Behind the Crazy High Valuation: Is MiniMax a Bubble or a Glimpse into the Future?

03/31 2026

03/31 2026

448

448

In the analysis of large model business models, 'Deep Dive into Minimax and Zhipu: Large Models, a Brutal Showdown of Computational Intensity and Funding Endurance?', Dolphin Research stated that in the current context of high model costs and rapid iteration, the large model industry has become a brutal showdown of funding endurance.

However, the true hardcore essence supporting 'financial appeal' cannot be separated from the two fundamental capabilities of model companies: 1) Model capabilities; 2) Product and commercial implementation capabilities.

In this piece, Dolphin Research focuses on analyzing how MiniMax performs around these two fundamental capabilities and offers a superficial discussion on how to judge MiniMax's asset value.

Here is a detailed analysis:

I. Model Capabilities: Intelligence is Not Top-Tier, but Strength Lies in Starting with Multimodal

Firstly, to develop a to C large model, Dolphin Research believes that multimodality is almost a basic requirement:

a. In current mobile internet apps, the content input by users and the content displayed to users typically involve full-media interactive forms such as text, images, videos, and voice;

b. Entering the Agent era, AI Agents need to be able to read text, recognize images, listen to audio, and even watch videos to help users perform operations on PCs or mobile devices.

Combining these two basic requirements means that a qualified large model company must possess multimodal input and output capabilities. Ideally, like Gemini and OpenAI, during model training, raw materials such as text, voice, and video are directly converted into unified Token IDs (Tokenizers) and trained using a unified neural network.

Even if this is not achievable, at least relatively smooth multimodal fusion capabilities should be present. In this regard, the two model providers currently listed in Hong Kong both possess such capabilities.

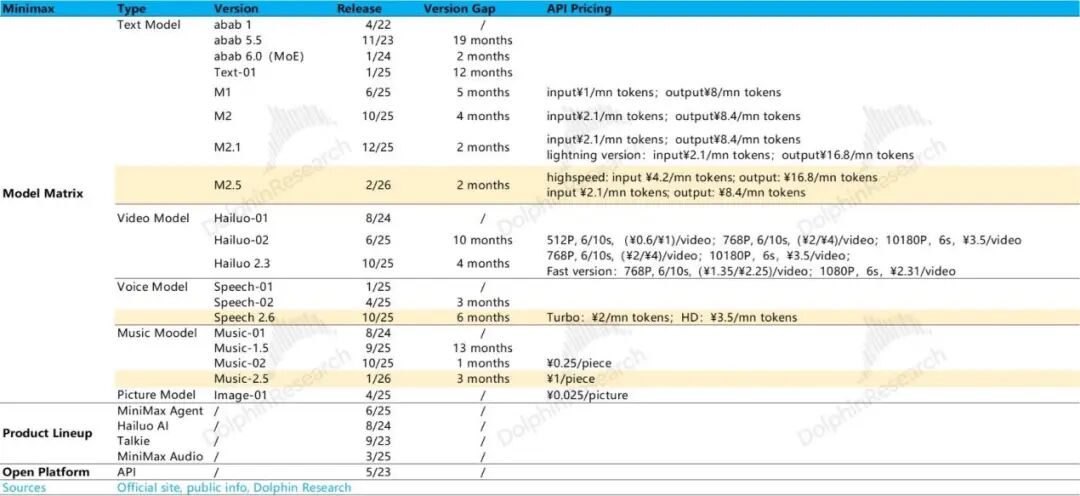

In this aspect, MiniMax is quite excellent, having adopted a multimodal approach very early on. Due to its product focus on pan-entertainment (can be translated as 'pan-entertainment' in this context), the company has a separate music model in addition to its voice model, and its model iteration speed is relatively fast. Across various vertical modalities, updates are generally made on a quarterly basis, with the base language model updating from M2.5 to M2.7 on a monthly basis.

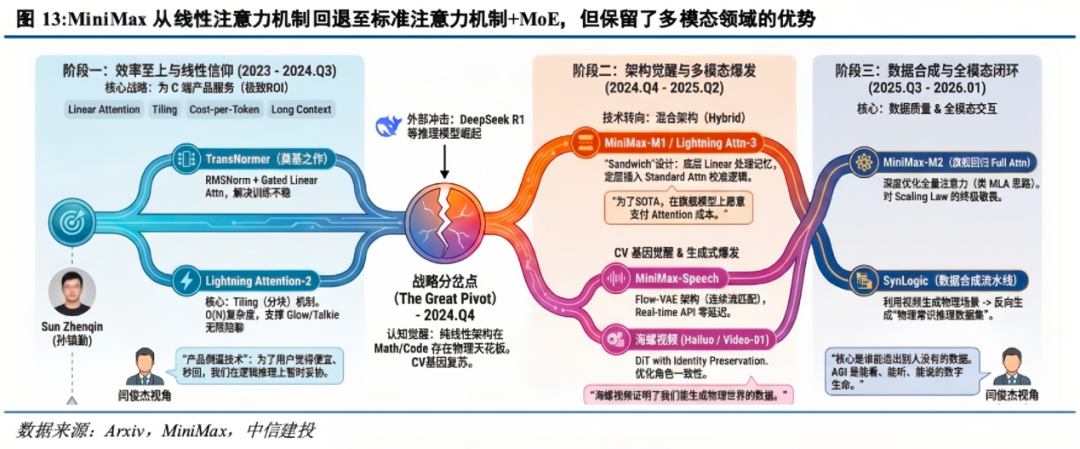

Additionally, from the company's path iteration over the past two years, it can be seen that DeepSeek represents a clear strategic impact on the company's development. Before DS, MiniMax's organizational driving structure was more product-demand-driven, pushing model technology and route selection.

The emergence of DeepSeek vividly demonstrated to Chinese peers how algorithmic innovation drives model capabilities, which in turn drives user adoption and use cases. After DeepSeek set the example, MiniMax began to focus more on model technology itself, entering a phase where model technology drives product performance iteration, with models undergoing architectural innovation and multimodal research and development.

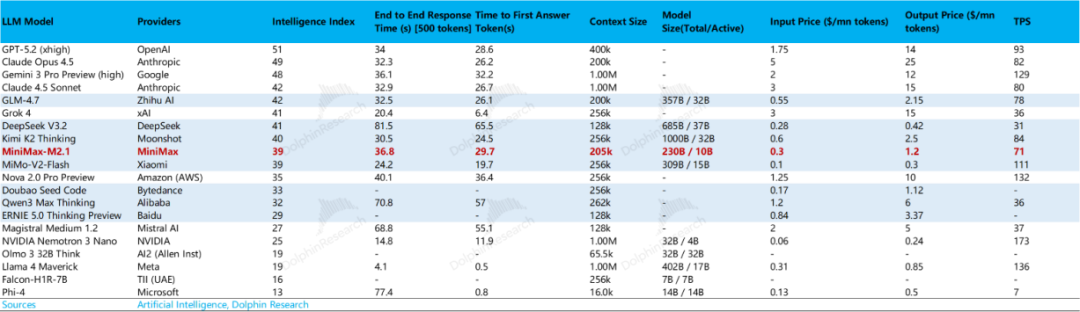

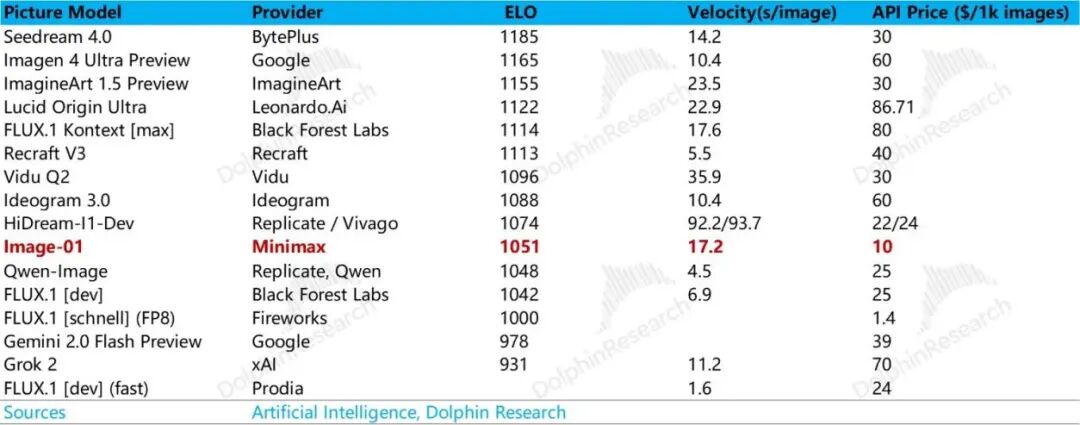

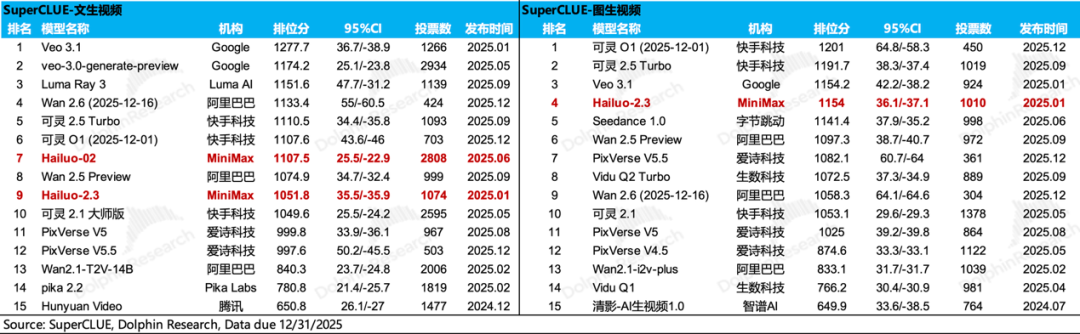

From the perspective of various modality classifications in models, among the listed models, MiniMax's overall intelligence level is not the highest, but it is continuously iterating, maintaining a leading position overall.

MiniMax's models primarily excel in having a decent intelligence level + multimodal capabilities, with the most competitive pricing. In the Agent era, where Token consumption is rampant, 'affordability' in pricing has become increasingly important.

