Zhongji Innolight and Its Peers Turned into AI Scratch Cards by Wall Street

06/15 2026

06/15 2026

398

398

The Endpoint of Computing Power 'Water Sellers' Becomes Wall Street's Gaming Machines

Can U.S. Investors Experience a 40cm Limit Down with Zhongji Innolight?

Zhongji Innolight and its peers have finally caught Wall Street's attention. However, the way they are seen and the actions taken do not involve raising long-term funds and entering the market with financial reports. Instead, volatility is packaged and presented first. The financial reports of Zhongji Innolight and its peers are still there, and the industry chain logic remains intact. But in Wall Street's hands, what is served first is the double-leveraged ETF.

Simply put, Zhongji Innolight, YOFC, and TFC Communication are being turned into AI lotteries by Wall Street.

The foundation of this lottery is, of course, fundamentals. NVIDIA is still selling cards, cloud vendors are still expanding their CapEx, and AI data centers are consuming more and more high-speed optical modules. However, in Wall Street's hands, fundamentals are merely raw materials. What is truly processed is volatility, and this means:

Wall Street treats 'investing' in Zhongji Innolight and its peers as running a casino.

01 SK Hynix Hits the Jackpot First

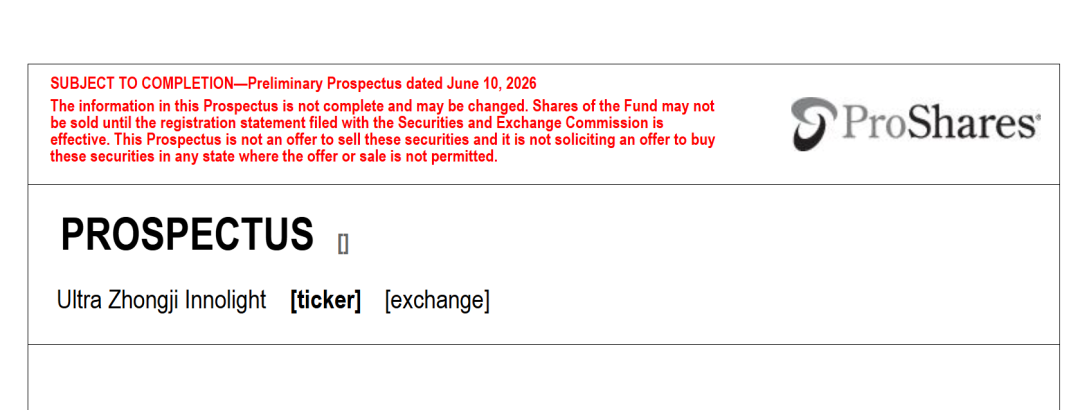

Recently, U.S. ETF issuer ProShares filed with the SEC to launch a product named ProShares Ultra Zhongji Innolight, aiming to track twice the daily performance of Zhongji Innolight's stock.

In summary: If Zhongji Innolight rises by 1%, this product theoretically aims to rise by 2%; if Zhongji Innolight falls by 1%, it theoretically aims to fall by 2%.

But that's not all. Besides Zhongji Innolight, ProShares also simultaneously filed for double-long products related to Chinese AI hardware companies such as YOFC and TFC Communication. It even preemptively filed for other AI supply chain-related companies like CATL, Luxshare, and Cambricon.

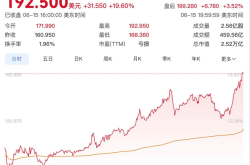

In other words, Wall Street is not just targeting a single company but packaging the 'Big Three' A-share optical module companies and other enterprises into its AI trading shelf. Once the news broke, many investors immediately became excited, and even Zhongji Innolight's intraday stock price briefly surged after the information spread.

The market is so excited because a similar scenario just played out with SK Hynix, and the gains were quite irrational.

In October 2025, CSOP Asset Management launched the SK Hynix Daily Leveraged 2x Product on the Hong Kong Stock Exchange. The logic behind this product is simple: it aims to track twice the daily performance of SK Hynix. If Hynix rises, it strives to rise twice as much; if Hynix falls, it strives to fall twice as much.

On its own, this product is just an ordinary leveraged tool; but placed within the AI market trend, the enormous gains immediately distort its original purpose.

From the chart, this product has almost continuously risen since its launch, driven by the HBM and DRAM shortage trend, with its price surging from single digits to a peak of HKD 148.65. Of course, there were retracements, oscillations, and large negative lines along the way, but the overall trend was incredibly exaggerated.

This event greatly stimulated the market and ordinary investors. It proved that as long as an asset is believed by the market to be related to AI, capable of rising, volatile, and understandable to retail investors, financial institutions can repackage it. While a stock's rise may reflect industrial prosperity, a double product's rise transforms it into a financial narrative—and grants access to the ticket of financial freedom.

