"Current gasoline vehicles are akin to horse-drawn carriages of yesteryear."

06/22 2026

06/22 2026

351

351

Lead

Introduction

The 300,000-400,000 RMB segment remains the most resilient for gasoline vehicles.

Undoubtedly, the trend towards electrification has reached a vigorous phase in the global automotive market.

From January to May, cumulative sales of new energy vehicles (NEVs) in China reached 5.802 million units, up 3.5% year-on-year; including 3.97 million units sold domestically and 1.833 million units exported. In the first four months, over one-fifth of new cars sold in the European market were pure electric vehicles (BEVs). According to the European Automobile Manufacturers' Association (ACEA), BEVs accounted for 20.9% of new car registrations from January to April.

For domestic consumers, the rising penetration rate of NEVs is a natural outcome. However, for some international consumers, constrained by certain objective factors, the pace of electrification may not match that of China. Nevertheless, foreign automakers have already sensed the dawn of a new era.

Recently, Martin Sander, Member of the Board of Management for Sales, Marketing, and After Sales at Volkswagen, stated in an interview that the transition from gasoline to electric vehicles may be more natural than many anticipate. He even drew a parallel: "Current gasoline vehicles are akin to horse-drawn carriages of yesteryear."

The crux of the matter lies in the question: "When were horse-drawn carriages ever banned? The answer is never."

People naturally abandoned horse-drawn carriages as daily transportation once automobiles became more convenient and efficient. Sander believes the industry has spent too much time discussing internal combustion engine bans, overlooking what truly attracts consumers to EVs. In the long run, EV adoption should stem from voluntary consumer choice rather than government mandates.

01 Horse-Drawn Carriages Did Not Disappear

Currently, while many consumers in Europe and the United States remain concerned about charging infrastructure, vehicle pricing, and long-distance usability, automakers' enthusiasm for electrification has not waned. Sander feels that discussions around EVs focus too heavily on regulations and deadlines. Repeatedly discussing future bans on gasoline vehicles risks alienating consumers who are still satisfied with their current cars.

He argues that automakers and governments should focus on improving charging networks, reducing electricity costs, and highlighting the everyday benefits of EVs—such as quieter operation, lower maintenance costs, and quicker acceleration. These tangible advantages will gradually win over users.

"Once these conditions are in place, by 2035, the proportion of customers still wanting to buy gasoline vehicles might shrink to just 3%, 4%, or 5%." "Of course, gasoline vehicles may not disappear entirely. Just as horse-drawn carriages persist today for leisure or enthusiast activities, gasoline cars will likely retain a niche market decades from now."

Sander's horse-drawn carriage analogy may sound exaggerated, but it clearly illustrates Volkswagen's assessment of market trends. As technology advances and infrastructure improves, EV adoption will naturally rise steadily. Much like the transformations witnessed in China's automotive market over the past years, today's consumers increasingly recognize the value offered by NEVs.

Thus, the shift from gasoline to new energy vehicles resembles a gradual shift in consumer preferences rather than an abrupt revolution.

Of course, many argue that the accuracy of such predictions remains uncertain. Throughout automotive history, numerous technologies once seemed inevitable but were later slowed by market realities. Even so, major automakers continue to actively prepare for a future where EVs dominate a larger market share. The real challenge now lies in convincing skeptics that EVs represent the best choice for daily transportation.

Notably, following such predictions, signs of slowing BEV adoption have emerged in key markets. While China maintains high EV penetration, U.S. sales have plummeted due to reduced subsidies. Europe has shifted from "zero-emission mandates" to more flexible "emission reduction" targets, creating space for plug-in hybrid and range-extender technologies.

Despite market adjustments, Volkswagen has tailored its powertrain strategies to different regions. In Europe, the electric version of the best-selling small gasoline car, the ID. Polo, will be launched, along with a significant redesign of the criticized ID.3. The ID. Polo GTI will soon hit the market, followed by the ID. Tiguan later this year.

