmartMore's 5.8%. With rapid market growth, SmartMore's share risks dilution or being surpassed.

2. Gross Margin of Just 37.3%, Hardware Supports Half the Business

From securing its first AI quality inspection project after founding in 2019 to launching cloud-edge integrated AI vision software in 2020 and intelligent inspection robots in 2021, SmartMore achieved a software-to-hardware business layout within three years.

Currently, its core businesses include industrial AI agents and AI infrastructure, with the former comprising robots, edge AI sensors, and agent software systems.

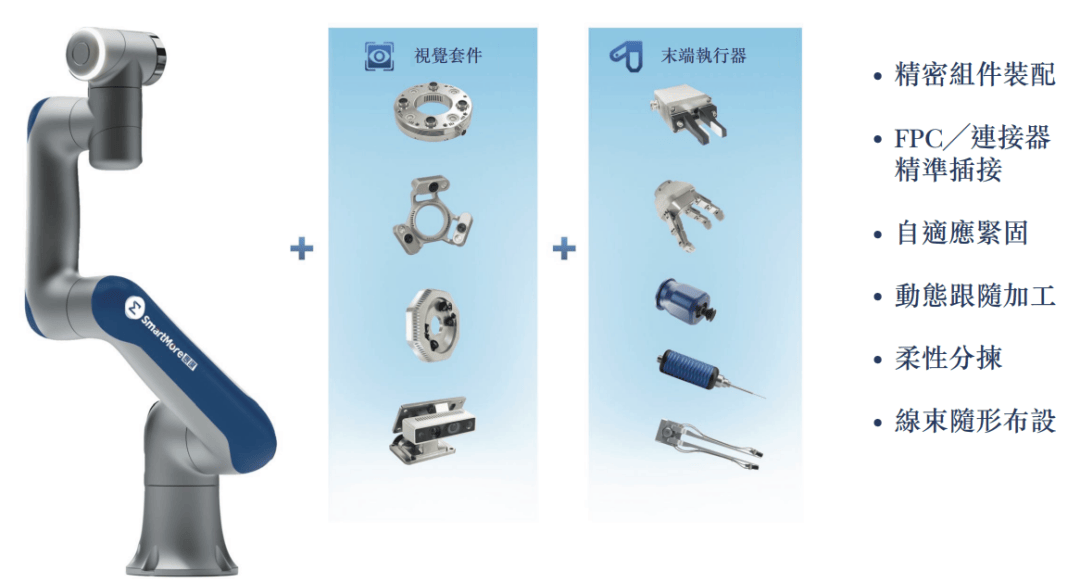

(Figure/SmartMore's Intelligent Operation Robots (Source: Prospectus))

By 2025, SmartMore's robots had inspected over 17 billion products or components, with approximately 140,000 cutting-edge industrial agents delivered.

In its prospectus, SmartMore defines itself as an AI company redefining industrial automation in the AI era.

However, a breakdown of its revenue reveals that hardware supports nearly half its business.

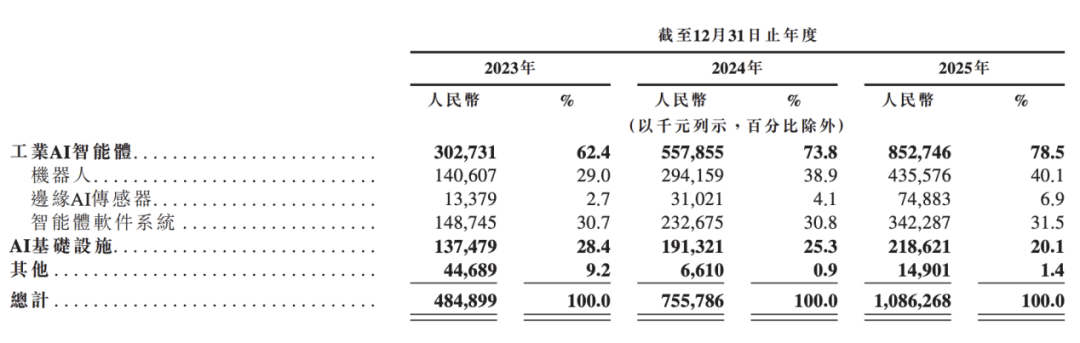

(Figure/Prospectus)

