Visual China's Hong Kong IPO: 700 Million Content Assets Brace for AI Era, Sheds 145 Key Accounts in Two Years

06/16 2026

06/16 2026

571

571

Unveiling Business Essence, Delving into Corporate Core

Author | Yang Cheng

On June 14, Visual (China) Culture Development Co., Ltd. (hereinafter referred to as "Visual China", 000681.SZ) submitted its application for listing on the Hong Kong Stock Exchange. Amidst the fierce competition in AI large models, Visual China's image copyright business is encountering formidable challenges.

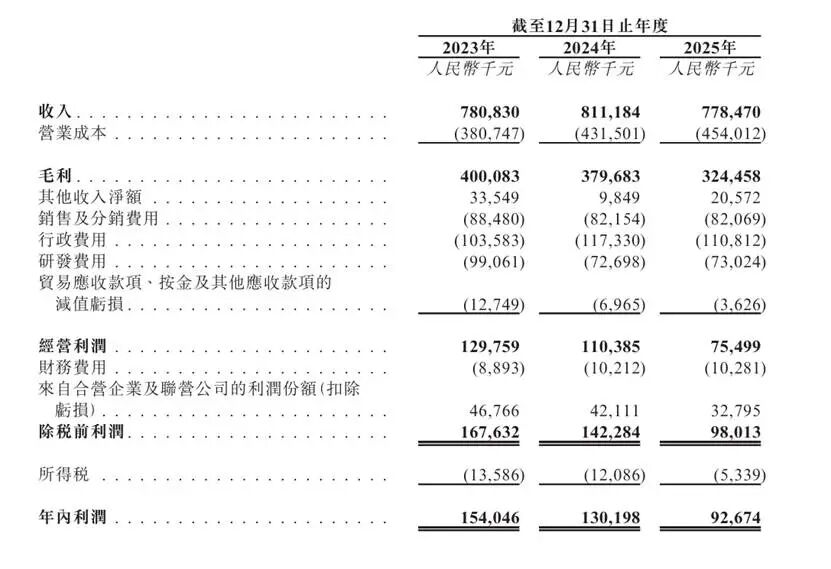

In 2025, Visual China reported a revenue of 778 million yuan, marking a 4.1% year-on-year decrease; its net profit also declined by 28.5% year-on-year to 93 million yuan. Business pressure is also evident on the client front.

From 2023 to 2025, the number of key accounts (KA clients, referring to clients with an annual consumption of 100,000 yuan or more) for Visual China's content licensing services dwindled from 776 to 631, with the customer retention rate dropping from 83.0% to 77.6%.

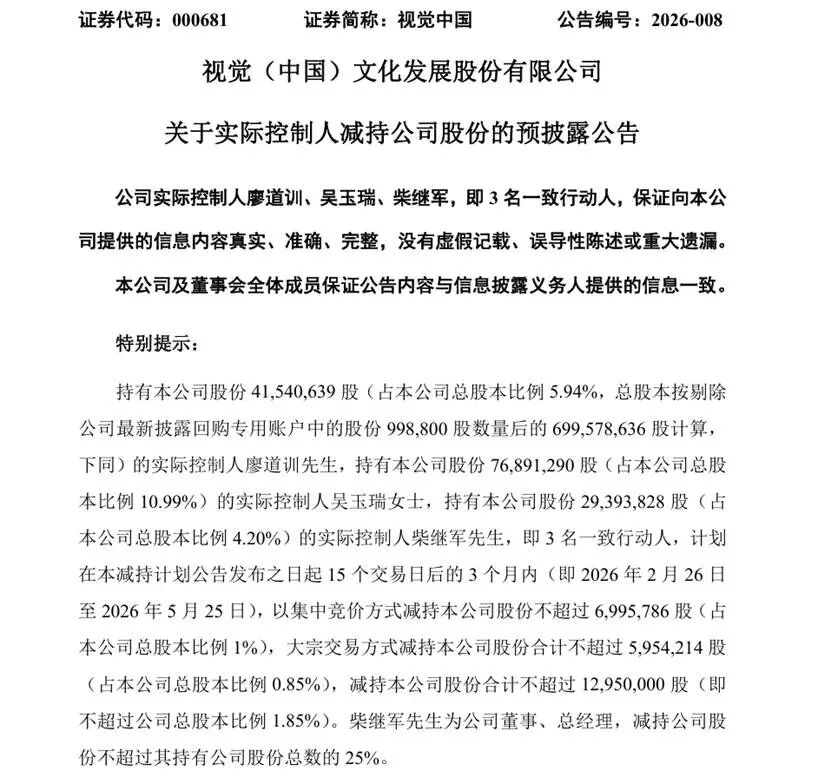

In response to industry transformations, Visual China has consistently underscored its AI strategy in recent years, viewing it as a future growth avenue. However, during this pivotal transformation phase, the company's actual controllers, Liao Daoxun, Wu Yurui, and Chai Jijun, initiated a share reduction plan in January 2026.

