'China's Pioneer Domestic GPU Stock' Moore Threads Posts Profit in Q1, Yet True Profitability Unverified

05/15 2026

05/15 2026

680

680

On May 13, Moore Threads inaugurated the Industrial Embodied AI Innovation Center at the Wuxi Embodied AI Industry Partner Salon. This event signifies its establishment of the first industrial ecosystem stronghold following its public listing, expanding its business scope from smart computing centers to the vast trillion-yuan embodied AI sector.

More than five months prior, on December 5, 2025, 'China's first domestically produced GPU stock' made its debut on the STAR Market. With an initial public offering (IPO) price of 114.28 yuan, its shares soared to 650 yuan at the opening bell and peaked intra-day at 688 yuan, marking an over 500% increase and briefly surpassing a market capitalization of 300 billion yuan.

However, financial reports paint a more sobering picture than the stock charts.

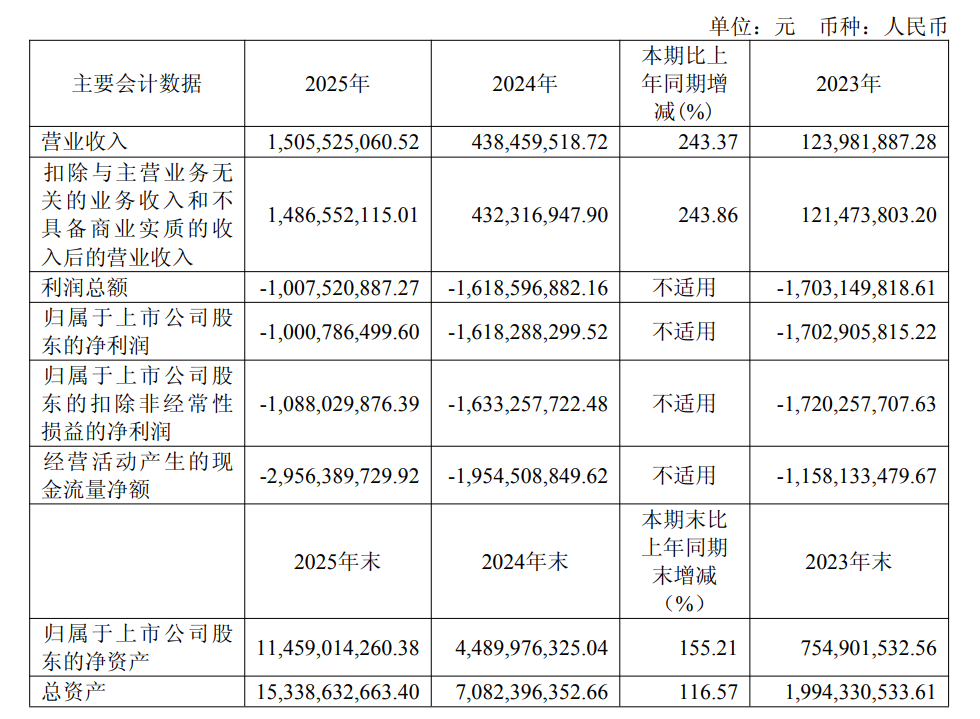

In 2025, Moore Threads' revenue reached 1.506 billion yuan, a 243% year-on-year surge. Yet, its gross margin declined from 70.71% to 65.57%, net cash from operating activities extended to -2.956 billion yuan, R&D expenditure climbed to 1.305 billion yuan (accounting for 86.68% of revenue), and the net loss attributable to shareholders stood at 1.001 billion yuan.

Source: Company Annual Report

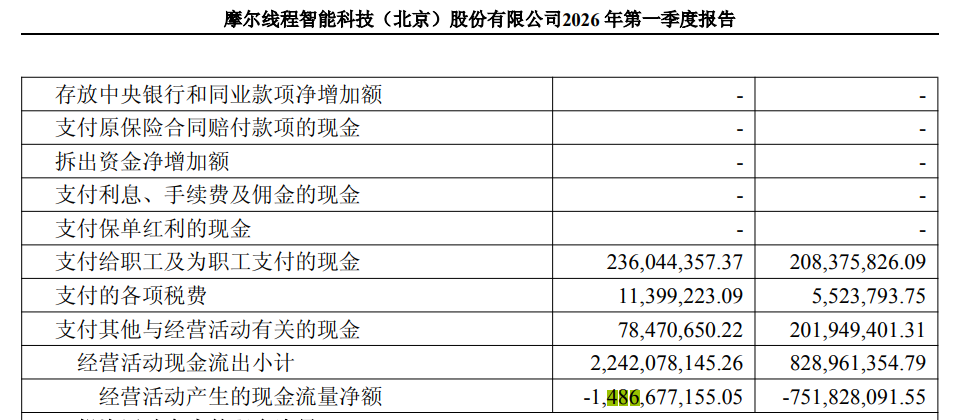

In the first quarter of 2026, the company reported its inaugural post-IPO profit, with a net profit attributable to shareholders of 29.359 million yuan. Nevertheless, non-recurring gains and losses amounted to 83.641 million yuan, leaving a core net loss of -54.282 million yuan after adjustments.

Notably, net cash from operating activities in Q1 2026 was -1.487 billion yuan, nearly doubling year-on-year.

Source: Company Financial Report

As a fabless semiconductor company, Moore Threads specializes in chip design, characterized by light asset utilization and rapid iteration cycles, while outsourcing all manufacturing processes. This business model prioritizes speed but compromises bargaining power within the supply chain, keeping cash flow under persistent pressure. Currently, 97% of its revenue stems from cloud smart computing contracts.

Meanwhile, the embodied AI sector remains in its nascent stages, with no immediate prospects for scalable revenue. For Moore Threads, the true challenge lies in transitioning its core business from 'narrative-driven' to 'profit-generating' before its cash reserves are depleted.

Source: Company Annual Report

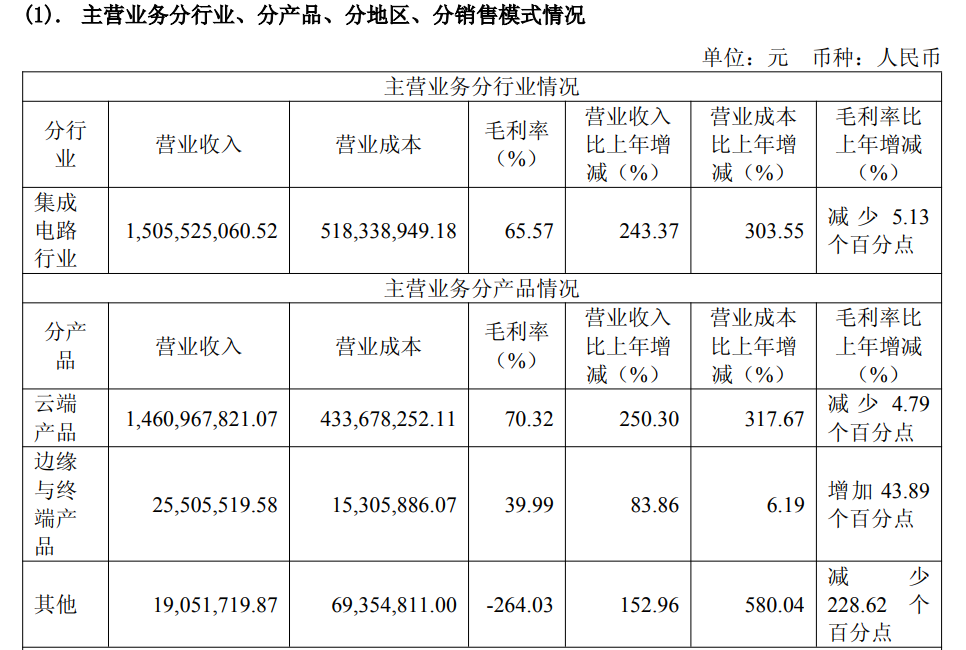

1. Declining Gross Margin and High Customer Concentration

In 2025, Moore Threads' revenue skyrocketed by 243.37% to 1.506 billion yuan, while its net loss narrowed by 38.1% to 1.001 billion yuan, maintaining robust growth since its inception.

However, a closer examination reveals growth risks that overshadow the losses. High margins failed to translate into equivalent market expansion, exposing an over-reliance on a single sector.

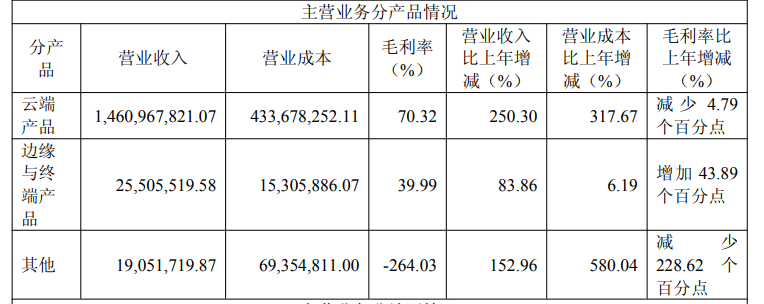

Cloud smart computing products generated 1.461 billion yuan in revenue (accounting for 97.04% of the total), with GPU boards, smart computing all-in-ones, and Kuae large-scale smart computing clusters forming the core. Edge and terminal products contributed a mere 26 million yuan (<2%), still in the early stages of market expansion and failing to establish an effective second growth curve. This leaves the company vulnerable to demand fluctuations in the smart computing sector.

In comparison, domestic peers experienced stronger growth in 2025: Cambricon's revenue reached 6.497 billion yuan (a 453.21% year-on-year increase), while Maxio Technology's hit 1.644 billion yuan (a 121.27% year-on-year increase), slightly surpassing Moore Threads.

Notably, margin trends diverged sharply: Cambricon's gross margin fell by 1.56 percentage points to 55.15%, Maxio's rose by 3 percentage points to 56.51%, while Moore Threads' margin dropped by 5.14 percentage points to 65.57% in 2025 and further by 10.27 percentage points to 67.35% in Q1 2026, indicating persistent margin pressure.

Source: Company Annual Report

Rising upstream foundry costs and a higher proportion of low-margin hardware integration in smart computing clusters further squeezed profits.

Moreover, Moore Threads' revenue is almost entirely tied to the smart computing cluster market. Annual report data reveals that its top five clients accounted for 1.375 billion yuan (91.36% of sales), primarily consisting of large internet firms and government agencies engaged in large-scale model training and smart computing center construction, with sizable single orders.

This highly concentrated customer base exposes weaknesses in channel development, with negligible expansion among small and medium-sized enterprises (SMEs).

For a company with just over 1.5 billion yuan in annual revenue, any adjustment in procurement rhythms, project delays, or strategic shifts by core clients could trigger sharp quarterly performance swings. This 'big-order dependency' model fills growth curves with uncertainty.

In response, Moore Threads plans to align with cutting-edge AI technologies, iterate products to meet differentiated demand, optimize its customer mix, and reduce reliance on major clients.

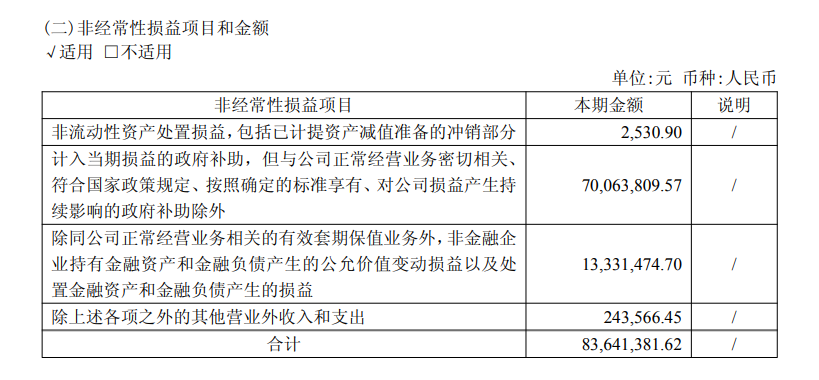

2. Government Subsidies Prop Up Quarterly Profit

In Q1 2026, Moore Threads achieved single-quarter profitability for the first time, with a net profit attributable to shareholders of 29.36 million yuan.