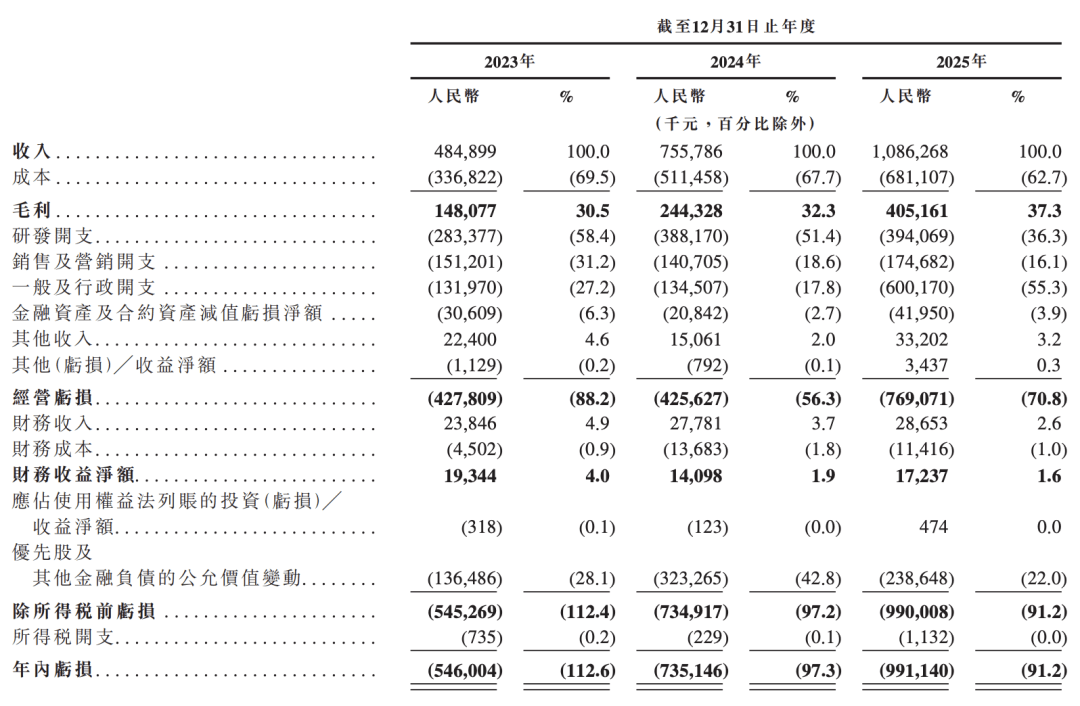

From 2023 to 2025 (hereinafter referred to as the "reporting period"), SmartMore's total revenue reached 485 million yuan, 756 million yuan, and 1.086 billion yuan, respectively. Industrial AI agents accounted for 62.4%, 73.8%, and 78.5% of revenue, serving as the primary income source.

During the same period, AI infrastructure contributed 28.4%, 25.3%, and 20.1% of revenue, while other businesses accounted for 9.2%, 0.9%, and 1.4%.

Within SmartMore's core industrial AI agent business, the robot segment's revenue share rose from 29% in 2023 to 40.1% in 2025, while edge AI sensors increased from 2.7% to 6.9%.

Thus, hardware accounted for at least 47% of total revenue in 2025 (potentially higher when considering hardware bundled with AI infrastructure deliveries).

This business structure significantly differentiates SmartMore's gross margin profile from pure software-focused AI firms. During the reporting period, its overall gross margins were 30.5%, 32.3%, and 37.3%, respectively— Although there has been continuous growth (albeit sustained growth /continuously increasing), but still below the 60% or higher margins typical of pure software AI companies. For instance, STAR Market-listed AI software firm Hexin Information has maintained margins above 80% for six years, while listed AI application firm Wondershare Technology exceeds 90%.

