The Bottom-end Electric Vehicle Market Collapses: What Should Leapmotor and Chery Do as They Enter the Market?

03/31 2026

03/31 2026

503

503

Lead-in

Introduction

While entry-level EVs were facing a collapse crisis, the soaring fuel prices unexpectedly became their new opportunity.

In the first quarter of 2026, the most severely impacted market segment was undoubtedly entry-level EVs.

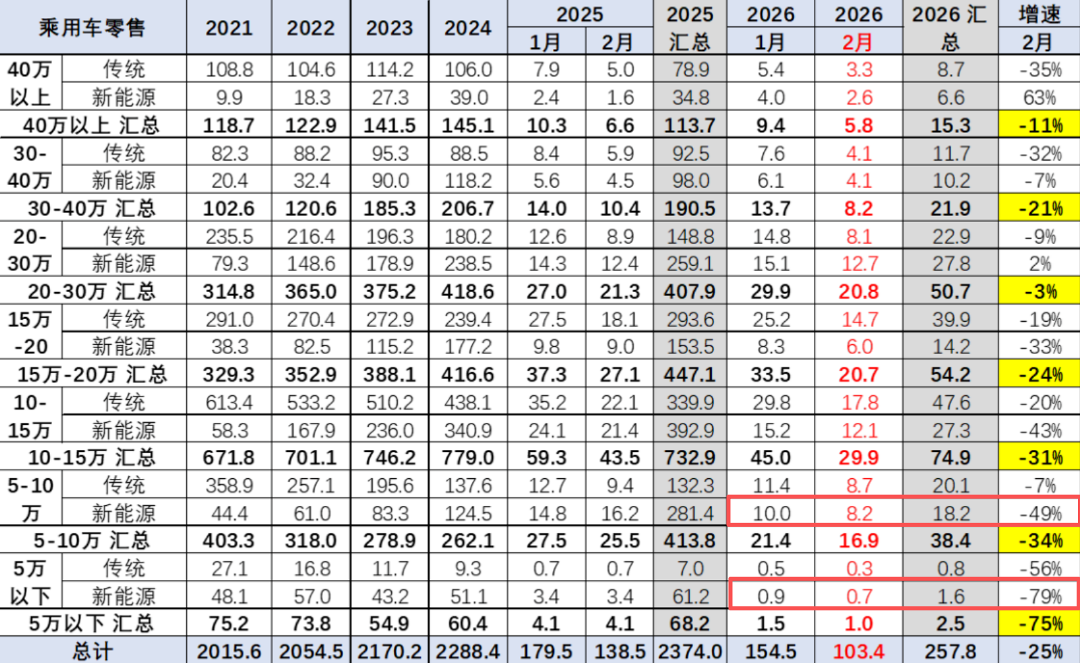

Although March data has not yet been released, cumulative data from January-February 2026 shows that sales of new energy vehicles (NEVs) priced between RMB 50,000-100,000 plummeted by over 49% year-on-year, while those under RMB 50,000 crashed by 79%. The triple pressure of policy phase-out, hybrid competition, and high-base effect depletion instantly eliminated growth opportunities and market dividends in what was once a blue ocean for sales.

