Domestic GPU Company with Heavy Tencent Ties Clears Regulatory Hurdle, Shanghai State-Owned Assets Reap Bountiful Returns Once Again

06/17 2026

06/17 2026

550

550

On June 15, Shanghai Enflame Technology Co., Ltd. received the green light for its Initial Public Offering (IPO) at the listing committee meeting.

As the inaugural IPO contender on the STAR Market in 2026, Enflame Technology journeyed from acceptance on January 22 to approval in 145 days. While not the swiftest, it has successfully ridden the wave of hard-tech listings, emerging as another potential unicorn with a trillion-yuan market valuation.

With this milestone, the "Four Little Dragons" of China's domestic GPU industry—Moore Threads, MetaX, Biren Technology, and Enflame Technology—are poised to make their collective debut in the capital markets, marking a significant leap for China's domestic GPU sector into the "big leagues."

However, amidst the soaring performance, the issue of "heavy reliance on a single large customer" looms large.

1. Soaring Revenues, Half-Year Figures Set to Eclipse Last Year's Total

In the tech arena, falling behind means being left in the dust. But Enflame Technology shows no signs of slowing down. In the high-stakes race for AI computing power, Enflame Technology has delivered a stellar performance.

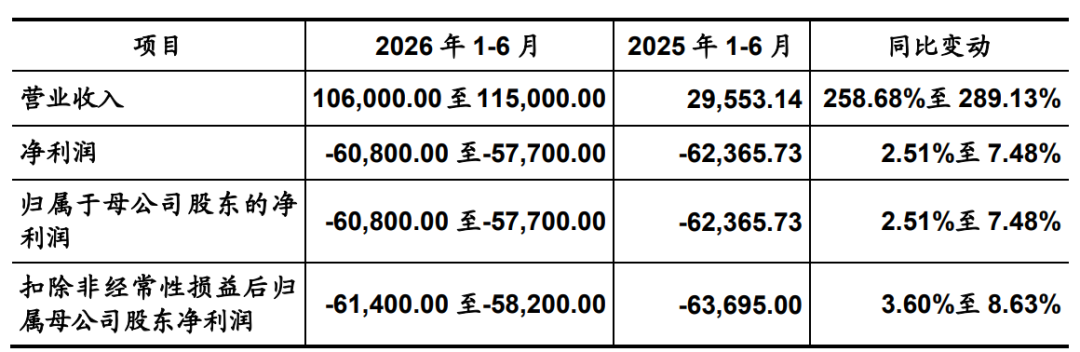

Prospectus data reveals that the company's revenue soared to 990 million yuan in 2025, with a Compound Annual Growth Rate (CAGR) of 81.32% from 2023 to 2025. The momentum continued into 2026, with the company projecting first-half revenue between 1.06 billion yuan and 1.15 billion yuan, skyrocketing by 258.68% to 289.13% compared to the same period last year.

Enflame Technology's revenue forecast for the first half of 2026. Chart source: Prospectus (the same below).

In essence, the company has surpassed its entire previous year's revenue in just six months. This is not merely a numerical feat but a direct reflection of the surging demand for domestic computing power from downstream internet behemoths.

Yet, the flip side of soaring revenues is persistent losses. In the first half of 2026, the company anticipates a net loss attributable to the parent company between 577 million yuan and 608 million yuan, with cumulative losses over three and a half years nearing 5 billion yuan.

The root causes of these massive losses are twofold:

