Is Saido the fallback option for Seres?

06/12 2026

06/12 2026

515

515

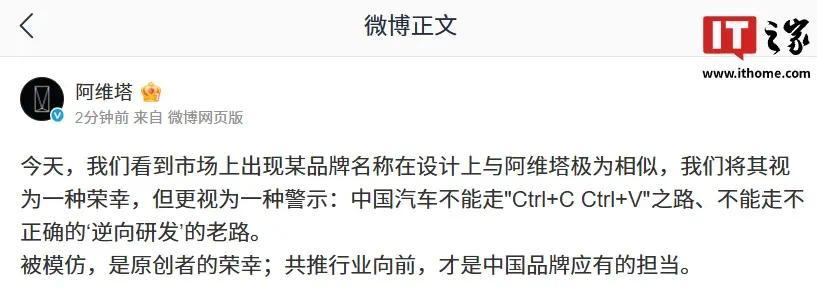

On the evening of June 9th, Saido Technology unveiled its new automotive brand, AIVA, in Beijing. Earlier that afternoon, Avatr's official social media account took the first shot: 'Chinese automakers must not follow the 'Ctrl+C Ctrl+V' path,' and 'Being imitated is the honor of the original creator.' Everyone could see the implication—the four letters of AIVA resemble both Avatr's AVATR and Aito's AITO.

The verbal sparring was lively, but it conveniently obscured the biggest issue with the Seres brand: a company claiming to de-Huawei-ify still chose a name heavily associated with Huawei.

Actions speak louder than words.

Beyond the brand controversy surrounding AIVA, what deserves more attention is that Seres has quietly completed its structural adjustments, with Saido serving as a fallback option for Zhang Xinghai's entire group.

Zhang Zhengyuan: Proving Himself for the Third Time

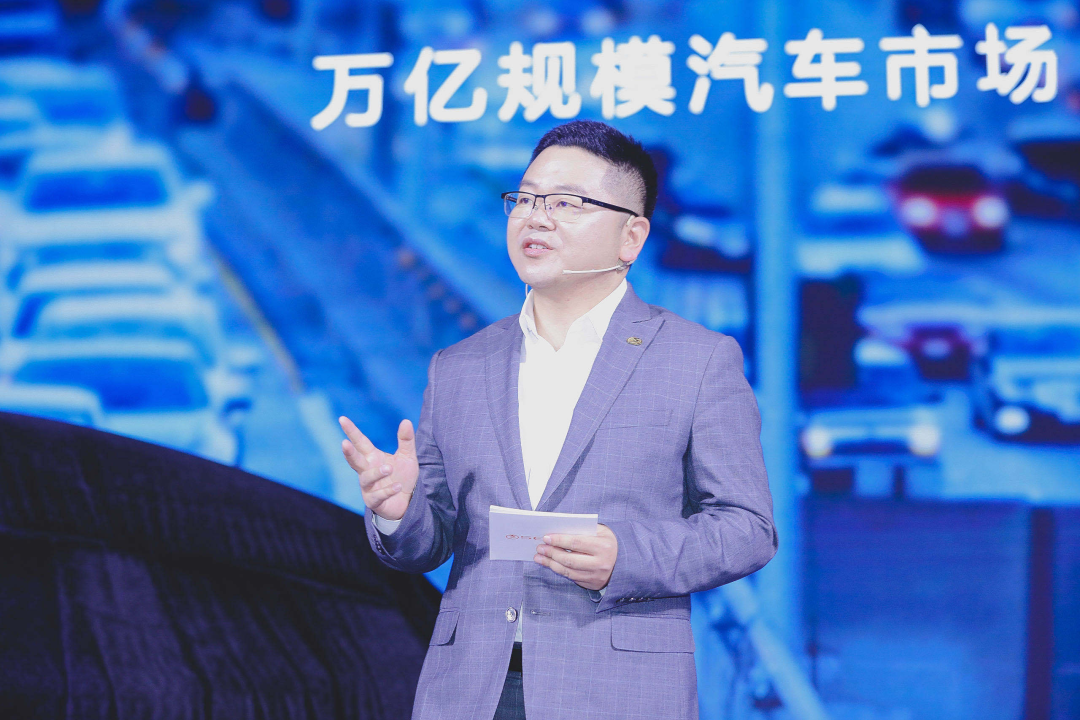

At a small-scale pre-launch briefing, Saido Technology Chairman Zhang Zhengyuan first clarified one point: 'The claim that Saido Technology is Seres' second brand is incorrect.'

