Intel: Bidding Adieu to Its 'Darkest' Chapter, the Former Titan Launches a 'Counterattack'

04/24 2026

04/24 2026

626

626

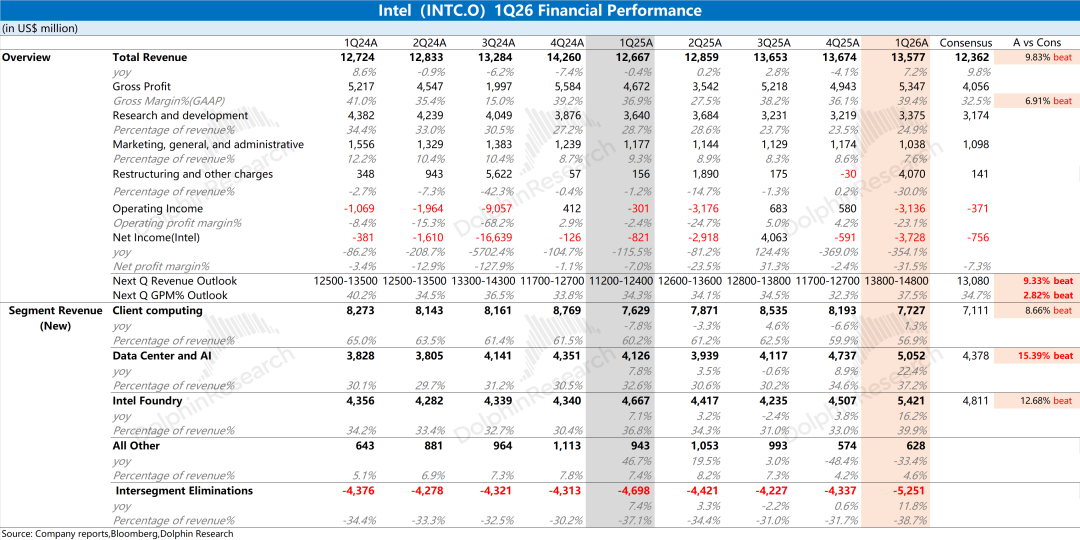

On the morning of April 24, 2026, Beijing time, following the closure of the U.S. stock market, Intel unveiled its financial report for the first quarter of 2026 (ending in March 2026). Here are the highlights:

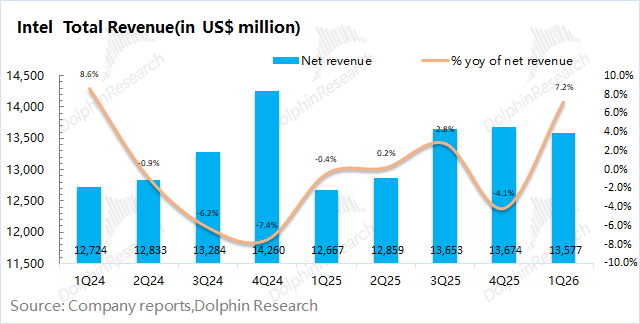

1. Core Data: The company reported revenue of $13.6 billion for the quarter, marking a 7% year-on-year increase and significantly surpassing its own guidance ($11.7-12.7 billion). This growth was primarily fueled by heightened demand for server CPUs and price increases for its products.

The gross margin for the quarter reached 39.4%, far exceeding market expectations of 32.5%. This sequential improvement was largely attributed to price hikes for server CPUs (ranging from 10-15%) and enhancements in process technology yields.

2. Progress in Layoffs and Cost Management: Intel's core operating expenses (comprising R&D and sales and administrative expenses) amounted to $4.4 billion this quarter, with the core operating expense ratio dropping to 32.5%.

The company maintained its momentum in layoffs and cost-cutting measures, reducing its total workforce to 83,200, a decrease of 1,900 from the previous quarter. Intel had previously set a target to reduce its workforce to 75,000 by the end of 2025 and may consider further job cuts thereafter.

3. Business Performance: After adjusting its business disclosure scope, Intel's primary revenue streams continue to be client business and data center and AI, which together account for over 90% of total revenue.

