Hynix Employees Await 3 Million Won in Bonuses, Samsung Employees Go on Strike: A Dramatic Clash Between Korea's Memory Giants

05/15 2026

05/15 2026

550

550

Both companies are raking in profits, yet SK Hynix employees are awaiting an estimated 3 million won in average annual bonuses for 2026, earning them the nickname 'big shots,' while Samsung employees are taking to the streets to demand fairness. Both companies produce memory chips and are riding the AI wave, so where does the gap lie? The answer lies in their profit-sharing systems. This is not a technical analysis but a business parable about how to divide the pie.

01

A Tale of Two Extremes

In early 2026, something surreal happened in South Korea's memory chip industry.

At SK Hynix, employees in the first quarter received year-end bonuses averaging over 100 million won per person—more than 500,000 yuan—coupled with rumors of a 140 million won annual bonus for 2025, roughly 650,000 yuan. On social media, they were dubbed 'Hynix VIPs.' The dating market was even more absurd, with some pretending to work at Samsung to avoid being pursued for their wealth. You can sense the mindset behind this.

Image source: Internet

Then, on April 23, many workers at Samsung's Pyeongtaek campus walked off the production line to demand justice.

Image source: Internet

Both in South Korea and in the memory chip business, the disparities are staggering. On TV, a person wearing a Hynix uniform walks into a luxury store, and the staff's attitude changes instantly. A new term emerged: 'Hai Yi Chi Han'—Hynix, medical school, dental school, and traditional Korean medicine school—all considered equally prestigious in the South Korean dating market. Meanwhile, Samsung lost over 200 senior engineers in the first four months of the year, with some jumping to Hynix and boasting a 3.5-fold salary increase—not 35%, but 350%.

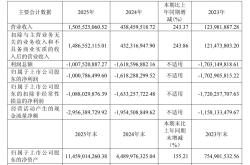

Both companies are making money hand over fist, and the numbers are staggering. Samsung's first-quarter operating profit hit 57.2 trillion won, up 756% year-on-year. These figures are 'insane' by any industry standard. But once the money enters company coffers, where it flows is a different story.

Hynix's approach can be summed up in one word: splurge. Macquarie, an international investment bank, made an extremely optimistic forecast: if operating profit reaches 447 trillion won by 2027 and 10% is shared as bonuses, per capita bonuses could soar to 1.29 billion won, or 6.1 million yuan. Six point one million yuan in annual bonuses. Of course, this is an extremely optimistic estimate and not yet guaranteed, but even if 80% is achieved, it would still be remarkable.

What about Samsung's memory division? Per capita bonuses range from 450,000 to 600,000 yuan. Not bad, but when compared side by side, it's a case of 'inequality is worse than scarcity.'

Thus, the anger of tens of thousands of workers could no longer be contained. The union stubbornly demanded conditions: abolish the bonus cap and allocate 15% of operating profit for sharing.

Shin Jae-yoon, chairman of Samsung's board, panicked and warned that a strike would wipe out tens of billions of dollars in exports. Did it work? On May 13, the second round of labor-management negotiations collapsed, and the union announced a general strike starting May 21, potentially lasting dozens of days. Since Samsung's founding in 1969, nothing like this had ever happened.

Image source: Internet

The gap between people in the same country and industry is hard to describe. But in the end, it's not about who has more money—it's about how the pie is divided.

02

Systems Determine Destiny

Why is the gap widening despite both companies being profitable?

SK Hynix and Samsung are both thriving in the same supercycle for memory chips, but the lives of their employees are diverging at a visible pace.

Frankly, this isn't about who works harder—it's about their profit-sharing systems.

Hynix underwent a genuine systemic revolution. In September 2025, it signed a ten-year labor agreement with its union, allocating 10% of annual operating profit directly into employee performance bonuses. Critically, the cap that previously limited profit-sharing bonuses to no more than 1,000% of base salary was removed.

