The 'Double-Edged Sword' of Roborock's Operations: Soaring Scale Amid Profit Dilemma Under Heavy Marketing Spend

06/12 2026

06/12 2026

467

467

By | Xingxing

Source | Beiduo Business & Beiduo Finance

On June 2, Roborock (688169.SH) announced that it plans to use its own funds to repurchase some of its issued Renminbi ordinary shares (A-shares) through centralized bidding transactions, with a repurchase price not exceeding RMB 179.86 per share and total repurchase funds ranging from RMB 300 million to RMB 400 million.

However, behind this confident repurchase plan, the sentiment in the secondary market has quietly changed. On May 27, a block trade occurred in Roborock, with 56,600 shares traded at RMB 100 per share, totaling RMB 5.6647 million. The closing price of the company on that day was RMB 117.00 per share, meaning the transaction was discounted by approximately 14.53%.

This was not an isolated incident. Two weeks earlier, on May 11, a large block of Roborock shares was also sold at a discount, with a transaction price of only RMB 98 per share, a 17.91% discount from the closing price that day, and a transaction amount of RMB 6.1740 million. The total amount of the two transactions exceeded RMB 10 million. Such "discount sales" occurring on the eve of the repurchase announcement are intriguing.

As funds choose to exit painfully rather than stay, it reflects the market's reassessment of the value of Roborock, once known as the "king of robot vacuums." Whether due to concerns about profit recovery, product diversification progress, or considerations for future growth expectations, Roborock's valuation logic is clearly no longer as glamorous as before.

Roborock's story begins with Xiaomi's ecosystem.

According to Tianyancha and public information, in 2016, Roborock launched its first Mi Home robot vacuum cleaner as an OEM for Xiaomi, gaining a foothold in the market with its self-developed LDS laser radar navigation technology. Leveraging Xiaomi's brand, channel, and supply chain advantages, this robot vacuum cleaner achieved sales of one million units in just 16 months.

As Xiaomi's ecosystem matured, the first batch of OEM companies that grew up also gradually accumulated technology and validated production capacity, beginning to plan for "going solo." Roborock also launched its own brand, "Roborock Smart Robot Vacuum Cleaner," in 2017, taking the first step toward independence.

In the following years, Roborock has been fighting to build its own brand barriers. When it listed on the STAR Market in 2020, the company's own brand business accounted for about 70.7% of its revenue, and this figure increased to 98.8% the following year. In 2023, Roborock claimed the top spot in global sales in the robot vacuum cleaner industry, earning the nickname "king of robot vacuums."

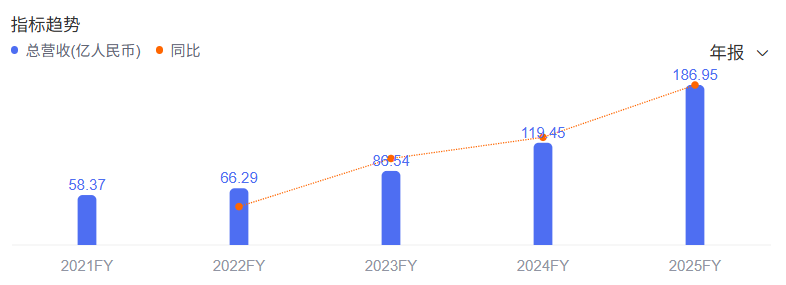

Roborock's revenue scale indeed supports this story. From RMB 5.837 billion in 2021 to RMB 8.654 billion in 2023, the company's revenue climbed steadily, with a compound annual growth rate of approximately 21.76%. In 2024, revenue surpassed RMB 10 billion, increasing by 38.03% year-on-year to RMB 11.945 billion.

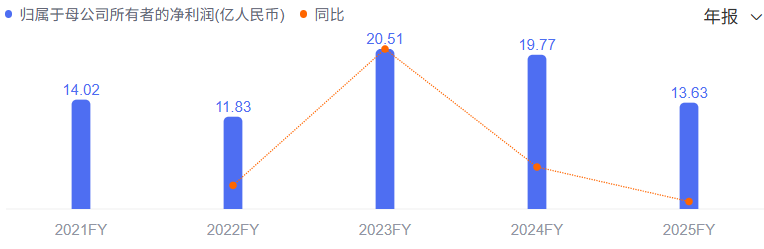

However, the glamour of revenue did not fully translate to the profit side. After reaching RMB 1.402 billion in net profit attributable to shareholders in 2021, Roborock's profit fell to RMB 1.183 billion in 2022. Although it rebounded strongly by 73.32% in 2023, reaching a record high of RMB 2.051 billion, it declined again by 3.64% to RMB 1.977 billion the following year.