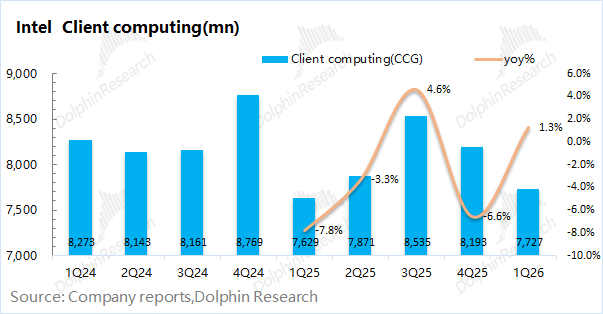

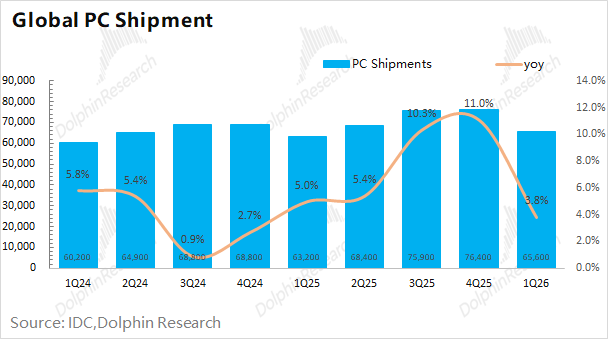

a) Client Business: Revenue in this segment reached $7.7 billion, up 1.3% year-on-year. Despite the launch of the company's Panther Lake, and considering a 4% year-on-year increase in global PC shipments this quarter, Intel still experienced a market share decline in the PC market.

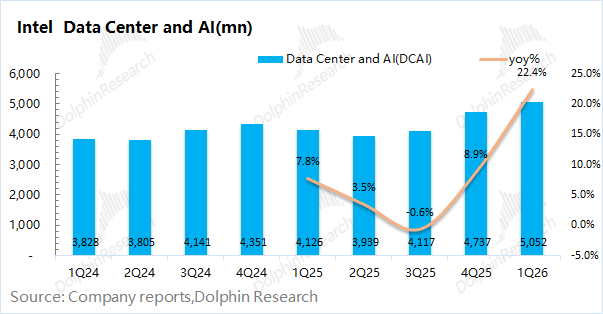

b) Data Center and AI: Revenue in this segment soared to $5.05 billion, a 22% year-on-year increase. This business remains centered around data center CPUs, with growth driven by demand for Intel's Xeon CPUs and price increases (estimated at 10-15%). Following collaboration with NVIDIA, Intel recently announced deeper cooperation with Google, establishing partnerships with two major players in the AI chip market for its Xeon CPUs.

Against the backdrop of large models shifting focus from training to inference, market attention is increasingly turning to 'latency.' CPUs naturally handle tasks such as data preprocessing and resource scheduling, further enhancing inference efficiency while reducing latency.

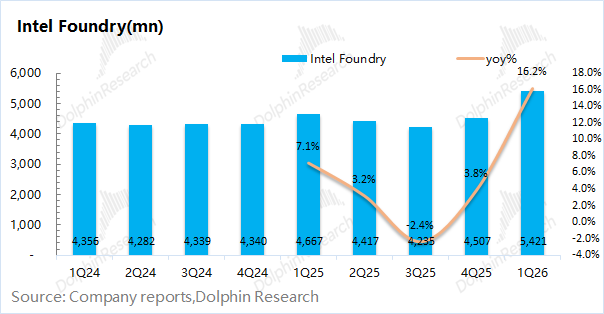

c) Intel Foundry Business: Revenue in this segment amounted to $5.42 billion, up 16% year-on-year. Although Intel's 18A process has entered mass production, foundry revenue this quarter was primarily derived from Intel 7. External foundry revenue was around $170 million, mainly serving Intel's internal products.

The company's latest 18A process is primarily used for its own Panther Lake products. Although the 18A process still lags behind TSMC in transistor density, as long as Intel can improve yields, it still has the potential to become a 'backup option' for downstream customers.

Currently, Intel's foundry business primarily serves its own products and urgently requires endorsement from a 'major customer.' The recently announced 'Terafab' project in collaboration with Elon Musk is expected to serve as a blueprint for Intel's future external foundry business.

4. Next Quarter Guidance: Intel anticipates revenue of $13.8-14.8 billion for the second quarter of 2026, surpassing market expectations of $13.1 billion. The gross margin for the second quarter of 2026 is expected to be 37.5%, outperforming market expectations of 34.7%.

