Huawei's Rise and RoboSense's Decline: LiDAR Sector Enters Duopoly Era

04/24 2026

04/24 2026

432

432

Is Selling LiDAR Finally Profitable?

In late March, major LiDAR players Hesai Technology, RoboSense, and Innovusion released their 2025 financial results. Financial data from the three companies suggests the industry is "turning a corner"—after years of investment and losses, profitability finally appears within reach.

Of course, it's just a glimmer for now, far from time to celebrate. First, the "methods" of achieving profitability or reducing losses vary, with stable profits from core operations still some way off. Second, the industry remains fiercely competitive, with unit prices still falling, making easy money elusive. Third, while some giants have turned profitable and others narrowed losses, the trend toward profitability is undeniable.

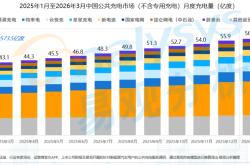

In just a few years, Chinese LiDAR manufacturers have overturned European giants to dominate the market absolutely. By 2025, Huawei, Hesai, RoboSense, and Innovusion nearly monopolized the domestic market, with Huawei and Hesai leading by a wide margin; market space for "other" players continues to shrink.

This January, industry rankings shifted again, with RoboSense dropping from third to fourth place, continuing its decline.

RoboSense's market share decline is traceable. In ADAS, Huawei primarily deploys on its own vehicles; Hesai is strongly tied to leaders like Li Auto and Xiaomi; Innovusion relies mainly on NIO; RoboSense's key customer XPeng is shifting to pure vision, while another major client BYD began mass-purchasing Hesai and Huawei LiDAR in 2025, with rumors of BYD gradually adopting in-house LiDAR. Thus, RoboSense's automotive prospects look bleakest.

Currently, Huawei's powerful ecosystem enables rapid rise, capturing 41.5% market share in 2025 (including blind-spot LiDAR), becoming industry leader; early frontrunners RoboSense and Innovusion see shrinking shares, widening the gap with the top two.

The "duopoly" trend in automotive LiDAR intensifies, prompting firms to pivot toward robotics for new breakthroughs.

Profitability Achieved, But "By Any Means Necessary"

At first glance, two of the three listed LiDAR leaders achieved interim profitability.

In 2025, Hesai reported revenue of RMB 3.028 billion (+45.8% YoY) and net profit of RMB 436 million, turning from loss. Hesai became the first in the industry to achieve full-year GAAP profitability, with three consecutive quarters of GAAP profits.

Of Hesai's annual net profit, RMB 170 million came from operating profit (less than 40%), with the rest from interest and investment gains.

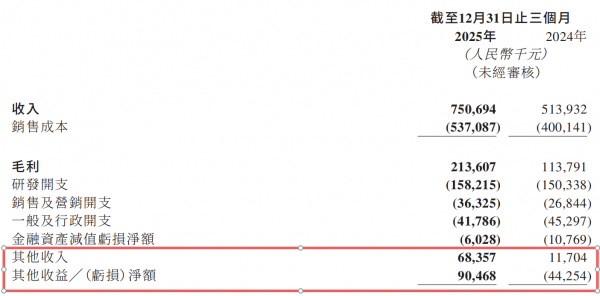

RoboSense also achieved "interim profitability." Its announcement showed Q4 2025 revenue of RMB 751 million (+46.1% YoY), with quarterly operating profit of RMB 130 million and net profit of RMB 104 million, marking its first single-quarter profit.

Compared to Hesai, RoboSense's profitability is less substantial. First, it remains unprofitable annually; second, excluding government subsidies, customer compensation, and fair value changes in financial assets, its Q4 operating profit remains negative.

In Q4 2025, RoboSense reported other income of RMB 68 million and other net gains of RMB 90 million, totaling RMB 158 million, exceeding its quarterly operating profit of RMB 130 million.

These two "non-operating" income streams mainly came from one-time customer compensation and investment gains, carrying high uncertainty.

