MLCC: Igniting a Multi-Billion Supply Chain Battle | Golden Eye

06/17 2026

06/17 2026

435

435

In April 2026, Murata, Samsung Electro-Mechanics, and Taiyo Yuden successively announced MLCC price hikes. Murata raised prices for AI server and high-end automotive-grade products by 15%-35%, with Samsung Electro-Mechanics following closely with double-digit percentage increases.

Simultaneously, China's Ministry of Commerce added TDK, Mitsubishi Materials, and other Japanese companies to its export control watchlist, implementing near-zero clearance for Japanese heavy rare earths (yttrium oxide, dysprosium oxide, terbium oxide, etc.).

These two events, seemingly independent, point to the same supply chain bottleneck: MLCC.

01 Why is MLCC called the 'Rice of the Electronics Industry'?

MLCC, or Multilayer Ceramic Chip Capacitor, may sound complex, but it's ubiquitous in every electronic product around you.

It's on your phone's motherboard, in power modules, essential for the three electric systems of new energy vehicles, and densely packed on AI server computing boards. Its role is simple: voltage stabilization, filtering, energy storage, and noise reduction. But its usage is enormous—trillions consumed globally annually, with single-unit prices ranging from cents to a few dollars. Like rice, individually insignificant but indispensable in aggregate.

The core raw material for MLCC is ceramic dielectric powder. The purity, particle size, stability, and crystal structure of the powder directly determine the capacitor's performance ceiling. This field has long been dominated by a few players: Japan's Sakai Chemical, U.S.-based Ferro, and Japan's Murata monopolize global high-end MLCC powder, with downstream customers also being Murata, Samsung Electro-Mechanics, TDK, and other Japanese-Korean giants.

Barriers extend beyond technology. Lengthy validation cycles, numerous patent restrictions, and stringent process requirements have kept domestic powder manufacturers confined to mid-to-low-end markets, eyeing high-end shares but unable to seize them.

However, since 2026, three forces have simultaneously disrupted this stalemate.

02 Export Controls, AI Boom, and New Energy Vehicle Supply-Demand Shifts

The first tailwind comes from policy.

In January 2026, the Ministry of Commerce issued the 'Announcement on Strengthening Export Controls of Dual-Use Items to Japan.' In February, it added TDK, Mitsubishi Materials, and other Japanese MLCC and powder companies to its export control watchlist, implementing near-zero clearance for Japanese heavy rare earths—yttrium oxide, dysprosium oxide, and terbium oxide.

Yttrium oxide is the primary dopant for MLCC powder, while dysprosium and terbium are essential additives for automotive-grade and AI high-voltage MLCCs. Japanese MLCC powder manufacturers now face supply disruptions and dwindling inventories. Chinese powder makers, previously competing on cost, now gain an edge in 'supply security'—a scarcity amplified by AI's historical opportunity.

The second tailwind comes from AI computing power.

NVIDIA's Rubin platform began mass production in March 2026. AI servers consume far more MLCCs than traditional servers.

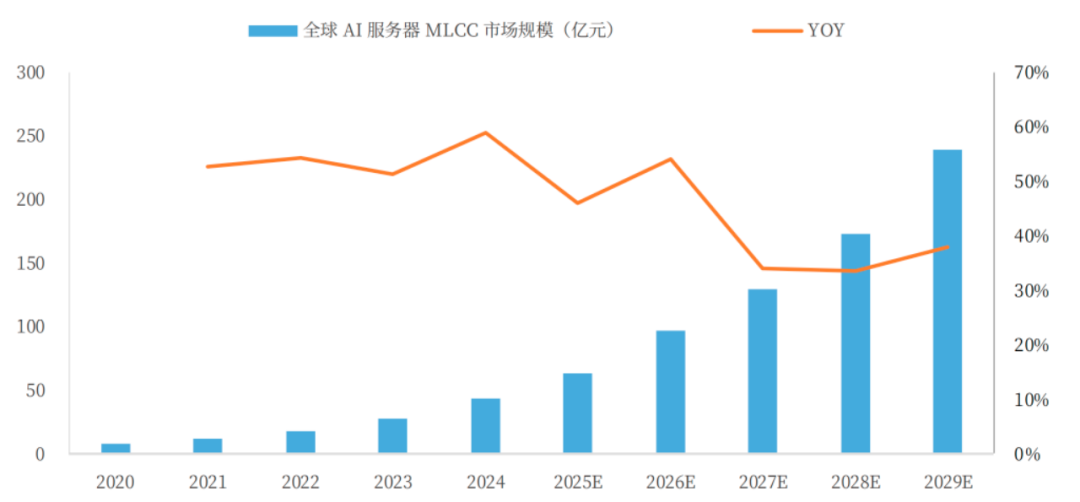

Frost & Sullivan data provides precise comparisons: An 8-card AI training server uses about 48,000 MLCCs per unit, while a flagship full-rack AI server exceeds 440,000 per unit—over nine times that of ordinary servers.