Non-recurring gains totaled 83.64 million yuan, including 70.06 million yuan in government subsidies (accounting for 84% of the total). After adjustments, the core business loss stood at 54.28 million yuan, indicating that self-sustaining profitability remains unproven.

Source: Company Financial Report

For 2025, non-recurring gains reached 87.24 million yuan, including 28.79 million yuan in government subsidies. Against a net loss of 1.001 billion yuan, these external infusions provided a buffer.

For domestic GPU firms still in the heavy R&D phase, policy support serves as a transitional phase. However, relying on policy dividends as the foundation of a business model is unsustainable in the long run.

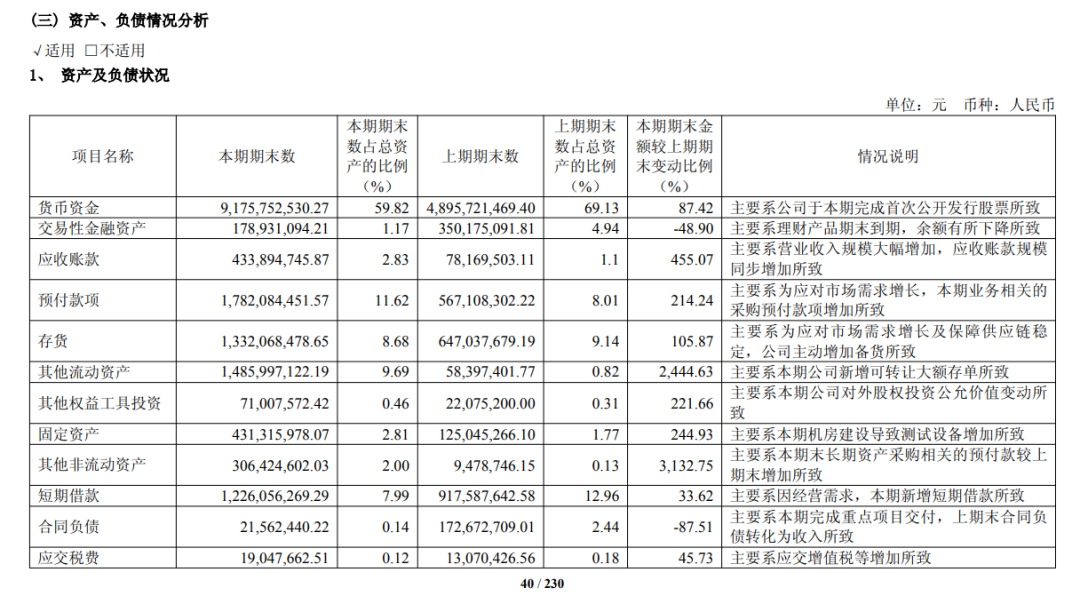

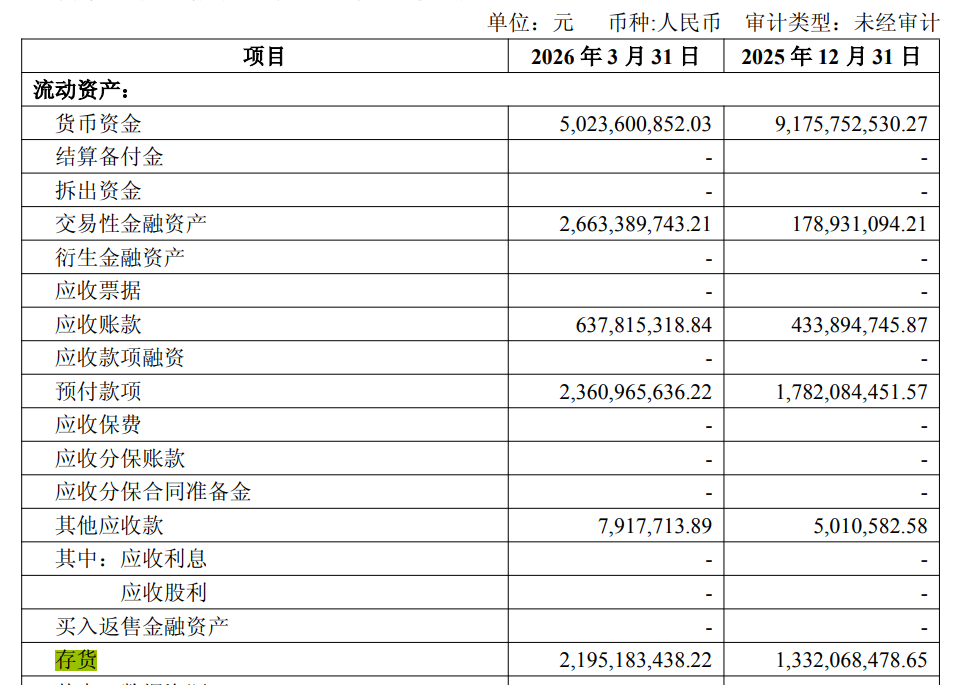

Inventory risks represent another underestimated threat.

Source: Company Financial Report

By the end of 2025, the inventory value stood at 1.332 billion yuan after 186 million yuan in impairment provisions, marking a 105.9% year-on-year increase. In Q1 2026, inventory climbed further to 2.195 billion yuan.

Source: Company Financial Report

Notably, the AI chip sector evolves rapidly, characterized by short product lifecycles. In 2025, the company booked 117 million yuan in inventory write-downs. If future demand underperforms or product iteration lags, inventory impairment pressures will intensify.

Moore Threads' rise aligns with a unique historical window: the shift from 'optional' to 'mandatory' domestic substitution.

Frost & Sullivan projects that China's AI chip market will grow from 142.5 billion yuan in 2024 to 1.3 trillion yuan by 2029, representing a 54% compound annual growth rate (CAGR). Scaling large-scale model training clusters and surging inference demand are driving the first wave of smart computing center upgrades.

In this context, Moore Threads' core strength lies in its 'full-stack' capabilities, powered by its self-developed MUSA architecture, which covers AI training, inference, and graphics rendering.