Customer compensation, while providing short-term "relief," often means long-term client loss and reduced future revenue.

Investment gains, per RoboSense's disclosure, mainly came from valuation increases due to portfolio company financings. Primary market uncertainties, high exit barriers, and long cycles make this unsustainable.

Thus, despite two of the "Big Three" declaring profitability, it's premature to say the LiDAR industry is profitable.

Huawei's Rise, RoboSense's Decline

Overall, the market is still expanding rapidly.

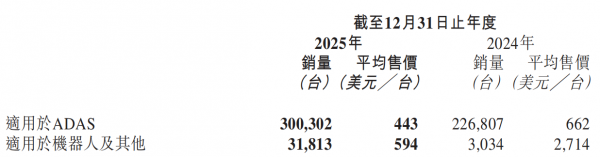

In 2025, Hesai, RoboSense, and Innovusion shipped 1.62 million, 912,000, and 333,000 LiDAR units (+222.9%, +67.6%, +44.6% YoY), respectively; ADAS LiDAR shipments were 1.381 million, 609,000, and 300,000 units (+202.6%, +17.2%, +32.4% YoY).

Huawei's growth cannot be ignored. According to Gasgoo Auto Research Institute, including blind-spot LiDAR, Huawei's 2025 installations reached 1.4063 million units (+234.4% YoY). Only Hesai's growth rate is comparable.

Thus, a clear trend emerges in LiDAR: companies with larger shipment volumes grow faster, driving industry consolidation.

In 2024, RoboSense led with 33.5% market share, followed by Huawei (27.4%), Hesai (25.6%), and Innovusion (13.4%). By 2025, rankings flipped: Huawei led with 41.5%, Hesai rose to second with 33.8%, RoboSense fell to third with 17%, and Innovusion held just 7.7%.

In one year, RoboSense's market share collapsed, leaving it in a different tier from Huawei and Hesai. More alarmingly, this January, RoboSense's share further declined to 10.1%, surpassed by Innovusion.

From industry leader in 2024 to fourth place this January, RoboSense's decline, if continued, could leave LiDAR dominated by Huawei and Hesai in Tier 1, with Innovusion and RoboSense in Tier 2, forming a duopoly.

Price Wars Now Cost Wars

Despite robust 2025 market growth, with LiDAR giants seeing double-digit shipment increases, revenue growth lags far behind, indicating persistent industry "involution."

Hesai's 2025 ADAS LiDAR shipments grew over 200%, but product revenue rose just 53%; media estimates show its unit price fell from RMB 3,900 in 2024 to around RMB 1,800 in 2025.

RoboSense's ADAS revenue fell over RMB 200 million in 2025 despite a 17.2% shipment increase; its average ADAS LiDAR price dropped from RMB 2,600 in 2024 to around RMB 1,800 in 2025.

Similarly, Innovusion's ADAS LiDAR grew 32.4% but revenue fell ~USD 17 million; its average price dropped from USD 662 in 2024 to USD 443 in 2025 (~RMB 4,500 to ~RMB 3,000 at current rates).

With prices falling, LiDAR firms have two ways to protect profits or reduce losses: 1) product mix adjustment, increasing sales of higher-margin products like robotics; 2) cost reduction, mainly by squeezing suppliers.

Chips, the highest-value LiDAR component, are a primary cost-cutting target; but this often encounters technical blind spots.

A case in point: RoboSense's technical and patent dispute with single-photon detection chip leader Amsens. In 2021, to address SPAD chip shortages, RoboSense partnered with Amsens to co-develop SPAD-SoC chips, with RoboSense handling digital parts and Amsens focusing on SPAD design and analog parts. By 2023, the partnership ended.

In November 2025, RoboSense sued Amsens for trade secret and patent infringement; in December, Amsens counter-sued for trade secret and patent violations.