Meanwhile, Visual China's R&D expenditure has not witnessed a significant uptick. In 2025, R&D spending amounted to only 73.02 million yuan, a decrease of 26 million yuan from 99.06 million yuan in 2023.

01 Revenue Reverts to Two-Year Low

Established in 2000 and listed on the Shenzhen Stock Exchange in 2014, Visual China stands as a leading provider of visual content copyright trading and creative customization services in China. By integrating images, videos, audio, and other content, it caters to news media, brand companies, and internet enterprises.

According to the prospectus, from 2014 to 2025, Visual China amassed a cumulative total of over 400,000 paying clients and disbursed 3.1 billion yuan in royalties to content providers. By the end of 2025, the company boasted over 700 million content pieces and more than 800,000 contracted contributors.

In terms of operational performance, Visual China has faced substantial growth pressures in recent years. In 2025, the company's revenue reverted to the level of two years prior, with net profit decreasing by approximately 37 million yuan during the same period, a drop of about 28.5%.

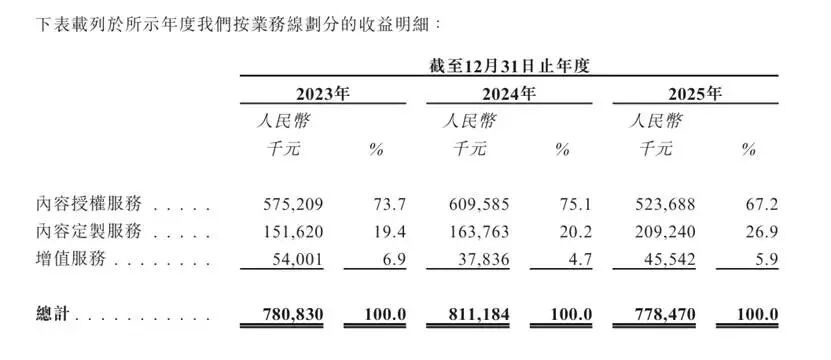

From 2023 to 2025, Visual China's revenue stood at approximately 781 million yuan, 811 million yuan, and 778 million yuan, respectively; net profit was approximately 154 million yuan, 130 million yuan, and 93 million yuan, respectively. Visual China's operating business is segmented into three areas: content licensing services, content customization services, and value-added services.

Among these, content licensing services have long constituted more than half of the company's total revenue. However, revenue from content licensing services decreased by 14.1% from 610 million yuan in 2024 to 524 million yuan in 2025, contributing significantly to the overall decline in Visual China's revenue.

Meanwhile, Visual China has witnessed a steady decline in the number of KA clients in recent years, with customer retention rates also looking bleak. From 2023 to 2025, the number of KA clients for Visual China's content licensing services was 776, 724, and 631, respectively; customer retention rates were 83.0%, 80.2%, and 77.6%, respectively.

In response, Visual China attributed the decline in content licensing services revenue to clients tightening their marketing budgets. Concurrently, the rapid advancement of AI technology has also revolutionized content procurement and consumption models within the industry.

Contrary to the decline in content licensing services, revenue from content customization services has surged. From 2023 to 2025, content customization services contributed revenue of 151 million yuan, 164 million yuan, and 209 million yuan, respectively, accounting for 19.4%, 20.2%, and 26.9% of the total revenue in the same year.

However, the revenue growth from content customization services has not translated into a simultaneous boost in profitability. From 2023 to 2025, the gross profit margins for content customization services were 18.2%, 15.1%, and 16.4%, respectively. Although the gross profit margin rebounded in 2025, it remained below the 2023 level.

With the rising proportion of low-margin content customization business, Visual China's overall profitability is also under duress. The company's overall gross profit margin decreased from 51.2% in 2023 to 46.8% in 2024 and further to 41.7% in 2025.

02 Behind the AI Facade: Controlling Shareholders' Share Reduction, Inadequate R&D Investment

In recent years, the swift evolution of AI technology is reshaping the visual content industry. Presently, with the backing of large models like GPT, Doubao, and Qianwen, users can generate images and even dynamic videos by simply inputting text descriptions, posing fresh challenges to the traditional image copyright business.

Faced with industry upheavals, Visual China has persistently highlighted its AI strategy in recent years. Company President Chai Jijun has also publicly alluded to the industry opportunities brought by AIGC (Artificial Intelligence Generated Content) on multiple occasions. However, just as Visual China is weaving its AI transformation narrative, the company's actual controllers have embarked on a share reduction plan.

On January 28, 2026, Visual China announced that three major shareholders, Liao Daoxun, Wu Yurui, and Chai Jijun, planned to reduce their stakes in the company by a total of no more than 12.95 million shares over the next three months, accounting for 1.85% of the company's total share capital.