Dolphin Research looks at the ratio of Token input price to model intelligence index. Among large models with higher intelligence than MiniMax, only DeepSeek has lower pricing, but DeepSeek primarily focuses on language modalities. When considering multimodal capabilities, DeepSeek's appeal diminishes.

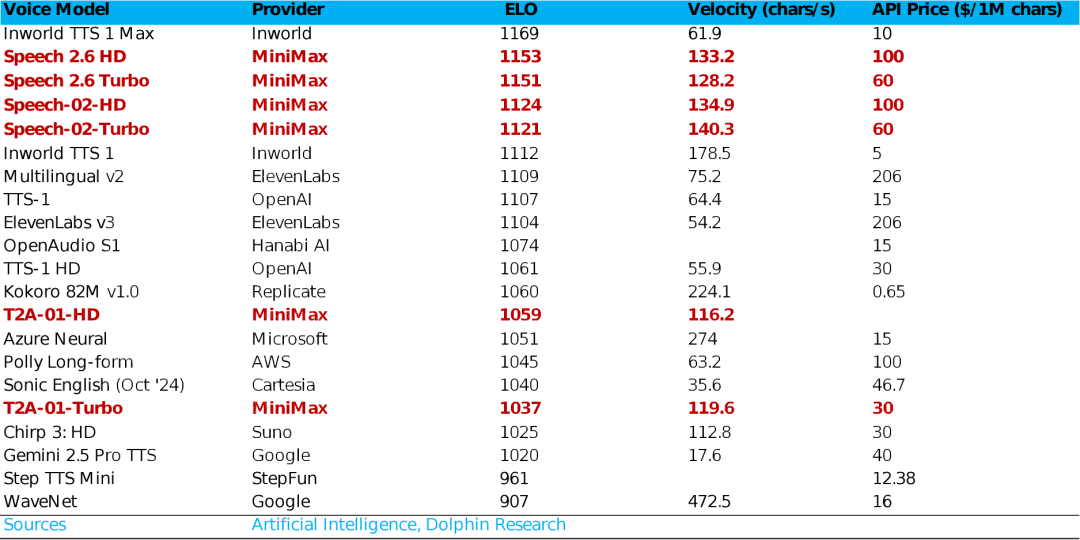

The core factor limiting model pricing is still the model's own intelligence level. This is very evident in MiniMax's voice models, where higher intelligence levels allow for higher pricing ceilings:

The Speech series models rank high in terms of Elo value (dimensions such as naturalness, expressiveness, and emotional authenticity of generated speech) and have significantly higher pricing compared to peers.

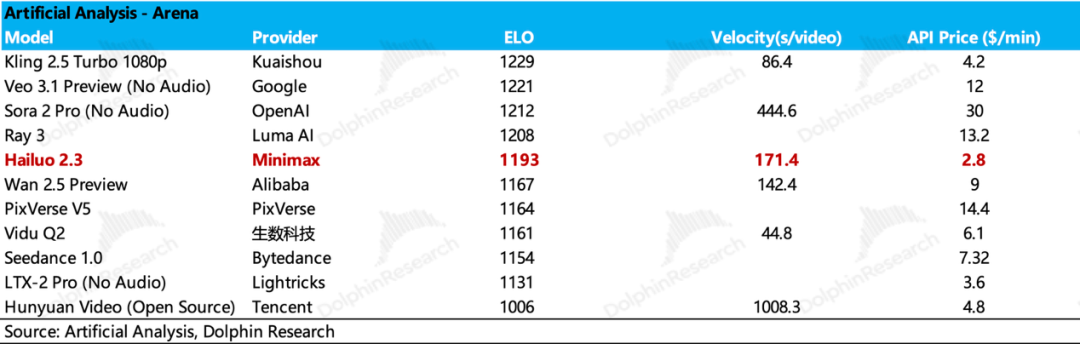

The video model Hailuo 2.3 behind the video production platform has slightly weaker industry competitiveness in vertical modalities compared to voice models but is stronger than language models. It represents a model with above-average performance and extremely competitive pricing.

However, in actual scenario implementations, not all scenarios require the 'brute force' approach to achieve the highest level of intelligence. When models penetrate daily scenarios on a large scale, cost-effectiveness, especially the level of intelligence per unit cost, becomes a realistic consideration for deployment.

MiniMax becoming the largest open-source model supporting AI 'shrimp farming' platform OpenClaw also reflects that at the stage of large-scale implementation, cost per unit of intelligence is one of the core considerations for enterprise procurement.

II. Behind Extreme Cost-Effectiveness: Shining are Unparalleled Manpower Efficiency and Computational Resource Input-Output Ratio

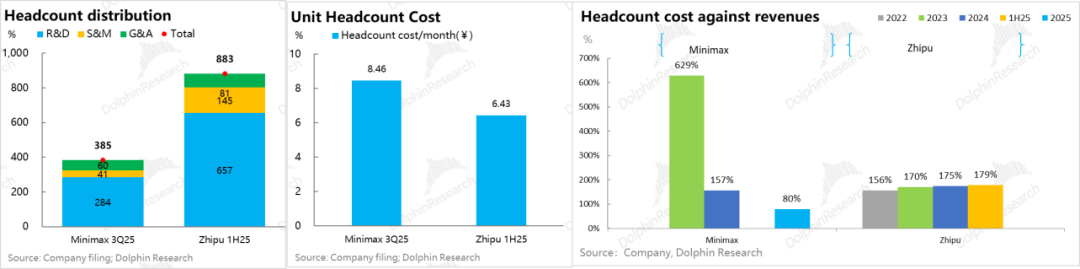

From a pricing and unit intelligence perspective, MiniMax is exactly the most cost-effective among first-tier multimodal model providers. Behind this cost-effectiveness lies unparalleled efficiency in manpower and investment. Compared to Zhipu, MiniMax demonstrates extreme organizational efficiency where 'fewer people can achieve more':

a. The total number of employees will be 428 by the end of 2025, with an approximate monthly cost per employee (excluding option expenses) of 110,000 yuan, compared to Zhipu's 60,000 yuan in the first half of 2025.

b. However, in terms of revenue generated per employee, due to MiniMax's to C asset-light subscription/recharge model, its manpower efficiency is significantly higher than Zhipu's offline to B project-based model.

c. In addition to the input-output ratio of manpower, MiniMax also has higher absolute computational resource investment and corresponding revenue output from computational resource investment.

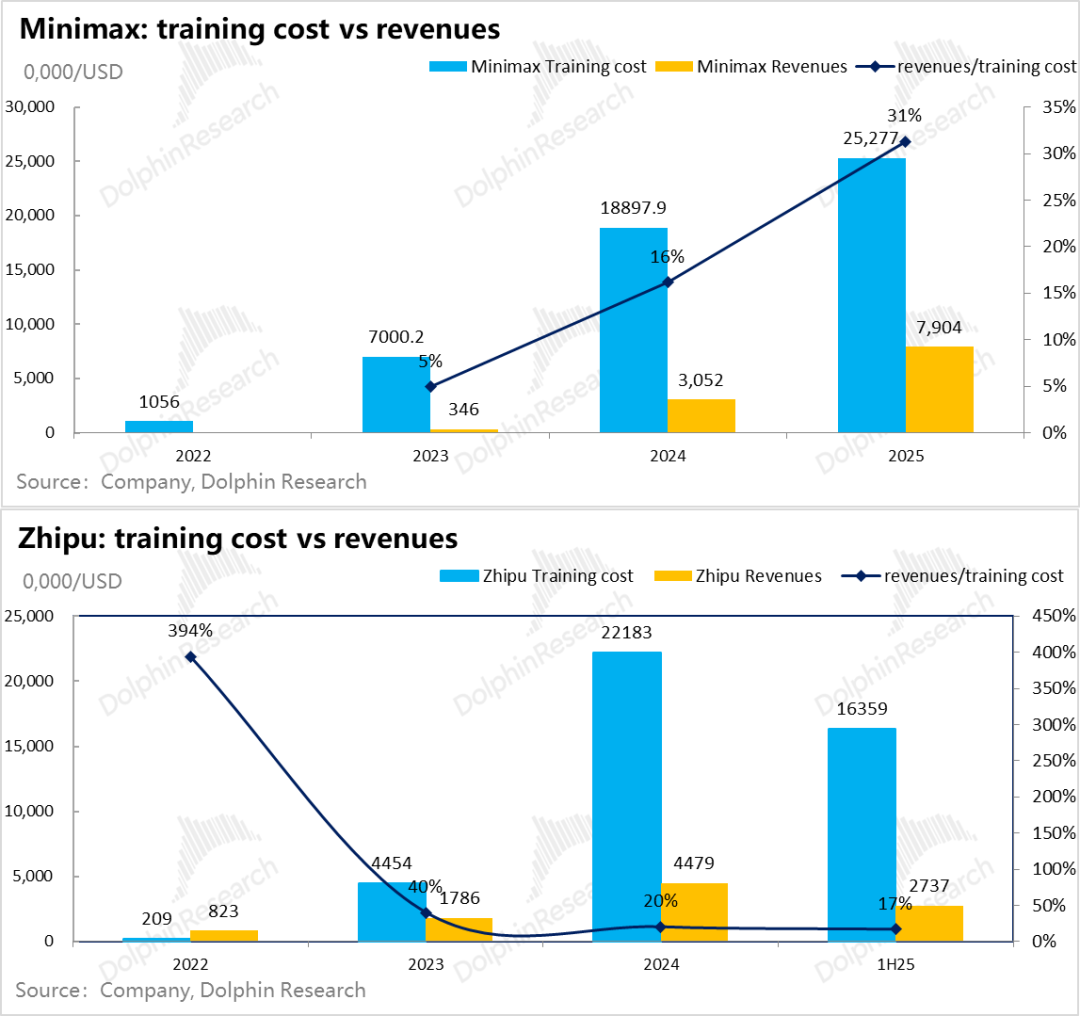

For example, in 2025, MiniMax invested approximately $250 million in training costs (nearly 1.8 billion yuan), while Zhipu spent $160 million (over 1.1 billion yuan) in the first half of the year.