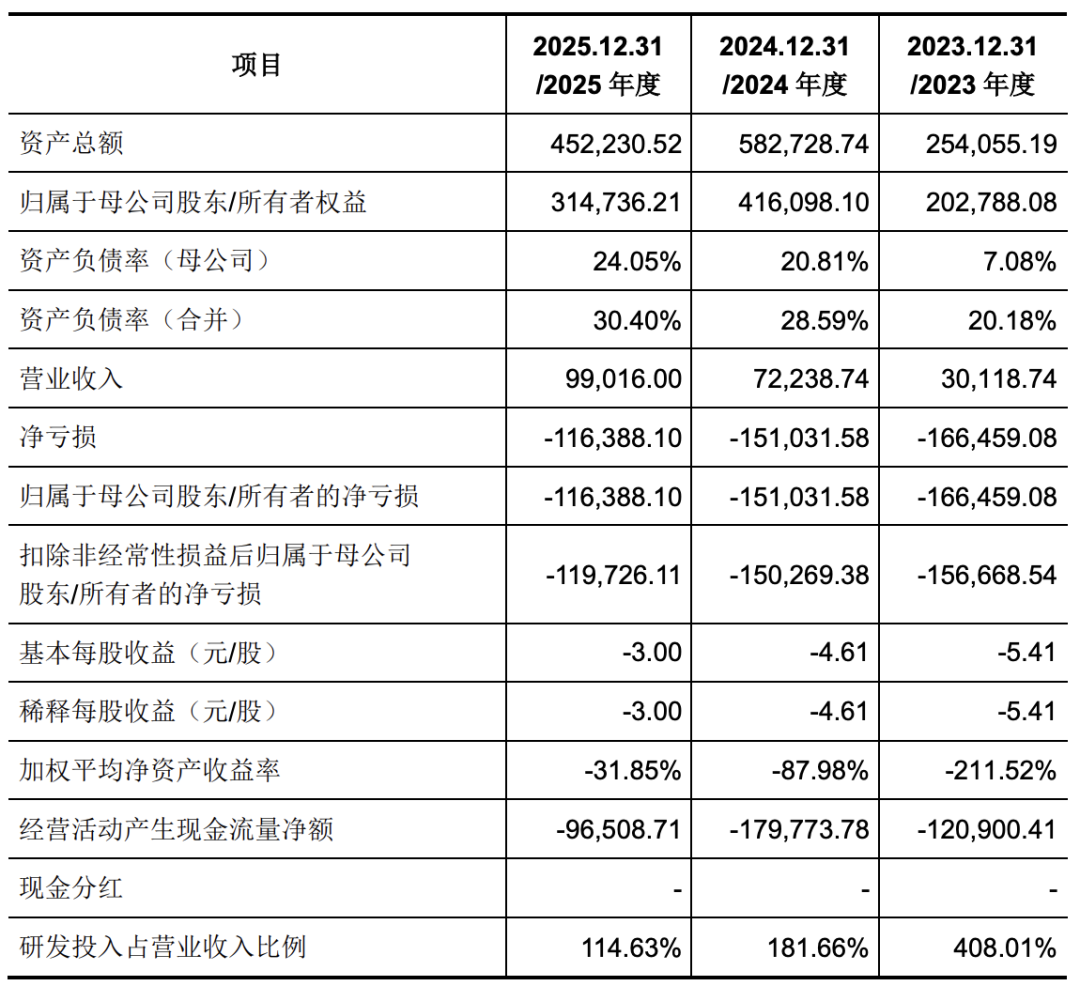

Firstly, "R&D is a costly endeavor." To keep pace with international giants, the company must maintain a high level of R&D investment. In 2023, R&D expenditure accounted for a staggering 408% of revenue, meaning the company spent 4 yuan on R&D for every 1 yuan earned. Even with a significant revenue increase in 2025, this ratio remained at 114%. Cumulative R&D investment over three years reached 3.676 billion yuan.

Secondly, "inventory and accounts receivable are draining cash flow and profits." As a fabless company, Enflame Technology does not need to build its own wafer fab. However, due to large-scale purchases and extended payment terms from downstream major customers, its inventory and accounts receivable have ballooned. Inventory surged to 863 million yuan by the end of 2025, with an overdue accounts receivable rate as high as 82.96%, leading to a cumulative operating cash outflow of nearly 4 billion yuan over three years. Moreover, significant provisions for inventory write-downs and bad debts have directly eroded net profits.

This "bleeding sprint" is essentially the price that domestic AI chips must pay during their breakthrough phase. For a hard-tech company that has not yet achieved full profitability, balancing "scaling up through burning cash" with "self-sustaining growth" is a real-world challenge it must confront.