Dolphin Research's Comprehensive View: Price Hikes for Profit, Foundry Bets on the Future, and the 'Painful' Transition Nears Its End

Intel's performance this quarter comprehensively exceeded market expectations, with revenue returning to positive year-on-year growth and a significant recovery in gross margin. Revenue growth was primarily driven by demand for server CPUs and related product price hikes, while the improvement in gross margin was mainly attributed to product price increases and yield enhancements in Intel 3 and 18A processes.

Currently, the majority of Intel's wafer capacity is allocated to its own products. External foundry revenue this quarter was approximately $170 million, accounting for 3% of the company's total foundry manufacturing department revenue.

Compared to this quarter's performance, Intel's guidance for the next quarter was even more 'astonishing.' The company expects revenue of $13.8-14.8 billion next quarter, marking a 7%-15% year-on-year increase, primarily driven by volume and price increases in server CPUs.

Intel anticipates a gross margin (GAAP) of around 37.5% for the next quarter, a sequential decline due to the initial stage of 18A mass production and the absence of first-quarter inventory gains in the second quarter. However, this guidance still significantly outperformed market expectations of 34.7%. As one of the company's key indicators, the substantial recovery in gross margin reflects that Intel's product price hikes and yield performance in processes like 18A exceeded market expectations.

The recent surge in Intel's stock price was primarily driven by a series of positive developments, including the announcement of repurchasing equity in its Irish factory, as well as deeper cooperation with customers like Elon Musk and Google, injecting renewed confidence into the market.

For Intel, the market primarily focuses on the following aspects:

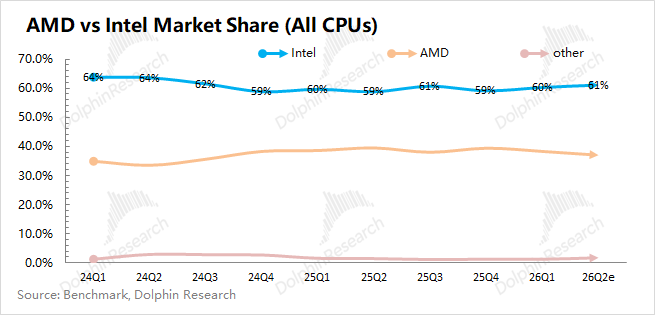

a) CPU Market Share: The Bedrock of Intel's Current Performance

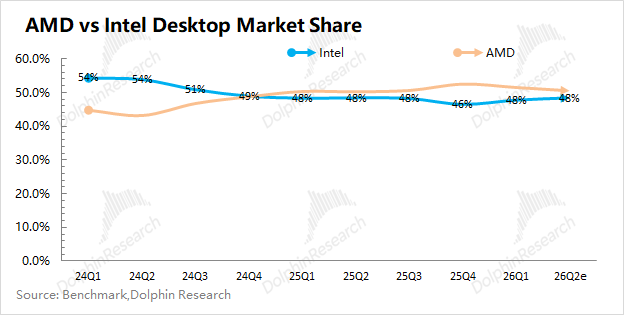

Intel still maintains a leading overall market share in CPUs but continues to face competition from AMD, particularly as AMD has surpassed Intel in the desktop CPU market.

In the server CPU market, which is closely watched by the market, Intel's shipments have been squeezed to below 80% by AMD. The growth in Intel's data center and AI business this quarter was primarily driven by increased overall demand for server CPUs and product price hikes (ranging from 10-15%).

b) Repurchase of Equity in the Irish Factory (Fab 34)

To raise funds during its transition, Intel previously sold a 49% stake in its Irish Fab 34 factory to asset management giant Apollo. On April 1, 2026, Intel announced it would spend approximately $14.2 billion to repurchase this stake, regaining 100% control of the factory.

Fab 34 is Intel's sole manufacturing base in Europe utilizing EUV technology, currently primarily producing chips on the Intel 3 node for Core Ultra PC processors (Meteor Lake) and Xeon 6 series server CPUs (Granite Rapids). This repurchase underscores Intel's optimism about the current upcycle in CPUs and its reluctance to share half of the factory's profits.