In China, Volkswagen showrooms prominently feature large SUVs tailored to local preferences. The company is well aware of competitive pressures from Chinese automakers. Sander states that success in China will help Volkswagen build better vehicles for the UK and European markets. "Everything we learn in China will help us maintain global competitiveness—the key lies in scale, efficiency, and cost."

Of course, Volkswagen is not alone. Many European mainstream brands have recently expanded their electric lineups. BMW is preparing to launch a new i3 sedan, reportedly capable of traveling 559 miles on a full charge, with a 10-minute charge adding 249 miles of range. The Mercedes-Benz CLA EV also surpassed its EPA-rated range in independent testing, achieving 385 miles on a full charge.

Meanwhile, rising fuel prices have prompted some hesitant car owners to reconsider EVs.

02 Usage Scenarios Determine Powertrain Choice

In fact, just a few days ago, renowned automotive influencer Han Lu shared his perspective on the evolution of powertrains for family vehicles on social media. He argued that given current advancements in battery technology, vehicle energy efficiency, and charging speeds (including battery swapping), by 2029, there will be little justification for launching new gasoline-engined plug-in hybrid (including range-extender) family vehicles, except for off-road and hardcore SUVs.

"As for the future of plug-in hybrids (and range-extenders), they will first fully replace gasoline vehicles. By 2029, gasoline cars will largely consist of nostalgic models with 6-8-cylinder, ultra-large displacement engines. Plug-in hybrid (and range-extender) models will persist, serving niche scenarios—99% of their use cases will involve off-roading and long-distance travel, increasingly shifting toward specialized, niche (niche) vehicles."

He noted that 2026-2027 will mark the final years when conventional (non-off-road) plug-in hybrid (and range-extender) models remain widely available. From 2028 onward, their presence will sharply decline across ordinary sedans, SUVs, and MPVs. By 2029, he estimates that 80-90% of new vehicles on the market will be BEVs.

Clearly, both Han Lu's and Sander's assessments appear bold against the backdrop of accelerating global EV market growth. However, they align closely in their overarching direction: a BEV-dominated market landscape is imminent.