So, when ProShares included Zhongji Innolight, YOFC, and TFC Communication in its double-long product filings, the market naturally thought of SK Hynix. This is what truly excited the market.

In the past, A-share investors discussing Zhongji Innolight and its peers focused on how long the optical module trend could last. However, after ProShares' double-long product filings, the question shifted: It's no longer whether Zhongji Innolight and its peers can rise but whether overseas capital will treat them as the next 'Hynix trade.'

This question alone is enough to excite the market. Because capital markets love hearing not entirely unfamiliar stories but old scripts that have just proven successful once.

So, is China's version of SK Hynix really coming?

02 What's Coming Is Not China's SK Hynix

But Rather, SK Hynix-Flavored AI Lottery?

China's version of SK Hynix certainly sounds appealing. With SK Hynix's K-line having set an example, the market can easily transpose its imagination:

South Korea has HBM; China has optical modules. SK Hynix was turned into a double product, and so were Zhongji Innolight and its peers. SK Hynix had a massive rally, so can Zhongji Innolight and its peers have another?

Unfortunately, what's coming this time may not be the next SK Hynix but merely an SK Hynix-flavored AI lottery.

The reason is simple: When SK Hynix was discovered, it was more like a value discovery. In the past, the market viewed SK Hynix through the lens of the memory cycle: price hikes, price drops, capacity expansions, and inventory reductions. It wasn't until AI servers placed HBM at the center of the table that investors suddenly realized this company wasn't just a cyclical stock but an indispensable 'shovel seller' in the AI arms race.

But Zhongji Innolight and its peers are different. Before ProShares launched its double-long products, were A-share optical modules lying at the bottom? In fact, since 2023, optical modules have been one of the strongest themes in A-share AI trends. Zhongji Innolight, YOFC, and TFC Communication are no longer obscure companies hidden in the corners of the supply chain.

800G, 1.6T, North American CSPs, Nvidia's supply chain—these terms have been discussed countless times by the market. In the end, even those who don't follow tech stocks know that if AI continues to burn money, optical modules will undoubtedly be a critical piece. The stock prices are even more honest: In about a year, Zhongji Innolight surged over 15x, YOFC over 13x, and TFC Communication over 600%.

But here's the issue: Zhongji Innolight and its peers have already proven themselves. Now, the market doesn't just want proof—it wants continued proof.

Early investors in Zhongji Innolight bought it when the market hadn't fully grasped optical modules. Now, investing in Zhongji Innolight means betting on whether it can continue to exceed market expectations after the market has already understood its value. The former is value discovery; the latter is a game of odds.

During the value discovery phase, the market can reward you for 'being better than expected.' But in the odds game phase, the market asks: 'Are you even better than I imagined?' So, for Zhongji Innolight and its peers now, only continuing to exceed expectations counts as positive news; anything less than imagined may be treated as a disaster.

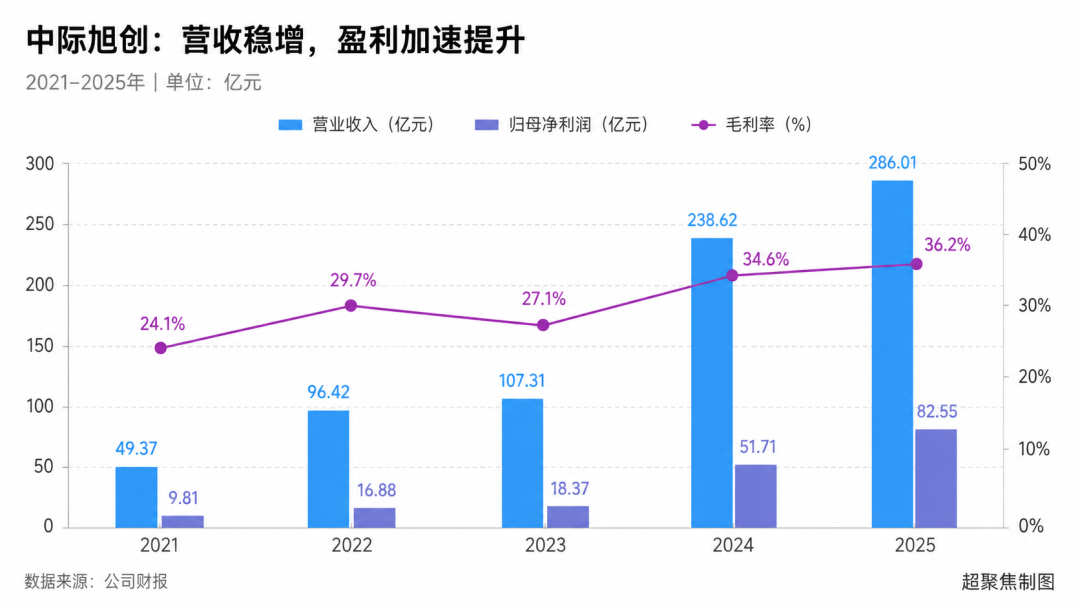

Of course, this doesn't mean Zhongji Innolight's growth rate may slow down. After all, the reality of high growth is undeniable: From 2021 to 2025, Zhongji Innolight's revenue grew from RMB 4.937 billion to RMB 28.601 billion, net profit from RMB 981 million to RMB 8.255 billion, and gross margin from 24.1% to 36.2%.

