Three Paths for Computing Power Energy Storage: The Divergent Strategies of Kstar, Shoto, and Sungrow | Xinliu AIDC Column

05/18 2026

05/18 2026

638

638

[Abstract] With the leap in power density of AI computing centers (AIDC), traditional lead-acid + UPS backup power architectures are gradually becoming obsolete, making high-voltage lithium batteries, HVDC, and solid-state transformers essential.

The global AIDC energy storage market is expected to grow at a super-high compound annual rate of 52.7%, with demand projected to expand 15-fold by 2030 compared to 2026. An industrial restructuring centered around the 'foundation of computing power' has already begun.

In this wave, three types of players have taken distinct breakthrough paths: Kstar leverages its existing advantages to secure orders on two fronts; Shoto successfully transforms by relying on its deep customer resources, with AIDC energy storage becoming its primary growth driver; Sungrow enters the field with its leading photovoltaic and energy storage technologies and substantial financial resources, taking a bet on cutting-edge technologies. This article aims to dissect the positioning logic, core product advantages, and risks and challenges of these three representative manufacturers, shedding light on who will truly capture the massive power demand behind AI computing power.

The following is the main text:

01 Problems Precede Opportunities

To understand this supply chain, we must first clarify why data centers suddenly need 'energy storage' rather than just 'backup power.'

Data center energy storage is no longer just a backup power source that 'keeps things running for 30 seconds during a blackout.' For decades, a simple architecture of lead-acid batteries paired with UPS systems was sufficient to provide short-term power until diesel generators could start up, given the power density of 6-8kW per cabinet in traditional data centers.

However, the rise of AIDC (Artificial Intelligence Data Centers) has fundamentally overturned this architecture. Fully loaded GB200 NVL72 cabinets consume over 120kW of power. While Huawei's Ascend 384 super node doubles computing power, the power density of entire cabinets surges to 30-40kW, with some scenarios even exceeding 600kW.

High-rate discharge, rapid response, and high spatial density have become core requirements for AIDC energy storage, making traditional lead-acid batteries entirely unsuitable.

As a result, two types of incremental demand have emerged in the market: new AIDC installations requiring lithium battery backup systems and the replacement of lead-acid batteries with lithium batteries in existing data centers. Guosen Securities estimates that the global AIDC-related HVDC market will reach approximately 38 billion yuan by 2030, with solid-state transformers accounting for about 23.9 billion yuan. According to the Vice President of Narada Power, global demand for high-voltage lithium batteries in data centers is expected to reach around 20GWh in 2026, surpassing 100GWh by 2030. If green power supply becomes widespread by then, energy storage demand could exceed 300GWh, 15 times the 2026 estimate.

To put these numbers in perspective, global new energy storage installations in data centers were just 16.5GWh in 2024. The core challenge in this sector has shifted from 'whether there is a market' to 'who can meet the explosive demand.'

02 Kstar: Deep Technological Application and Dual-Track Layout for an Established Data Center Player

Kstar has been in the data center infrastructure business for over three decades, primarily focusing on UPS systems with batteries as a complementary offering. Its clients include leading internet giants such as ByteDance, Alibaba, and Baidu. The acceleration of AIDC construction represents not a crossover but a dual upgrade in terms of pricing and product specifications for Kstar.

In terms of product layout, Kstar has developed a full-stack solution covering power supply, temperature control, and high-voltage DC systems.

The Power Fort integrated power module has been successfully deployed in a large cloud computing data center in Zhejiang, offering high efficiency, reliability, and intelligence suited for high-density computing scenarios. The LiquiX AI liquid-cooled CDU, launched in response to the liquid cooling trend in AIDC, further enhances temperature control capabilities for high-power cabinets. Additionally, Kstar plans to introduce a complete 800V HVDC product line in 2026, directly compatible with NVIDIA's next-generation Rubin Ultra platform, covering mainstream AI computing architectures.

