Trillionaire Musk

06/17 2026

06/17 2026

427

427

If you win a lottery jackpot of 100 million yuan every day, you would need to win consecutively for 246 years to catch up with Musk.

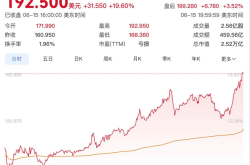

On June 16, 2026, a milestone moment in human wealth history will arrive.

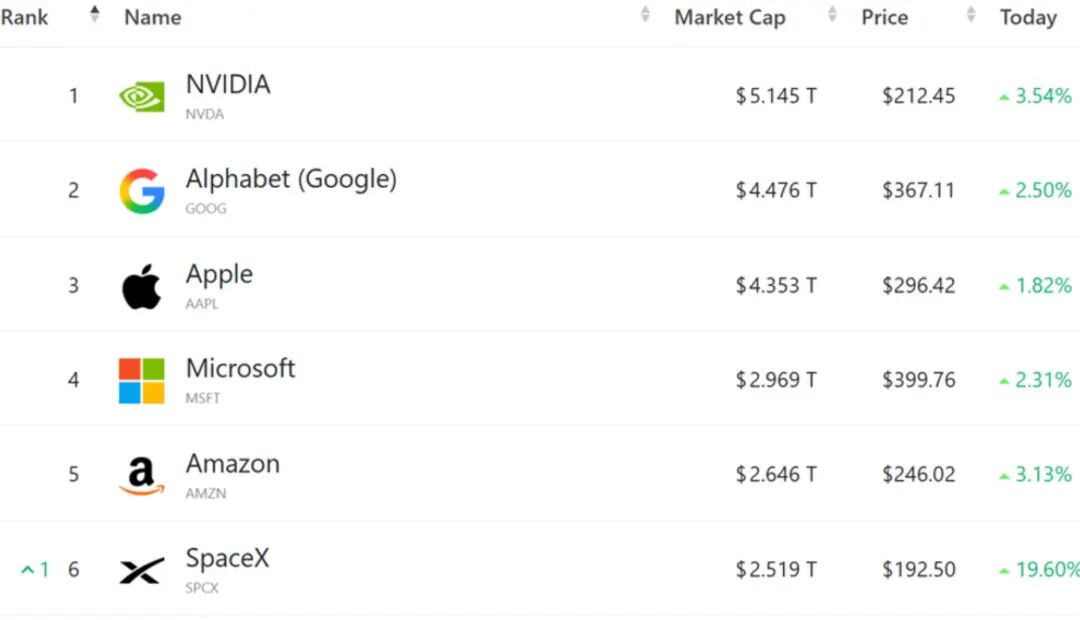

With SpaceX's cumulative two-day gain exceeding 42% following its Nasdaq listing, its market capitalization soared to $2.1 trillion, propelling Elon Musk's personal net worth past $1.3 trillion (exceeding RMB 9 trillion) and officially making him the first trillionaire in human history.

Looking at the global rich list, his net worth far surpasses that of Larry Page, the second-richest person and co-founder of Google, by $301.4 billion. It is equivalent to the combined wealth of 8.8 Warren Buffetts and even surpasses the combined net worth of the world's second to sixth richest individuals.

RMB 9 trillion—a figure that may be abstract to many. Written in Arabic numerals, it looks like this: '9,000,000,000,000.' Count the zeros? There are 12 after the '9.'

To put it in a somewhat inappropriate analogy: if you won a lottery jackpot of 100 million yuan every day, you would need to win consecutively for 246 years. If the jackpot were smaller, say 10 million yuan daily, you would need to keep winning for 2,460 years—meaning you would have had to start 200 years before Qin Shi Huang unified the six states; otherwise, you would still be too late.

If you laid out $1 trillion worth of $100 bills end-to-end to form a 'road of cash,' its length would be more than four times the distance from Earth to the Moon, allowing for two round trips.

According to 2025 data from the International Monetary Fund (IMF), only 20 countries and regions worldwide have a GDP reaching or exceeding $1 trillion annually. This means Musk's personal wealth exceeds the annual economic output of nearly 90% of the world's countries or regions.

It's that exaggerated.

Musk's $1.3 trillion net worth primarily consists of three parts: First, SpaceX stock holdings contribute approximately $720 billion, accounting for over 55% and serving as the core driver of his trillion-dollar net worth. Second, Tesla stock holdings contribute about $410 billion, making up 31% and remaining his second-largest wealth pillar. Third, stakes in X Platform, humanoid robot Optimus, and artificial intelligence startups total approximately $170 billion, accounting for 14% and representing the core of future wealth growth.