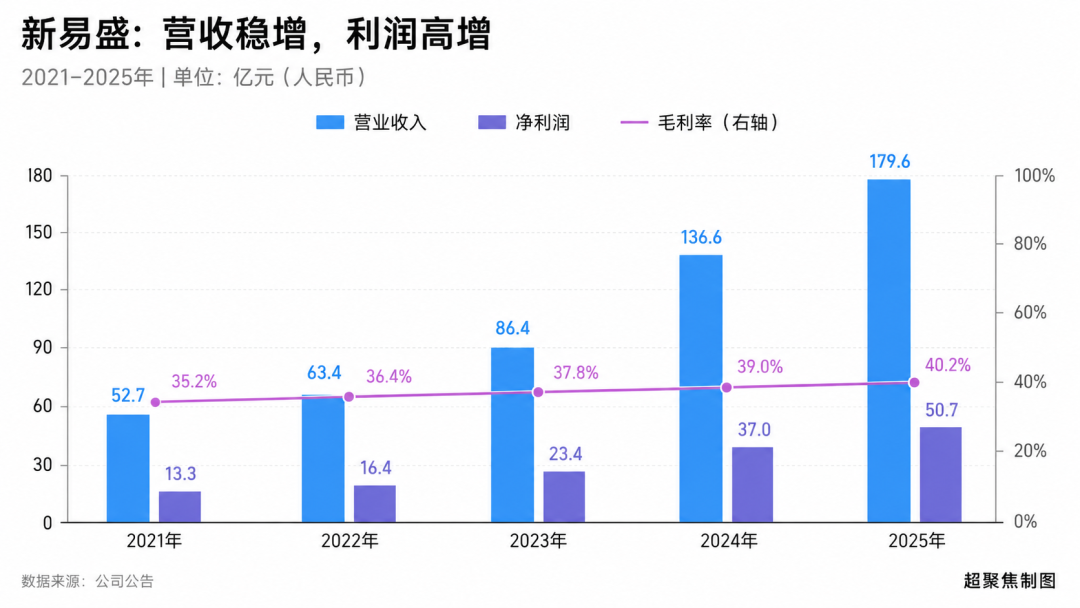

The same goes for YOFC: Revenue grew from RMB 5.27 billion to RMB 17.96 billion, net profit from RMB 1.33 billion to RMB 5.07 billion, and gross margin from 35.2% to 40.2%.

But these are all in the past. The market doesn't pay for 'excellence that has already happened.' It's willing to pay for 'excellence that continues to exceed expectations in the future.'

This is the biggest difference between Zhongji Innolight and its peers and SK Hynix.

SK Hynix's rise was more like the market suddenly discovering an undervalued AI play. For Zhongji Innolight and its peers this time, the market already knows they are good plays. Now, it's betting on whether they can continue to draw winning hands.

So, buying them now is no longer a gamble on 'whether optical modules are a good track ( track means 'track' or 'sector' in Chinese, often used metaphorically for investment opportunities).' Instead, it's betting on whether variables like AI CapEx, 1.6T volume growth, North American orders, and gross margins can continue to surprise the market.

Precisely because of this, they are being turned into AI lotteries by Wall Street: Their fundamentals are strong enough to convince people this isn't just a concept; their prices are high enough to accommodate more imagination; and their volatility is large enough to make people willing to pay for double leverage.

So, China's SK Hynix may not have arrived yet. But China's AI hardware 'lottery' might truly be on its way.

- END -

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?

-

![]()

DeepSeek's Financing Details Revealed! How Liang Wenfeng Secured Control

-

![]()

Valued at 210 Billion Yuan, Generating 42 Billion Yuan in Annual Revenue, Xiaohongshu May Proceed with IPO

-

![]()

Three Straight Months of Growth in Heavy Truck Sales: Both New and Veteran Players Are on the Same Wavelength!

-

![]()

AI Rewrites the Logic of Going Global: Cross-border E-commerce Reaches a New Turning Point

-

![]()

DeepSeek Secures Over 50 Billion Yuan in Initial Funding Round: Tencent and CATL Among Investors

-

![]()

Trillionaire Musk