In market expansion, Kstar has achieved substantial breakthroughs in North America's external power supply business for cabinets, securing its first batch of UPS OEM orders worth over 100 million yuan in 2025, with a second batch exceeding 300 million yuan scheduled for delivery in 2026. Domestically, testing with ByteDance takes about six months, and positive feedback by the end of Q1 2026 could drive significant revenue growth, demonstrating its tangible technological positioning value.

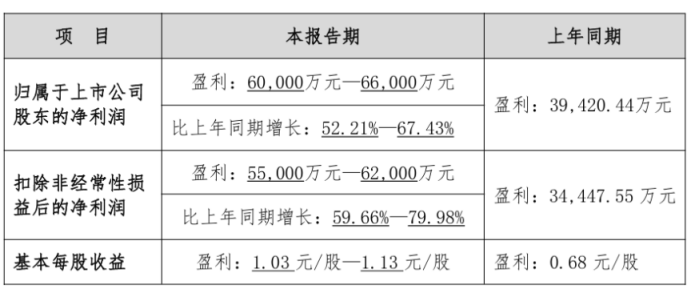

Kstar's financial performance also reflects the strength of its AIDC business: net profit attributable to shareholders is expected to reach 600 million to 660 million yuan in 2025, up 52% to 67% year-on-year. Soochow Securities projects that data center revenue will exceed 3 billion yuan for the full year, up about 20% year-on-year, while energy storage revenue will reach approximately 900 million yuan, nearly doubling year-on-year. Revenue in the first three quarters increased by 23.93% year-on-year, with Q3 single-quarter growth accelerating to 41.71%.

Source: 2025 Annual Performance Forecast of Shenzhen Kstar Science & Technology Co., Ltd.

However, Kstar is simultaneously ramping up efforts in both AIDC power supplies and BESS, two areas with vastly different competitive dynamics.

Running both tracks in parallel inevitably requires trade-offs in resource allocation. Moreover, there is no industry consensus on the timeline for HVDC to replace UPS. Kstar's official stance is to maintain dual-track preparations: optimizing existing UPS efficiency while also developing HVDC capabilities. This strategy is sound in principle but means it cannot fully commit to either direction in execution.

03 Shoto: Market Resource Conversion, Customer Barriers, and Scenario Migration

The core narrative of Shoto's story is straightforward—the customer trust accumulated over two decades in telecommunications base station energy storage became a direct passport into data center energy storage in 2025. Shoto is one of the few companies in the industry to complete a four-dimensional layout covering customers, technology, capacity, and globalization, with AIDC energy storage officially established as its primary growth engine.

In its 2025 annual performance announcement, Shoto explicitly adopted a 'one core, two wings' strategy, focusing on AIDC energy storage as the core, with new power storage and telecommunications storage as supporting pillars. The business structure upgrade and strategic transformation fully manifested in 2025, accelerating its shift from a traditional telecommunications storage manufacturer to a global provider of AIDC energy infrastructure solutions. On April 10, 2026, Shoto announced plans to invest in an annual production capacity of 12GWh for semi-solid-state AIDC energy storage cells.

The telecommunications and data center scenarios are highly homologous, both demanding extreme power supply reliability and having certification cycles typically exceeding one year. This high switching cost has turned Shoto's customer resources into a difficult-to-replicate moat.

Shoto has consistently ranked among the top global suppliers of energy storage batteries for telecommunications and data centers, covering all five major domestic telecommunications operators and serving five leading global telecommunications operators and equipment manufacturers. Among the top ten self-owned data center enterprises in China, 80% are stable customers. This customer network, built over two decades, provides the most solid growth foundation for its AIDC business.