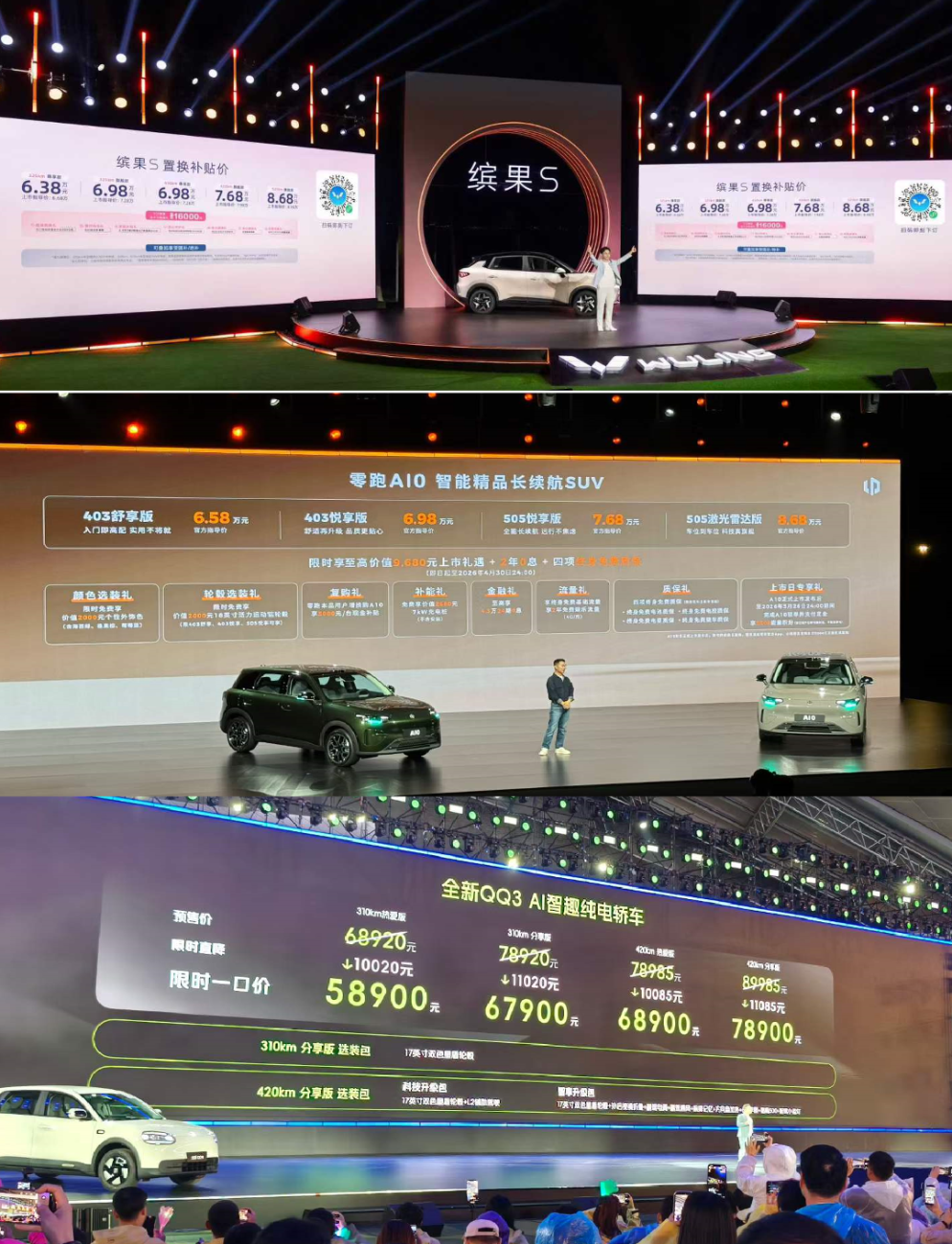

Yet, amid these dismal market figures, one entry-level EV after another was boldly launched. On March 13, Wuling introduced the Binguo S with a pure electric range of 525KM, priced at RMB 86,800. Wuling, adhering to its consistent cost-effectiveness strategy, took the lead in driving competition on price and range.

On March 26, Leapmotor launched the A10, priced between RMB 65,800-86,800, bringing Qualcomm's latest cockpit chip, LiDAR, and advanced intelligent driving to the RMB 80,000 segment, redefining intelligence and value in this market tier.

On March 30, Chery revived the iconic QQ as the pure electric QQ3, with blind orders exceeding 61,000 units during the pre-launch phase. Upon launch, it offered a limited-time price starting at RMB 58,900, stirring the market with extreme cost-effectiveness.

More and more automakers are firm ly entering this segment, attempting to replicate the sales success of BYD Seagull and Geely Galaxy E5. The former achieved 1 million sales in just 27 months, while the latter reached a cumulative 600,000 units in under 18 months, leaving others envious.

On one hand, the segment is rapidly cooling, facing collapse; on the other, Leapmotor, Chery, and others are entering against the trend, compounded by recent sustained fuel price hikes, creating new opportunities and possibilities for entry-level EVs.

However, questions remain: In this fiercely competitive game, can pioneers continue to hold their advantage? Can newcomers replicate blockbuster success? This is not just a survival test for automakers but also a core reflection of China's NEV market transitioning from wild growth to mature rationality.