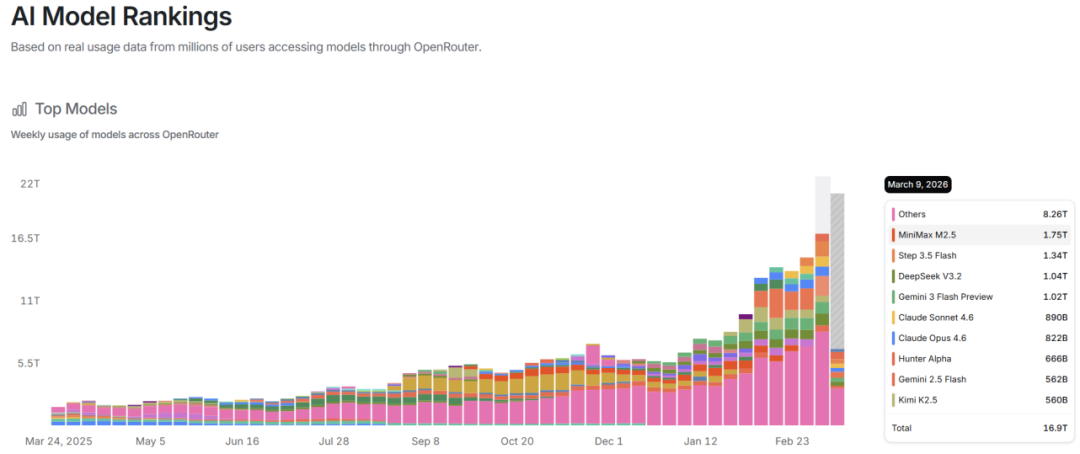

However, in terms of investment recovery capability, whether it is MiniMax's ability to cover training expenses with revenue or the token invocation volume displayed by third-party OpenRouter, MiniMax demonstrates clear superiority.

Putting these points together for a comprehensive evaluation, it can be basically seen that under the impact of DeepSeek, MiniMax has ultimately formed a route where technology itself drives model development. It has achieved multimodal capabilities with basically controllable investment, and the performance of various vertical models is generally above average.

When we comprehensively consider the model's intelligence level, diversity, and the ability to control cost investment behind it, MiniMax becomes a unique presence in the large model circle.

III. Product Implementation: The Top Player Among Independent Model Providers

For model providers, model research and development is the top priority, but entering 2026, relying solely on models is no longer sufficient, especially for model providers that are not global leaders.

The ability to implement models in scenarios has become an indispensable key link in the positive cycle of financing, i.e., the story of a full-stack closed loop for model providers. It is precisely in this aspect that MiniMax, with above-average model performance, truly stands out among independent model providers.

MiniMax's strategic choice in this regard is also very interesting: From the beginning, model and product development were almost simultaneous, naturally focusing on both products and technology.

Moreover, in terms of commercial implementation choices, unlike Kimi, it focuses on to C self-developed product implementation, avoiding the crowded Chatbot track. For to B (Model-as-a-Service) implementation, it focuses more on asset-light, low-manpower API interface services.

3.1 Calculated Commercial Choices: to C Differentiation + Simultaneous Overseas Expansion, Avoiding Becoming 'Cannon Fodder' Early On

Furthermore, in terms of to C commercial implementation, as an independent model provider, there are two very 'calculated' choices:

a) It did not follow Kimi's to C implementation method of relentlessly pursuing general-purpose AI chat applications 'Chatbots' - a 'traffic gateway' in the AI era that major companies are willing to fight for at all costs - thus avoiding becoming 'cannon fodder' in the major companies' AI gateway battles (the red envelope battles during this year's Spring Festival season illustrate everything).

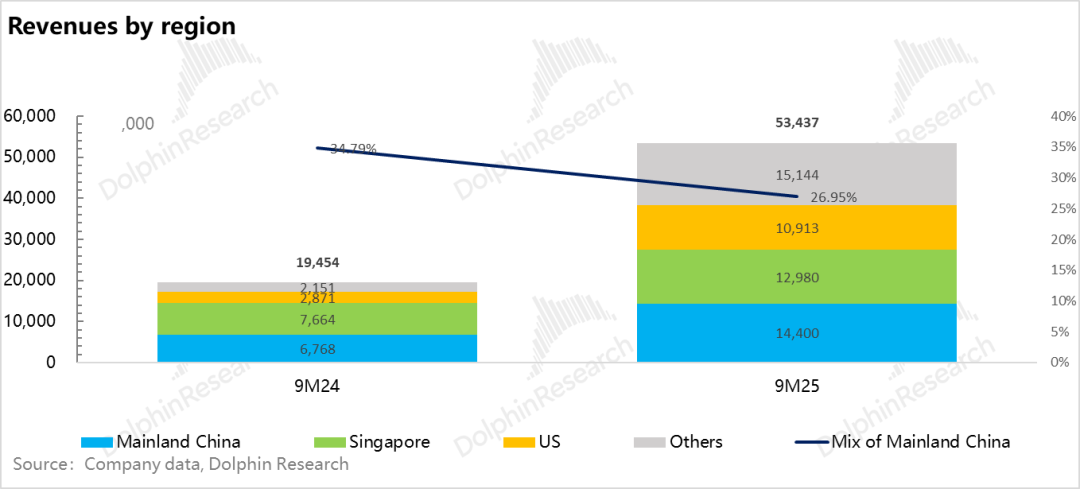

b) Global commercialization was launched simultaneously from the beginning: It positioned itself as a global market from the start, so the AI-native products and API interface services it launched were globally available from the beginning. The stronger payment capability in overseas markets also provided MiniMax's model research and development with more 'recovery' space.

From an overall commercial implementation perspective, focusing on to C multimodal, avoiding Chatbot + prioritizing asset-light API services for to B business (not choosing to B project-based commercialization) has prevented it from becoming cannon fodder in the marketing battles like Kimi during the major companies' ChatBot battles.

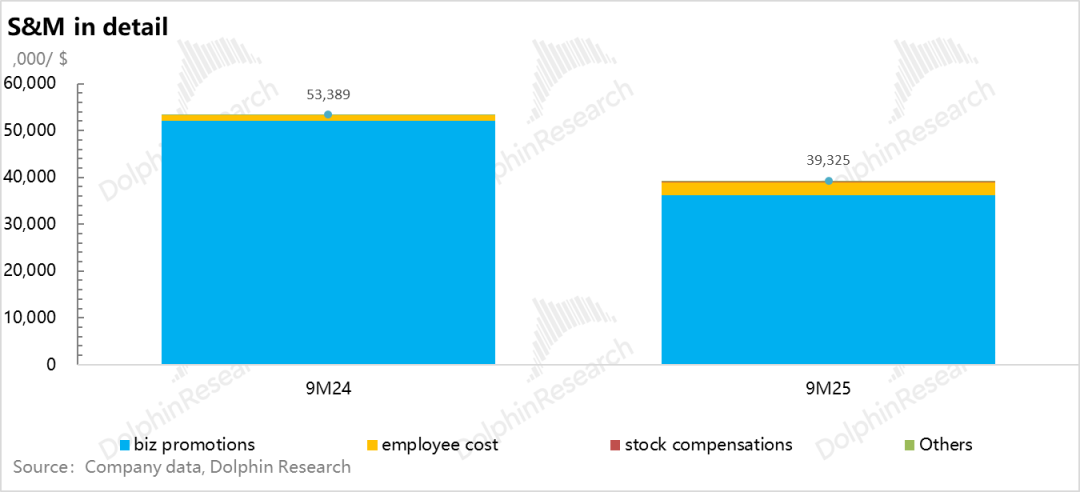

Moreover, after the impact of DeepSeek, MiniMax realized that model capability iteration is the core driver for acquiring customers and usage time, so it even reduced the absolute value of customer acquisition expenses amidst the major companies' battles.