Based on Visual China's closing price of 28.01 yuan on January 27, the total value of the share reduction by Liao Daoxun, Wu Yurui, and Chai Jijun is approximately 363 million yuan. It is noteworthy that while Visual China is fervently promoting its AI transformation story, R&D investment has not exhibited a significant upward trend.

From 2023 to 2025, the company's R&D expenditure was 99.06 million yuan, 72.70 million yuan, and 73.02 million yuan, respectively. Not only has R&D spending not increased, but it also decreased by approximately 26 million yuan in 2025 compared to 2023.

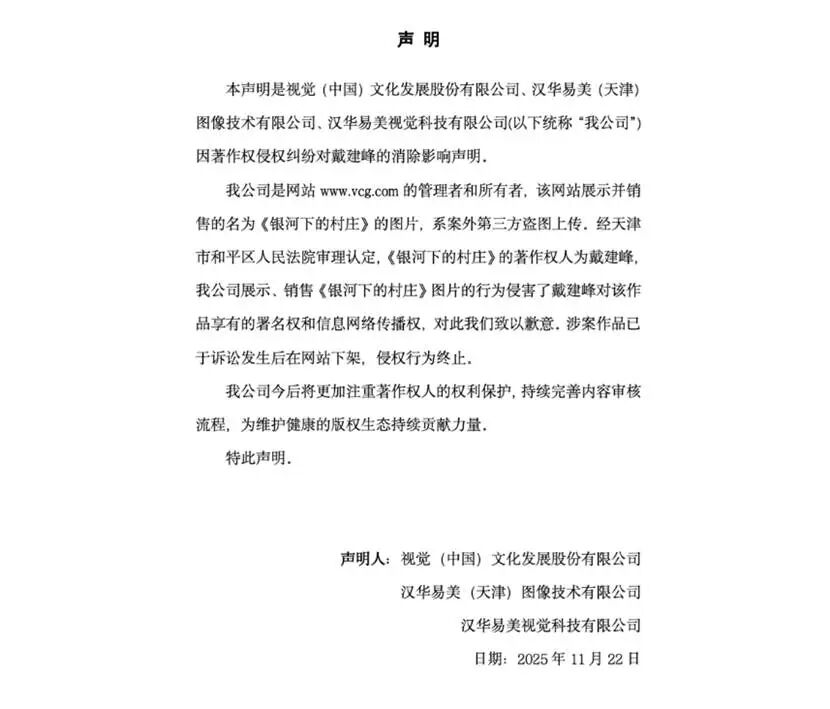

Moreover, Visual China's copyright assets, which it considers its core competitive edge, have also been embroiled in ownership controversies in recent years. In 2023, renowned astrophotographer Dai Jianfeng revealed that he had received calls and emails from Visual China, alleging that his official account "Jeff's Starry Sky Journey" had infringed upon 173 images owned by Visual China and demanding compensation exceeding 80,000 yuan. However, the so-called "infringing photos" provided by Visual China were, in fact, his own creations.

Subsequently, Dai Jianfeng filed a lawsuit against Visual China for selling his works without authorization and demanding compensation. In November 2025, the court's first-instance judgment indicated that after acquiring Dai Jianfeng's work "Village Under the Milky Way" through a third party, Visual China and related companies commercially sold it on their official website without obtaining the corresponding copyright authorization, infringing upon Dai Jianfeng's right of information network dissemination and right of attribution. They were jointly and severally liable to pay 15,000 yuan in compensation and issue a public apology.

Furthermore, the court determined that Visual China's prior demand for compensation exceeding 80,000 yuan from Dai Jianfeng on grounds of infringement was clearly inappropriate and that the company had failed to fulfill its necessary ownership review obligations. Now, Visual China's traditional copyright business is under strain, and the growth in the scale of content customization services has not translated into increased profits. The share reduction by the actual controllers and fluctuations in R&D investment have also prompted the market to reassess the true nature of the company's AI transformation.

END

The images in this article are sourced from the internet.

-

![]()

Seres: 'Xiao Sai' Humanoid Robot Makes Official Debut! Will It Give Stock Prices a Lift?

-

"Copper Foil Magnate" Capitalizes on AI Boom: Leading CCL Company Sees Market Value Soar by HK$220 Billion in Six Months

-

![]()

Why Are Convolutional Neural Networks and Transformer Architectures Unfit for Embodied AI?

-

Bethel's Q1 Revenue Growth Decelerates, Profits Turn Negative: Chery-Related Deals Contribute 40%, Gross Margin Feels the Squeeze

-

![]()

A Strong Start Gone Awry: FAW Toyota, Once Ahead, Now Struggles to Keep Pace

-

![]()

Wang Chuanfu: Chinese Automobiles Will Surely Reach the Top of the World! BYD Will Become the World's Number One by 2030!

-

![]()

The Soaring Price of Automotive-Grade Memory Chips: Is AI the Culprit?

-

Leapmotor’s Rise: Triumph Amidst Turmoil