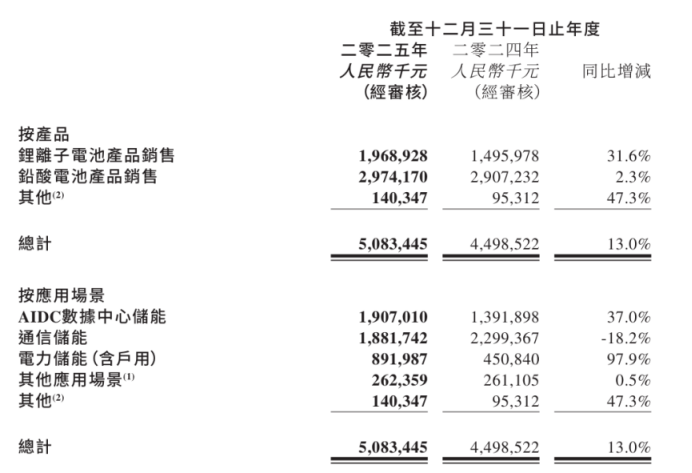

From an operational structure perspective, the group achieved revenue of 5.083 billion yuan in 2025, up 13.0% year-on-year, with lithium battery product revenue accounting for 38.7% of the total. The business structure continued to optimize toward high-growth, high-value-added directions. Revenue from AIDC energy storage reached 1.907 billion yuan, up 37.0% year-on-year, accounting for 37% of total revenue, officially surpassing telecommunications storage as the group's largest revenue source, marking the full formation of its second growth curve.

More groundbreaking is the explosive growth in the AIDC segment, where lithium battery revenue surged by 598.3% year-on-year, and sales volume increased by 531.8% year-on-year, far exceeding expectations for the replacement speed of high-rate lithium battery products in backup power and energy storage scenarios for computing centers. This also reflects Shoto's leap in product structure.

Figure: Shoto's Revenue Breakdown by Product and Application. Source: Shoto's 2025 Annual Performance Announcement

Products and technologies are the core strengths supporting Shoto's high growth in AIDC. Traditionally focused on selling battery products, Shoto began extending into systems in 2025.

The 'ImmerGuard' high-voltage lithium battery system is a new product specifically developed for AIDC scenarios, supporting multi-scenario customization for 'source-grid-load-storage integration.' The aluminum-shell 5MWh standardized energy storage system adopts semi-solid-state cell technology and a 1P104S structure, improving energy density and standardization. The AI SmartEye battery monitoring system, jointly developed with the Dalian Institute of Chemical Physics, Chinese Academy of Sciences, is based on an architecture of 'battery intrinsic mechanisms + deep learning + digital twins' and won the TOP Innovation Award at the 2025 International Energy Storage Innovation Conference. The low-temperature sodium battery, capable of stable discharge at -40°C, was developed in collaboration with Tsinghua University and achieved mass production and commercialization, primarily targeting cold-climate scenarios and specific overseas markets.

Source: Shoto

Additionally, Shoto's moat lies in customer relationships, certification completeness, and service response speed. The revenue contribution from its top five customers dropped from 54.2% in 2022 to 34% in 2025, a positive sign of reduced dependency. However, the real pressure is that the competitive landscape in the AIDC energy storage sector began to change dramatically in the second half of 2025. While customer barriers are effective against smaller players, their efficacy against entrants like CATL remains to be seen over time. Shoto's relatively single product line and concentrated market focus make its volatility coefficient higher than most competitors.

04 Sungrow: High-Stakes Crossover, The Photovoltaic and Energy Storage Giant Bets on AIDC

Among the three, Sungrow entered the AIDC power supply market latest but with the strongest capital and technological reserves.

In May 2025, Sungrow explicitly announced on the Shenzhen Stock Exchange's interactive platform that it would establish a department to develop AIDC power supply business; the first complete units rolled off the production line in June; and in July, it simultaneously entered testing processes with two leading cloud service providers in Virginia and Texas, USA. The entire process, from announcement to shipment, took less than three months.