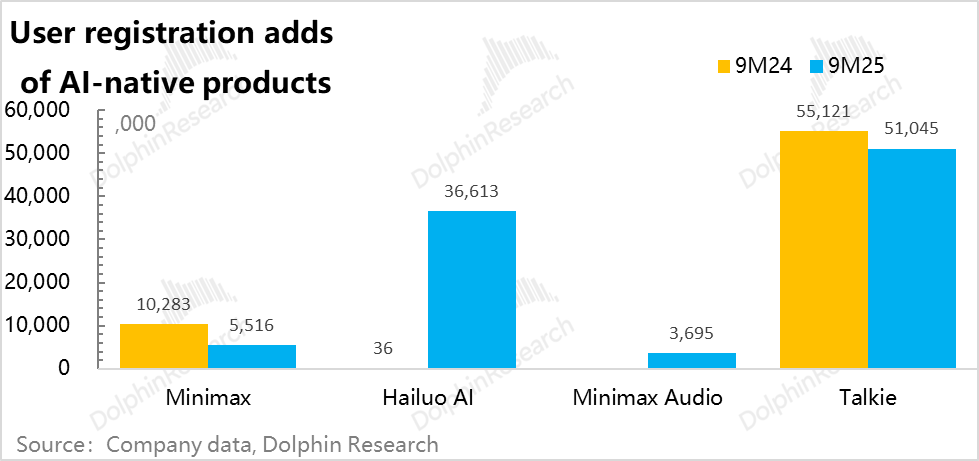

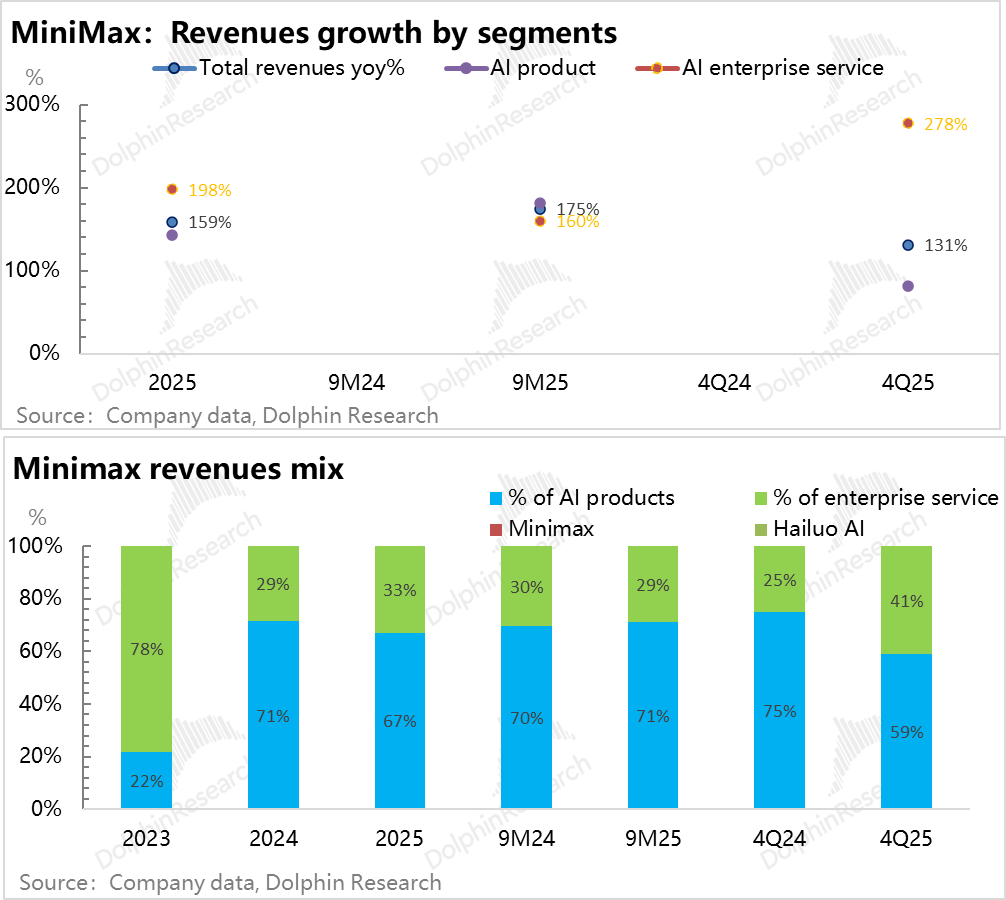

Focusing on model research and development, using models to iterate products, and reducing marketing expenses on the product side resulted in a significant decline in MiniMax's customer acquisition cost per new registered user in 2025 - dropping from $0.8 in 2024 to $0.4, directly halving.

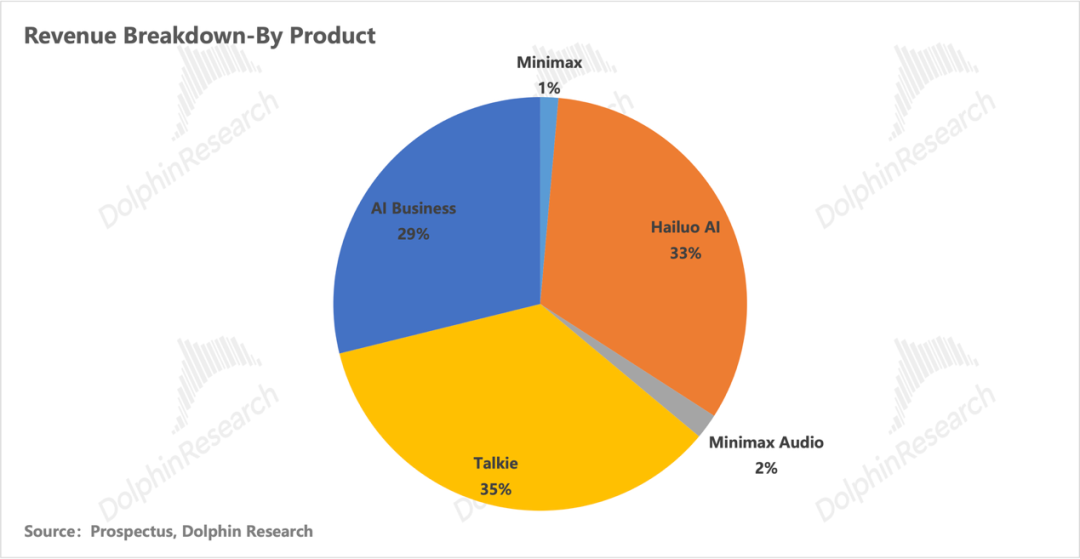

Under the product strategy of model multimodality and C-end differentiation, MiniMax has successfully developed two niche yet popular overseas products: one is the AI chat companion app Talkie (known as Xingye in China), and the other is the video generation service Hailuo AI (known as Hailuo in China).

While the chat companion platform Talkie is not popular in China, it ranks relatively high in the download charts for niche apps overseas. These products also serve as the foundation for MiniMax AI's commercialization, positioning it as a leading independent model provider.

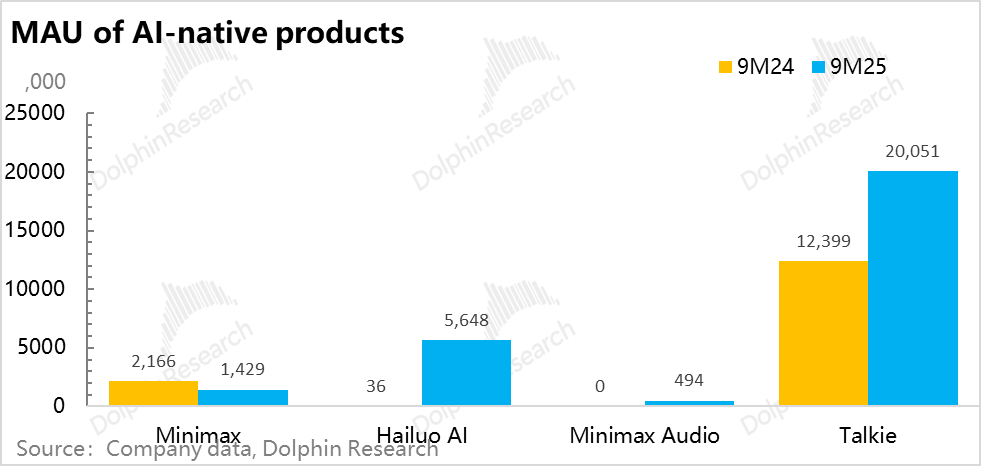

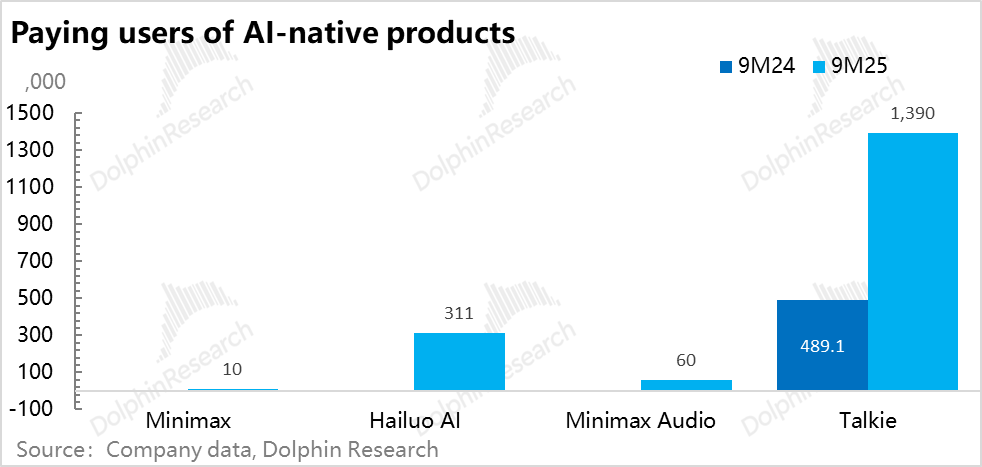

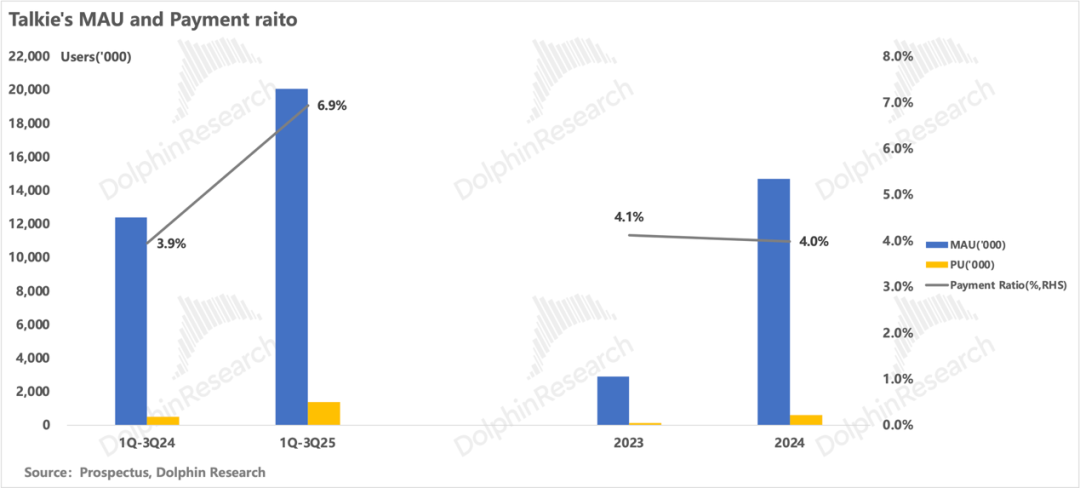

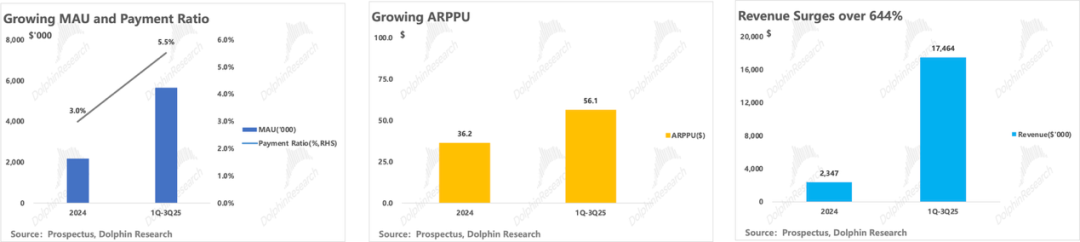

However, in terms of scale, among the app family, Talkie, which has the most users, had 20 million monthly active users (MAUs) by the end of September 2025, while the newly launched Hailuo app had only 6 million MAUs in 2025.

In other words, although the company has achieved a closed loop from AI R&D to AI-native product deployment, its so-called AI products—both in terms of app content and user base—still have a long way to go before reaching applications with over 100 million users.