While these lawsuits focus on technical disputes, they reflect RoboSense's cost-control mindset.

RoboSense's 2025 gross margin was 26.5%, while Hesai's was 41.8%—a one-third difference in the same track (sector)! In reality, while both sell LiDAR, their customer bases and applications differ greatly: RoboSense "focuses" on low-price products.

"To cut costs, RoboSense must fully self-develop and control SPAD chips, leading to the dispute with Amsens," an industry insider noted.

The case is ongoing. Amsens claimed in late 2025 that RoboSense's E1 series infringes its patents and trade secrets. Worst-case, if courts support Amsens, related products could be banned, dealing a severe blow to RoboSense.

However, such disputes are not unique: Hesai is also suing Innovusion for patent infringement, with no judgment yet.

With certain scale growth, LiDAR competition in technology, scale, and ecosystem will intensify, with strong incentives to control costs, lower prices, and capture market share—likely leading to more technical and commercial disputes.

Robotics Business: "Trying Something New"?

With ADAS LiDAR market share consolidating and competition stiffening, giants are eyeing non-ADAS fields, with robotics as a key growth market.

Most aggressively, RoboSense—which declined most in ADAS—stated in its annual report that robotics has become its "second growth engine." In 2025, RoboSense shipped 303,000 LiDAR units for robotics and other uses, surpassing Hesai.

Note that RoboSense's robotics gross margins were 34.5% in 2024 and 39.7% in 2025; Hesai did not disclose robotics margins separately, but its overall margins were 42.6% in 2024 and 41.8% in 2025. Robotics margins typically exceed ADAS, so Hesai's robotics margins likely exceed its overall figures. Yet RoboSense's robotics margins are lower than Hesai's overall, indicating sharp pricing differences.

Industry analysts suggest that after losing ground in ADAS, RoboSense may seek to "fight back" with price wars in robotics. However, while robotics LiDAR margins are high, customization, high R&D costs, and weak scale effects mean Net profit margin (net margins) may not exceed automotive markets unless large bulk orders are secured. This brings us back to ADAS logic: large-scale robotics applications are limited, with even fewer clients, all under industry scrutiny.

Public info shows that leading embodied AI firm Unitree Technology's two humanoid robots use Hesai's JT128; Honor's first humanoid robot also uses the JT series.

Last month, Hesai announced it became Neolix's largest LiDAR supplier, providing ATX and FTX series for next-gen L4 autonomous delivery vehicles, covering all Neolix mass-production models; days later, Hesai signed a 10 million-unit exclusive supply deal with Roborock for JT series LiDAR for lawn mowing robots. Public data shows Hesai's robotics orders far exceed competitors', likely maintaining its lead.

RoboSense also stated in its earnings report that it secured an exclusive order from Ninebot's WindLand and recently partnered with Neolix.

Not to forget Huawei: at last year's Developer Conference, Huawei Cloud launched CloudRobo, an embodied AI platform providing core models for robotics firms. Huawei also established the Global Embodied AI Industry Innovation Center, collaborating with over a dozen leading robotics companies. Huawei's robotics "strategy" mirrors its automotive approach—providing technological foundations and platform support. Could Huawei repeat its automotive success in robotics?

Robotics is an important market but unlikely to offer a better business story than automotive. Why would ADAS laggards believe they can "turn around" in robotics?

Ultimately, as a rapidly evolving product with expanding applications, LiDAR's competitive edge comes from technology. After glimpsing profitability, industry competition will enter a new phase—shifting from cost and shipment battles back to technological and ecological prowess.

The views and opinions expressed in this article are for reference only and do not constitute investment advice. Investment involves risk; decisions should be made cautiously.

-

Hao Jida, Apple Supply Chain Coil Supplier, Switches Brokerage and Revives IPO Amidst Customer Dependency and Compliance Challenges

-

![]()

Annual Advertising Expenditure of VOYAH with Yudeshui: A Deep Dive

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket