How Much Can Doubao Make by Charging Fees?

06/22 2026

06/22 2026

388

388

ByteDance Doesn't Rely on AI for Profit, But It Can Force Others to Keep Burning Money

Before Doubao even started charging, ByteDance internally raised its "value" once.

In April this year, ByteDance initiated its first buyback of "Doubao shares" at a price of $13.08, a 30.8% increase from the previous grant price of $10. Just two months later, on June 17, according to the Kechuangban Daily, ByteDance adjusted the price of "Doubao shares" again, raising the buyback price to $14.85, a 13.5% increase in two months.

Notably, during the same period, ByteDance's overall option buyback price increased from $229.5 in April to $235.5 in June, a mere 2.63% rise, far less dramatic than the increase in Doubao shares.

Coincidentally, as the price of Doubao shares rose again, the paid version of Doubao was about to debut. Previously, the Doubao App Store page displayed three subscription tiers: Standard at 68 RMB/month, Enhanced at 200 RMB/month, and Professional at 500 RMB/month, with annual fees of 688 RMB, 2048 RMB, and 5088 RMB, respectively.

With internal price hikes for Doubao shares and external preparations to charge for Doubao, is ByteDance finally looking to profit from Doubao?

The answer might be the opposite. Charging for Doubao is not about making money from AI but about breaking free from the old order of user acquisition and dragging the industry into its new paid rules.

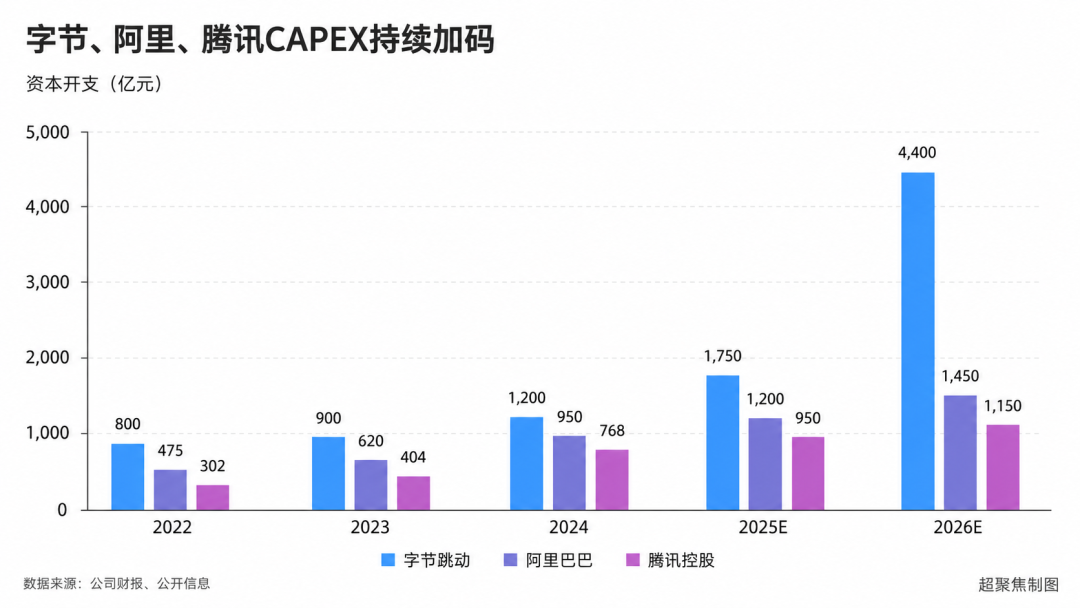

01 ByteDance Has No Shortage of Funds

When news of Doubao charging fees first surfaced, many believed ByteDance's investment strategy in AI would change. However, its actions in the first half of the year indicate that ByteDance is far from short on funds for AI investment.

In January this year, Reuters reported that ByteDance's planned capital expenditures for 2025 exceeded 150 billion RMB, with most allocated to AI. About half would be spent on overseas AI infrastructure, while domestic AI investments would focus on data centers and network equipment, with suppliers including Huawei, Cambrian, and NVIDIA.

