The Rules of Humanoid Robot Industry Are Being Rewritten

03/30 2026

03/30 2026

450

450

A Tale of Two Extremes: Where Will Humanoid Robots Go?

The spring of 2026 brings scorching heat to the humanoid robot sector.

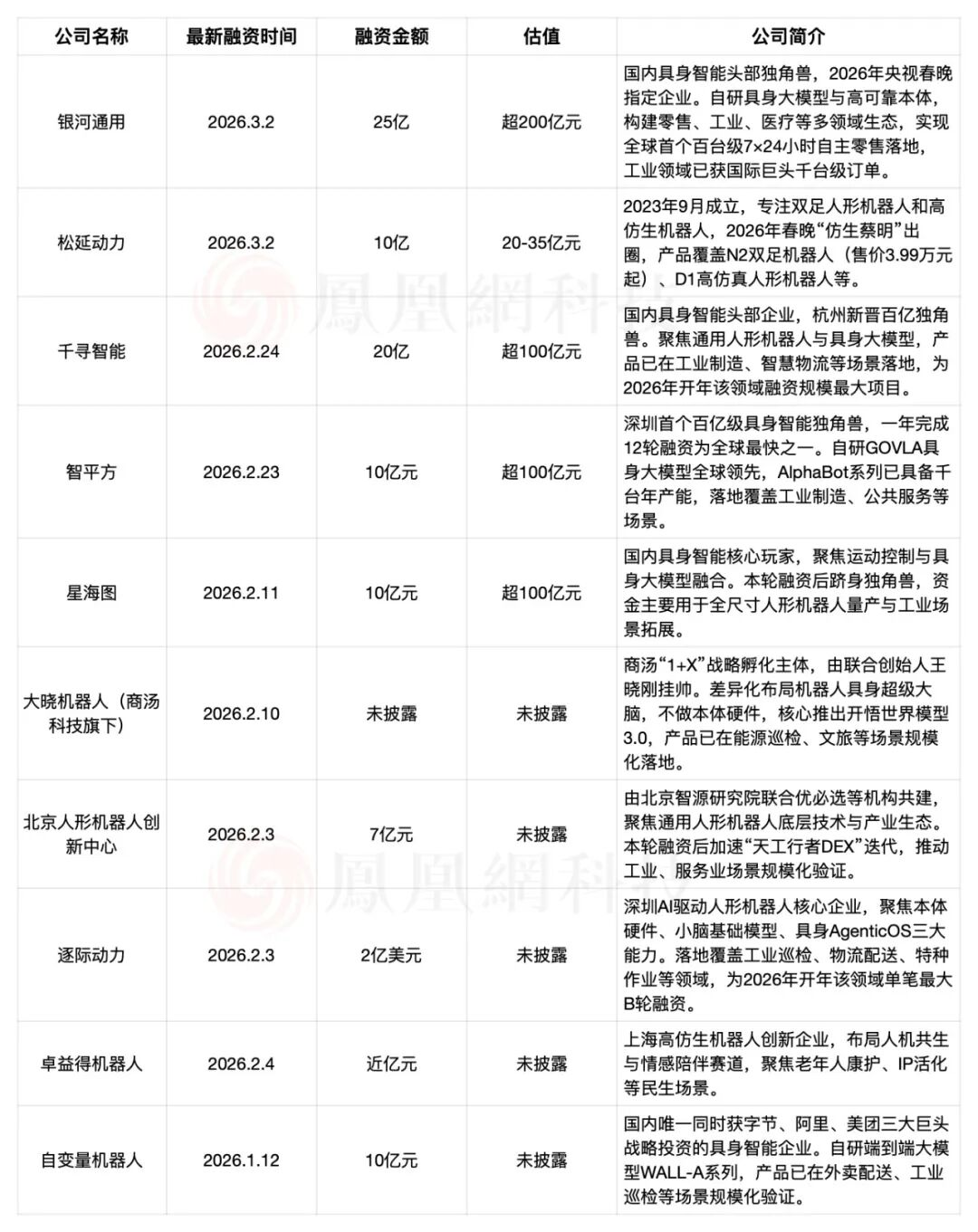

Domestic robot companies like Ai Square and Qianxun Intelligence, established just two to three years ago, have secured billion-dollar-level financing in succession. The "drums of IPO" are also beating loudly, with over 10 humanoid robot companies preparing to go public in the past six months.