From an industry perspective, Tesla has never been just a car company but rather the embodiment of Musk's entire ecosystem. Over the past decade, traditional automakers have followed the logic of 'earning manufacturing profits from car production': Toyota and Volkswagen have relied on large-scale vehicle production and sales to earn per-unit profit margins, with net profits consistently locked at 5%-8% of revenue and valuations anchored to three traditional metrics: sales volume, production capacity, and gross profit margin.

In contrast, Musk has completely stripped away the manufacturing attributes of automakers, redefining Tesla as a mobile intelligent terminal + AI data platform + energy ecosystem gateway.

To put it more simply, traditional automakers earn money by selling cars as products, while Musk earns money from ecosystems, data, and capital. The vehicle business serves as a cash flow generator, scenario enabler, and user data collector, while aerospace, AI, and social media businesses drive capital valuation growth. This bidirectional empowerment has created a unique trillion-dollar wealth model, which remains an insurmountable core barrier for all other automakers to replicate.

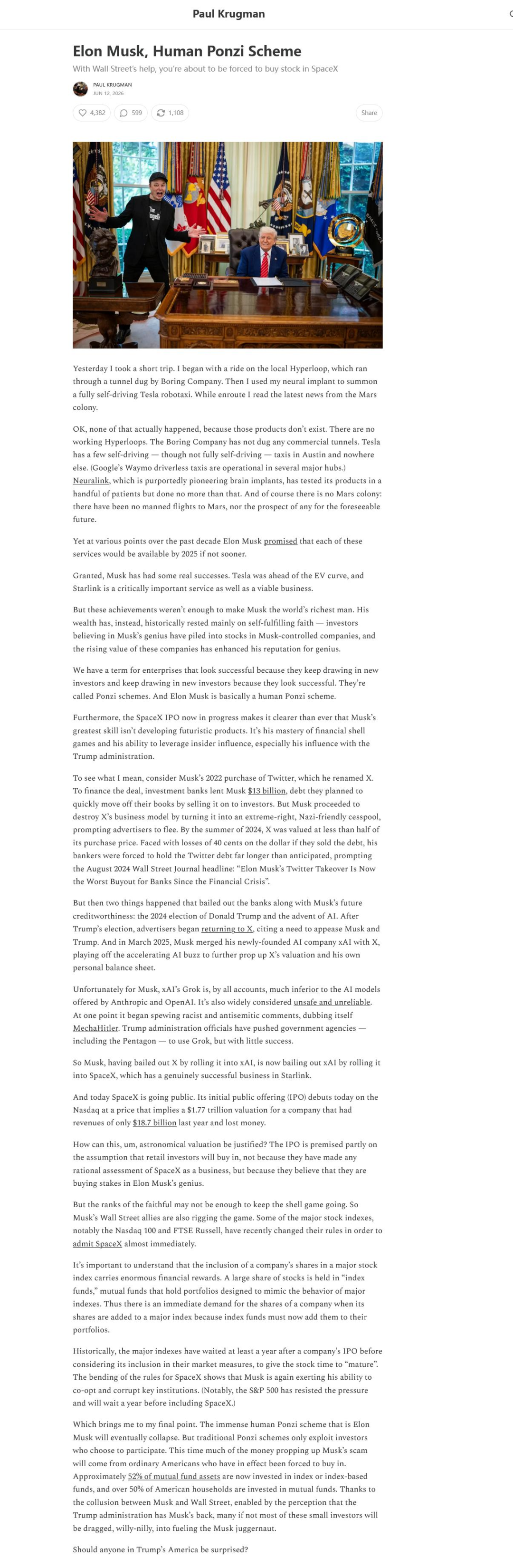

No wonder some still dislike Musk. While everyone was watching this capital extravaganza, Nobel laureate in economics Paul Krugman threw cold water on it, publishing a heavyweight article in his column titled 'Elon Musk: Humanity's Ponzi Scheme.'

Krugman bluntly stated that Musk is not developing future tech products but is instead manipulating financial capital operations and leveraging his government connections. 'SpaceX's IPO is entirely built on a Ponzi scheme. Retail investors are pouring money into SpaceX not because they have seriously evaluated the company's commercial value but because they blindly believe Musk is a genius. However, this capital game is not one retail investors can play until the end.'

After all, Musk still has many dreams yet to be realized, leaving him vulnerable to criticism.