Soon after, the South China Morning Post revealed that ByteDance had increased its AI infrastructure spending plan for 2026 by 25%, raising it from the previously budgeted 160 billion RMB at the end of last year to 200 billion RMB.

By May, Bloomberg, citing insiders, reported that ByteDance was discussing capital expenditures of up to $70 billion for 2026, all earmarked for data centers and AI infrastructure. This figure, equivalent to 400-500 billion RMB, is 6.4 times ByteDance's 2024 spending and more than double its 2025 expenditures.

With successive rounds of increased investments, the capital expenditures of the new BAT (ByteDance, Alibaba, Tencent) have shifted from "ByteDance leading but with a small gap" to "ByteDance surpassing the combined spending of A and T," clearly aiming to outspend its competitors.

In concrete actions, this is reflected in ByteDance's global acquisition of AI chips.

In June 2024, ByteDance was reported to be collaborating with Broadcom to develop a 5nm AI processor for custom ASICs. In August 2025, VeriSilicon was also rumored to be deeply collaborating with ByteDance to customize a new inference chip, causing its stock price to surge by 20cm at one point, though ByteDance quickly denied both rumors.

In May this year, Bloomberg claimed that Qualcomm had disclosed an AI data center chip agreement with ByteDance, which planned to purchase millions of ASICs to support Agent deployment.

Domestically, according to Shandian News, ByteDance had pre-purchased over $5 billion worth of domestic computing power products, involving suppliers such as Cambrian and Huawei's Ascend.

In June, according to Yicai, ByteDance was negotiating with Iluvatar CoreX to purchase AI chips, primarily for inference workloads, while also initiating contact with Baidu's Kunlun Core. This procurement is expected to exceed 50,000 chips, mostly for inference tasks to support Doubao's user expansion.

If this deal materializes, Iluvatar CoreX will become ByteDance's third major domestic GPU supplier after Huawei and Cambrian.

In addition to continuously acquiring AI chips on the market, ByteDance has not neglected recruiting top talent.

Over the past year, talent turnover within ByteDance's AI team has become more pronounced. According to previous reports by Jiemian News, nearly 70 technical talents have left ByteDance's Seed team in the past year, joining domestic leading internet companies, large model companies, and international tech giants.

Among them, Qiao Mu, the head of the large language model team, was dismissed due to an internal complaint letter; Yang Jianchao, the head of visual multimodal generation, took a temporary break due to family and long-term high-intensity work; Li Hang, the head of ByteDance AI Lab, stepped down and transitioned to a contract/advisory role...

To retain the most critical asset in large model R&D—people—ByteDance has upped the ante.

After the 2026 Spring Festival, ByteDance's Seed team established a new World Model Research Group, headed by Fan Haoqi, a former researcher at Meta's FAIR Lab, reporting to Zhou Chang, the head of Seed's multimodal and world model teams.

In April, according to Wall Street See, ByteDance recruited Guo Daya, a core researcher from DeepSeek, as one of the heads of the Agent direction, with rumors of a "100 million RMB annual salary" circulating. In May, Dong Xin, a former research scientist at NVIDIA, was also reported to have joined ByteDance's Seed LLM large language model training research team.

Each of these top researchers comes with exorbitant salaries and annual compensation packages beyond ordinary imagination.

In addition to poaching mature talent, ByteDance is also vying for fresh graduates. In April, ByteDance's Seed team launched its 2027 campus recruitment for large model talent, planning to recruit about 100 large model talents globally, and explicitly mentioned that eligible fresh graduates and outstanding interns would also have the opportunity to receive "Doubao shares."

While investing heavily to bring in top researchers, ByteDance has also introduced a special incentive plan—"Doubao shares."