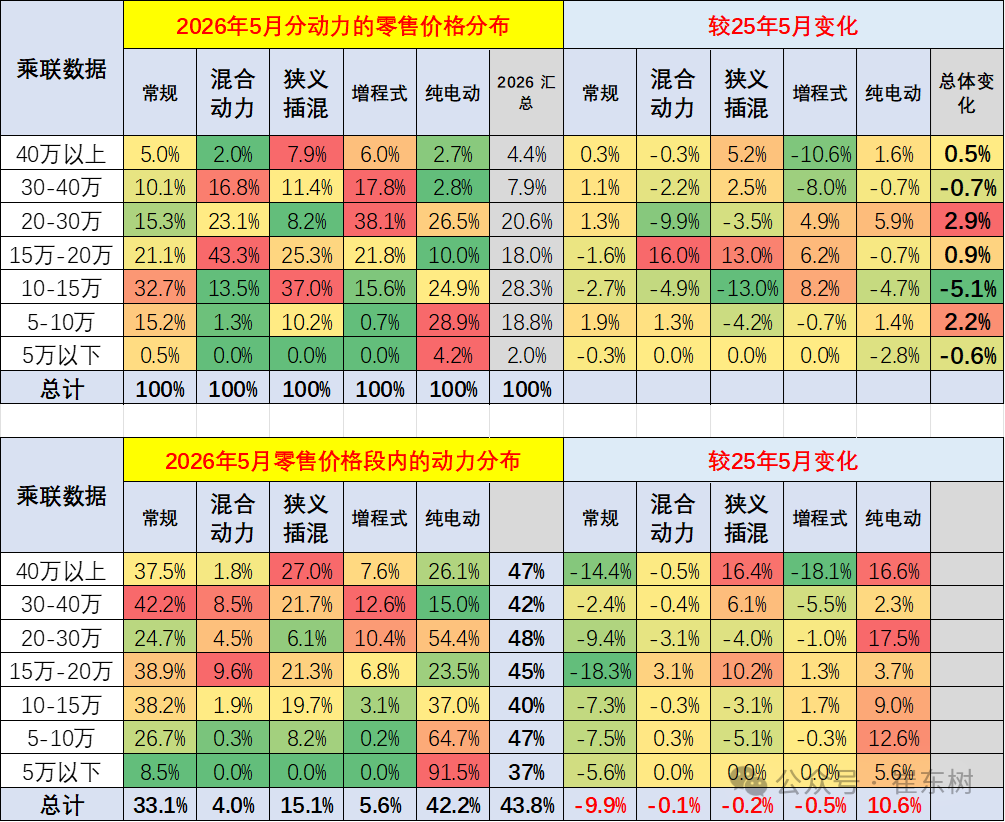

Data supports this outlook. Recently, the China Passenger Car Association (CPCA) released sales data for May 2026, broken down by price segments and powertrain types, revealing the distribution of five powertrain forms: gasoline, HEV, plug-in hybrid, range-extender, and BEV.

In the sub-50,000 RMB segment, only BEVs (91.5%) and gasoline vehicles (8.5%) are present. In the 50,000-100,000 RMB range, BEVs dominate with 64.7%, followed by gasoline (26.7%) and plug-in hybrids (8.2%), while HEVs and range-extenders combined account for just 0.5%.

The picture shifts slightly in higher-priced segments. In the 100,000-150,000 RMB market, gasoline vehicles lead with 38.2%, but BEVs close the gap at 37%, with plug-in hybrids at 19.7%. This distribution pattern also applies to the 150,000-200,000 RMB segment.

The 200,000-300,000 RMB segment presents a unique case. Here, BEVs account for over half the market at 54.4%, while gasoline vehicles hold 24.7% and range-extenders trail at 10.4%. However, in the 300,000-400,000 RMB and above-400,000 RMB segments, the top three are gasoline, plug-in hybrids, and BEVs.

Across these seven price segments, BEVs command over 50% market share in three segments, tie with gasoline in one, and compete closely with plug-in hybrids in two. More importantly, compared to the previous year, BEVs registered the highest growth in five segments.

Additionally, in May 2026, China's gasoline passenger vehicle market suffered a significant decline, with sales dropping 39% year-on-year and market share falling to 37.1%, a historic low.

As many analysts note, the rapid arrival of the BEV era is driven by multiple factors. Declining battery costs have lowered BEV pricing, while advancements in battery technology and fast-charging infrastructure have alleviated range anxiety, enhancing BEV market competitiveness.

Of course, this does not imply the immediate disappearance of gasoline, plug-in hybrid, HEV, or range-extender vehicles. Both Sander and Han Lu acknowledge that different powertrains will support distinct usage scenarios: high-performance nostalgic vehicles, off-roaders, family cars, and so on.

Editor-in-Chief: Shi Jie Editor: He Zengrong

THE END

-

![]()

Technology Sector's Meteoric Rise | Historic Transformation of A-Share Market Capitalization

-

Automotive Market News: New Energy Vehicles Set to Expand into Rural Areas by 2026!

-

![]()

Exorbitantly Bold! Liang Wenfeng Invests 20 Billion Yuan of His Own Funds and Imposes 'Dictatorial Terms'

-

![]()

FAW-Audi and SAIC-Audi Restructuring: One Maintains Profit from Gasoline Cars, the Other Stakes Future on Electric Vehicles

-

![]()

When Smart Grows Up, Will It Still Be Appealing?

-

![]()

Global Strategy Forum on Automotive Supply Chain Empowerment via Hong Kong's Global Reach Concludes Successfully

-

![]()

In-depth Report on the 2026 Hong Kong Auto Expo | China's Auto Industry Upgrading Systemic Competition in Global Expansion: How Can Hong Kong Empower It?

-

![]()

The decline of fuel vehicles is irreversible, and extended-range and plug-in hybrids may fare even worse