3.2 Models are expensive, and monetization must keep pace

In 2023, when MiniMax primarily had only Talkie with less than 3 million MAUs, the company began to focus on monetization. However, the monetization potential with just a few million MAUs was limited.

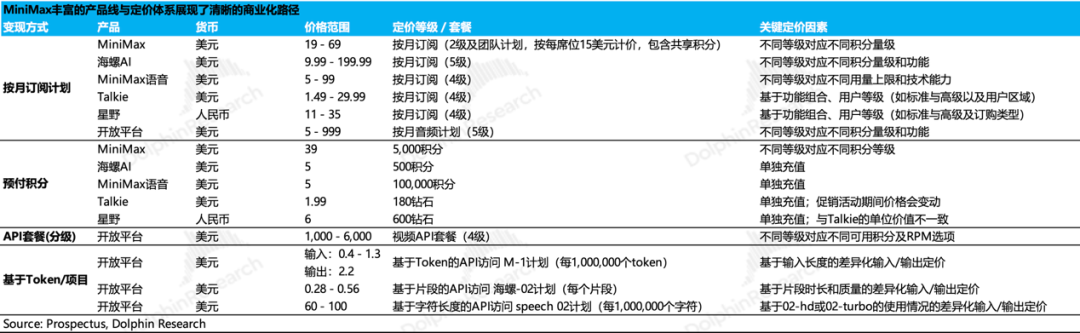

As an early investor, MiHoYo's influence is evident in MiniMax's product monetization strategies, which are not fundamentally different from those of pan-entertainment (pan-entertainment) products. Both rely on internet value-added services, including subscription and top-up services.

However, in terms of business essence, as Dolphin Research has stated, the nature of AI product subscriptions is the purchase of tokens for input and output during the model inference phase.

1) Talkie/Xingye: Emotional chat companions, niche but beautiful

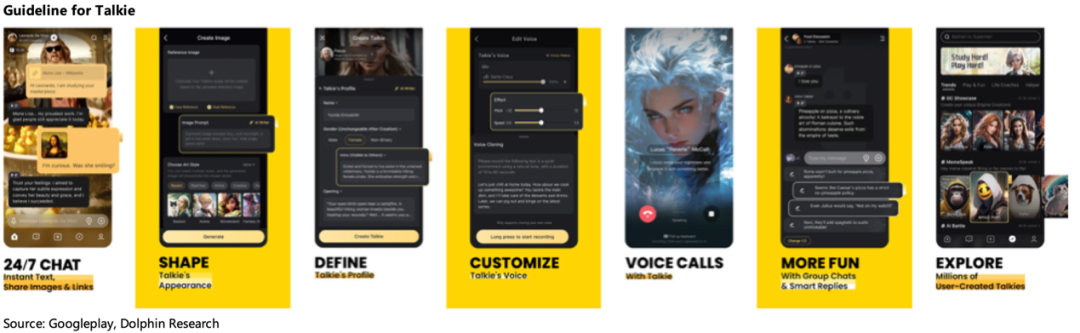

Talkie (overseas) and Xingye (domestic) can be understood as AI emotional chat companion apps. Users can create AI virtual characters with distinct strengths and skills, and other users can interact and co-create with these AI characters.

Dolphin Research noticed during app usage that for some virtual boyfriend/girlfriend AI characters, users invest emotionally and engage in consumption behaviors such as celebrating birthdays and buying gifts for the AI characters.

Despite its niche audience due to its strong interactive and emotional focus, Talkie boasts superior user engagement compared to efficiency tools like AI assistants and AI search (typically 10-20 minutes), with an average daily usage time exceeding 70 minutes per user.

Additionally, through product designs like virtual cards and gifts, Talkie/Xingye functions not just as an AI chat tool but as a community entertainment platform that integrates "companionship + gaming + socializing + transactions."

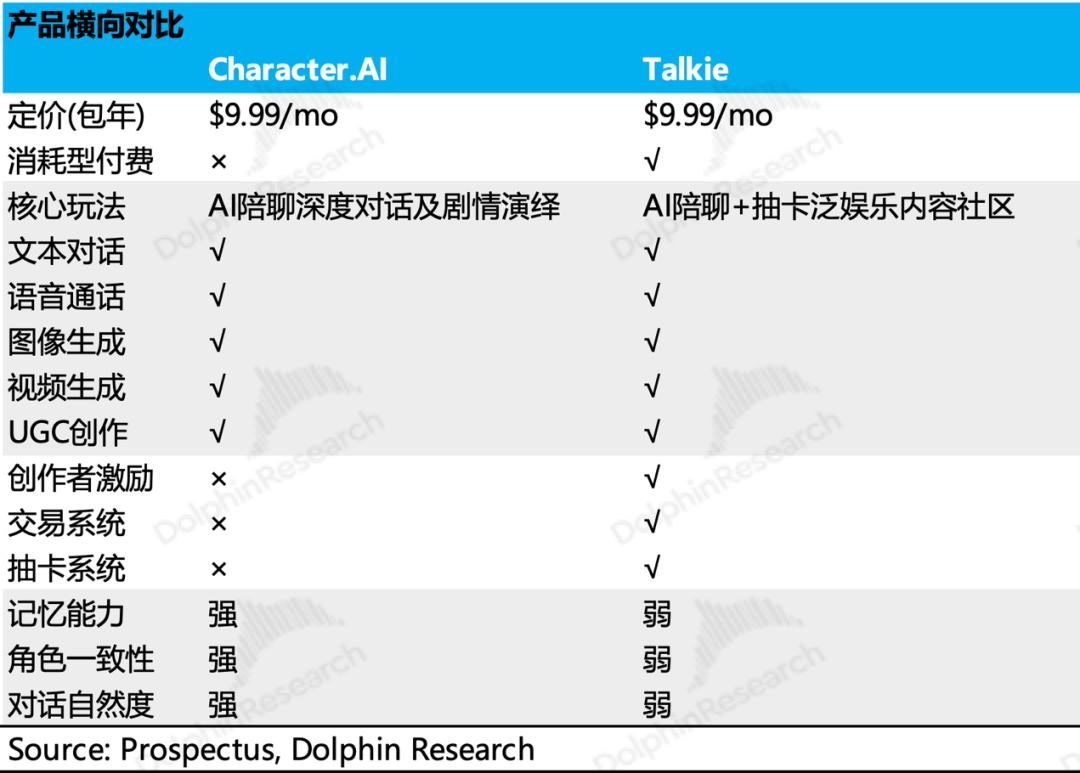

a. Creation side: The Xingye Marketplace allows transactions of Xingnian cards (cards unlocked or purchased by users during interactions with AI characters, with certain scarcity attributes), and creators receive a share of the revenue. In comparison, Character.AI primarily focuses on a "love-driven" chat model, lacking a strong community feel.

b. Consumption side: Blind box card draws and secondary trading mechanisms endow (impart) cards with scarcity and circulation premiums, enhancing user stickiness. Leaderboard rankings further stimulate activity, introducing a "ranking logic" that further motivates user spending.

From this, it is evident that once a product achieves a certain MAU, the front-end monetization forms are largely similar. Talkie employs a pan-entertainment monetization approach, with the underlying assets for transactions and purchases being AI-generated content.

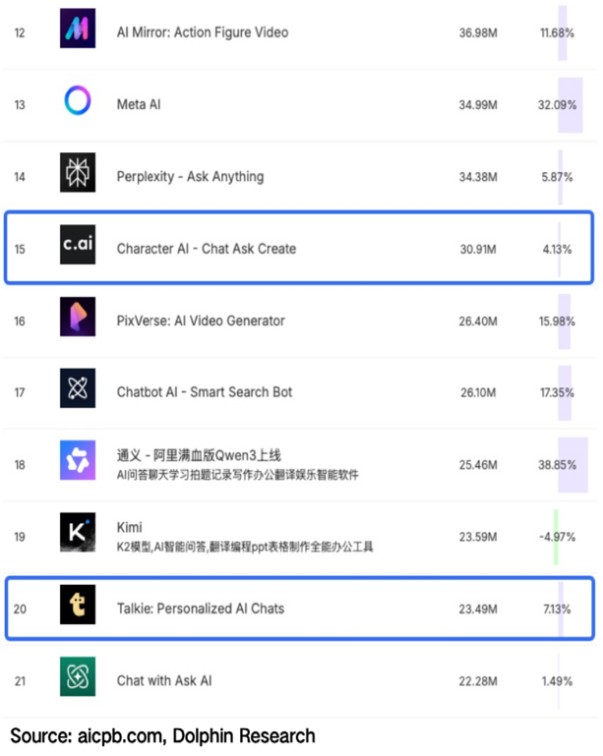

Talkie is the second-ranked player in its niche segment, maintaining high MAU growth and steady pay (payment) penetration. The prospectus discloses that Talkie/Xingye's MAU has reached 20 million, with a year-over-year growth rate of approximately 62%. According to aicpb data, in the December 2025 global AI product app monthly active rankings, Talkie/Xingye ranked 20th, second only to Character.AI in the companionship category.

In terms of payment conversion, the payment rate increased by 3 percentage points year-over-year to 6.9%, breaking the long-standing bottleneck of around 4% since 2023 and significantly driving the year-over-year growth of paying users by 184% to nearly 1.4 million.

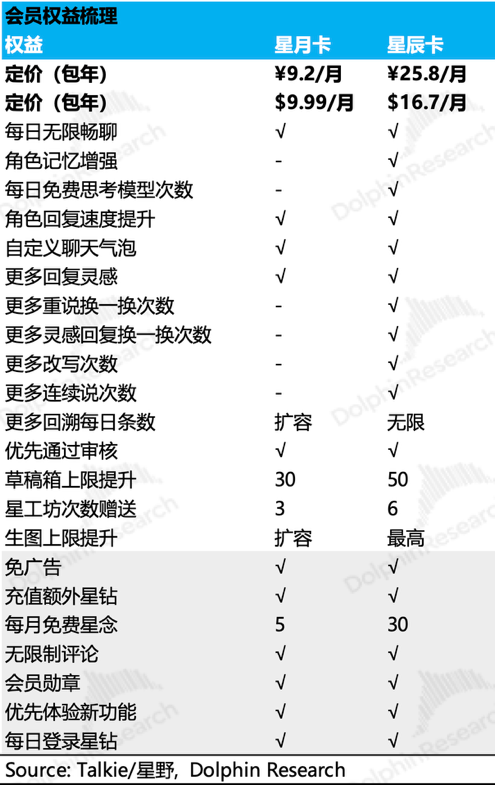

Value-added monetization occurs through dual channels of subscriptions and in-app purchases: a. Tiered subscriptions; b. High-frequency in-app purchases: mainly low-frequency ($6+) Xingzuan top-ups paired with high-frequency card draw consumption.