Doubao shares are virtual stock incentives specifically designed for Doubao's large model business, binding the core AI talent's rewards to the Doubao business line separately, no longer constrained by ByteDance as a whole, thus providing greater salary growth space for Doubao researchers.

And this is also reflected in the price increases. Since being granted at $10 per share in the fourth quarter of last year, the price of Doubao shares had risen to $13.08 by the first buyback in April this year, and recently jumped again to $14.85, accumulating a 48.5% increase.

In comparison, in October 2025, ByteDance's option buyback price for current employees was $200.41; it rose to $229.5 in April this year; and then to $235.5 in June, a 17.5% increase, about one-third of the increase in Doubao shares.

This suggests that ByteDance, while searching for ASIC designers overseas, binding Samsung's 6nm capacity, and acquiring domestic GPUs, is also poaching top talent with high salaries and growth prospects, locking in core teams with "Doubao shares," and forcibly creating a moat with money. This is hardly the choice of a company "short on funds" for AI investment.

02 Doubao Wants More Valuable Users

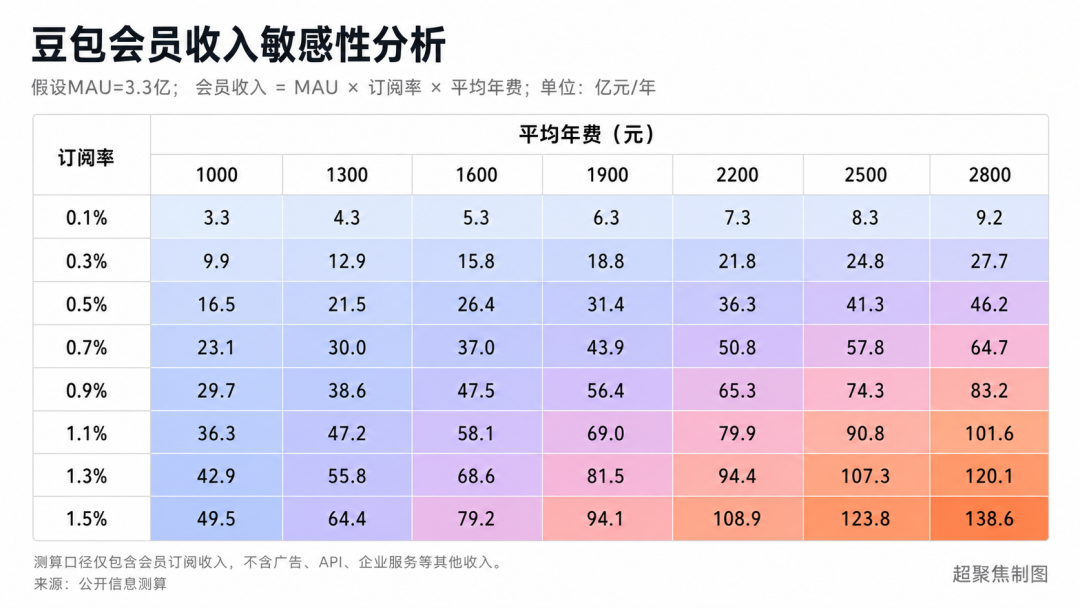

If we conclude solely based on expenditures that Doubao is not aiming to make money, it might be somewhat biased. We can estimate how much ByteDance could earn by introducing paid subscriptions for Doubao.

First, let's look at the pricing. Previously, the Doubao App Store page disclosed three subscription tiers: Standard at 68 RMB/month, Enhanced at 200 RMB/month, and Professional at 500 RMB/month, with annual fees of 688 RMB, 2048 RMB, and 5088 RMB, respectively.

With pricing in place, combined with user numbers, we can conduct a simple revenue sensitivity analysis for Doubao.

According to the latest statistics from AI data platform Aicpb.com, Doubao's MAU is approximately 330 million users. Considering its massive user base and the undeveloped paid habits domestically, we estimate its subscription rate will range from 0.1% to 1.5%, with the average annual fee per subscriber expected to fall between 1000 and 2800 RMB. The revenue ceiling for Doubao membership is not particularly high.

