Zhipu: Trillion-dollar Market Cap, Is China's Anthropic Really Here?

06/23 2026

06/23 2026

411

411

Zhipu's June performance, in contrast to the consistently weak broader market, has been nothing short of spectacular. First, news of its inclusion in a major index before June triggered significant capital fluctuations on the same day. Then, from June 10 to June 18, its stock price doubled in nearly a week. Finally, on June 22, Zhipu's market capitalization successfully surpassed HK$1 trillion.

Such strong performance has exceeded market expectations. In our previous earnings review, we noted that Zhipu has stronger momentum compared to MiniMax, with the core judgment being that capital pricing is based on the scarcity of model intelligence. Standing at the current juncture, facing Zhipu's unexpectedly high market capitalization, we believe this view remains reasonable, but "intelligence scarcity" alone is clearly insufficient to explain it.

1. Is it driven by ARR?

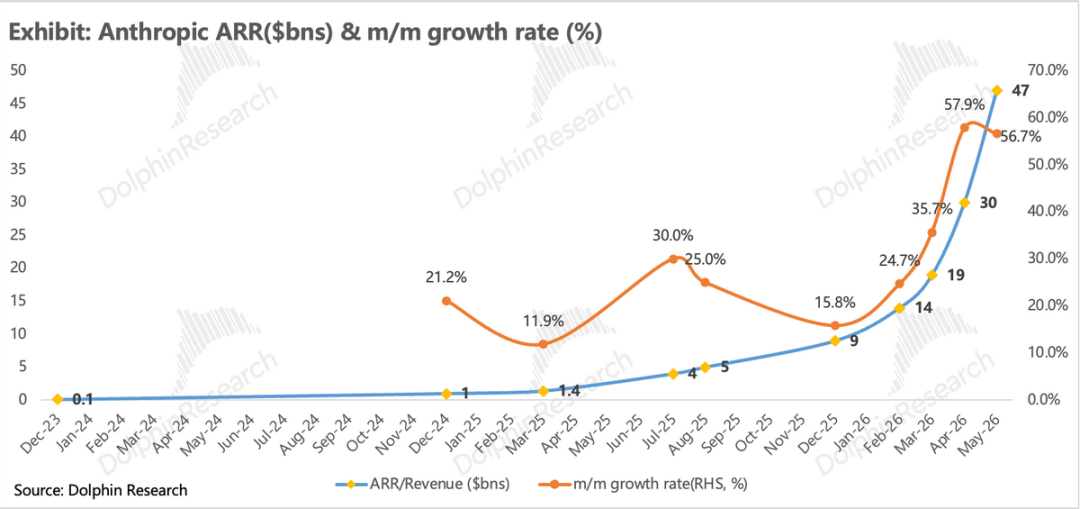

Zhipu's pricing logic has already evolved into an overseas comparable To B business model (Claude) valuation mode since its post-holiday stock price surge. From Anthropic's ARR growth curve, there has been no sign of a slowdown, with an accelerating trend since the beginning of the year, exceeding 55% monthly growth in April/May. This opens up room for imagination (imagination space) for Zhipu's growth.

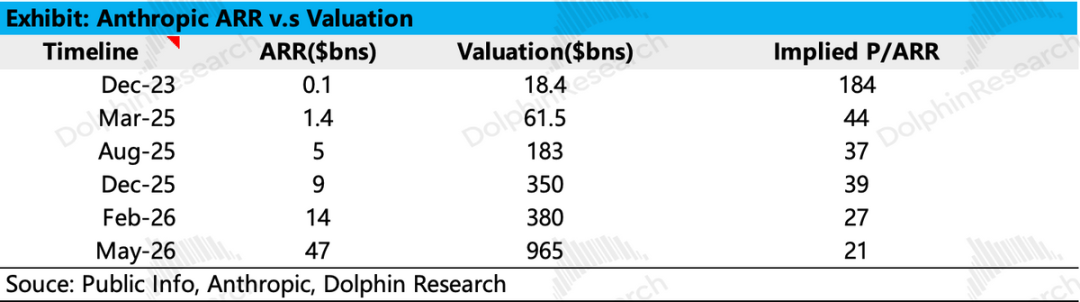

In our previous review, we provided a reference: assuming Zhipu replicates Anthropic's pace and achieves $1 billion in ARR in about a year (corresponding to a month-over-month growth rate of about 12%), with Anthropic's P/ARR multiple, the corresponding valuation would be about $60 billion. However, Zhipu's current market capitalization has reached $150 billion. Using the same Anthropic P/ARR multiple in reverse, this price implies an ARR of about $4 billion, corresponding to a month-over-month growth rate (March-June) as high as 150%, which is clearly unrealistic.