Zhang Zhengyuan is the nephew of Seres founder Zhang Xinghai, born in 1981. His resume reflects a typical sales-oriented background: General Manager of Dongfeng Xiaokang's Procurement Center, General Manager of Chongqing Xiaokang Import & Export, General Manager of Sales Company, and later a board director at Seres Group, with long-term responsibility for sales and marketing. He has never been involved in product definition.

Prior to Saido Automobile's launch, Seres had already completed its family-style strategic layout (deployment): On June 5th, Zhang Xinghai stepped down as Seres Automobile's chairman, succeeded by his son Zhang Zhengping (born 1989). On June 9th, nephew Zhang Zhengyuan unveiled AIVA. Within a week, the Zhang family had positioned its lineup—the son guards Aito, while the nephew tests life without Huawei.

Interestingly, Zhang Zhengyuan's career trajectory and Aito's success are deeply intertwined. His greatest victory came in 2021 when he spearheaded Seres' collaboration with Huawei, building Aito's sales and service system from scratch—the 40,000-unit monthly sales network for Aito was his brainchild, marking the pinnacle of his career.

However, his independent ventures have all faltered: As chairman, manager, and legal representative of the Lantech brand, its first model sold 21,600 units in 2023. Seeing Aito's success, Lantech claimed to 'incorporate Huawei technology,' though it only used HiCar smartphone integration, which consumers saw through. By the first half of 2025, retail sales had collapsed to 10,300 units, down 34% year-on-year, with further contraction in 2026. Over three years, Lantech cycled through three technological narratives—Dongfeng's foundation, Huawei's peripheral tech, and now Doubao.

This created an inescapable public relations vortex: Was Aito's success due to Zhang Zhengyuan's business acumen or Huawei's inherent advantages?

This marks his third attempt to prove himself—and the first time he holds full command.

This is also why he insists Saido is not Seres' second brand. Saido must 'cut ties' with Seres as much as possible.

Three reasons explain this. First, financial reporting: Lantech has been a thorn in the listed company's side, with monthly sales in the hundreds to low thousands dragging down overall performance. Second, resource allocation: Aito consumes the majority of production capacity and marketing budgets, leaving Lantech starved for development resources. Moreover, with Aito using HarmonyOS cockpits across its lineup, developing a second cockpit solution internally would publicly divert resources. Third—as a joint-venture automaker insider revealed to 21st Century Business Herald—an independent legal entity can bypass the exclusivity clauses in Huawei's cooperation agreements. Remaining within the group would make de-Huawei-ification contractually impossible.

However, the benefits of independence are substantial: A 6.67 billion yuan capital increase, with Chongqing Shapingba's state-owned fund 'Shaci Zhiyuan' holding 34.5% as the majority shareholder, CATL's Quest Investment taking ~9.89%, an employee stock ownership plan controlling 16.48%, and Seres contributing existing assets to reduce its stake to 32.96% while deconsolidating performance. Post-independence, Saido can independently plan production lines, supply chains, and distribution channels without group-level constraints.

Zhang Zhengyuan must prove his capabilities are entirely independent of Huawei and Seres.

No Free Agents in This Alliance

Why Seres needs this external experiment becomes clear when examining its financials.

From 2022 to the first half of 2025, Seres procured over 75 billion yuan from its top supplier, including 42 billion yuan in 2024 alone. Advertising and channel expenses soared from 4 billion yuan in 2022 to 18.1 billion yuan in 2024. These investments yielded tangible results: The Aito M9 dominated the 500,000-yuan SUV segment for 21 consecutive months, with 2025 revenue reaching 165.05 billion yuan, two consecutive years of profitability, and dual A+H listings.

But the Q1 2026 report revealed colder numbers: Revenue hit 25.746 billion yuan, up 34.46% YoY; net profit attributable to shareholders was 754 million yuan, up just 0.89% YoY; core profit (excluding one-time gains) plunged 73.87% YoY to 103 million yuan. Non-recurring gains contributed 652 million yuan, with government subsidies alone accounting for 628 million yuan—meaning the company generating over 25 billion yuan in quarterly revenue earned just 100 million yuan from its core business, a 0.4% core profit margin. The shadow of rising revenue but stagnant profits not only persists but deepens. The better Aito sells, the more it proves Seres lacks profit distribution rights in its most successful business.