01 Half of the Market Suffers a Poor Start

Looking back at 2025, entry-level EVs were the undisputed growth engine of China's NEV market and a core anchor for automakers to capture market share and stabilize their foothold.

The explosive potential of this segment was vividly demonstrated by Geely Galaxy E5. In 2025, its annual sales soared to 465,800 units, accounting for nearly 40% of Galaxy's total sales with just one model. It reached 500,000 deliveries in 14 months, becoming a phenomenal national commuter car. Alongside the 435,600 units of Wuling Hongguang MINI EV and 311,000 units of BYD Seagull, these three models propped up half of the entry-level pure EV market, giving their brands a decisive edge in NEV penetration.

Beyond the market leaders, second-tier brands also achieved sales breakthroughs through entry-level EVs. Models like MG4 from MG and T11 from ARCFOX consistently sold over 10,000 units monthly in the second half of 2025, becoming core drivers of brand sales growth. These successes clearly prove that entry-level EVs have become a key lever for automakers to achieve scale and brand popularization.

It's easy to understand that the rise of entry-level EVs precisely met the core needs of Chinese families for travel. For urban commuters, a 300-400km range fully covers daily commuting, with electricity costs of just a few cents per kilometer. Especially for first-time buyers and users in lower-tier markets, the sub-RMB 100,000 price point, compact size, and continuously upgrading configurations make pure EVs a better choice than fuel vehicles.

More notably, the dual support of trade-in subsidies and NEV purchase tax exemptions created vast market space for entry-level EVs. Last year, NEV models under RMB 50,000 could be purchased for RMB 20,000-30,000 after subsidies; even those priced at RMB 70,000-80,000 could be bought for under RMB 50,000 with full subsidies, making them the preferred commuter cars in lower-tier markets.

As a result, the entry-level NEV market (RMB 50,000-100,000) surged from 1.245 million units in 2024 to 2.814 million units in 2025, a 126% increase, directly adding 1.57 million units and becoming the fastest-growing market segment.

But the good times didn't last. In early 2026, trouble arrived for entry-level EVs. Sales of NEVs priced at RMB 50,000-100,000 reached only 182,000 units in the first two months, down 49% year-on-year, while fuel vehicle sales in the same segment were 201,000 units, down 7%. For NEVs under RMB 50,000, sales plummeted by 79% to just 16,000 units. These trends caused NEV penetration to drop by 3-4 percentage points in the first two months.

The core reasons, besides consumption depletion from last year's strong trade-in policies, include the dual withdrawal of NEV purchase subsidies and tax exemptions, coupled with mainstream plug-in hybrid models (PHEVs) now priced fully within the RMB 100,000 segment. Models like BYD Qin PLUS DM-i and Geely Galaxy Star 6, with their "fuel-electric flexibility and no range anxiety," have delivered a dimensionality reduction blow to entry-level pure EVs.

For most families with only one car, the limited 300-400km range of pure EVs makes long-distance travel and charging inconveniences hard to resolve. PHEVs, however, meet urban commuting needs with pure electric mode while relying on fuel for long trips, perfectly fitting all travel scenarios.

Thus, on top of an ultra-high base, the year-on-year decline of entry-level EVs in 2026 became an industry consensus. This depletion effect, compounded by policy phase-outs, created an illusion of collapse-like sales drops. Essentially, this is a normal correction as the industry shifts from high-speed growth to steady development.

However, the author believes that demand in this segment hasn't disappeared. As more automakers invest products and resources here, outdated, low-price, low-quality models will accelerate their exit. Consumers will still choose products with higher cost-effectiveness and lower travel costs, while core demands for technology, reputation, quality, safety, and after-sales will become more important than mere low pricing.

02 Bucking the Trend: Why Dare They Double Down on This Competitive Segment?

Despite the market downturn, Wuling Binguo S Long Range, Leapmotor A10, and Chery QQ3 remain firm in their market entry, not just as a result of prior planning but because these brands genuinely need entry-level EVs as core sales pillars.

For instance, Wuling is a major player in entry-level models, and the Binguo S Long Range helps expand its user base demanding longer range. Leapmotor needs the A10 to support its annual sales target of 1 million units. Chery, aiming to establish itself in the NEV market, sees entry-level EVs as a inevitably choice. Moreover, these products have identified opportunities amid the crisis and found differentiated paths to breakthroughs.