The Hyperloop proposed in 2013 has yet to see any commercial operations; The Boring Company's tunnels have not built any commercial toll tunnel networks, with some test sections being mocked as 'expensive parking lots'; Full Self-Driving (FSD) has missed promises for nearly a decade, with 'fully autonomous cross-country travel in the U.S.' still unfulfilled; Neuralink has only been tested on a few patients; and a Mars colony remains a fantasy...

In Krugman's eyes, Musk might just be the American version of Li Hongzhang.

If we talk about winning, Musk has truly won through his model. In the first quarter of 2026, Tesla delivered 358,000 vehicles, falling short of market expectations, and its vehicle business growth has entered a stable phase. However, Tesla's market capitalization remains firmly above the $2 trillion mark, maintaining its position as the world's most valuable automaker.

The core reason capital markets assign a premium to Tesla is no longer vehicle sales volume but rather the commercialization progress of FSD's full self-driving capabilities, the energy closed loop (closed-loop energy system) of Gigafactories, and the deployment capability of Robotaxi autonomous taxis. Tesla's $20 billion in capital expenditures for 2026 will see over 70% allocated to AI computing power, autonomous driving iteration, and robotics research, while R&D investment in new vehicle models continues to shrink.

To some extent, capital markets now judge an automaker's value based solely on its self-developed autonomous driving capabilities and deployment speed. In contrast, global automakers focusing on hardware manufacturing and outsourcing autonomous driving solutions continue to see their valuations decline, even if they sell over a million vehicles annually. Building cars is no longer about manufacturing capabilities but about AI evolution capabilities.

Among the top 10 global automakers by market capitalization in 2026, only Tesla has achieved cross-industry layout (layout); the rest remain confined to the mobility sector, with their combined market caps falling short of Tesla's alone. The capital market's choice is clear.

This has also given hope to domestic new energy vehicle startups that have struggled to turn a profit, showing them that there's another way to play the game.

Li Xiang announced at the end of 2024 that Li Auto would transition to AI, and at an internal meeting earlier this year, he emphasized the urgency of this transformation. Li Xiang himself stated that this year represents the last 'boarding opportunity' to become a leading AI enterprise.

He Xiaopeng, Tesla's biggest fan, announced at this year's global product launch event: '2026 will be a critical year for XPeng's commercialization of physical AI.' AI will become the core engine driving growth in automotive, robotics, and other businesses. Compared to Musk, he has simply replaced the overly ambitious rockets with flying cars, a field others avoid.

On June 5, 2026, at Qualcomm's Automotive Technology and Collaboration Summit, NIO founder William Li bluntly stated: 'Today's automotive companies must become AI companies, and today's smart cockpits must become AI cockpits.'

Seeing so many automakers eager to learn from Musk, as if adopting the strategy of 'learning from the enemy to defeat them,' it's necessary to throw some cold water.

Musk's trillion-dollar net worth is the result of mature U.S. capital markets, Silicon Valley's tech innovation ecosystem, global market reach, and years of technological accumulation—not solely from product layout (layout).

When it comes to layout (layout) capabilities, Jia Yueting in China is second to none. However, domestic automakers operate in entirely different geopolitical capital environments, industrial policies, and user demands. Blindly replicating Musk's ecosystem-based automotive model, detached from local supply chains and user needs, will only lead to strategic missteps.

Moreover, the tech valuation bubble is detached from the fundamentals of automotive manufacturing, and the industry's tolerance for error is rapidly decreasing. If Tesla faces regulatory hurdles for global FSD deployment, if Robotaxi commercialization falls short of expectations, or if space project R&D overruns occur, valuations of Musk's companies will also quickly correct.

Qi Baishi famously said, 'Those who learn from me thrive; those who imitate me perish.' As Tesla's apprentices, most new energy vehicle startups began by disassembling a Tesla.

Among these diligent students, who will become the next Xu Linlu?

Note: Some images are sourced from the internet. If there is any infringement, please contact us for removal.

-END-

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?

-

![]()

DeepSeek's Financing Details Revealed! How Liang Wenfeng Secured Control

-

![]()

Valued at 210 Billion Yuan, Generating 42 Billion Yuan in Annual Revenue, Xiaohongshu May Proceed with IPO

-

![]()

Three Straight Months of Growth in Heavy Truck Sales: Both New and Veteran Players Are on the Same Wavelength!

-

![]()

AI Rewrites the Logic of Going Global: Cross-border E-commerce Reaches a New Turning Point

-

![]()

DeepSeek Secures Over 50 Billion Yuan in Initial Funding Round: Tencent and CATL Among Investors

-

![]()

Trillionaire Musk