This isn't unique to Seres. Under Huawei's Smart Selection model, Huawei deeply controls product definition, design, core technologies, channels, and brand marketing, while automakers handle vehicle manufacturing and supply chains—a dynamic faced by all second-tier automakers in this partnership.

Avatr fired the first shot, but three distinct narratives emerged.

First, brand defense: AVATR's diluted name represents real losses, and with Avatr facing sales pressure, grabbing attention through controversy offers real benefits. Second, proxy warning: Huawei itself could never speak out—Aito represents Smart Selection's face, and publicly criticizing Seres would expose alliance fractures. With Avatr and Seres both holding 10% stakes in HiNova (Huawei's joint venture), having another alliance member attack under the guise of 'originality vs. copying' focuses fire on the name while threatening the act of departure itself. Third, pure coincidence.

No sources confirm the second narrative. But alliance politics dictates: It doesn't matter who fires the shot—all members hear the same message: Departure carries consequences.

Adding to this gunfight's awkwardness: CATL is both an Avatr shareholder and a Saido investor. The shooter and the target share the same battery supplier. Loyalty in this alliance has always been contractual, not strategic.

The True Test of Independence

Now, let's examine the substance of this 'independence.' Saido's supplier lineup includes: ByteDance for cockpit interaction (Doubao and Volcano Engine 'co-defined, co-designed'), DeepRoute.ai's NOA solution for advanced autonomous driving (instead of Huawei's ADS), CATL for batteries, and majority funding from Chongqing state-owned assets.

The sole achievement of de-Huawei-ification is expanding the supplier list from one row to four.

At SAIC's 2021 shareholders' meeting, Chairman Chen Hong famously rejected Huawei's turnkey solution, stating: 'That would make Huawei the soul and SAIC the body. We must keep our soul in our own hands.' Seres initially took the opposite path—surrendering its soul to Huawei for its first payday. Now, it's using that payday to purchase four new souls in the market.

What about self-developed technologies? In 2024, Seres invested 7.053 billion yuan in R&D (4.86% of revenue), much of it adapting Huawei's Smart Selection solutions. Lantech cycled through three technological narratives in three years, each time changing suppliers but never itself.

Rereading the 'clever' strategies from Chapter One becomes illuminating: Ceding control, deconsolidating performance, making state-owned assets the majority shareholder, binding employees through stock ownership, and ensuring failures don't tarnish the listed company's financials. Individually, these are textbook moves; collectively, they form a confession—a company's hedging strategies reveal its true beliefs. Seres lacks confidence in 'life without Huawei' to even risk consolidation. It designed this experiment as: If it succeeds, Seres retains 32.96%; if it fails, the listed company bears no responsibility.

This is Zhang Zhengyuan's real dilemma. He must prove 'Seres and I can succeed without Huawei.' Yet in his setup—cockpit, autonomous driving, batteries, and funding all come from external partners—the one link (link) needing no external help still doesn't exist.

The mass-produced AIVA ME7 hits the market this year, officially targeting the 200,000+ yuan segment, directly competing with Xiaomi SU7, Model 3, and XPeng P7+. Seres' approach to escaping Huawei? Replacing one Huawei with four Huawei-like partners. If ME7 correctly answers the 'product definition' question for the first time, all this cleverness will matter—Zhang Zhengyuan has roughly six months left.

-

![]()

History’s Largest IPO Is Set to Debut—But Chinese Investors Are Shut Out

-

![]()

Should 44 Million Electric Vehicles Be Subject to Road Maintenance Fees If They Don’t Refuel?

-

![]()

US Stock IPO | Anthropic and OpenAI File Successively, Three Giants Aim for a Combined $4 Trillion Market Debut

-

This Smart Toilet Enterprise Holds the Key to AI Computing Power

-

![]()

Breaking News! An AI Company Valued at 5.8 Trillion USD Rushes for IPO with Annual Revenue of 170 Billion USD

-

The Underground 'Computing Battle': How HPC and Large Models Revolutionize Oil Exploration

-

![]()

New Breakthrough! Haiguang Optoelectronics Clears HKEX IPO Hurdle

-

![]()

AI Computing Power Surge Propels Dongtian’s Optoelectronic Communication Business to Soar!