Take the Binguo S, which for the first time brought the price of an entry-level pure EV with over 500km range below RMB 80,000, initiating a new era of long-range competition in this segment. Future entry-level EVs without this capability—or with only ~400km range at similar prices—will be at a disadvantage.

Leapmotor A10 continues its ultra-cost-effective approach, with a breakthrough logic of "entry-level pricing + high-end configuration " through technological dimensionality reduction. Priced from RMB 65,800, the A10 offers dual ranges of 403km and 505km, standard configuration s Qualcomm 8295 chip, and features LiDAR in high-end variants for full-scenario assisted driving, bringing Intelligent Driving configurations from RMB 300,000 models down to the RMB 80,000 segment. This unconventional configuration strategy shatters the stereotype of entry-level EVs as basic vehicles, precisely targeting young users' core demand for intelligence.

Chery's confidence in the QQ3 stems from the iconic IP's appeal and comprehensive product upgrades. As a symbol of national mini-cars, the QQ series has over 1.5 million users. The new QQ3 features Qualcomm 8155 chip, rear-wheel drive, multi-link independent suspension, and a 2700mm wheelbase for ample interior space.

The common strategy of these three new models is to shift from price wars to value wars, where low pricing is just one selling point. They offer superior space, intelligence, and safety, allowing users to enjoy high-quality travel at affordable prices. This marks the transition of entry-level EV competition from low-price volume sales to a value-for-money era.

Despite short-term sales collapses, the fundamental demand for entry-level EVs remains unshaken. Three core pillars ensure this segment won't truly collapse.

First, sustained fuel price hikes amplify the cost advantage of electricity. With No. 95 gasoline exceeding RMB 9 per liter, annual fuel costs for ICE vehicles easily surpass RMB 10,000, while entry-level EVs cost just around RMB 1,000 annually—a 10-fold difference. For budget-constrained families and commuters, this long-term cost gap is an irreplaceable attraction. In other words, the higher fuel prices rise, the more pronounced the advantage of entry-level pure EVs becomes.

Second, while China's NEV penetration has exceeded 50%, demand in lower-tier markets, for elderly commuting, and as family's second cars remains unfulfilled. Entry-level EVs, with their affordable pricing and convenience, are core vehicles for further increasing NEV penetration. As battery technology matures, safety improves, and charging infrastructure expands in lower-tier markets, user acceptance of entry-level pure EVs will continue to rise.

More notably, after 2-3 generations of iteration, entry-level EVs have shed their cheap image, now featuring premium chips, long-range batteries, and comfortable suspensions. These products are no longer basic commuter cars but mainstream models balancing cost-effectiveness and quality.

Policy phase-outs have eliminated low-end production capacity reliant on subsidies, while hybrid competition has forced pure EV upgrades. High-base depletion has returned the industry to steady growth. The entry of Wuling Binguo S, Leapmotor A10, and Chery's new QQ3 proves that the entry-level segment won't vanish but will evolve from "low-price commuter tools" to "high-quality national travel vehicles."

Editor-in-Chief: Cao Jiadong Editor: He Zengrong

THE END

-

![]()

Five Emerging Golden Entrepreneurial Pathways in the Agent Ecosystem: A Deep Dive into the Report (Part 2)

-

![]()

GEM-TIPS Makes Its Debut at Shenzhen International AI Expo: “Octopus AI Brain” + Intelligent Agent Cluster Pave New Ways for Industrial Intelligence

-

![]()

'China's Pioneer Domestic GPU Stock' Moore Threads Posts Profit in Q1, Yet True Profitability Unverified

-

![]()

Hynix Employees Await 3 Million Won in Bonuses, Samsung Employees Go on Strike: A Dramatic Clash Between Korea's Memory Giants

-

![]()

Twelve Years On, Can Cheng Yixiao Steer Kling to Another Victory?

-

![]()

From Data Scarcity to Open Source Boom: How China's Embodied AI Data Industry Can Break Through

-

Trend丨Indium Phosphide (InP) Prices Soar Amid AI Boom, with Cycles and Disruptions Set to Continue

-

![]()

One Article to Decode 'Computing Power Inflation': Why AI Costs Less for You While Computing Power Firms Rake in Profits