Under neutral conditions, if Doubao can achieve a 1.1% subscription rate, with each user contributing an annual fee of 2200 RMB, the full-year revenue from Doubao membership would not even reach 8 billion RMB. Assuming the most optimistic scenario, with a 1.5% subscription rate and an average annual fee of 2800 RMB, the annual revenue would only be 13.86 billion RMB.

This figure is substantial but pales in comparison to ByteDance's AI investments.

A few billion RMB annually would not cover the salaries of genius researchers, and over a hundred billion RMB would not fill the bills for purchasing chips, building data centers, or issuing Doubao shares.

Moreover, this is just revenue, not profit. Doubao's paid membership revenue would still need to deduct significant channel costs, inference costs, bandwidth costs, and service costs. The more users pay, the heavier the token usage, and the greater the underlying computational consumption. How much of this tens to hundreds of billions in gross profit would remain is uncertain.

Therefore, charging for Doubao is unlikely to be ByteDance's way of recouping costs through membership fees. Instead, it is probably targeting the high-value users of the "Big Three" (presumably referring to leading AI companies).

Currently, there are not many paying users among domestic AI companies. Those willing to pay for large models are often high-frequency users in coding, investment research, office work, design, and data analysis. This group is vertical, has clear needs, and is willing to pay for stronger models, faster responses, and higher quotas. These are the users that companies like Zhipu, MiniMax, and Kimi are truly vying for.

And Doubao is targeting these high-value individuals.

For ByteDance, as long as Doubao can offer stronger model capabilities, higher usage quotas, and more cost-effective pricing in its Professional version, it has a good chance of luring these users away from other AI products with computational power and subsidies.

In this light, the purpose of Doubao charging fees is not just to make money but also to screen its audience. The so-called membership fees are more like a threshold for selection.

The free version of Doubao keeps the vast majority of ordinary users engaged, continuing to cultivate usage habits; the paid version of Doubao targets high-demand users, using a superior experience to reaffirm Doubao's value.

In the past, Doubao was jokingly referred to as "Tangbao" or "Caibao," largely because ByteDance lacked computational power, making it seem like a "sickly" ChatBot to ordinary users. However, if the paid version can enhance models, inference, Agents, code, long-text processing, and professional scenarios, Doubao could become ByteDance's gateway to high-end AI users.

And to provide superior capabilities for high-value users means burning more tokens, which is not a significant issue for the financially robust ByteDance.

This is where competitors feel the most pressure: Doubao has become the "standard" for domestic AI. The free version offers comprehensive capabilities, making it difficult for competitors to raise prices; the Professional version has sufficient computational power and technical support, forcing competitors to compete on specialized skills and cost-effectiveness.

The paid Doubao is like "Thanos" in the domestic AI industry obtaining the Infinity Gauntlet. Once it gathers the power of all six Infinity Stones, the industry will face an unavoidable infinite war.

- END -

-

![]()

"Current gasoline vehicles are akin to horse-drawn carriages of yesteryear."

-

![]()

Gasoline Vehicles Wait for Electric Vehicles to 'Stumble', Electric Vehicles Anticipate Gasoline Vehicles to 'Decline'

-

Entire 330-Kilometer Area Fully Unveiled! Hengqin Set to Eliminate Safety Officers and Steering Wheels Next Week, Ushering in China’s First Fully Autonomous City

-

![]()

New Energy Vehicle Order Rankings: Insights Revealed

-

![]()

China Invests Nearly 200 Billion Yuan This Year to Boost Car Sales

-

![]()

Oil Prices Revert to 7-Yuan Range: Are Gasoline Cars Getting a Reprieve?

-

![]()

Momenta Secures CSRC Approval: Is It Poised to Be the 'Pioneer in Physical AI Stocks'?

-

![]()

What's the Use of Having a General-Purpose Motion 'Cerebellum' for Humanoid Robots?