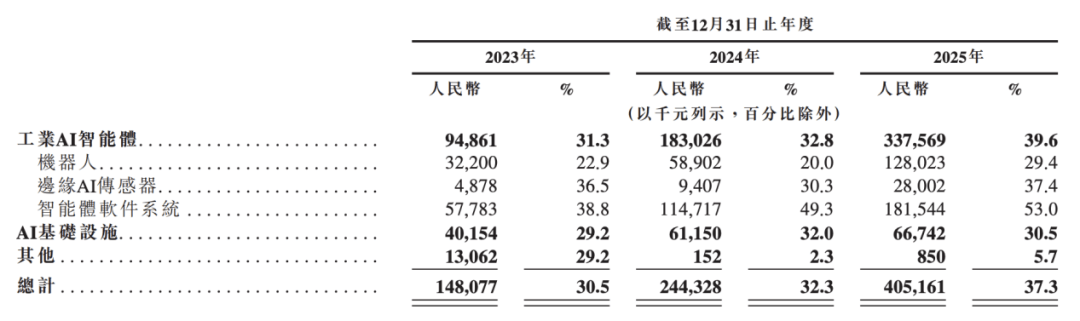

(Figure/SmartMore's Business Gross Profit and Margin Breakdown (Source: Prospectus))

Across business segments, hardware like robots and edge AI sensors consistently showed lower margins than agent software systems, dragging down the overall margin.

Since its inception, SmartMore has secured multiple funding rounds from investors including IDG Capital, Hidden Hill Capital, Lenovo Group, Cornerstone Capital, ZhenFund, Pine Venture Capital, and Sequoia China. By its final funding round in February 2026, the company's post-money valuation reached $1.23 billion.

However, in secondary market valuation logic, gross margin levels significantly impact tech company valuations. High hardware revenue shares tilt market perceptions toward manufacturing or integrator valuations, while higher software and service shares justify AI tech company premium valuations.

Based on 2025 revenue, SmartMore's $1.23 billion valuation implies a static price-to-sales (P/S) ratio of approximately 8.2x. This exceeds valuations of pure hardware firms and some integrated peers, reflecting market recognition of its high growth expectations while implying strong anticipation for improved software revenue share and margin enhancement.

Whether SmartMore can fulfill these expectations will determine its valuation stability.

3. Luxury "Client Circle" Fails to Sustain Self-Sufficiency

One of the most striking highlights in SmartMore's prospectus is its client roster.

As of December 31, 2025, SmartMore had served over 730 clients, with the count rising from 229 in 2023 to 497 in 2025.

Its clients include industry leaders such as Tesla (new energy vehicle leader), Carl Zeiss (century-old optics and precision measurement giant), Luxshare Precision (consumer electronics "contract manufacturing king"), and BOE Technology Group (global display panel leader), spanning high-growth sectors like consumer electronics, new energy, precision manufacturing, and rail transit.

Gaining entry into these top firms' supply chains signifies industry recognition of SmartMore's technical prowess, product reliability, and service capabilities.

However, this luxury "client circle" has yet to translate into healthy cash flow.

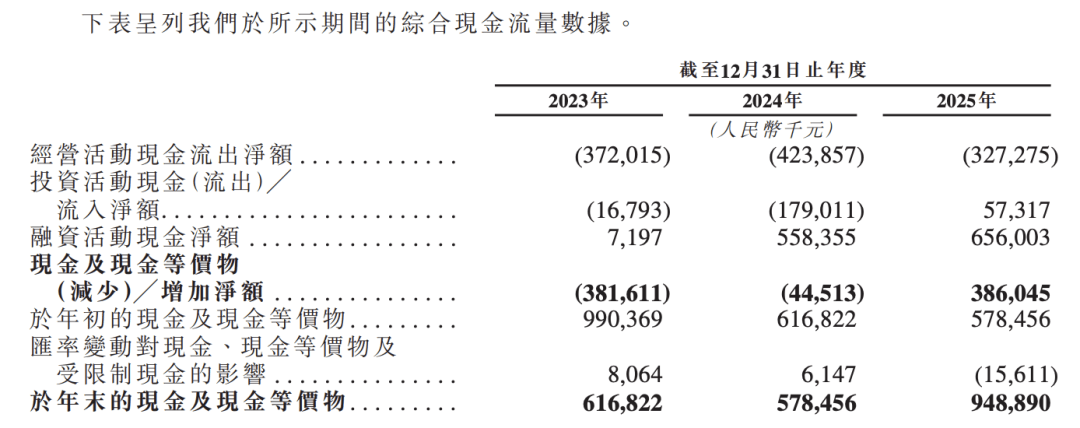

During the reporting period, SmartMore's net operating cash outflows were 372 million yuan, 424 million yuan, and 327 million yuan, respectively, totaling 1.123 billion yuan over three years.