Murata projects AI server MLCC demand to grow 30% annually from 2025 to 2030, reaching 3.3 times 2025 levels by 2030. The global AI server MLCC market expanded from 760 million yuan in 2020 to 4.31 billion yuan in 2024, with projections hitting 23.91 billion yuan by 2029, a 39.6% CAGR.

Source: Weirong Technology Prospectus, Frost & Sullivan

AI demands more than just volume from MLCCs. High capacitance, high voltage, high temperature resistance, and small size—four high-end metrics simultaneously pressure powder quality. To meet premium capacity, Japanese manufacturers are converting mid-to-low-end production lines to high-end, tightening mid-to-low-end supply. The market now faces 'high-end shortages and low-end tight balance.'

The third tailwind comes from new energy vehicles.

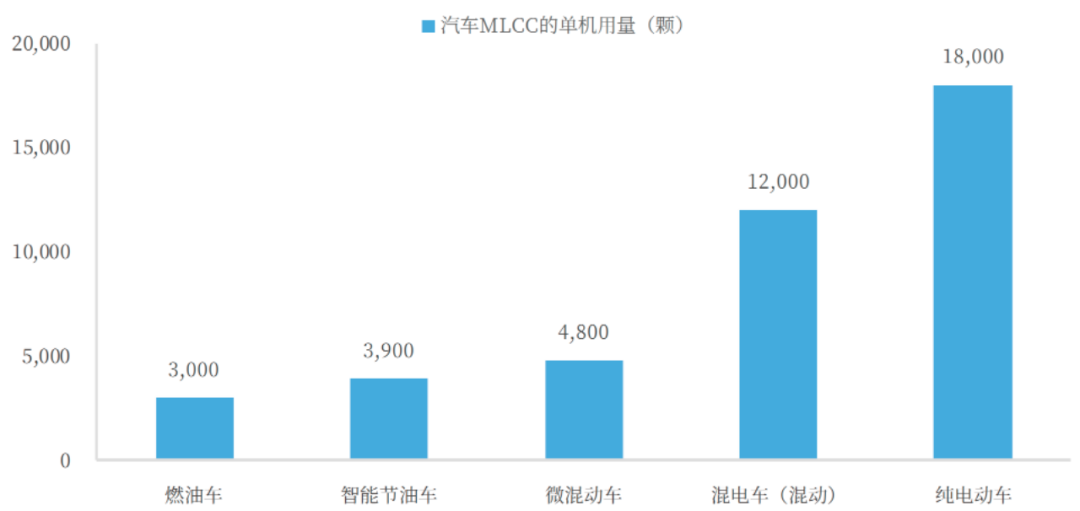

A gasoline vehicle uses about 3,000 MLCCs on average. A pure electric vehicle (EV) uses 18,000—six times more.

Weirong Technology's prospectus reveals: Hybrid vehicles, with added high-voltage battery management systems and dual-motor drive controls, use about 12,000 MLCCs per unit—four times that of gasoline vehicles. Pure EVs, with fully deployed 'three electric systems,' push usage to 18,000 per unit.

Source: Weirong Technology Prospectus

Murata predicts vehicles equipped with L2+ advanced driving assistance systems will grow 2.8-fold by fiscal 2027. Every percentage point increase in smart driving penetration elevates demand for high-quality, high-performance MLCCs.

According to Dataintelo, the global MLCC market is expected to grow from $14.8 billion in 2025 to $28.6 billion in 2034, a 7.6% CAGR.

With these three tailwinds converging, the supply-demand balance has tipped decisively.

03 Price Hikes and Shortages: A Tight Balance Unfolding

In February 2026, Murata executives revealed MLCC order inquiries were double current capacity, prompting price hike evaluations. By late March, they announced across-the-board price increases for AI server and high-end automotive-grade MLCCs, effective April 1, with raises of 15%-35%.

Samsung Electro-Mechanics followed suit in April with double-digit percentage hikes, joined by Taiyo Yuden.

TrendForce data paints a tense picture: From February to April 2026, MLCC suppliers' capacity utilization rates rose steadily, with the overall order-to-shipment ratio climbing from 0.89 in March to 0.92 in April. Murata, Samsung Electro-Mechanics, and Taiyo Yuden maintained order-to-shipment ratios above 1, indicating new orders exceeded shipping capacity.

Wind data confirms industry prosperity: Seven of ten MLCC concept stocks reported Q1 net profit growth. Three-Ring Group posted Q1 revenue of 2.681 billion yuan (+46.25% YoY) and net profit of 791 million yuan (+48.48% YoY), attributing growth to increased MLCC customer recognition.

Why can't supply keep up? The key lies in 'stacking' technology.

To achieve greater capacitance in limited volumes, manufacturers stack ceramic dielectric films and metal electrodes layer by layer. Higher stack counts exponentially increase technical difficulty. Leading domestic player Weirong Technology has achieved over 1,200-layer stacking, delivering 100µF and 220µF ultra-high capacitance in 0805 and 1206 sizes, respectively—a first for mainland manufacturers.