Additionally, its founding team, primarily composed of former NVIDIA executives, enables rapid product iteration and strong market responsiveness among domestic players.

However, gaps remain in technical accumulation, ecosystem development, and brand influence. Coupled with a single-client structure, subpar profitability, and mounting inventory risks, these challenges define Moore Threads' new phase.

The competitive landscape is intensifying. Huawei Ascend leads with full-stack capabilities and ecosystem strength, while Cambricon and Hygon Information have deep-rooted client bases. Emerging players like Maxio and Biren are rapidly launching products with capital backing, crowding the market.

In this environment, Moore Threads' path forward is clear: boost R&D to enhance product performance, expand channels to diversify clients and reduce concentration, and strengthen supply chain management to control inventory.

Yet, the gap between a 'clear path' and 'effective execution' remains vast.

3. Persistently High R&D Investment

In 2025, Moore Threads allocated 1.305 billion yuan to R&D (accounting for 86.68% of revenue), placing it in the top tier domestically and competitively internationally.

From another perspective, the company reinvested nearly 90% of its revenue into R&D while still posting losses.

Within R&D expenses, staff compensation exceeded 55% (725 million yuan), with technical service fees also rising. By the end of 2025, the R&D team numbered 1,009 (79.2% of total employees), with 77.21% holding master's degrees or higher. The company has filed 2,014 intellectual property (IP) applications, including 1,743 invention patents, building a full-stack proprietary tech framework from chip architecture to software stacks.

Source: Company Financial Report

In December 2025, the company unveiled its fifth-generation autonomous chip architecture 'Huagang,' boosting compute density by 50% and efficiency tenfold, supporting full-precision computing from FP4 to FP64. The 'Huashan' training-inference chip and 'Lushan' graphics rendering chip, based on Huagang, are in late-stage development.