Intel has shifted from a 'defensive mode' to an 'offensive mode,' demonstrating confidence in its own operating cash flow and no longer needing to 'sell assets' to sustain operations.

c) Deepened Strategic Cooperation: Elon Musk and Google

① Collaboration with Elon Musk: Intel, in partnership with Elon Musk's Tesla, SpaceX, and xAI, launched a project called 'Terafab.' The plan is to construct a mega-fab in Austin, Texas, dedicated to designing and manufacturing ultra-high-performance chips for Musk's robots, Dojo supercomputers, and autonomous driving systems.

Although specific collaboration details have not been disclosed, this opportunity brings much-needed endorsement from a 'major customer' for Intel's foundry services and allows it to participate in the competition for advanced process external foundry services.

Tesla revealed in its earnings call yesterday that it 'will make an upfront investment of $3 billion in the near future, with Terafab expected to adopt Intel's 14A process.' According to Intel's previous plans, 14A mass production is expected around 2028. This incremental information adds relative certainty to the collaboration, and Intel's stock price rose +3% after the market closed yesterday.

② Collaboration with Google: Intel and Google announced a multi-year collaboration aimed at advancing next-generation AI and cloud infrastructure, with the core being the deployment of multiple generations of Intel Xeon processors in Google's global infrastructure and the joint development of custom ASIC architecture infrastructure processing units (IPUs).

Although Google is still developing its own Axion CPU (ARM architecture), x86 remains the 'king' in the enterprise market. With the vast majority of enterprise customers' existing business running on x86 architecture, Google's collaboration with Intel on Xeon processors is also aimed at acquiring more external customers. (This is similar to the previous collaboration between NVIDIA and Intel to provide x86 solutions.)

Compared to CPU procurement, the market places greater importance on the joint development of IPUs by Google and Intel. IPUs (similar to NVIDIA's DPUs) are specifically designed for networking, storage, and security tasks. This frees CPUs from 'grunt work' at the bottom level, allowing them to focus on high-value logical tasks like agent orchestration and reducing overall CPU pressure.

Regarding the TPU Direct Storage technology mentioned in Google's recently released TPUv8, which writes data directly from Google's managed storage layer to HBM, bypassing traditional CPU intermediaries, this does not diminish CPU functionality but rather allows CPUs to focus more on complex logic, tool invocation, and feedback loops for AI models.

Considering Intel's current market capitalization ($335.3 billion), it corresponds to approximately 33 times PE for core operating profit after tax in 2027 (assuming a compound revenue growth rate of 11%, a gross margin of 46.5%, and a tax rate of 10%). Intel's relatively high PE (TSMC is around 24x PE) includes market expectations for the recovery of its CPU business and its external foundry business.

Overall, Intel's performance this quarter was commendable. Especially the strong recovery in gross margin indicates that the impact of server CPU price hikes and yield improvements was better than expected. Given that storage price increases squeezing the PC market are inevitable, the company's current performance primarily hinges on the performance of server CPUs, foundry business, and gross margin.

Intel's deeper collaboration with NVIDIA and Google indicates that x86 will remain a viable option for downstream customers, laying the groundwork for the growth of its server CPU business. On the other hand, the 'Terafab' project in collaboration with Elon Musk brings expectations for the company's subsequent 'external foundry' business.

The recent surge in Intel's stock price was primarily driven by positive events (repurchases, Google, and Elon Musk). The company provided even more 'surprises' in this financial report, showcasing the 'robust' performance of its server CPU business.

After Intel established deep cooperation with NVIDIA and Google, the next focus is primarily on the progress of its external foundry business. Currently, the company's 18A process is in the mass production ramp-up stage, with attention on manufacturing process yields and the company's gross margin performance.

With TSMC's capacity 'tight,' as long as Intel's foundry business performs well, it can become a 'backup option' for chip manufacturers. This allows the company to secure 'overflow orders' from TSMC while also bringing more growth opportunities.

Below is a detailed analysis:

I. Core Data: Revenue & Gross Margin, Far Exceeding Expectations

1.1 Revenue: Intel achieved revenue of $13.6 billion in the first quarter of 2026, up 7% year-on-year, significantly surpassing the guidance range ($11.7-12.7 billion), primarily driven by increased demand for server CPUs and product price hikes.