Image source: Internet

How is this money distributed? 80% is paid immediately, with the remaining 20% deferred over two years, earning a 10% annual fixed return. Even more aggressively, up to half of the bonus can be converted into company stock. This bonus pool is primarily for engineers, though it's unclear whether all formal employees are covered. However, it's expected that all formal employees will receive some share.

This wasn't the boss's sudden act of generosity—it was hard-fought at the negotiating table, round after round, in black and white.

What about Samsung? It's still stuck in traditional arithmetic. Its bonus system relies on overall performance and target achievement rewards. No matter how high the memory division's profits, the bonus cap is usually set at 50% of annual salary. While some at Hynix earn bonuses worth 1.5 times their annual salary, Samsung employees face a transparent glass ceiling—company profits are linked to their earnings, but with a strict cap. The share they receive has already been predetermined.

This situation is quite frustrating.

I ran the numbers. In 2025, Hynix employees' average bonus was estimated at around 140 million won, roughly 650,000 yuan. Samsung's memory division averaged 450,000 to 600,000 yuan. The difference was about a hundred thousand yuan—not glaring. But in early 2026, things changed dramatically. Hynix's first-quarter operating profit margin soared to 72%. Extrapolating this for the full year, per capita bonuses could reach 3.5 million yuan. Even optimistically, Samsung's average would be around 2.35 million yuan.

What's the difference? 1.15 million yuan. A year earlier, the gap was just 100,000 to 200,000 yuan. In one year, a chasm opened.

Samsung's union is now fighting to enshrine 15% of operating profit in contracts and abolish the 50% cap. Management offers only 10%. Whether they'll succeed remains unknown.

Image source: Internet

Of course, beneath these profit-sharing differences lie fundamental earning capabilities.

03

HBM: Rewriting the Rules

Frankly, this round of memory industry riches boils down to one thing: HBM.

