Zhipu, Going All-in on AI

04/02 2026

04/02 2026

386

386

Author | Hao Xin

Editor | Wu Xianzhi

The financial reports of Zhipu and MiniMax collectively highlight a key issue: going public for domestic large models is a starting point, not an endpoint.

Zhipu, which once prided itself on benchmarking against OpenAI, took a sharp turn at last night's earnings call, rebranding itself as 'China's Anthropic.'

The reason is simple: an asset report exposed the truth behind Zhipu's IPO. By the end of 2025, Zhipu's net liabilities had soared to RMB 8.11 billion, leaving it insolvent. Without IPO funding, survival itself would be at risk. In this sense, its early-year IPO was indeed a lifeline.

Time waits for no one. Now is Zhipu's moment to prove it can generate profits—and even greater future earnings. 'China's Anthropic' must deliver tangible results.

Another interesting trend is the fading intensity of competition among domestic large models. Introducing new concepts and creating new frameworks, with each claiming dominance within their own ecosystems, has replaced direct head-to-head rivalry.

MiniMax previously proposed formulas like 'AI platform company' and 'Intelligence Density × Token Throughput,' while Zhipu now introduces 'Large Model Operating System' and 'Token Architectural Power.'

Labeling is about drawing a visible, benchmarkable value curve for capital markets. The battle over concepts is, at its core, a struggle for discourse power.

Financial data doesn't lie. It acts as a mirror, reflecting the shared predicament of China's domestic large model industry: when everyone starts at the same line, armed with freshly raised capital, they tread a path never taken before.

The ultimate question remains: how much is your technology truly worth?

Going All-in for Breakthroughs

If Zhipu's current strategy were to be summarized, it might be 'going all-in for breakthroughs.'

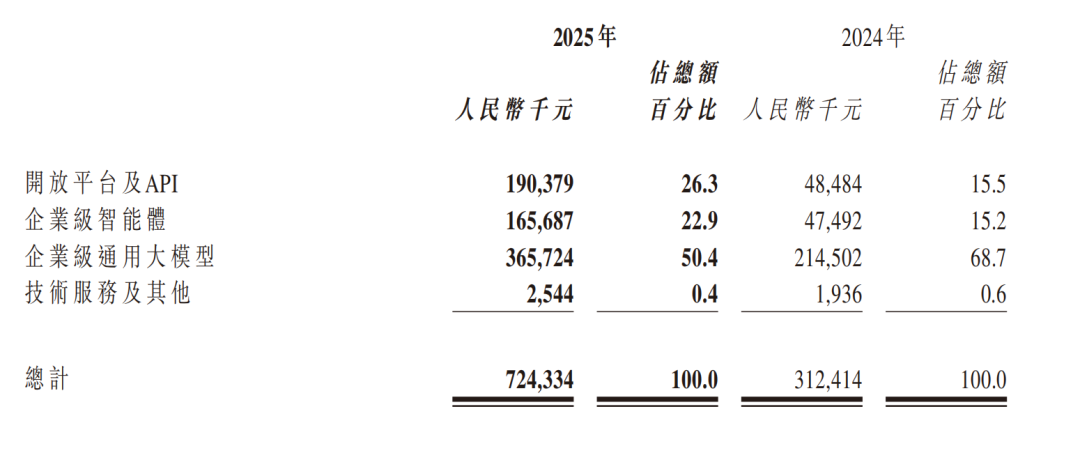

Financial reports show Zhipu's 2025 annual revenue reached RMB 724 million, up 131.9% year-on-year. However, while revenue doubled, annual losses widened to RMB 4.718 billion, a 59.5% increase.

The primary driver is Zhipu's heavy R&D investment. In 2025, R&D spending hit RMB 3.18 billion, up 44.9% year-on-year—4.4 times its revenue.

According to Zhipu's core formula in the financial report—AGI commercial value = Intelligence Ceiling × Token Consumption Scale—going all-in for breakthroughs is inevitable. It means trading R&D investment and losses for leadership in intelligence ceiling and Token scale growth. This also implies that Zhipu will face significant challenges in achieving profitability anytime soon.