Stepping back, using Anthropic's growth phase growth rate to test whether this valuation is acceptable: Anthropic's ARR took nearly half a year to grow from $1 billion to $5 billion, with a month-over-month growth rate of about 30%. Based on this, let's make a set of assumptions: if Zhipu's current ARR has already reached $1 billion (which itself implies a nearly 60% month-over-month growth rate in the past three months), and then grows at the same 30% month-over-month rate for another half year, the ARR would be about $5 billion. Under Anthropic's valuation multiple, this roughly aligns with a $150 billion market capitalization.

In other words, the current valuation at least implicitly contains two layers of expectations: first, Zhipu's ARR has already approached $1 billion at this moment; second, it needs to maintain a month-over-month growth rate of about 30% for the next half year. However, Zhipu's recently disclosed official ARR is only $250 million. Under this expectation, Zhipu would need to push its ARR from $250 million to $1 billion in three months and maintain a 30% month-over-month growth rate for the next six months without any slowdown. The implied expectations are undoubtedly overly optimistic.

Although the specific ARR situation is currently unknown, from an observable volume and price perspective, Zhipu is experiencing both volume and price increases, confirming the trend of rapid ARR growth.

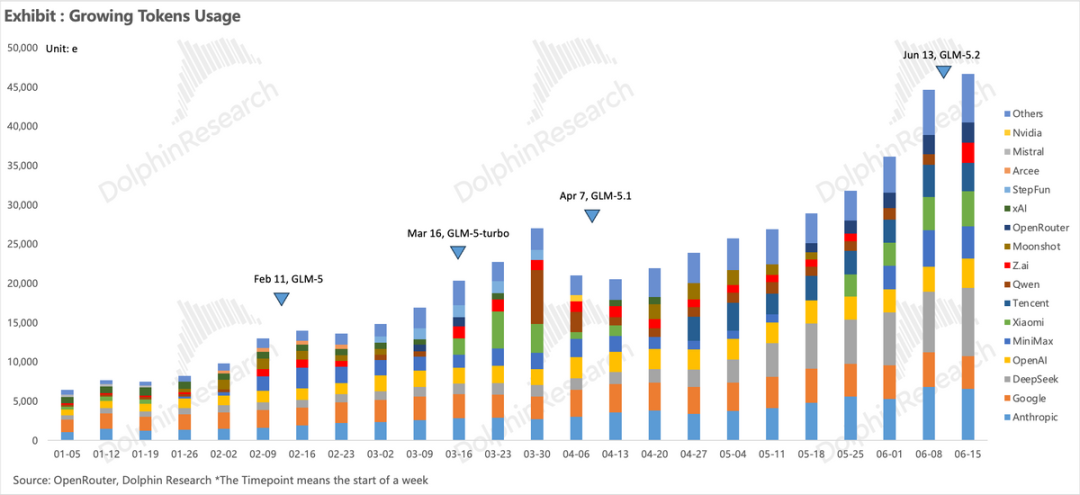

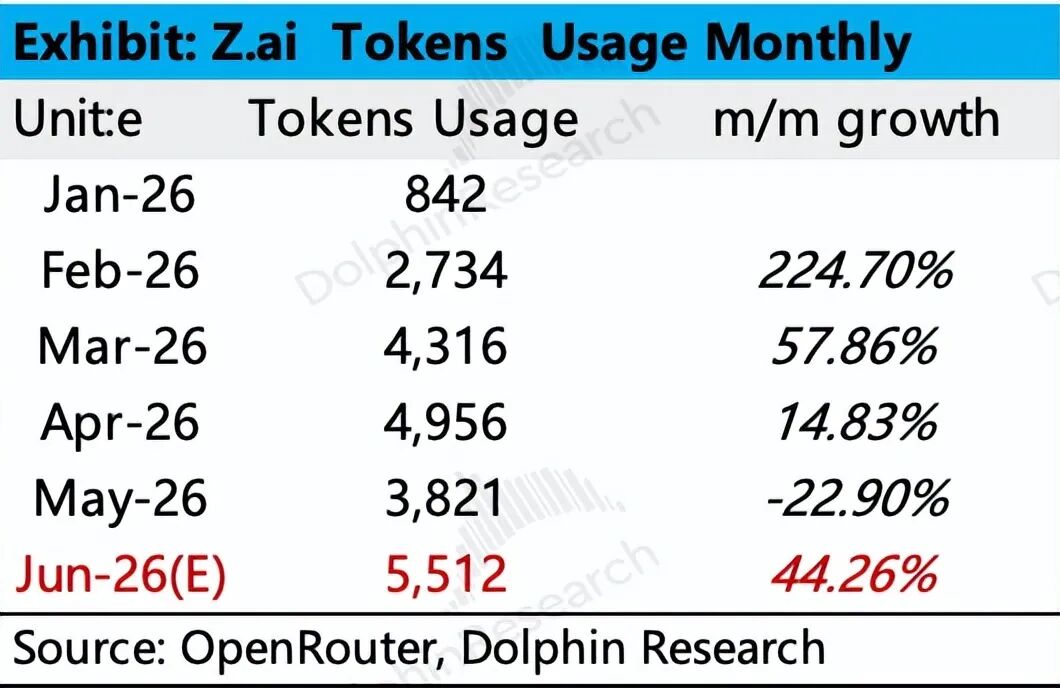

Volume: We observed on OpenRouter that the overall usage of platform models is still on an upward trend. Zhipu's token usage on the OR platform grew at an average monthly rate of 40% from January to June 2026 (Dolphin Research's forecast), but the growth rate since March has been only 8%. Part of the reason is that its usage is highly synchronized with the release of new models, with each new model launch typically bringing about a month of high-intensity usage followed by a decline.

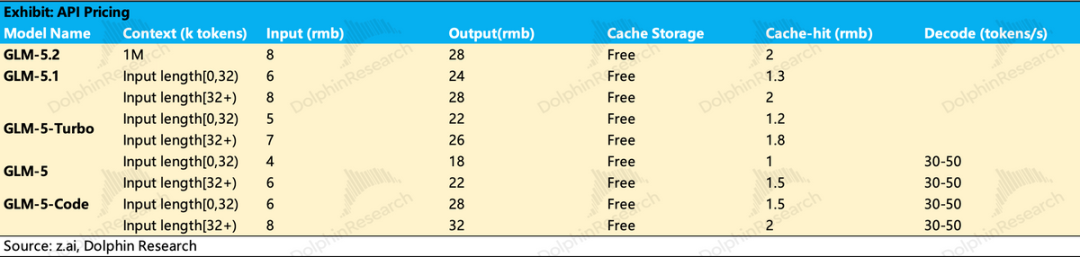

Price: In terms of pricing, the API pricing has not officially increased (5.2 vs. 5.1), but in reality, GLM-5.2 has shifted from tiered pricing to blended pricing, charging all usage at higher rates instead of offering lower rates for certain usage levels, which is a de facto small price increase.