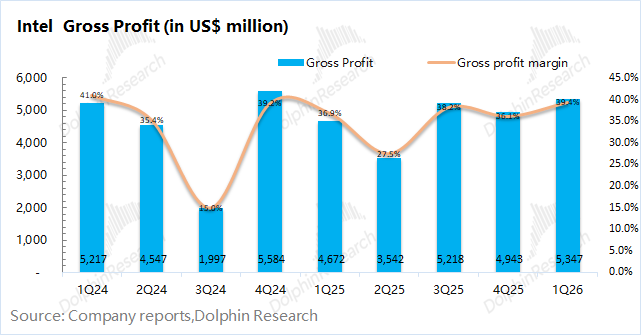

1.2 Gross Profit and Gross Margin: Intel achieved a gross profit of $5.35 billion in the first quarter of 2026, up 14% sequentially. The gross margin for this quarter was 39.4%, up 3.3 pct sequentially, significantly exceeding market expectations of 32.5%. The improvement in gross margin was mainly driven by server CPU price hikes and yield enhancements.

Intel anticipates a gross margin (GAAP) of 37.5% for the next quarter, better than market expectations of 34.7%. The sequential decline in gross margin next quarter is mainly due to the absence of first-quarter inventory gains in the second quarter and the initial stage of 18A mass production. Dolphin Research believes that the impact of server CPU price hikes this time was better than the market's original expectations. Driven by server CPU price hikes and 18A mass production ramp-up, the company's gross margin is expected to rise again subsequently.

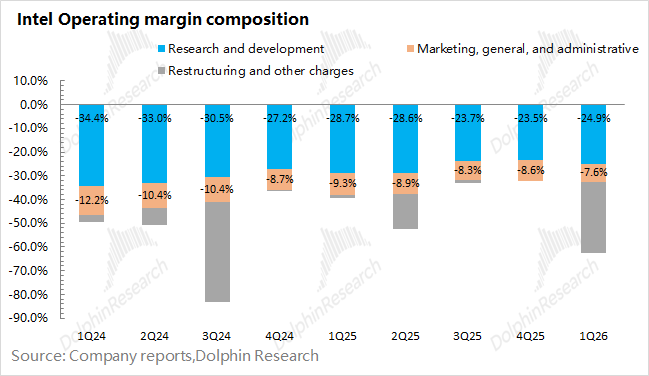

1.3 Operating Expenses: Intel's core operating expenses were $4.4 billion in the first quarter of 2026, down 8% year-on-year. After the company's new CEO set a goal of 'cutting costs,' operating expenses have also become a focal point.

Specifically: ① R&D expenses: $3.38 billion, down 7% year-on-year; ② Sales and administrative expenses: $1.04 billion, down 12% year-on-year.

The company continued its pace of layoffs and cost reductions this quarter, with the total number of employees shrinking again to 83,200, a decrease of 1,900 sequentially. The company previously aimed to reduce the workforce to 75,000 by the end of 2025 and may consider further job cuts thereafter.

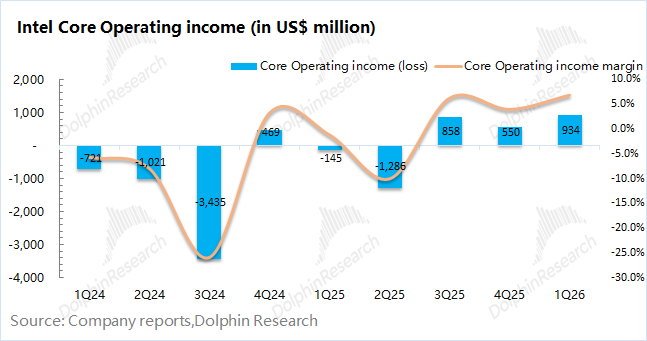

1.4 Net Profit: Intel reported a net loss of $3.73 billion in the first quarter of 2026. From an operating perspective, the company's core operating profit for this quarter was approximately $930 million, better reflecting the company's true operating conditions. The sequential improvement in core profit this quarter was mainly driven by server CPU price hikes and the overall recovery in the company's gross margin.