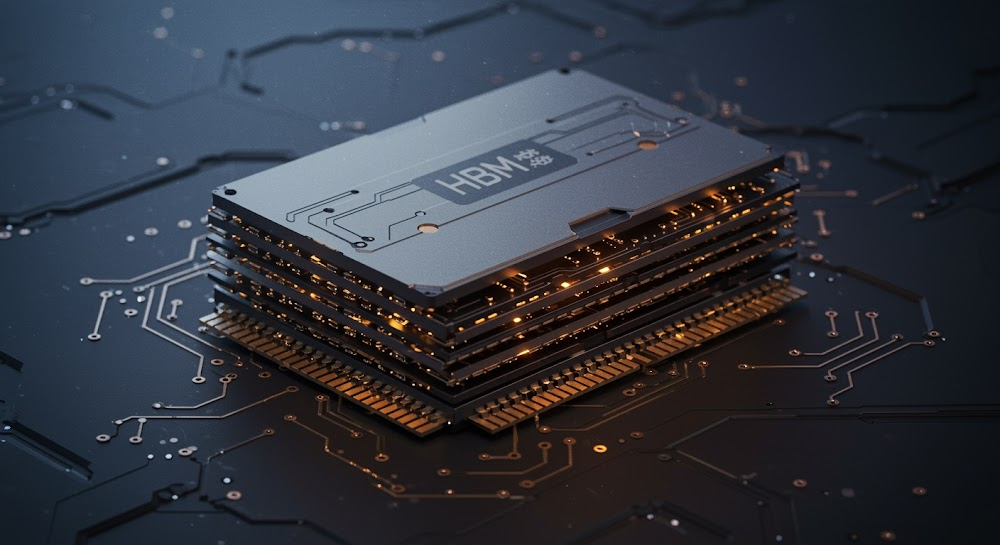

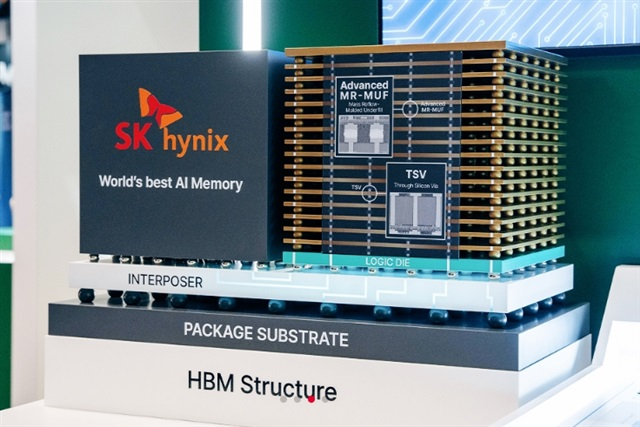

Why? Think about it—AI training requires GPU speed, but without sufficient data, it's useless. It's like a chef with unparalleled skills but no ingredients—stuck waiting. Traditional memory bandwidth can't keep up, causing data bottlenecks and idle compute power. HBM's brilliance is simple: stack DRAM chips like floors in a building, connect them with TSV silicon vias, and multiply data transmission channels.

However, a single AI server uses eight times more HBM than a standard server, and producing one HBM wafer consumes the capacity of three DDR5 wafers with lower yields.

Image source: Internet

Reduced production and high demand have pushed HBM3E 36GB prices sharply upward, with some high-spec products doubling from two years ago. DDR5 particle prices are even crazier, surging over tenfold in the same period. The four major cloud giants invested hundreds of billions of dollars in AI infrastructure in 2026—a significant portion flowed to HBM manufacturers.

Who benefits the most? SK Hynix.

This company has sharp vision. In 2014, when HBM was still a concept, Hynix partnered with AMD to develop it. In 2021, it became the first to mass-produce HBM3, coinciding with NVIDIA's large-scale shipments, making it a core supplier. While competitors were still tackling technical challenges, Hynix captured roughly 60% of the global HBM market. Its 2026 capacity? Fully booked, with orders two years out. Most absurdly, Hynix proposed a 50% price hike to NVIDIA, which accepted it without hesitation. In Q1 2026, Hynix's operating profit margin hit 72%, significantly higher than most global semiconductor giants. In 2025, its profits surpassed Samsung's for the first time in history.

Image source: Internet

What about Samsung? In short: started early, finished late.

Samsung stumbled on heat and power consumption tests for HBM3 and HBM3E, failing NVIDIA's certification for an extended period. Samsung denies 'failure' but admits tests are ongoing. You know the drill—2024–2025 was the golden window for AI GPUs when HBM was scarce and prices peaked, and Samsung watched Hynix cash in. Later, some HBM3E passed tests, but the market hierarchy was set, contracts signed, and doors closed. Now Samsung pins its hopes on HBM4 for a comeback.

But let's not forget—Samsung remains the world's largest and most financially robust memory manufacturer. By May 2026, its market cap briefly topped $1 trillion, making it Asia's second tech company (after TSMC) to reach this milestone. It's not weak—it has money, factories, and technical accumulate (accumulation). But in this round of AI memory, it clearly lags behind SK Hynix.

Yet market competition is an infinite game. Samsung might catch up someday.

04

The Strike's Dilemma

In Q1 2026, Samsung Electronics reported 133.9 trillion won in revenue, a 756% surge in operating profit, a market cap exceeding $1 trillion, and its stock price tripling in a year. Time to celebrate, right? Wrong—on April 23, Pyeongtaek campus saw the largest strike since 1969.

The more money earned, the bigger the problems. Counterintuitive, but not surprising.

The trigger was simple: SK Hynix abolished bonus caps, and its employees' bonuses surged to over three times Samsung's. In short: 'they eat meat, we drink thin soup.' Samsung's frontline workers, comparing paychecks, couldn't take it anymore. Union membership soared, and demands shifted from 'give us benefits' to 'enshrine 15% of operating profit in contracts'—a fight for systemic change.

The union wants a predictable future; management wants to retain flexibility. This isn't about money—it's about power.

The timing couldn't be worse.

The union announced a general strike starting May 21. Samsung was at a critical juncture for HBM4 mass production—NVIDIA and AMD orders were piling up, and every minute of downtime could send orders to Hynix. Some estimated losses at 40 trillion won (over $180 billion). Over a thousand tier-1 suppliers and hundreds of tier-2/3 suppliers would suffer.