In Q1 2026, R&D spending reached 369 million yuan (a 49.95% year-on-year increase), outpacing revenue growth.

This heavy R&D investment has been the core driver of Moore Threads' growth from zero to one in five years. However, its technical iteration speed and ecosystem maturity still lag behind international leaders. Founder Zhang Jianzhong stated at the MUSA Developer Conference: 'Where process falls short, architecture compensates.'

Moore Threads' R&D philosophy reflects its NVIDIA heritage.

Zhang spent 14 years at NVIDIA, rising from sales to Global Vice President and Greater China General Manager. Co-founders Zhang Yubo, Zhou Yuan, and Wang Dong also hail from NVIDIA's technical, ecosystem, and sales core departments.

This seasoned NVIDIA team brings not just proven tech routes and industry experience but also a deep understanding of the GPU sector's 'ecosystem-first' nature—a key reason for Moore Threads' full-function GPU strategy from inception.

On December 5, 2025, Moore Threads became 'China's first domestic GPU stock' on the STAR Market, attracting 80 venture capital/private equity (VC/PE) firms and nearly 8 billion yuan in funding. Capital markets bet not just on the company but on the 'NVIDIA-style' team's ability to replicate success.

In its annual report, Moore Threads positions itself as 'one of China's few firms with full-function GPU R&D and mass production capabilities.'

This claim holds merit, given its MUSA unified architecture and full-scenario product matrix, which hold an early-mover advantage in domestic full-function GPUs. However, viewed globally, its commercialization remains nascent, with leading status more confined to niche sectors than the broader market.

Recognizing that chip sales alone cannot disrupt market dynamics, Moore Threads is pursuing business model upgrades.

The May 13 Wuxi Industrial Embodied AI Innovation Center marks this shift. Unlike past tech collaborations, this center unites top institutions like Tsinghua AIR Innovation Center and Shanghai Jiao Tong University's Wuxi Photonics Chip Research Institute, along with 16 industrial chain (supply chain) firms including Tianqi Automation and Wuxi CRRC Times Intelligent Equipment, covering the full chain from upstream chips to downstream industrial applications.

The strategy is clear: replicate NVIDIA's path from hardware vendor to one-stop solution platform, building developer ecosystems and user stickiness through downstream application binding.

If successful, Moore Threads' valuation logic will transform from a client-dependent chip designer to an ecosystem leader shaping industry standards.

However, ecosystem building is a costly, long-term endeavor. NVIDIA spent over two decades building its CUDA empire, while Moore Threads' embodied AI ecosystem is just beginning. With the embodied AI market itself in early stages and business models immature, this new sector will not contribute material earnings shortly.

Moore Threads boasts a top-tier team, the rarest strategic position, and the most valuable window of opportunity. However, it also faces the most genuine dilemmas—the market is willing to pay for 'potential,' but not indefinitely.

The window of opportunity for domestic substitution will not remain open forever. 2026 will be a critical year; whether non-recurring profit can turn positive, whether the customer base can diversify, and whether

-

![]()

AI Agent Smartphones: The Next Competitive Edge Transcends Large Models

-

![]()

Over 880 Million Yuan Worth of Orders Unveiled, Bidding Launched for Shenzhen Eastern Public Transport

-

![]()

Tesla's Robotaxi Hits the Road: A Monumental Gamble with an Uncertain Future

-

![]()

Ford and Geely Forge New Joint Venture in Spain, Sidestepping Changan and JMC

-

![]()

199 RMB! Godox's First Camera Review: Subpar Photography, Transparent Viewfinder Frame is the Highlight

-

![]()

AI Smartphones: A Modern-Day 'Emperor's New Clothes'?

-

![]()

Yonyou Network: A Company Selling 'Transformation' but Struggling in Its Own Transition

-

![]()

Focus | CCCC’s Takeover of Greentown Comes to Fruition: Why Did the 11-Year ‘Control Without Authority’ Era End?