Note: Core Operating Profit = Gross Profit - R&D Expenses - Sales and Administrative Expenses

2. Segment Data Performance: AI Growth Reaccelerates, Foundry Breakthrough Emerges as Key

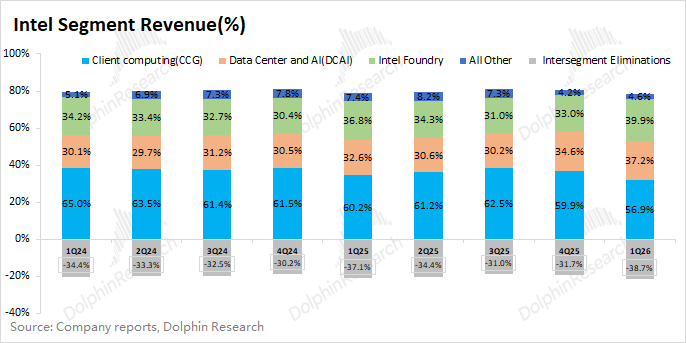

Following a change in CEO, Intel has once again revised its approach to disclosing business segments. The company now divides its owned product business into two main segments: Client Business and Data Center & AI, with the remaining operations, including wafer foundry and all other businesses, grouped separately. The Network and Edge Business is no longer reported as a standalone segment, while entities such as Altera, Mobileye, and IMS are uniformly categorized under All Other Businesses. After the divestiture of Altera and Mobileye, other businesses mainly encompass IMS operations, startup projects, and additional operations.

Post-business restructuring, it is evident that Client Business and Data Center Business constitute Intel's primary revenue streams. Considering internal offsets and wafer foundry operations, Intel predominantly operates on a self-production and self-sales model, with external foundry services contributing minimal revenue (currently less than 3%).

2.1 Client Business

Intel's client revenue reached $7.7 billion in the first quarter of 2026, marking a 1.3% year-over-year increase. While the client business has shown signs of recovery, its performance still lags behind the overall PC market.

Note: The company restructured its business segments in the first quarter of 2025, integrating a portion of the original Network and Edge revenue into Client Business.

According to IDC industry data, global PC shipments totaled 65.6 million units in this quarter, up 3.8% year-over-year. Despite this growth, factors such as rising memory prices and reduced government subsidies have kept the industry relatively sluggish. In comparison, Intel's client revenue grew by only 1.3% year-over-year, indicating a continued loss of market share in the PC segment. Notably, AMD has surpassed Intel in the desktop CPU market.

Intel previously announced a collaboration with NVIDIA in the PC space, aiming to launch SoC products for the AI PC market by integrating NVIDIA's GPUs. This move is intended to counter AMD's competitive impact in the PC market.

2.2 Data Center & AI

Intel's Data Center & AI revenue reached $5.05 billion in the first quarter of 2026, representing a 22% year-over-year surge. This accelerated growth is primarily driven by demand for AI server CPUs and related products.

Previously, the company's Data Center & AI revenue hovered around $4 billion. As model development transitioned from training to inference, Intel's AI business (centered on server CPUs) has demonstrated noticeable improvement.

Historically, AI training emphasized "computing power," with the CPU playing a relatively minor role. However, as the focus shifts to AI inference, the market places greater importance on "latency." The CPU now handles resource scheduling, data preprocessing, and other tasks, directly influencing throughput, latency, and efficiency during the inference phase.

Since Intel has yet to achieve a breakthrough in GPUs, its Data Center & AI business remains heavily reliant on CPU products. As AI training gives way to AI inference, increased demand for server CPUs has driven price hikes for related products (10-15%), a trend expected to continue fueling growth in Intel's AI business.

Following its collaboration with NVIDIA, Intel recently deepened its partnership with Google, agreeing to supply server CPUs to two major leaders in the AI chip market. Although both companies are developing their own CPUs, their decision to strengthen ties with Intel underscores the enduring demand for x86 architecture in the downstream end-user market, creating additional growth opportunities for Intel's server CPU business.

In addition to server CPUs, Google will collaborate with Intel on the joint development of IPUs. The IPU (akin to NVIDIA's DPU) is specifically designed for networking, storage, and security tasks, freeing the CPU from low-level operations and enabling it to focus on high-value logic such as Agent orchestration, thereby reducing overall CPU strain.

Regarding Google's recently announced TPU Direct Storage technology in the TPUv8, which enables direct data transfer from Google's managed storage layer to HBM, bypassing traditional CPU intermediaries, some market observers have argued that this "diminishes the CPU's role." However, Dolphin Research believes this allows the CPU to concentrate on complex logic, tool invocation, and feedback loops for AI models, ultimately achieving greater efficiency.