Comparatively, Zhipu's model pricing has almost reached the ceiling for domestic models. We believe its high pricing is justified for two reasons: first, the scarcity of intelligence gives it the confidence to raise prices; second, its products are primarily targeted at B-end clients, who are more concerned with the productivity benefits brought by model intelligence improvements and are relatively insensitive to price.

Further comparing the two business models: the C-end model represented by MiniMax and OpenAI versus the B-end model represented by Anthropic and Zhipu. The latter's valuation performance is significantly better than the former, and the B-end monetization logic has largely been validated. Anthropic has consistently equipped its models with the highest pricing based on superior intelligence, and once it reaches the intelligence ceiling, users can only complain about the price while still paying. Zhipu's price increase for its Coding Plan in February was also interpreted by the market as confidence in its model capabilities. In contrast, on the C-end, Doubao's plan to charge fees/OpenAI's introduction of ads has instead caused user dissatisfaction.

Based on the above volume and price analysis, usage has indeed maintained high growth (but clearly not as high as the above estimates), and prices have de facto increased slightly. However, this is still insufficient to support our core assumption that Zhipu's ARR has already approached $1 billion. Therefore, the current significant stock price rebound is more about valuation premiums.

2. What aspects does the valuation premium manifest in?

1) GLM-5.2 is the first domestic model to rank among the top three in intelligence. On June 13, Zhipu released GLM-5.2 through its Coding Plan and opened the API on June 17. GLM-5.2 is a 744 billion-parameter MoE model with 40 billion activated parameters and a context window of up to 1 million tokens. It excels in programming and long-term agent workflows, representing a significant improvement over the previous generation model, and its weights are openly available under the MIT license.