Concurrently, the company reported annual losses of 546 million yuan, 735 million yuan, and 991 million yuan, respectively, with cumulative losses reaching 2.272 billion yuan. Adjusted net losses were 394 million yuan, 379 million yuan, and 272 million yuan, totaling 1.045 billion yuan.

(Figure/Prospectus)

This indicates that while client orders generated book revenue, they have not converted into actual cash inflows.

As of each reporting period-end, SmartMore's trade receivables and bills receivable were 270 million yuan, 533 million yuan, and 744 million yuan, respectively, with corresponding allowances for credit losses on trade receivables and bills receivable at 80.1 million yuan, 77.9 million yuan, and 87.6 million yuan.

Moreover, the company's collection periods remained elevated. During the reporting period, days sales outstanding (DSO) for trade receivables and bills receivable were 214 days, 194 days, and 214 days, respectively.

(Figure/Prospectus)

Additionally, SmartMore has made substantial investments in R&D and sales/marketing. In 2023, R&D and sales/marketing expenditures totaled 435 million yuan, rising to 569 million yuan by 2025. Although their share of revenue declined from 89.6% in 2023 to 52.4% in 2025, absolute spending continued to grow. Coupled with surging administrative expenses, total costs far exceeded gross profits.

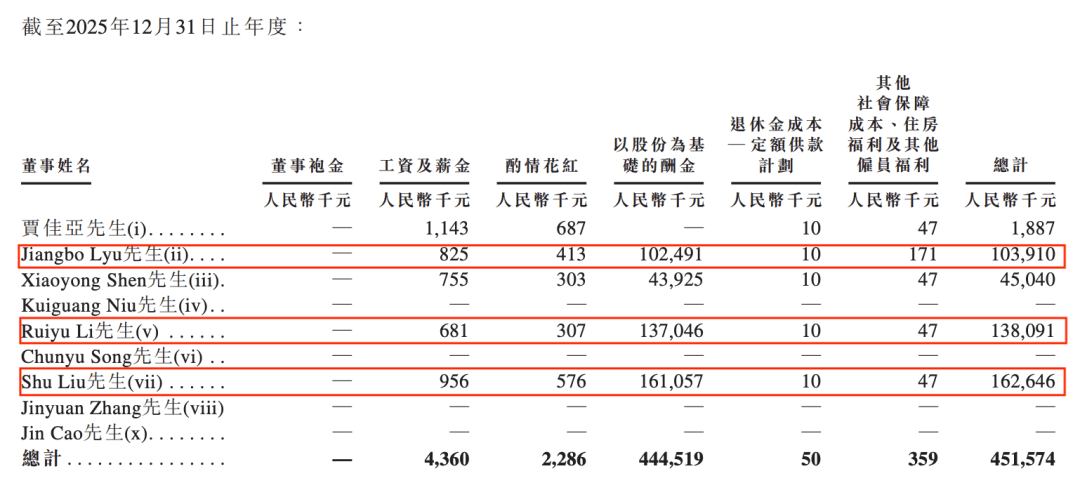

In 2025, general and administrative expenses skyrocketed to 600 million yuan, accounting for 55.3% of revenue—a more than threefold year-over-year increase.

SmartMore explained in its prospectus that this surge primarily resulted from "significant increases in share-based compensation expenses"—each of the company's three directors received share-based compensation exceeding 100 million yuan in 2025. While equity incentives are common in startups, such a concentrated large-scale incentive in a single year naturally raises external concerns about operating costs.

(Figure/Prospectus)

Regarding sustained losses, SmartMore attributed them in its prospectus to its startup phase, with strategic priorities focused on long-term success and financial returns in the industrial AI agent market rather than sacrificing future market potential for short-term profitability. The company has made substantial investments in product development, market expansion, and infrastructure to achieve sustained larger-scale operations, with profitability still under establishment and optimization.

Notably, SmartMore did not specify a timeline for achieving break-even in its prospectus.

While explaining sustained losses through long-term layout (strategic layout /strategic layout ) aligns with early-stage industry patterns, it cannot mask the core reality of unestablished self-sufficiency—a critical challenge supporting its $1.23 billion valuation and IPO ambitions.

Capital patience is finite. Jia Jiaya and SmartMore must not only aim high in redefining industrial automation for the AI era but also ground themselves in cash flow reality, ultimately proving their value through profitability.

*Note: The featured image is sourced from the Jiemian Gallery.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?