This speed was made possible by its existing technological foundation, which did not require building from scratch. Sungrow's inverters and energy storage systems have long operated on 1500V platforms, making 800V DC a downgrade and allowing it to apply existing technological capabilities to new scenarios. Meanwhile, NVIDIA's white paper explicitly mentions SST (Solid-State Transformer) paired with large-scale energy storage as one of the ultimate forms of AIDC power supply architectures. Sungrow has been pre-researching 35kV solid-state transformers for nearly a decade, an accumulation virtually unmatched among current competitors.

Financially, it has strong support. In 2025, revenue reached 89.18 billion yuan, with net profit attributable to shareholders at 13.46 billion yuan, up 33% and 56% year-on-year, respectively. Overseas revenue in the first half of 2025 was 25.379 billion yuan, accounting for about 58%, while energy storage business gross margins remained high. The company shipped 43GWh of energy storage systems globally in 2025, a significant increase from 28GWh in 2024. With substantial cash flow, Sungrow can afford to support a new direction that may take two to three years to generate meaningful revenue.

Source: Sungrow's 2025 Annual Report Summary

On August 26, 2025, Sungrow announced the establishment of an AIDC business division. The composition of its team reflects a clear understanding of the task—core members primarily come from professional data center power supply companies like Delta and Eaton, rather than being directly transferred from within the photovoltaic and energy storage divisions. This indicates an awareness that AIDC power supply and photovoltaic inverters involve entirely different approaches in customer relationships, certification systems, and service logic, and that muscle memory from photovoltaic and energy storage cannot be directly applied.

The real question is how wide the window of opportunity is. Foreign leaders like Vertiv, Eaton, and Schneider Electric have been operating with global cloud service providers for years, while domestic markets have deeply embedded local suppliers like Kstar, as mentioned earlier. Sungrow's technological entry point is clear, but the path from 'first complete units off the production line' to 'scaled order deliveries' involves not just time but also the scene's demand for supplier error tolerance. Data centers allow no room for trial and error.

In its investor relations documents, Sungrow describes its AIDC business as 'striving to achieve product rollout and small-scale deliveries in 2026,' using remarkably restrained language. This is not avoidance but an accurate recognition of the track ( track can be translated as 'sector' or 'market'). What it is doing now is using the excess profits from its core photovoltaic and energy storage business to buy an entry ticket for AIDC—2026 to 2027 will be the true validation period.

05 Epilogue

A horizontal comparison (Horizontal comparison) reveals the distinct logics of the three companies:

Kstar focuses on deep technological application, relying on scenario understanding and mature product capabilities to secure the current market. However, running two tracks in parallel means it cannot achieve maximum focus in either direction. Shoto leverages a customer list accumulated over two decades to gain a first-mover advantage in sector switching. Its current challenge is whether it can convert this advantage into deeper technological barriers before major players fully enter the field. Sungrow makes a well-prepared crossover while its core business generates strong cash flow, betting that new architectures like SST will eventually land and that it will be a major beneficiary as the deepest pre-researcher.

Different logics correspond to different risk profiles. When new production capacities are concentratedly put into operation from 2026 to 2027 and the competitive landscape undergoes accelerated reshuffling, it will gradually become clear who is on the right path.

-

![]()

Focus | CCCC’s Takeover of Greentown Comes to Fruition: Why Did the 11-Year ‘Control Without Authority’ Era End?

-

![]()

Final Verdict: The 2026 China Auto Forum Shines with Unique Characteristics at a Pivotal Moment

-

![]()

Tencent Maintains Matrix Approach, Alibaba Merges Entry Points: Tech Titans Initiate AI Agent Consolidation

-

![]()

Geely Secures Portion of Ford’s Spanish Production Capacity

-

![]()

Tesla Stalls This Second

-

![]()

Elon Musk's 'Money-Burning' Spree: All Car Sales Profits Poured into AI

-

![]()

Why Did Tesla’s Profits Drop and Cash Flow Go Negative?

-

![]()

AI Titans Are All in the Red: Time for Intelligent Driving Car Buyers to Reassess?