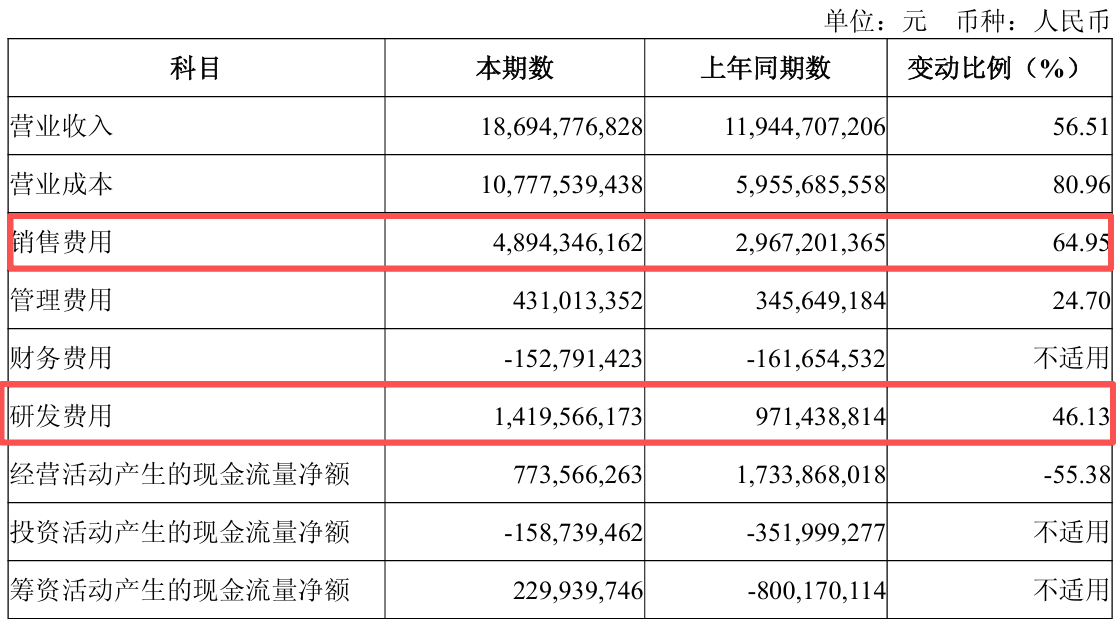

In 2025, the rift between Roborock's revenue growth and profit decline widened further. Annual revenue increased by 56.51% year-on-year to a record high of RMB 18.695 billion, but net profit attributable to shareholders fell to RMB 1.363 billion, a 31.03% year-on-year decline, with profit performance even worse than four years ago.

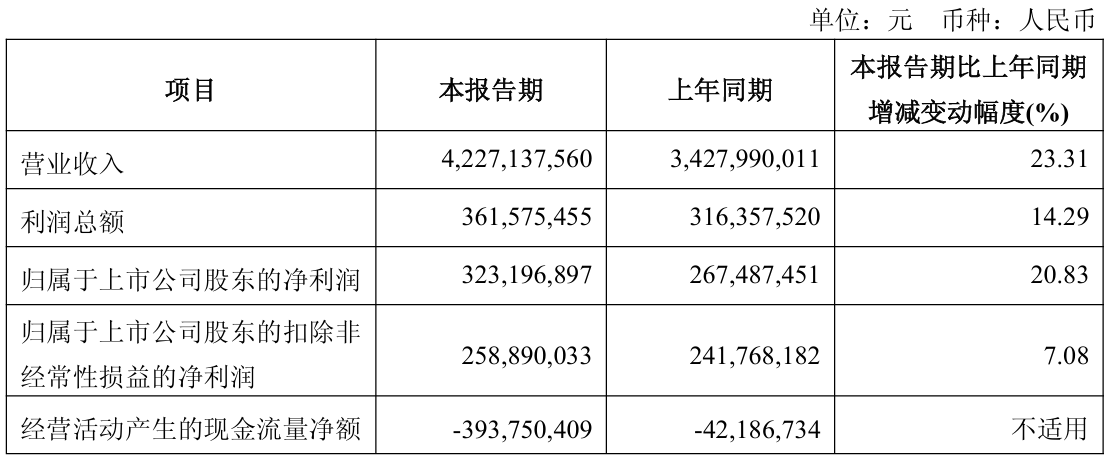

In the first quarter of 2026, Roborock's performance showed signs of recovery, with revenue increasing by 23.31% year-on-year to RMB 4.227 billion and net profit attributable to shareholders also increasing by 20.83% to RMB 323 million. The company attributed this to the sales of its high-end flagship product, the G30S Pro, but whether a single product can support its overall profit recovery remains to be seen.