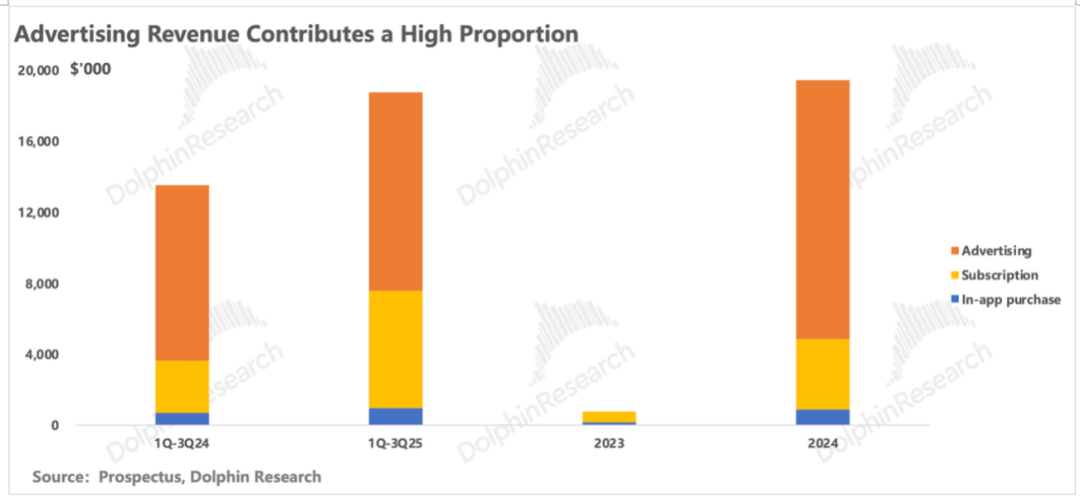

Talkie's unique feature—advertising: As the only AI product app with over 10 million MAUs, it is also the only AI app with advertising revenue, which accounts for over 60% of Talkie's total revenue.

From Talkie's advertising monetization, it is evident that even for AI-native apps, when MAUs exceed 10 million and daily active usage reaches 70 minutes, advertising monetization becomes almost natural.

Other models and products, such as MiniMax Audio, have not generated significant buzz or revenue.

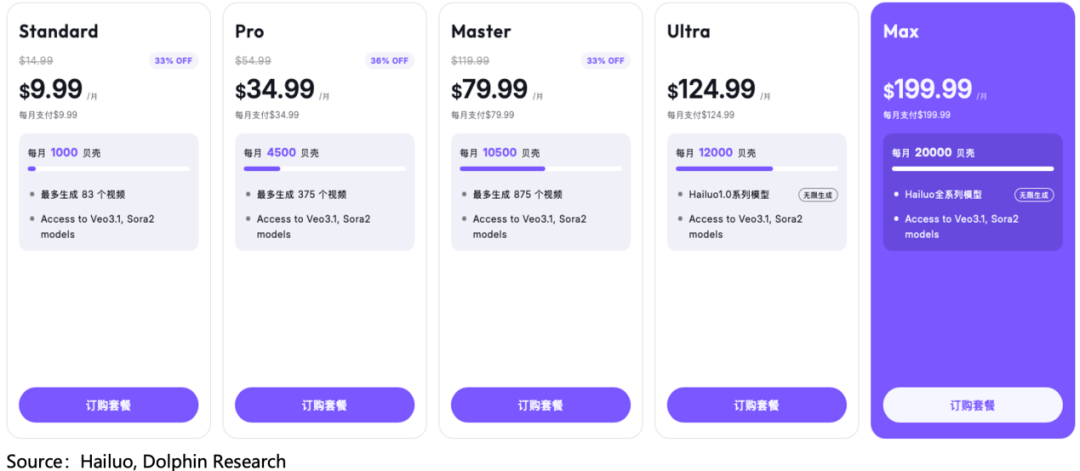

2) Hailuo AI: Overseas-driven, capturing both domestic and international markets

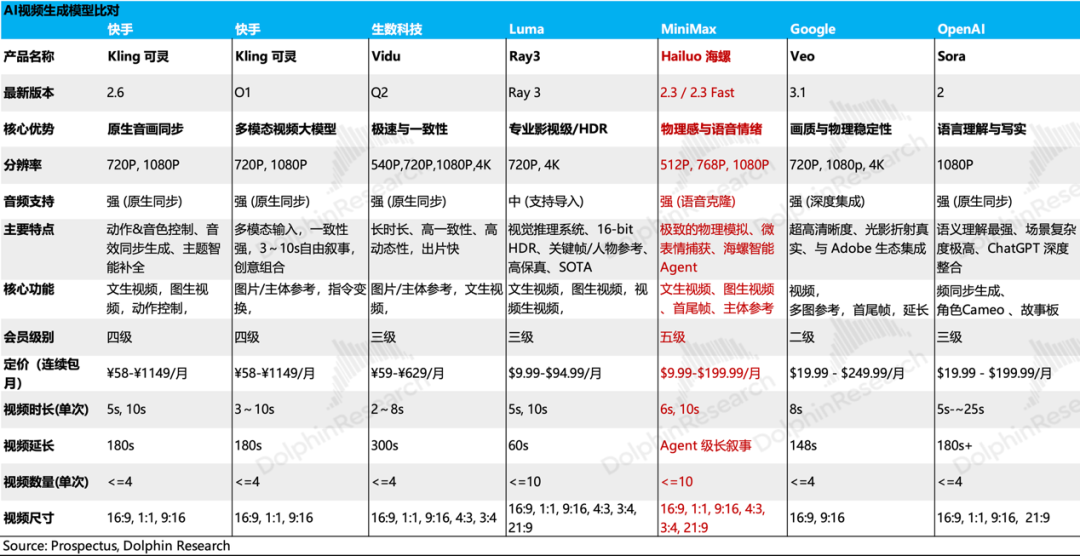

Hailuo is MiniMax's video generation model product, capable of providing real-time high-definition video (text-to-video, image-to-video), image generation, and Agent functions, primarily targeting creators and advertisers. Without enterprise certification, it is effectively a B2C product.

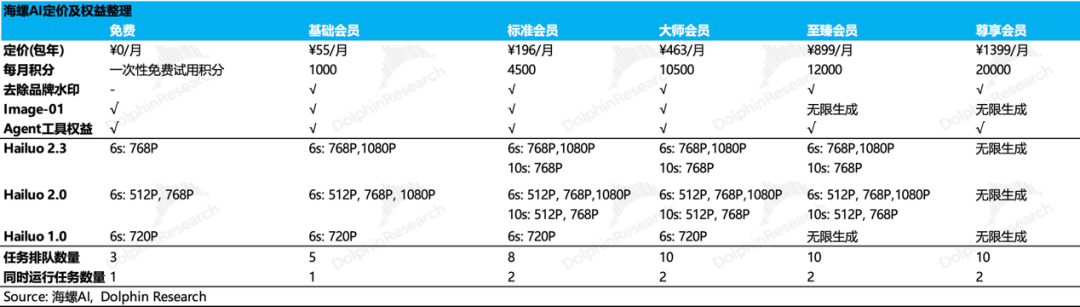

The model iterations are as follows:

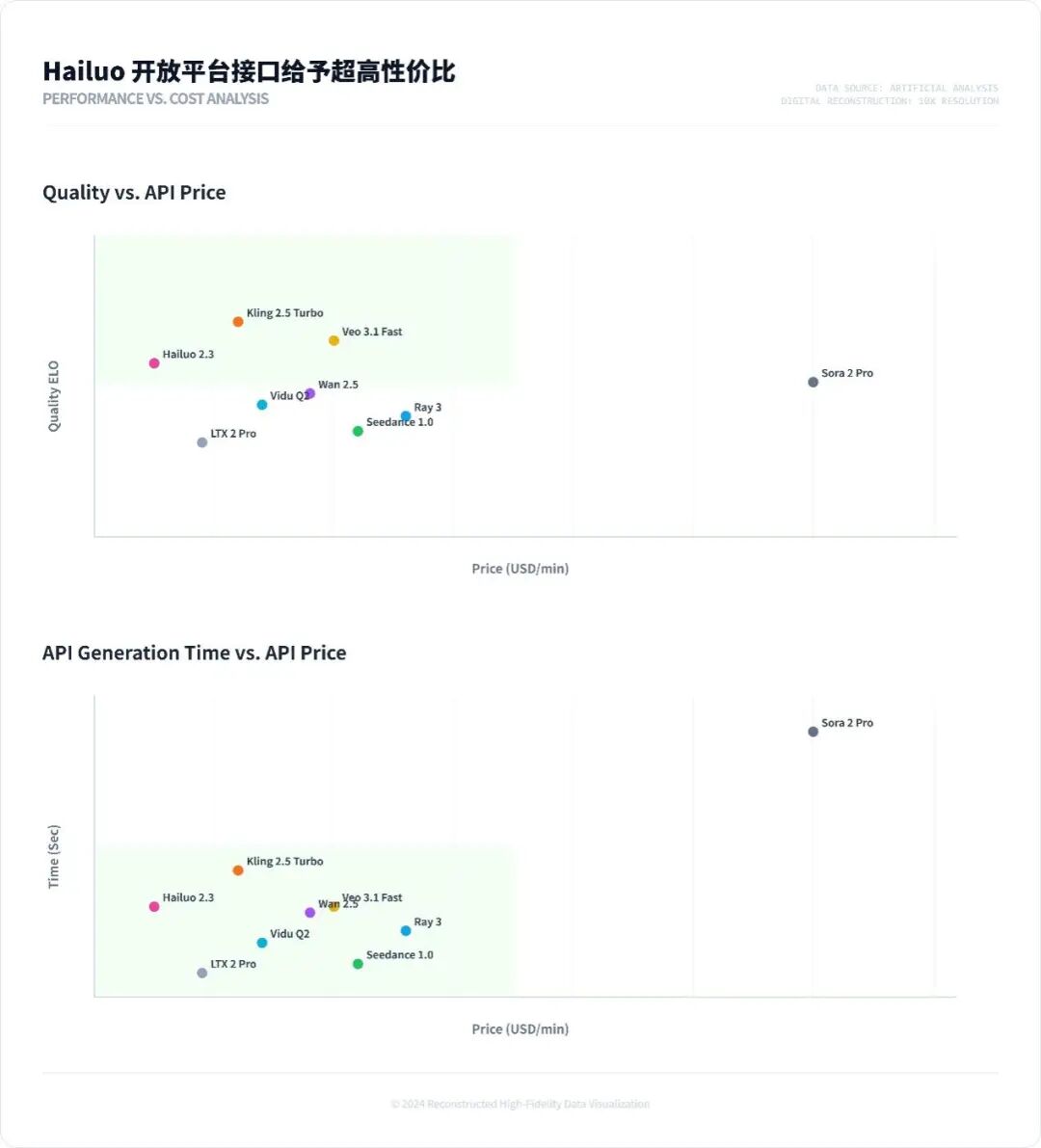

Hailuo's model ranks in the upper-middle range on several mainstream benchmarks; it has a pricing advantage domestically but lags behind Kling in performance. Revenue generation primarily relies on overseas markets.