However, high-end MLCC yield rates are far lower than standard products, consuming more capacity. Murata and Samsung Electro-Mechanics are now operating at full capacity, with limited new high-end capacity additions this year. Faced with surging AI demand, lead times for high-capacitance MLCCs are extending, potentially worsening supply-demand conflicts.

04 Domestic Substitution Poised for a Triple Leap

The global MLCC market is highly concentrated: Murata alone holds ~40% share, with Japanese and Korean firms dominating ~80% of the high-end segment. The materials market is similarly concentrated, with Japanese and U.S. companies controlling ~70% of high-end electronic ceramic materials.

But this pattern (landscape) is loosening.

Japanese giants are shifting capacity to AI and automotive high-end products, creating 'capacity crowding-out' in mid-to-low-end markets. Orders previously supplied by Murata and Samsung Electro-Mechanics are now flowing to Chinese manufacturers.

Domestic substitution is evolving through a 'triple leap':

Level 1: Mature consumer electronics replacement. Domestic MLCCs now fully replace imports in smartphones, wearables, etc. The 2025 'national subsidy' policy strongly supports consumer electronics demand, with the sector poised for continued rapid growth in 2026.

Level 2: Penetration into domestic automotive supply chains. As domestic new energy automakers prioritize supply chain security, domestic MLCCs are accelerating into core modules like BMS, electric drives, and controls.

Level 3: Breakthroughs in AI servers alongside domestic computing chains, achieving scale from 1 to N. This is the highest and toughest level, but current policy environments, supply gaps, and customer validation willingness present a historic window.

05 Key Players in the MLCC Supply Chain

Guoci Materials: A global leader in MLCC dielectric powder production, covering all types of base and formula powders. Clients include Samsung Electro-Mechanics, Yageo, Fenghua Advanced, and other top firms. Recently focused on AI server and automotive-grade MLCC powders, expanding high-end powder production. Its MLCC electronic paste business is also growing rapidly, developing high-capacitance, automotive-grade, and RF-specific pastes.

Three-Ring Group: A diversified player spanning alumina ceramic substrates, ceramic ferrules, crystal oscillator packages, MLCCs, and more. In 2024, it held 52% global market share in alumina ceramic substrates, 71% in ceramic ferrules/sleeves (No. 1 globally), 40% in crystal oscillator packages (No. 2 globally), and ranked 9th globally (1st domestically) in MLCCs with ~2.1% share. The company is actively breaking into high-end MLCCs, benefiting from this price hike cycle.

Fenghua Advanced: A domestic MLCC veteran with deep industry experience, forming a dual-mainforce with Three-Ring Group for high-end breakthroughs.

Weirong Technology: Specializes in miniaturized, high-capacitance, high-reliability MLCCs, currently in IPO process. It has achieved over 1,200-layer stacking, delivering 100µF industrial MLCCs in 0805 size—a mainland first. Products serve consumer electronics, AI servers, and automotive electronics.

Hongming Electronics: China's largest developer and manufacturer of specialty MLCCs for defense applications, also supplying consumer electronics brands like Apple and Lenovo while expanding into new energy vehicles.

Dali Kapu: A leader in RF microwave MLCCs, ranking 5th globally and 1st among Chinese firms in 2022. Its ceramic capacitor business accounted for 98.75% of revenue in 2025.

Wanwei High-Tech: Successfully developed multiple PVB resins (green temporary bonding carriers) for MLCCs, meeting foreign competitor technical standards. It leads Anhui Province's key R&D project 'MLCC Polyvinyl Butyral Resin Development,' advancing industrialization.

MLCC's nickname as the 'Rice of the Electronics Industry' stems not just from its vast usage and low unit price but also because it serves as the most authentic prosperity indicator in a mature industry.

Over the past three years, declining consumer electronics, mid-to-low-end powder price wars, high inventories, and low utilization rates plagued domestic manufacturers through a long winter.

In 2026, AI computing power and new energy vehicles hit the accelerator simultaneously. Export controls severed Japanese firms' rare earth supplies, price hikes validated supply gaps, and domestic substitution shifted from 'optional' to 'mandatory.'

This may mark a structural turning point.

For China's MLCC supply chain, the window is open. What follows tests powder purity, stacking precision, automotive certification, and mass production yield rates—these hard skills will determine who gets a seat at the table for this rice feast.

- END -

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?

-

![]()

DeepSeek's Financing Details Revealed! How Liang Wenfeng Secured Control

-

![]()

Valued at 210 Billion Yuan, Generating 42 Billion Yuan in Annual Revenue, Xiaohongshu May Proceed with IPO

-

![]()

Three Straight Months of Growth in Heavy Truck Sales: Both New and Veteran Players Are on the Same Wavelength!

-

![]()

AI Rewrites the Logic of Going Global: Cross-border E-commerce Reaches a New Turning Point

-

![]()

DeepSeek Secures Over 50 Billion Yuan in Initial Funding Round: Tencent and CATL Among Investors

-

![]()

Trillionaire Musk