Zhipu also serves as a case study for observing how large models and AI are penetrating B2B business landscapes, with new signals emerging from this financial report.

Zhipu's revenue structure underwent dramatic changes over the past year. For the first time, the financial report further segmented its business beyond on-premises and cloud deployments into enterprise-grade general-purpose large models, open platforms & APIs, enterprise-grade agents, and core services & others.

Specifically, the revenue share of high-margin on-premises deployment dropped from 84.5% to 73.7%, while lower-margin cloud-based deployment rose from 15.5% to 26.3%. This contributed to Zhipu's overall gross margin declining from 56.3% to 41% last year.

Zhipu's current margin decline is the inevitable cost of transitioning from a project-based AI company to a platform-based AI infrastructure provider. Some positive signals have emerged, such as AI companies gaining pricing power. The financial report states that by March 2026, platform registered users surpassed 4 million. Even with API pricing increased by 83% since late last year, the market still faces a compute shortage panic.

Agents are evolving from 'technical concepts' to 'commercial realities.' In Zhipu's 2025 financial report, its agent business saw explosive growth, with enterprise agent revenue reaching RMB 166 million, up 248.8% year-on-year. More importantly, its gross margin stood at 52.3%. Combining scalability and high margins, the agent business is becoming Zhipu's third revenue growth curve.

The agent business may become Zhipu's near-term focus. Its profit path is clear: if the business maintains gross margins above 50% and its revenue share rises to 30-40%, it could offset the drag of low-margin cloud services and shorten the timeline to break-even.

Additionally, agents not only consume model capabilities but also accumulate user scenarios and data. The more agents run on Zhipu's platform, the stronger its ecosystem lock-in becomes. Developers building agents on Zhipu will face higher switching costs in the future.

China's Anthropic?

Early on, Zhipu positioned itself as a follower of OpenAI, frequently referencing the title 'China's OpenAI' in public interviews. Even its funding pitch decks emphasized technical alignment with OpenAI's roadmap. At the time, Zhipu leveraged OpenAI-style narratives to attract capital and craft valuation stories.

Zhipu CEO Zhang Peng once half-joked, 'If Anthropic's Claude sells for $200, we'll sell for RMB 200.'

In Zhang's view, why could Zhipu benchmark against Anthropic?

This shift didn't happen in a vacuum. At least within its 2025 financial report, Zhipu validated three critical logics: its API business is scaling, with ARR proving scale effects; its pricing power logic holds, as customers are willing to pay for intelligence ceiling; and its Token ecosystem flywheel is spinning, making Zhipu one of China's top vendors for high-volume paid Token consumption.

This means Zhipu no longer relies on securing large, customized deals to survive. Instead, it can follow Anthropic's proven overseas path, establishing a business model where model capability → API calls → revenue growth → R&D reinvestment.

That's why Zhang announced at the earnings call, 'When the model is strong enough, API itself is the best business model. In 2026, Zhipu will develop along the commercial path of China's Anthropic.'

Anthropic's narrative is highly alluring—a proven high-growth trajectory. Anthropic's ARR surged from ~$1 billion at the end of 2024 to ~$9 billion by late 2025, nearing $19 billion by March 2026. Claude Code alone generates over $2.5 billion in ARR, with ~70-80% of revenue from enterprise API calls.

For Zhipu, ARR reached ~$250 million by late 2025, with API ARR growing 60x. It had 242,000 paid developers on its Coding Plan, with enterprise API revenue accounting for 26.3%.

Zhipu aims to convince the outside world that maintaining its current growth rate could replicate Anthropic's success, even achieving profitability by 2027.

This script is inspiring but difficult to replicate one-to-one.

Anthropic and Zhipu operate in fundamentally different ecosystems. Anthropic's $19 billion ARR is built on U.S. enterprises' annual software budgets, which amount to hundreds of billions of dollars.