However, looking across the ocean, a different picture emerges. Silicon Valley star project K-Scale Labs disbanded its team on the eve of mass production; Cartwheel Robotics' official website quietly shut down, with its founder leaving a harsh adage: "In hardware entrepreneurship, capital is as vital as oxygen."

A tale of two extremes. Opportunity and foam (bubble) arrive simultaneously at this moment.

01 Structural Fractures Behind the Financing Frenzy

Humanoid robots are experiencing an unprecedented financing boom, but a closer look at capital flows reveals a harsh reality:

The money isn't decreasing; it's accelerating its concentration.

GGII data shows that over the past three years, the number of domestic humanoid robot companies has surged from over 120 to over 320, with industry financing surpassing 58 billion yuan, including 38 billion yuan raised in 2025 alone. Entering 2026, this trend has become even more pronounced, with over 10 billion yuan in financing pouring into China's robotics sector in just the first three months, benefiting over 20 companies.

(Image Source: ifeng.com Technology)

This trend of "the strong getting stronger" is even more pronounced at the IPO level. Unitree completed its tutoring process in just 132 days from signing the agreement, setting the fastest record for tutoring (tutoring) time among embodied AI companies this year. Behind it, companies like Xinghaitu and Zhongqing Robotics have completed share reforms, while star robotics firm Leju Intelligence, which recently secured nearly 1.5 billion yuan in Pre-IPO financing, has officially begun IPO tutoring. The financing pace and listing speed of leading companies have left mid-tier projects far behind.

(Image Source: Unitree Technology Prospectus)

Therefore, from the perspective of RoboFront, the industry differentiation trend has become increasingly clear: The first tier, represented by Unitree Technology, Zhiyuan Robotics, and Leju Robotics, is accelerating its IPO process, with cumulative financing exceeding 1.5 billion yuan each, forming a dual-drive pattern of "self-generated revenue + external capital infusion," and is moving from technical validation to scalable delivery. The second tier, represented by companies like Xinghaitu and LimX Dynamics, has seen a noticeable narrowing of financing windows, with business models still under validation and seeking differentiated breakthroughs in niche scenarios. The third tier mainly consists of small and medium-sized enterprises and some cross-border entrants, which lack a clear technological path and core competitiveness and may gradually fall behind in the fierce competition.

In this light, when the dust settles from the financing race, what remains will be a ruthless filter (selection) for "survival eligibility." And what determines who stays at the table is no longer just financing capability itself.

02 A "Mature" Body and a "Bottlenecked" Brain

As capital concentrates among the leaders, what are these well-funded "players" doing now? The answer points to a deeper dimension of competition.

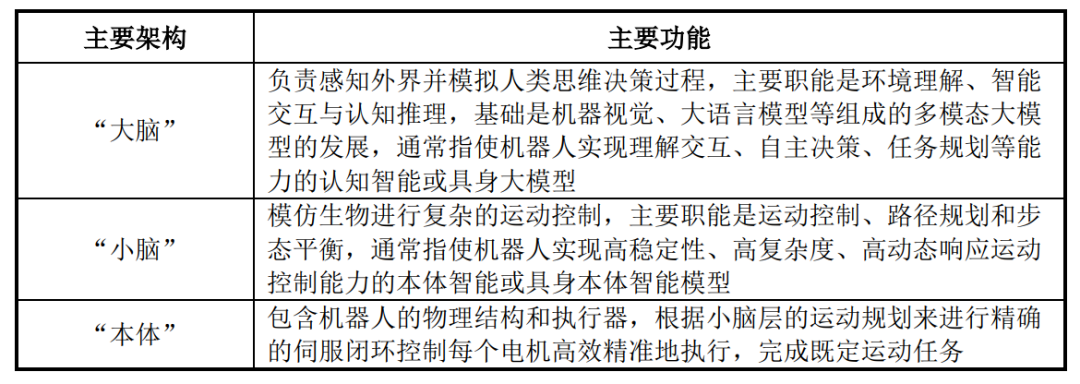

In the robotics industry, technical capabilities are often distinguished by "brain," "cerebellum," and "body." However, today, "body + cerebellum" technologies have matured, with stable walking, dynamic dancing, and somersaulting already fully validated in scenarios like the Spring Festival Gala. The "brain," however, is becoming the true bottleneck restricting scalable applications.