Image source: Internet

South Korean Prime Minister Kim Min-sik called emergency meetings, even considering emergency powers. The JoongAng Ilbo put it bluntly: this isn't just a corporate issue—it's shaking South Korea's foundations. Chairman Shin Jae-yoon warned more directly: hundreds of billions in exports lost, tens of trillions in tax revenue gone, currency pressure, GDP decline. Samsung's veins are welded to South Korea's economic arteries.

Capital markets were even harsher. On May 13, Samsung's stock plunged over 6%, while SK Hynix surged 7.68%. Capital voted with its feet: if you can't manage your own employees, why should clients trust you to deliver on time?

Frankly, this strike reveals something brutal. The tech cycle lifted Samsung to the clouds, but cracks in its profit-sharing system might pull it down first. Between the clouds and the abyss lies a paycheck.

05

The Shadow of Cycles

In memory, the boom times demand caution.

This is, at its core, a commodity business. When shortages hit, prices skyrocket; when oversupply occurs, every sale loses money. It's a relentless cycle. Three years ago, SK Hynix was in the mud—7.73 trillion won in operating losses for 2023, 9.14 trillion won in net losses, with ugly financials. Now, those sky-high bonuses and dating-market prestige are partly a gift of the cycle.

Things seem stable now, right? AI models are devouring HBM, low yields lock in capacity, and Samsung, Hynix, and Micron tacitly control supply. But this is the prisoner's dilemma the memory industry knows well—everyone understands that expanding production together is suicide, yet they clench one's teeth (clench their teeth) and do it anyway for market share. Samsung's HBM capacity will flood in 2027, Micron and ChangXin are fighting for orders, and Goldman Sachs already predicts double-digit HBM price drops in 2026. Can today's high margins hold?

There's also something else that makes people feel even more uncertain. SK Hynix has staked 70% of its advanced process capacity on HBM and DDR5, tying itself too closely to NVIDIA. When NVIDIA thrives, so does Hynix; when NVIDIA catches a cold, Hynix gets the flu. The question is, with cloud vendors spending so much money on GPUs, can AI revenue keep up? Capital markets are already demanding returns, and end consumers are not buying it—they wait and watch when prices rise, and hold out for price drops. This chain is more fragile than imagined.

Image source: Internet

What about the engineers in Seoul? They are actually more aware than anyone else. The second half of 2026 might mark the peak of this cycle, and the technological roadmap could change at any moment. History has repeatedly shown you that 'this time is different' are the four most expensive words.

The memory chip cycle never shows mercy. Everyone gets drunk at the feast and no one wants to leave. Will they wake up with a hangover the next morning, find their warehouses filling up, and then slap their thighs in realization: Oh, the cycle has come again.

- END -

-

![]()

Five Emerging Golden Entrepreneurial Pathways in the Agent Ecosystem: A Deep Dive into the Report (Part 2)

-

![]()

GEM-TIPS Makes Its Debut at Shenzhen International AI Expo: “Octopus AI Brain” + Intelligent Agent Cluster Pave New Ways for Industrial Intelligence

-

![]()

'China's Pioneer Domestic GPU Stock' Moore Threads Posts Profit in Q1, Yet True Profitability Unverified

-

![]()

Hynix Employees Await 3 Million Won in Bonuses, Samsung Employees Go on Strike: A Dramatic Clash Between Korea's Memory Giants

-

![]()

Twelve Years On, Can Cheng Yixiao Steer Kling to Another Victory?

-

![]()

From Data Scarcity to Open Source Boom: How China's Embodied AI Data Industry Can Break Through

-

Trend丨Indium Phosphide (InP) Prices Soar Amid AI Boom, with Cycles and Disruptions Set to Continue

-

![]()

One Article to Decode 'Computing Power Inflation': Why AI Costs Less for You While Computing Power Firms Rake in Profits