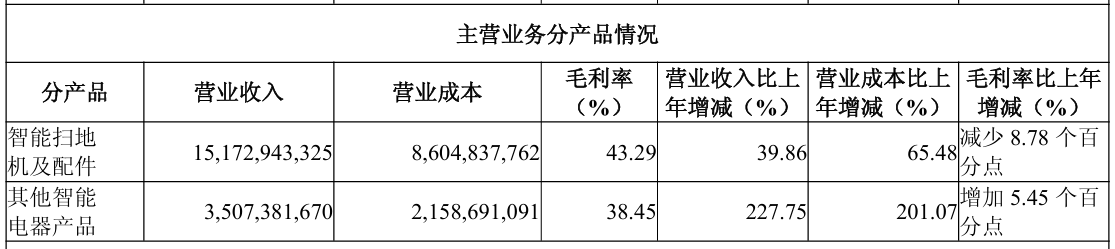

What exactly is eroding Roborock's once-impressive profits? The answer lies in its product mix. To capture market share, the company adjusted its business strategy to be "scale-oriented" starting in the third quarter of 2024, actively increasing the shipment proportion of mid-range and entry-level robot vacuums to achieve greater user coverage.

This approach of "trading profit for scale" has indeed earned Roborock a solid market position. According to IDC's latest "Global Home Intelligent Cleaning Robot Market Tracker," Roborock ranked first in both sales volume and value in the robot vacuum cleaner market, with a 27% global market share.

While the market position looks good on the surface, the company's profitability is starting to weaken. Roborock's gross margin for its main business fell from 55.32% in 2023 to 50.36% in 2024 and further to a low of 42.38% by the end of 2025, evaporating nearly 13 percentage points in just two years.

The "profit concession" in product mix is only one side of the coin. Shifting focus to expenses reveals that the excessively high sales expense ratio is the "invisible killer" eroding Roborock's profits.

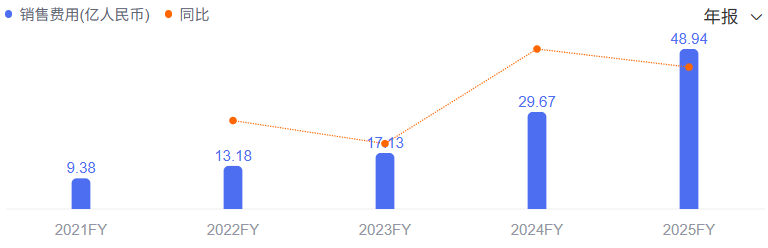

In 2021, Roborock signed Xiao Zhan as its brand ambassador, with sales expenses of about RMB 938 million that year, which could still be considered "restrained." However, these expenses have since surged, increasing by over 40% year-on-year to RMB 1.318 billion in 2022 and doubling to RMB 2.957 billion in 2024.

In 2025, Roborock's annual sales expenses skyrocketed by 64.95% year-on-year to RMB 4.894 billion, with a sales expense ratio as high as 26.18%. Advertising and marketing expenses surged to RMB 3.259 billion, a 69.42% increase, and platform service fees and commission expenses reached approximately RMB 868 million.

In other words, for every RMB 100 in revenue Roborock earns, it spends RMB 26 on sales, with over RMB 17 going to advertising and channels. The company's research and development expenses appear much more "low-key" in comparison. In 2025, R&D expenses were about RMB 1.420 billion, a 46.13% increase but less than one-third of sales expenses.

Entering 2026, Roborock's issue of "heavy marketing, light R&D" persists. Although sales expense growth slowed to 7.79% in the first quarter, the RMB 1.026 billion investment remains difficult to ignore, while R&D expenses were only RMB 286 million. The marketing-driven growth model does not seem to have truly shifted despite the profit decline in 2025.

This raises the question: Is this "king of robot vacuums," known for its technological edge, driving growth through technology or merely maintaining market share by burning money on marketing?

Roborock admitted in its 2025 financial report that to accelerate the full-price-band layout of its smart robot vacuum and floor-washing machine businesses, the company opened up the market through dense (intensive) new product and technology launches, which put some pressure on overall gross margins in the short term. However, this move could drive business growth and enhance global influence.