In overseas markets, MiniMax adopts a multi-video model fusion strategy, known as the "Model Container." Simply put, in addition to its proprietary model Hailuo, it integrates video generation models like Veo and Sora, offering users more flexible choices.

When researching Meitu previously, we noted that Meitu also employs a Model Container strategy. Clearly, MiniMax, as a large model provider, has an advantage by directly accessing RLHF data for model training and optimization.

Moreover, due to Hailuo's relatively high subscription pricing, the high ARPPU supports a revenue explosion of over 7x in the first nine months of 2025.

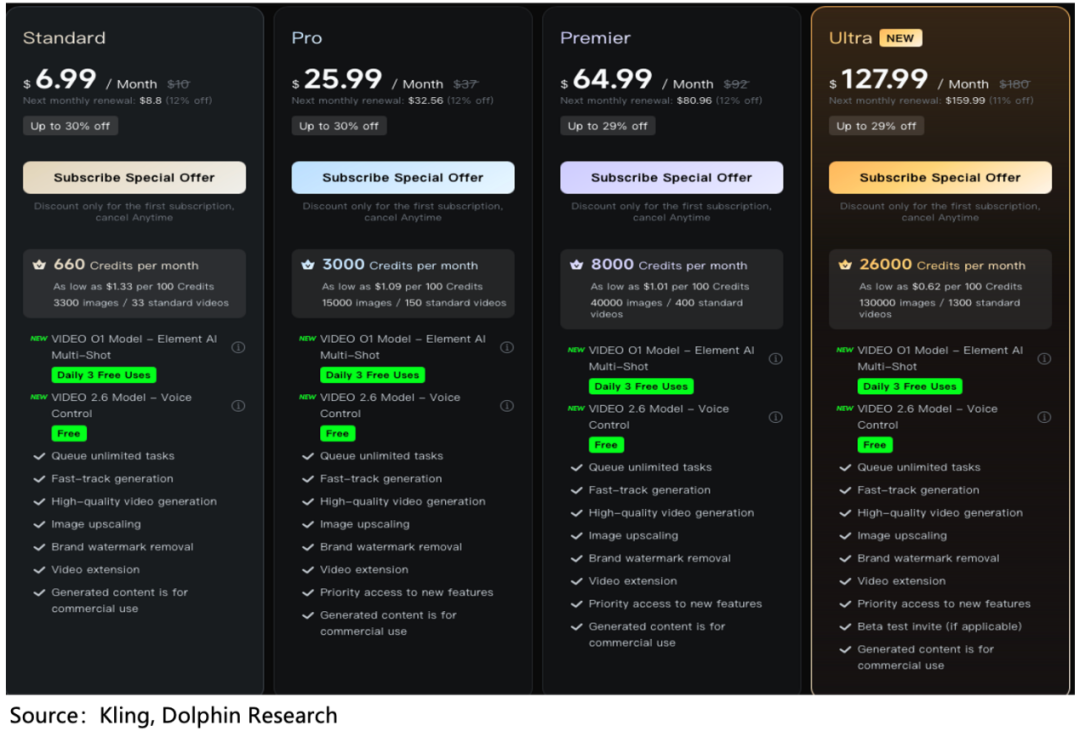

Hailuo's B-end open platform (API interface): It primarily competes on low pricing when the model performs reasonably well. The product has shortcomings in scenarios requiring high timeliness. In contrast, Kling balances high image quality, low cost, and inference speed, making it a leader in this segment.

Other models, primarily MiniMax Audio (based on the Speech model), have a relatively small user base. Even with a high payment rate and decent unit pricing, their revenue generation is average.

So, at present, apart from Talkie and Hailuo, what other products and services can genuinely support high valuations with growing revenue? Dolphin Research believes the answer likely lies in the B2B API business and the C-end productivity scenario MiniMax Agent.

1) Rising star: API, already a clear winner

As Dolphin Research previously stated, AI R&D competes on model intelligence, but during inference deployment, the intelligence per unit cost is equally important. After incorporating the advantages of multimodality, the intelligence per unit cost is the highest among open-source models.

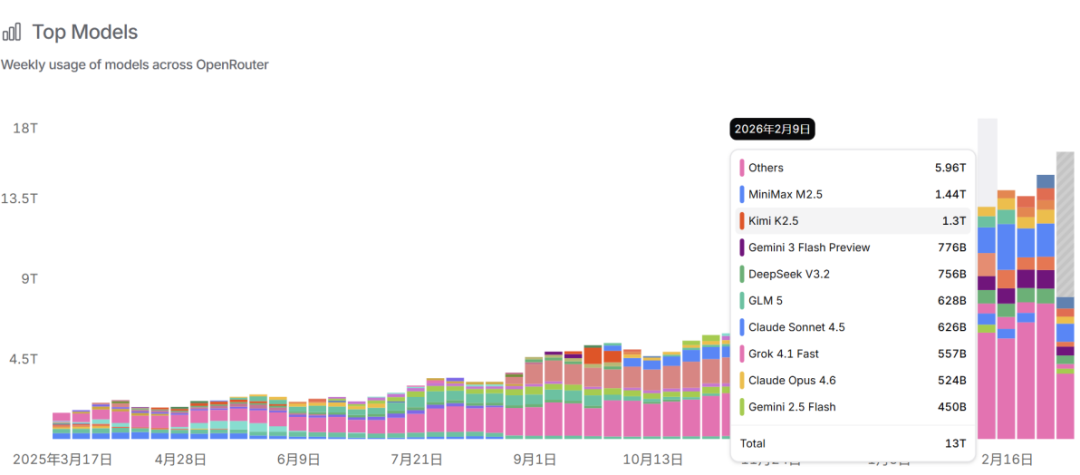

According to company financial disclosures, after the launch of OpenClaw in November 2025, MiniMax's API interface revenue accounted for nearly 41%, with a year-over-year growth rate of nearly 300%.

During the earnings call, the company disclosed that its ARR reached $150 million in February, up from an average monthly ARR of around $100 million in Q4. After the release of the M2.5 text model, the average daily token consumption in February increased sixfold compared to December 2025.

A clear trend now is that "raising lobsters" has become a core scenario for AI terminal deployment. For most scenarios with weak payment capabilities and not aimed at replacing productivity tools, using closed-source models like Claude is too "luxurious" (MiniMax $1-2 per million tokens vs. Claude's pricing around $20).

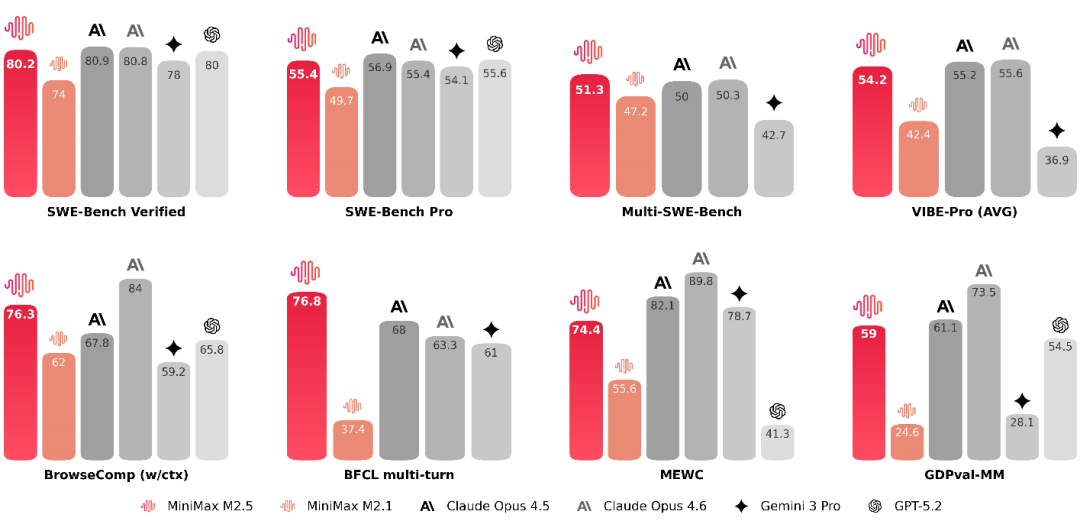

Compared to the cheaper-priced DeepSeek, the MiniMax model M2.5 excels in Agent and office collaboration capabilities. On leaderboards measuring Agent performance, M2.5 demonstrates strong results across various dimensions, including code resolution (SWE-bench verified), tool invocation and instruction adherence (BFCL & VIBE), and multimodal validation (GDPval-MM).

In other words, in scenarios where Agents are used, replacing Claude with MiniMax reduces costs without a significant decline in performance. Moreover, the launch of M2.5 perfectly coincided with the surge in popularity of OpenClaw, which became a key driver for the substantial increase in M2.5's usage volume.

2) Rising Star: Is AI Co-work the Next Big Thing?

If we examine Claude's two major post-holiday innovations: a. Claude Cowork, an AI agent embedded within the Claude desktop environment capable of autonomously executing multi-step tasks; b. Equipping this Agent with various business function plugins, such as sales and marketing, finance, legal, customer support, data analysis, and more.