2. Tencent: Major Shareholder and Key Customer

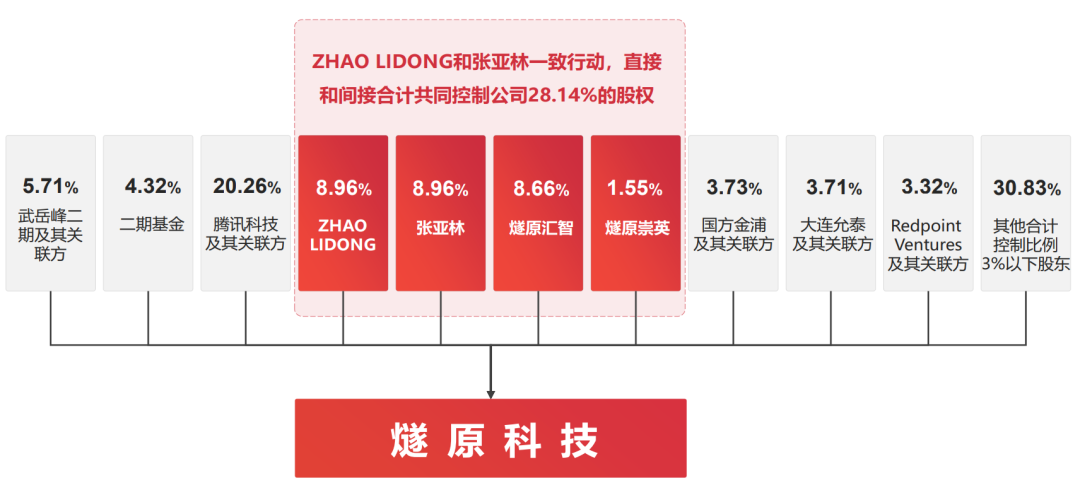

Among Enflame Technology's shareholders, Tencent stands out as a prominent figure.

Tencent Technology and its concerted action party, Suzhou Paiyi, collectively hold a 20.26% stake, making them the largest shareholder, with a stake percentage only slightly lower than the 28.14% collectively controlled by the two actual controllers.

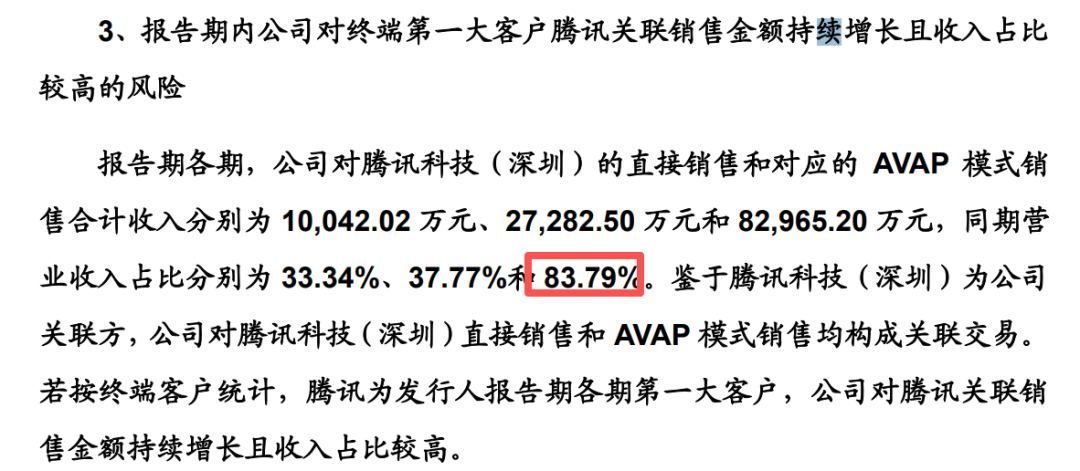

Tencent is not just the largest shareholder but also the driving force behind the company's performance growth. In 2025, direct sales and corresponding AVAP model sales to Tencent Technology (Shenzhen) accounted for a combined 83.79% of Enflame Technology's total. This deeply intertwined model of "being both the largest shareholder and the largest customer" has been instrumental in Enflame Technology's rapid growth in recent years but also represents its current biggest risk factor.

This "heavy reliance on a single large customer" is often viewed as a double-edged sword in the capital markets. On one hand, Tencent's endorsement signifies high technical recognition and market entry barriers; on the other hand, any adjustment in Tencent's procurement strategy or changes in their cooperation could lead to a precipitous drop in Enflame Technology's performance.

The market is more concerned about whether Enflame Technology can diversify its customer base beyond Tencent.

Notably, beyond Tencent, Shanghai's state-owned assets have been highly active. Institutions such as Shanghai Science and Technology Innovation Investment, Shanghai Integrated Circuit Industry Investment Fund, Shanghai International Group, and Pudong Venture Capital have participated in almost every funding round, now reaping the rewards of the IPO season.

Among the "Four Little Dragons" of domestic GPUs, except for Moore Threads, the other three have all been incubated and grown in Shanghai. As of June 2026, Shanghai boasts 95 listed companies on the STAR Market, ranking first in the country in terms of total initial public offering (IPO) funds raised and total market capitalization. This environment is fostering a batch of hard-tech IPOs.

3. The Gathering of the GPU "Four Little Dragons": The Battle for a Self-Developed Ecosystem

With Enflame Technology finally gaining access to the STAR Market, the "F4" of China's domestic GPU sector is complete.

However, the breakthrough strategies of these four companies differ significantly. Moore Threads, MetaX, and Biren Technology follow the GPGPU route, attempting to be compatible with NVIDIA's ecosystem. In contrast, Enflame Technology has chosen a more challenging path—developing its own ecosystem.