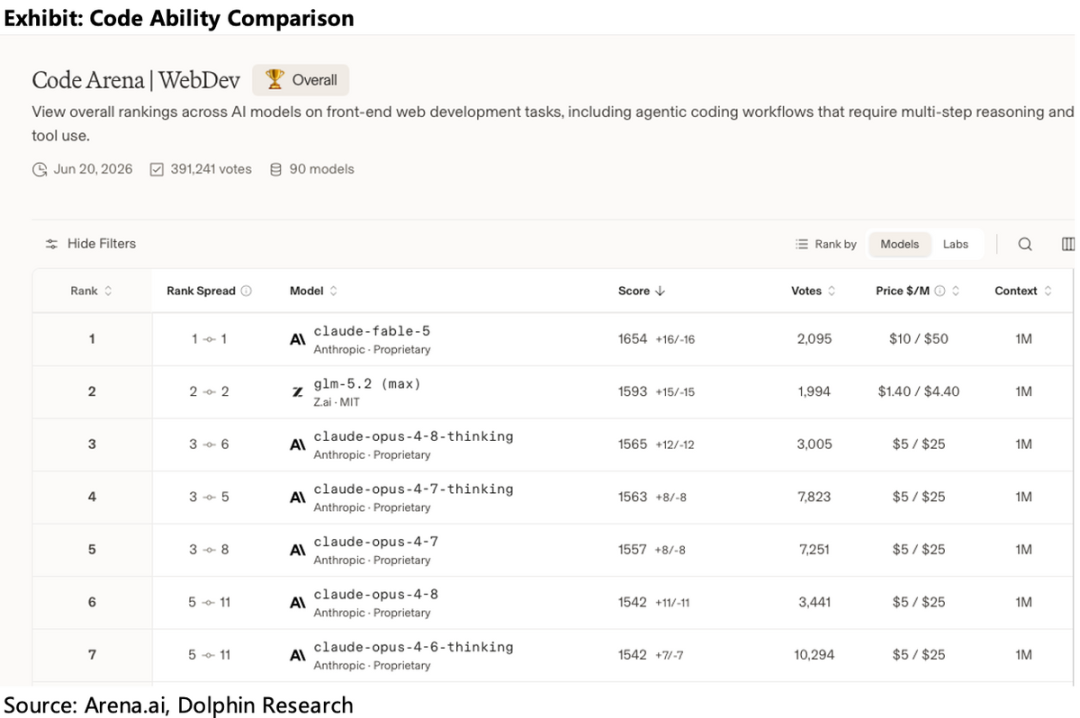

With GLM-5.2, Zhipu once ranked third globally and first in China on Artificial Analysis's model intelligence index, second only to (just behind) Anthropic and OpenAI; it ranked fourth/second globally and first/first in China on the programming/agent index (global rankings were adjusted downward as of June 22).

Meanwhile, in Arena.ai's evaluation, GLM-5.2 ranked second globally in programming capabilities, outperforming Opus 4.8 and second only to Fable 5.