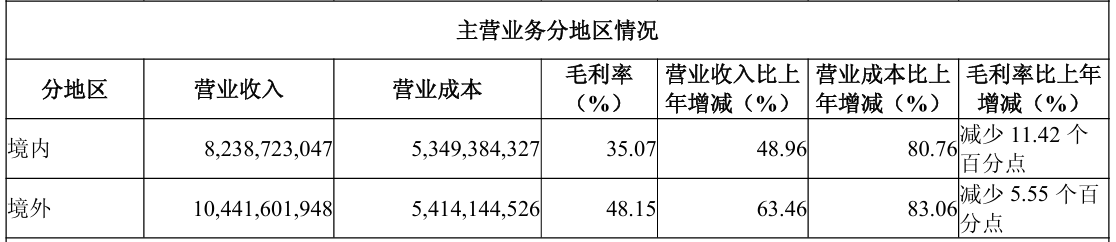

Indeed, Roborock's overseas business layout (layout) has achieved certain results. In 2025, the company's overseas revenue exceeded RMB 10 billion for the first time, increasing by 63.5% year-on-year to RMB 10.442 billion, accounting for 55.9% of total revenue and surpassing the domestic market for the first time to become the company's largest revenue source.

During major promotional events like "Prime Day" and "Black Friday" in 2025, Roborock ranked among the top sellers in Europe, North America, and Asia-Pacific regions, with the highest market share in some countries. By the end of the year, the company's products covered more than 170 countries and regions globally, with cumulative sales of smart robot vacuums exceeding 25 million units.

However, the problem remains that Roborock's fate, both domestically and overseas, is tightly tied to the single product category of robot vacuums. With an intensifying price war in China, although the incremental market is expanding, profit margins are being continuously squeezed. The structural flaw of "relying on one leg" is gradually becoming a Sword of Damocles hanging over the company.

To reduce the concentration risk of a single category and open up a second growth curve, Roborock has begun layout (laying out) new product categories. It has initially formed a multi-category matrix covering robot vacuums, floor-washing machines, washing machines, and lawn mowers, transitioning from household floor cleaning to a strategic layout (layout) of smart living across all scenarios.

In 2025, sales volume of Roborock's other smart appliance products reached approximately 2.1689 million units, a 250.45% year-on-year surge, while revenue also increased by 227.75% year-on-year to RMB 3.507 billion. However, this segment accounted for only 18.76% of total revenue, leaving a long way to go before it can truly support a diversified growth story.

According to a research report by Kaiyuan Securities, in 2026, Roborock's washing machines, floor-washing machines, and lawn mowers are expected to reduce losses by RMB 400 million, RMB 200 million, and RMB 100 million, respectively. The floor-washing machine business as a whole and the domestic robot vacuum market are expected to turn profitable, while the lawn mower business is expected to break even. In other words, the company's new businesses have yet to enter the profit-contributing stage.

On June 12, 2026, Roborock's stock price once hit RMB 98.43 per share, the lowest in 52 weeks (one year), retreating more than 55% from its historical high of RMB 237.48 per share. The once-thousand-billion-yuan market capitalization has vanished, leaving only RMB 27.49 billion today.

Roborock once told a compelling story of an OEM factory growing independently into the "king of robot vacuums" by "de-Xiaomi-izing." Today, however, it finds itself trapped in the "scale narrative" it wove. High marketing expenses, unfilled gaps from new businesses, and a significant stock price retreat are all costs and growing pains of its rapid expansion.

However, the expansion of its overseas footprint and loss reductions in new businesses at least show that Roborock still has "aces" up its sleeve. The story is far from over; the key lies in whether the company can find a new balance between scale and profit.

-

![]()

Should 44 Million Electric Vehicles Be Subject to Road Maintenance Fees If They Don’t Refuel?

-

![]()

US Stock IPO | Anthropic and OpenAI File Successively, Three Giants Aim for a Combined $4 Trillion Market Debut

-

This Smart Toilet Enterprise Holds the Key to AI Computing Power

-

![]()

Breaking News! An AI Company Valued at 5.8 Trillion USD Rushes for IPO with Annual Revenue of 170 Billion USD

-

The Underground 'Computing Battle': How HPC and Large Models Revolutionize Oil Exploration

-

![]()

New Breakthrough! Haiguang Optoelectronics Clears HKEX IPO Hurdle

-

![]()

AI Computing Power Surge Propels Dongtian’s Optoelectronic Communication Business to Soar!

-

![]()

Is Saido the fallback option for Seres?