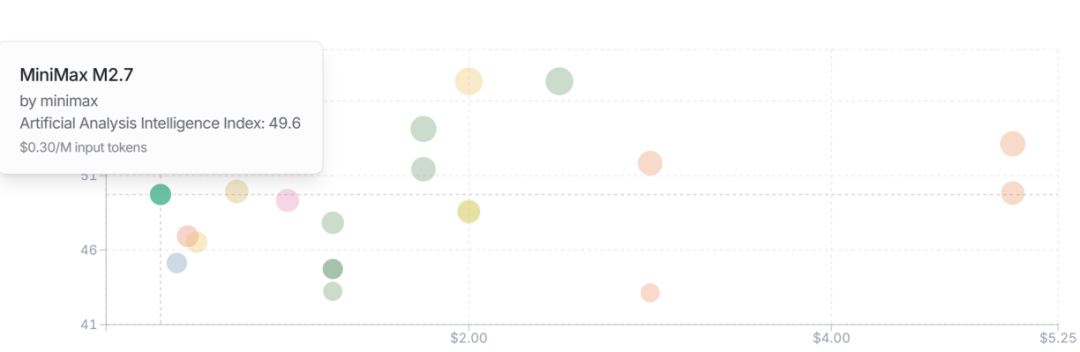

The newly launched MiniMax M2.7 model has been specifically optimized for Agent tasks. Beyond software engineering and Office editing tools, the MiniMax Agent powered by M2.7 is increasingly resembling an open-source version of Claude Cowork.

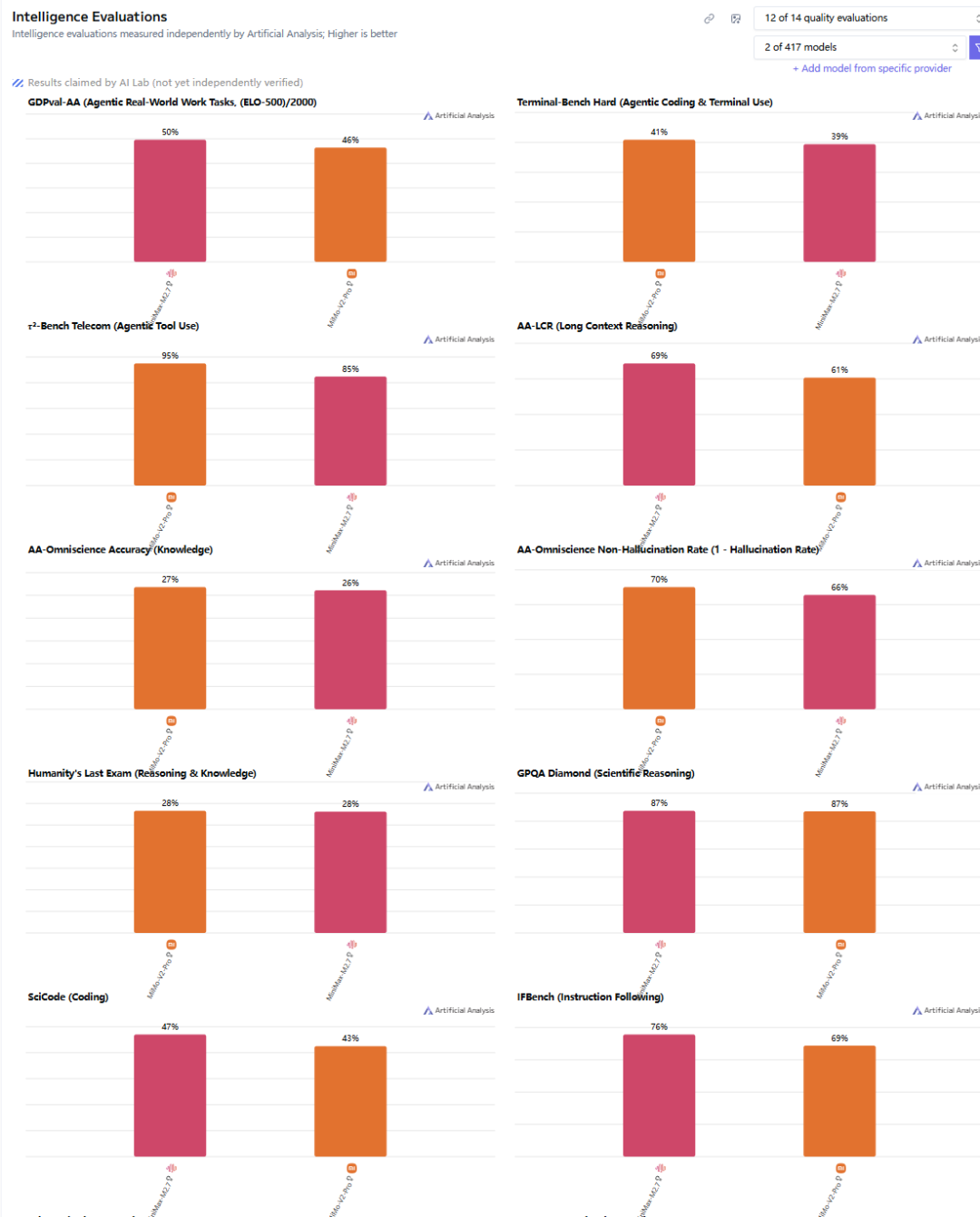

With the improvement in model intelligence, 2026 is poised to be a breakthrough year for AI transitioning from Coding to CoWork. Among domestic models, besides MiniMax's early focus on office Agents, the newly released Xiaomi Mimo-V2-Pro shares a very similar positioning. Market rumors suggest that the delayed release of the new DeepSeek V4 will also emphasize Agent capabilities.

Currently, Xiaomi's newly launched Mimo is multimodal and emphasizes Agent and Coding capabilities. Specifically, it performs slightly better in real-world Agent tasks, while Xiaomi excels in tool invocation. In terms of Coding abilities, they are on par, with Mimo-V2-Pro surpassing MiniMax in Openrouter usage volume over the short term. Overall, both have their strengths, with minimal gaps between them.

However, Mimo-V2-Pro is currently in a limited free trial phase. After this phase ends, Xiaomi's output pricing ranges from $3-6, while MiniMax's unit price is $1.2-2.4, making MiniMax slightly more cost-effective.

Source: Intelligence Analysis

IV. Open-Source Leader MiniMax: Value Following Under the Closed-Source Leader's Demonstration Effect

Not only do high-priced leading models like Claude and OAI take turns dominating the market, but among cost-effective leading models, the turnover rate is even faster. Under such conditions, how will large models ultimately compete in terms of business models and profitability?

A discernible trend is that models are increasingly becoming commoditized. Front-end systems, similar to Agent OS, can automatically schedule corresponding models based on user demand characteristics, weakening the internet's scale effect. Essentially, this is a competition of cost versus performance under a heavy-asset model.

In this process, besides technological leadership in models, cost control and operational efficiency are equally important. However, before the industry reaches its conclusion, the iteration speed of AI and its penetration rate in real-world scenarios are more core valuation drivers.

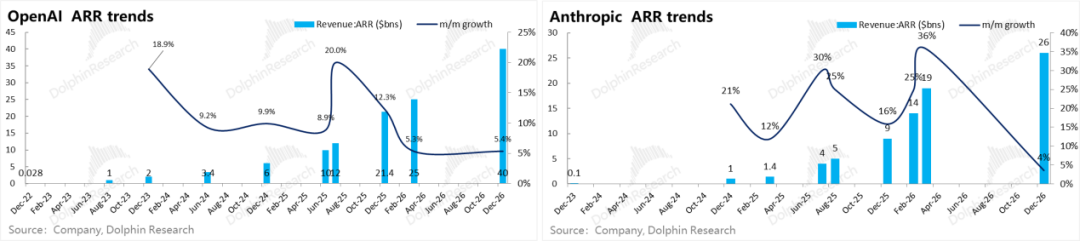

In terms of valuation, model business models are still in their early stages, with token consumption speed highly correlated with technological advancement and implementation. For open-source leading models, one approach is to evaluate revenue growth rates, drawing analogies to leading closed-source models based on the absolute value and growth slope of Annualized Recurring Revenues (ARR).

If we divide the revenue growth of OpenAI and Anthropic into two phases: a. $100 million to $1 billion; b. $1 billion to $10 billion.

We can observe that OAI, as a company more focused on B2C monetization, experienced very rapid month-over-month ARR growth in phase one, reaching 30-40%. However, Anthropic, which emphasizes B2B API services, had a month-over-month growth rate of approximately 20%. From $1 billion to $10 billion, the month-over-month growth rate for both was around 12%. Currently, OpenAI's month-over-month revenue growth rate is approximately 5%.

For the B2B-oriented Anthropic, the growth rate was around 20% in the $100 million to $1 billion phase and remained at 20% from $1 billion to $10 billion. This is primarily because, in the B2B model-as-a-service model, improvements in model capabilities can almost simultaneously accelerate revenue generation.

Currently, the driving force behind MiniMax's revenue growth is gradually shifting from B2C to B2B, with month-over-month revenue growth showing signs of acceleration. In 2025, the growth rate was 8%, and according to the company's statement of achieving an annualized revenue of $150 million in February, if we take the average monthly revenue in Q4 as the November revenue volume, its growth rate had accelerated to 14% by February.

Considering that, in the early stages when the two leading closed-source companies had revenues below $1 billion, absolute revenue could not fully reflect the true value of their assets, leading to PS valuations reaching an ultra-high range of 200-400X at one point. Therefore, Dolphin Research has conducted a more detailed value analysis of the two companies after they surpassed the $1 billion revenue mark... For more detailed value analysis, please refer to the article with the same title in the "Dynamic-Depth" section of the Changqiao App.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is only allowed with proper authorization.

// Disclaimer and General Disclosure

This report is intended for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referring to the content or information in this report are at the investor's own risk. Dolphin Research shall not be held responsible for any direct or indirect liabilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions expressed in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, solicitation, or recommendation regarding securities or related financial instruments. The information, tools, and data contained in this report are not intended for or designed for distribution to jurisdictions where such distribution, publication, provision, or use of the information, tools, and data would contravene applicable laws or regulations or result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or distribute in any form any copies or replicas, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?