Not following the compatibility route means building everything from scratch. Enflame Technology has independently developed its instruction set, hardware architecture, and a full-stack software platform called "TopsRider." This is akin to forging a new path beside the towering mountain that is NVIDIA.

This path is arduous and solitary at first, but once successful, it becomes a formidable moat. Currently, Enflame Technology has iterated through four generations of architectures and launched five cloud-based AI chips, with a product matrix covering chips, acceleration cards, and intelligent computing clusters. Although currently primarily used for inference scenarios, its first combined training and inference product, the L600, is on the way and expected to enter mass production in the second half of the year.

Supporting this "difficult path" is the hardcore expertise of two "seasoned veterans."

The company was co-founded by Zhao Lidong and Zhang Yalin in 2018. Zhao Lidong holds a Bachelor's degree in Electronic Engineering from Tsinghua University and a Master's degree in Electronics and Computer Science from Utah State University in the United States. He worked in Silicon Valley for over 20 years, where he was responsible for core CPU/GPU/APU R&D at AMD and participated in the establishment of AMD's China R&D Center. Zhang Yalin, with a Bachelor's degree in Electronic Engineering from Fudan University, was one of the main leaders in global chip R&D at AMD and successfully led the mass production of multiple world-class chips.

A little-known detail is that when Zhang Yalin joined AMD in 2008, it was Zhao Lidong who interviewed him. After working together at AMD for many years, the two hit it off and transitioned from foreign enterprise colleagues to "Chinese partners," founding Enflame Technology in Zhangjiang, Shanghai, in 2018. The company's name symbolizes the idea that "a single spark can start a prairie fire."

This deep technical expertise and tacit understanding have endowed Enflame Technology with a pure "hard-tech" gene from its inception and provided the most solid talent and technological backing for its commitment to developing its own DSA architecture.

4. Conclusion

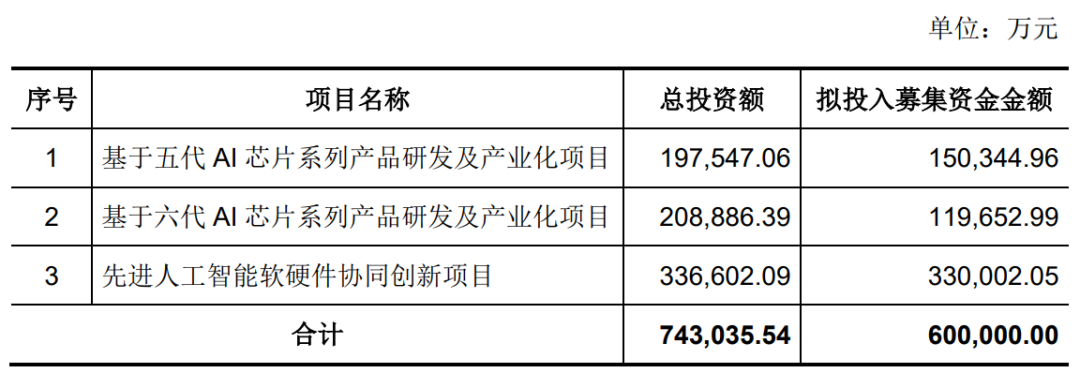

Enflame Technology plans to raise 6 billion yuan in this IPO, all of which will be invested in the R&D of fifth- and sixth-generation AI chips and related software and hardware.

For Enflame Technology, passing the regulatory review is not the finish line but the true starting point. In the brutal arena of AI computing power, high growth coexists with high losses, and customer dependency goes hand in hand with market expansion. In the future, it may not only face blockades from international giants but also need to address its own concerns about "relying on a single leg."

Can the prairie fire truly spread? Time will tell.

Deep Blue Finance New Media Cluster originated from the Deep Blue Finance Journalist Community and has a 15-year history. As a well-known domestic finance new media outlet, it focuses on China's most valuable companies, cutting-edge industry developments, and emerging regional economies, providing valuable content for investors, corporate executives, and the middle class. Welcome to follow.

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?

-

![]()

DeepSeek's Financing Details Revealed! How Liang Wenfeng Secured Control

-

![]()

Valued at 210 Billion Yuan, Generating 42 Billion Yuan in Annual Revenue, Xiaohongshu May Proceed with IPO

-

![]()

Three Straight Months of Growth in Heavy Truck Sales: Both New and Veteran Players Are on the Same Wavelength!

-

![]()

AI Rewrites the Logic of Going Global: Cross-border E-commerce Reaches a New Turning Point

-

![]()

DeepSeek Secures Over 50 Billion Yuan in Initial Funding Round: Tencent and CATL Among Investors

-

![]()

Trillionaire Musk