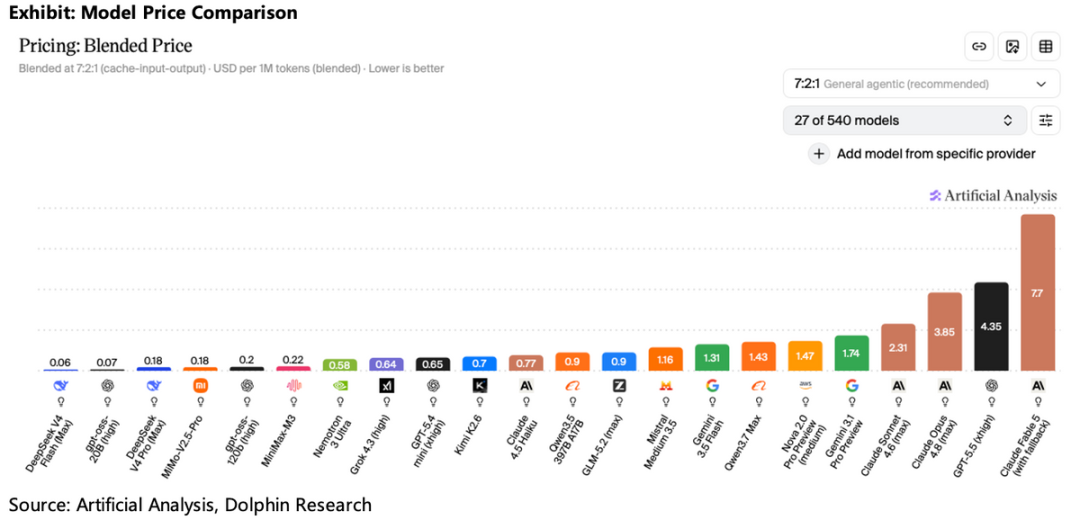

Furthermore, as the gap between open-source and closed-source models continues to narrow, founder Tang Jie publicly stated that Zhipu may surpass Anthropic within the year. Considering that domestic models are priced significantly lower than Anthropic's (Zhipu's API pricing is about 1/4 of Opus's and 1/10 of Fable 5's), this has greatly boosted market confidence in the substitution of domestic models.

2) The U.S. is closed, China is open. Just as Washington ordered a halt to overseas services by top U.S. models, and Anthropic cited export control directives to suspend Fable 5, Zhipu almost simultaneously launched an open-source version. A contrasting narrative naturally formed: while the U.S. is tightening access to cutting-edge technologies, China released MIT-licensed, region-unrestricted open weights in the same week.

This contrasting narrative can provide a short-term boost in valuation, but from a commercialization perspective, GLM-5.2 will not directly benefit from such bans. First, the restrictions on Fable 5 are not permanent and have reportedly begun to be reintroduced gradually. Second, given the short window of opportunity and the general belief that GLM-5.2's overall user experience is still slightly inferior to Opus 4.8, this demand is unlikely to translate into significant revenue growth.

From a longer-term perspective, if Zhipu indeed develops a model comparable to or even surpassing Anthropic's (notably, Zhipu was not on Anthropic's list in February accusing Chinese model companies of model distillation), then combined with recent U.S. and Anthropic's closed actions, we should perhaps view cutting-edge models as strategic assets bear (bearing) geopolitical significance.

Currently, the U.S. has two major players, OpenAI and Anthropic, while China currently has only Zhipu, so it is reasonable for it to enjoy a higher valuation premium.

3) Extremely narrow float. The actual free float is extremely low (less than 3% of total share capital on the listing day), coupled with passive demand from index inclusion, has amplified short-term scarcity multiple times. However, as various lock-up periods expire in the second half of the year and the float gradually increases, the current scarcity is clearly not the norm.

Combining the three points in Section 2, we believe Zhipu's valuation premium is reasonable. However, based on the ARR analysis in Section 1, even in an optimistic scenario where we assume the company achieves over $1 billion in ARR by September, implying a month-over-month growth rate of about 30%, and referencing Anthropic's average monthly growth rate of 20% from $1 billion to $9 billion in ARR, we calculate that Zhipu's ARR would reach about $1.73 billion by the end of 2026, implying a P/ARR multiple still as high as 80X. This means that even under optimistic expectations, the valuation multiple is nearly double that of Anthropic's same period ( same period ) level.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general viewing and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any person receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available materials and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or intended to be distributed to jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials conflicts with applicable laws or regulations or results in Dolphin Research and/or its affiliates or associated companies being subject to any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report only reflects the personal views, opinions, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or distribute in any form any copies or reproductions in any way, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Geely's Three Strategic Cards for Future Layout Unveiled at Hong Kong Auto Show

-

![]()

GAC Toyota’s Sales Boom: Forging Vehicles with Enduring Value for the Long Haul

-

![]()

Insider Insights on Brazil’s Internet Landscape: No Chinese Firm Has Made Significant Profits in 25 Years

-

![]()

【OFweek Weike Cup】HG Genuine Optics Nominated for 2026 Excellent Optical Component Supplier in the Optical Industry

-

![]()

European Sales of Chinese Vehicles Surge 1.5-Fold in a Year! EU Takes Action: Additional Tariffs on China’s Plug-in Hybrid Vehicles

-

![]()

Soaring 19-Fold, Market Value Hits Trillions: Is Zhipu a Legend or a Speculative Bubble?

-

![]()

【Electric Equipment】The first standard for shore power facilities of electric ships is introduced and will be officially implemented on August 1

-

![]()

【Intelligentization】Joint Development of Right-Hand Drive Robotaxi: Geely Yuancheng, WeRide, and Kwoon Chung Bus Sign Agreement