2.3 Intel's Foundry Business

Intel's wafer foundry revenue reached $5.42 billion in the first quarter of 2026, up 16% year-over-year.

Given that internal offsets across business segments totaled $5.25 billion this quarter, with external foundry revenue amounting to approximately $170 million (around 3% of the total), Intel's wafer foundry operations remain primarily internal, with minimal revenue from external foundry services.

Intel's CEO has previously stated that developing the foundry business is a top priority, positioning it as a critical opportunity for the company to "regain its footing." Intel's U.S.-based manufacturing capacity is a core strength and a key reason the U.S. government has sought to collaborate with SoftBank and NVIDIA to "support" the company.

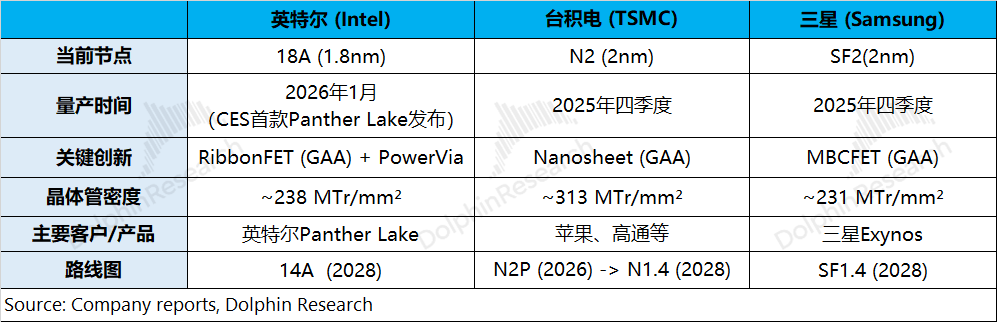

This quarter, foundry revenue remained concentrated in the Intel 7 segment, with the 18A process entering mass production in the second half of 2025 and currently used in Intel's own product, Panther Lake. While Intel's 18A products still trail TSMC in transistor density, the release of Panther Lake signals the company's renewed competitiveness in the cutting-edge process race.

Historically, Intel's foundry business struggled to secure external "major clients" and was primarily used for in-house product manufacturing. However, Intel recently launched a project called "Terafab" in collaboration with Elon Musk's Tesla, SpaceX, and xAI, reigniting market speculation about the company's potential for external foundry services.

According to Tesla's disclosure, "Terafab" is expected to adopt Intel's 14A process. Based on the company's previous plans, mass production of 14A is estimated to begin around 2028.

If mass production proceeds smoothly, Intel could not only secure endorsement from a "major client" but also attract orders from additional customers. Currently, advanced process "orders" are predominantly concentrated with TSMC. As long as Intel can offer a competitive product, it could become a "backup option" for downstream chip manufacturers, unlocking greater growth opportunities.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is only permitted with authorization.

// Disclaimer and General Disclosure

This report is intended for general informational purposes and is provided for the reference of users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, preferences, risk tolerance, financial situation, or unique needs of any individual recipient. Investors must consult independent professional advisors before making investment decisions based on this report. Any person using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be held liable for any direct or indirect responsibilities or losses arising from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are provided for reference only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for or proposed for distribution to jurisdictions where such distribution, publication, provision, or use would conflict with applicable laws or regulations or result in Dolphin Research and/or its subsidiaries or affiliated companies being required to comply with any registration or licensing requirements in such jurisdictions, nor are they intended for citizens or residents of such jurisdictions.

This report reflects the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and all copyrights are owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any way, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Wang Huiwen, Former Meituan Executive, Achieves 20-Fold ROI, Supports 24 AI Startups

-

![]()

Another AI Computing Power Unicorn Launches IPO! Founded by a Changjiang Scholar

-

![]()

OFILM Holdings Secures Zhongke Daojing, Marking a Significant Leap in the Optical Communication Industry!

-

What Will Be the Next Key Battleground for Large Models After AI Coding?

-

![]()

Leapmotor's Sales Soar, Yet Hidden Concerns Loom

-

![]()

China’s Action Camera Market Soars: 3.12 Million Units Sold in Six Months, DJI Secures 74% Dominance

-

![]()

Zhang Yiming: Strategic Retreat as a Path Forward

-

![]()

Exploring Charging for Some Features of QianWen App: Can It Follow the Path of Doubao?