In contrast, Chinese enterprises have smaller total IT budgets with rigid structures and lack a habit of paying continuously for software. Even if Zhipu becomes China's B2B AI market leader, its ceiling remains far lower than Anthropic's.

Anthropic can halt cash burn by 2027 because its revenue growth far outpaces loss growth. For Zhipu to achieve this, its revenue growth must not slow down. To match Anthropic's scale effects, Zhipu needs to maintain annual growth above 150% for the next three years.

This is challenging amid intensifying competition and rising compute costs. Moreover, Zhipu continues to pursue a 'go all-in for breakthroughs' strategy, meaning R&D intensity won't decline.

Relationship with major players poses potential risks. These firms use Zhipu's GLM not just for capability complementarity but also as a price anchor to suppress independent model vendors' pricing power.

For example, a vendor selling both its proprietary large model and GLM API might promote its in-house model if GLM is priced too high, or use GLM to pressure its R&D team to improve capabilities if priced too low. In partnerships with major players, Zhipu is effectively 'priced' by them, with ceilings set by these giants despite its current pricing power.

Zhang Peng did not address how Zhipu will counter major players' long-term strategy of being 'both customers and competitors.'

For now, Zhipu's answer is to maintain a technological edge. As long as GLM stays ahead, major players must keep procuring it. But this is a technological arms race—can Zhipu's R&D intensity withstand attacks from major players?

In short, Anthropic's new narrative clarifies what Zhipu is doing. But the market needs time to believe what Zhipu can achieve in China's ecosystem.

Two Formulas, Two Futures

The formulas proposed by Zhipu ('Intelligence Ceiling × Token Consumption Scale') and MiniMax ('Intelligence Density × Token Throughput') in their 2025 financial reports are not just strategic summaries but declarations of two distinct future paths for China's AI large model industry.

Zhipu defines intelligence as the absolute ceiling of model capability—its ability to solve the hardest problems. It defines scale as the total volume of model calls by users. MiniMax, however, defines intelligence as efficient problem-solving and scale as the total volume of Tokens processed by the system.

These differing initial definitions lead to clear divergences in focus. Zhipu pursues technological superiority to dominate high-end markets, while MiniMax seeks ultimate efficiency to capture mass-market scale.

Reflected in their financial reports, the two companies exhibit starkly different characteristics. Zhipu has high average selling prices (ASPs), fewer but highly sticky customers, and a ceiling limited by B2B market capacity. MiniMax has relatively lower ASPs, more customers with weaker stickiness, but a ceiling dependent on C-side monetization efficiency.

Through their financial reports and earnings calls, we also see differing ultimate visions for AI between Zhipu and MiniMax.

In Zhipu's vision, intelligence is 'productivity'—whoever controls the highest intelligence controls the economic lifeblood. Its proposed 'Large Model Operating System' implies that all future applications will run on an 'intelligence core' provided by a few vendors. Just as all PC applications today run on Windows/MacOS, all future agents and AI applications will depend on one or several intelligent operating systems.

In this endgame, pricing power is core. If multiple substitutable intelligence cores exist, the 'operating system's' value collapses. Thus, Zhipu must maintain technological superiority at all costs to ensure it remains irreplaceable.

MiniMax views AI as a connectivity tool. Like the internet or mobile internet, whoever connects the most users and provides the most convenient services gains the strongest network effects. In this worldview, intelligence is a ubiquitous resource, and technological barriers will rapidly lower, leading to a future where multiple players coexist, each dominating its niche.

In MiniMax's vision, scale is core. More users, data, and scenarios accelerate model iteration and reduce costs, creating a virtuous cycle. Thus, MiniMax must expand user scale at all costs, even accepting short-term losses to secure 'entry points.'

The differing endgames of Zhipu and MiniMax essentially answer the same question differently: what is the true moat in the AI era?

Zhipu's answer is technological capability; MiniMax's is scale effects.

Faced with the shared challenge of commercialization, both are still on their journeys.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?