Jiang Lei, Chief Scientist at the National Humanoid Robot Innovation Center, has stated that 2026 will become a watershed for the industry, with about 80% of domestic complete-machine companies still in the "platform-building" stage. Companies lacking dataset and large model capabilities will face significant risks. Data shows that in the first half of 2025, the cumulative duration of global open-source embodied datasets was less than 1,000 hours, insufficient to support substantive R&D.

Breaking through this bottleneck hinges on high-quality real-world robot data.

Such data provides real physical interactions, eliminates the Sim2Real gap, and serves as the core fuel driving the brain from "understanding" to "execution," with its irreplaceability becoming increasingly prominent.

For this reason, Chinese companies are accelerating their efforts in this dimension. On the one hand, leading companies are building algorithmic moats by accumulating high-quality datasets. For example, Ai Square is betting on end-to-end VLA large models, attempting to enable robots to achieve autonomous decision-making through massive data training, similar to self-driving cars.

On the other hand, the construction of data infrastructure is also progressing in tandem. In March, the "OpenAtom Embodied AI Open-Source Dataset Community" was officially launched.

Initiated by the OpenAtom Open Source Foundation and led by Leju Robotics in its construction, the community is jointly built by core entities including Ant Lingbo, Shanghai Jiao Tong University, Harbin Institute of Technology, Tongji University, Unitree, and Jushi Intelligence. It is the first embodied AI open-source dataset community initiated by a national-level platform.

The establishment of this community marks the transition of embodied AI data from corporate self-use to open-source sharing, aiming to address the industry's three major pain points: "lack of standardization, inconsistent quality, and difficulty in open sharing," providing institutional guarantees and resource coordination for the construction of embodied AI data infrastructure.

Additionally, at the data achievement level, the total downloads of Leju's LET dataset series across all platforms have surpassed 1 million, making it the largest provider of embodied real-world robot data in China.

Its data network covers 9 of the 14 humanoid robot training grounds nationwide, generating 25 million real-world data points annually. The LET dataset spans industrial, commercial, and household domains, encompassing 117 atomic skills and open-sourcing over 60,000 minutes of data. From data collection to open-sourcing to trading, Leju has established a complete chain, delivering a cumulative 20,000 hours of real-world data.

Therefore, the future may no longer be won by who raises the most money but by who can convert capital into data assets and data assets into technological barriers, as only then can they emerge victorious in this long race.

03 Who Qualifies to Be at the Table?

As data capabilities become the new underlying logic of competition, profound changes in industry rules are also emerging:

In the past, the race was about acceleration; today, the starting line itself has become the first hurdle.

The cruel (harsh) endings of Silicon Valley peers who fell before mass production have already validated this point. The collective efforts of top industry representatives are redefining the qualifications to even reach the starting line. Core entities from industry, academia, and research, including the China Academy of Information and Communications Technology, Shanghai AI Laboratory, Baidu, Leju Robotics, Unitree, and Ant Lingbo, have become the first cohort of builders for China's first embodied AI open-source dataset community, covering the entire "industry-academia-research-application" chain.

Leading companies provide industrial scenarios and data governance capabilities, universities contribute cutting-edge research and algorithm validation, and industry enterprises focus on technological breakthroughs in niche areas. This multi-party collaborative pattern is forming industrial synergy and setting benchmarks for industry access.

Institutional filter (selection) is also advancing in tandem. On February 28, 2026, the MIIT's Technical Committee for Standardization of Humanoid Robots and Embodied AI released the "Standard System for Humanoid Robots and Embodied AI (2026 Edition)," jointly compiled by over 120 research institutes and leading companies. The implementation of this standard system means that industry competition is shifting from wild growth to rule-based development.

In summary, 2026 marks a critical year for the robotics industry to transition from "technical validation" to "commercial validation." In the past two years, robotics companies competed on the impressiveness of their demo videos and the imagination of their technological routes. But from now on, the competition will focus on yield rates on production lines, stability at customer sites, and costs after scalable delivery.

As the capital frenzy subsides, only those players who simultaneously build moats in technological depth, data capabilities, and industrial collaboration may remain at the "table."

* Images sourced from the internet. Please contact us for removal if infringement occurs.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?