5,000 Companion Robots Sold: Can UBTECH Breathe a Sigh of Relief?

06/26 2026

06/26 2026

334

334

In June, UBTECH made waves in the consumer market for humanoid robots.

Its consumer brand, YouShiJie, began pre-sales simultaneously on JD.com and Tmall. The full-sized humanoid robot U1, available in male and female versions, focuses on emotional companionship and features 88 highly articulated motion joints. Within 10 days of its launch, pre-orders approached 4,000 units, exceeding 5,000 by June 21.

For comparison: In all of 2025, UBTECH sold a total of 1,079 full-sized embodied intelligent humanoid robots. Pre-orders for this consumer product in less than three weeks nearly quintupled last year's annual B-end sales.

UBTECH revealed that production for the U1 series is expected to reach 10,000 units this year. Additionally, the company set a production capacity target of 10,000 industrial humanoid robots.

In early 2026, UBTECH founder Zhou Jian stated, "Based on currently disclosed orders and bid wins, we may rank first globally in terms of both single contract value and cumulative value."

From these figures and statements, UBTECH appears to be making strides in both industrial and consumer markets, rapidly advancing from inception to scale. However, questions linger around the company, including concerns about falling behind and unclear profitability timelines.

In 2016, during the CCTV Spring Festival Gala, 540 UBTECH Alpha 1S robots performed a synchronized dance to Sun Nan's singing, catapulting UBTECH into the spotlight. The company returned to the gala in 2018, 2019, and 2021.

The exposure from the gala quickly translated into capital market success, attracting investments from prominent backers like Tencent and fueling multiple funding rounds.

In late 2023, UBTECH went public on the Hong Kong Stock Exchange as the "first humanoid robot stock," enjoying a moment of glory.

By 2025, however, the spotlight had shifted. During the Spring Festival Gala, robots from Unitree Technology, dressed in floral cottons and waving handkerchiefs, stole the show with their superior motion control, becoming the new face of humanoid robots. That year, Zhiyuan Robotics shipped 5,100 units, leveraging cost reductions through software-hardware decoupling and an ecosystem built on open-source large models, emerging as a new industry leader.

Also in 2025, UBTECH adjusted its financial reporting, listing "full-sized embodied intelligent humanoid robots" as a standalone business category for the first time. Previously, revenue was categorized by scenario.

In public perception and industry influence, the former "first mover" was being overshadowed by newcomers.

For 2026 shipment guidance, Unitree Technology aimed for 10,000–20,000 units, while Zhiyuan Robotics projected "tens of thousands." UBTECH targeted 5,000 units for its industrial Walker S series and had already exceeded 5,000 pre-orders for its U1 consumer product, showing significant growth.

Behind these order disparities lie differences in product positioning and pricing.

Unitree Technology's G1 starts at under RMB 100,000. In 2025, its humanoid robots averaged RMB 167,000, while UBTECH's models averaged RMB 760,000.

The price gap stems primarily from differing technical focuses and application scenarios. Industrial settings demand higher stability than consumer environments, impacting production costs. However, Unitree's exceptional cost control, reflected in its financials—falling product prices alongside rising gross margins (now at 60%)—cannot be overlooked.

In this track (race), volume and price drive each other. Lower prices boost sales, creating economies of scale that further reduce per-unit manufacturing costs. This "price-for-volume, volume-for-cost" flywheel is the core commercial logic in scaling from 1 to N.

Awareness, orders, and market position all influence how capital markets view UBTECH.

The past two years' Spring Festival robot performances have set public expectations for technology too high, while Unitree's first profitable year has raised market hopes for commercial returns.

These dual expectations put UBTECH, still loss (losing money) and relatively low-profile, in an awkward position.

Indeed, UBTECH's stock price has been on a rollercoaster since its IPO: After being included in the Stock Connect in March 2024, its shares surged 88% in a single day, hitting a historic high of HKD 328 and a market cap exceeding HKD 130 billion. However, it steadily declined, bottoming at HKD 40.8 in early 2025, erasing HKD 100 billion in value.

As UBTECH's humanoid robot shipments rose from 10 units (across models and sizes) in 2024 to thousands in 2025, its stock rebounded. Currently valued at around HKD 49 billion (RMB 42.6 billion), its market cap nearly matches Unitree's IPO valuation.

However, multiple agencies estimate Unitree's fair valuation post-IPO at RMB 60–100 billion, with expectations of growth beyond RMB 42 billion. Financially, UBTECH's 2025 revenue exceeded Unitree's by 17.7%, yet the market appears to be pricing them differently.

Factors include listing locations—Unitree plans to list on Shanghai's STAR Market, while UBTECH is on the Hong Kong Stock Exchange—with A-shares typically offering higher liquidity premiums for hard-tech firms. UBTECH's chosen path may also play a role.

Regarding robot performances as a business scenario, Zhou Jian stated, "Initially, I didn't believe it could form a stable, large market. Later, we found dancing had strong appeal in lower-tier markets. However, I still don't see it as a sustainable direction."

Zhou believes the right path for humanoid robots is assisting with repetitive, simple, and tedious labor. However, from a technical and cost perspective, mature household applications will take longer.

UBTECH's strategy unfolds in three phases: First, industrial deployment to assist factory workers; second, commercial applications; and third, household entry for companionship and communication.

The June launch of its companion robot suggests the "three-step" approach isn't strictly linear. Accelerating consumer robot development may be a pragmatic response to competition and commercialization pressures.

Persisting with "heavy lifting" tasks means UBTECH must heavily invest in "brains."

In embodied intelligence, the cerebellum handles motion control, the body executes hardware tasks, and the brain manages decision-making and planning. Dancing relies on the cerebellum and pre-programmed routines, but complex factory tasks like handling and quality inspection involve unstandardized emergencies. Resolving these requires the "brain."

Zhou publicly claimed, "No one in China invests more in embodied brains than us."

For brain algorithms to function effectively, the cerebellum and body must keep pace. When UBTECH started, its supply chain was immature, forcing the team to develop components in-house. Over time, "full-stack" became its identity.

Full-stack means building everything independently, from brain algorithms to cerebellar motion strategies and body joint motors. UBTECH's technology portfolio spans nearly all levels: the Thinker embodied large model, BrainNet 2.0 swarm network, Thinker-VLA visual-language-action model, and more.

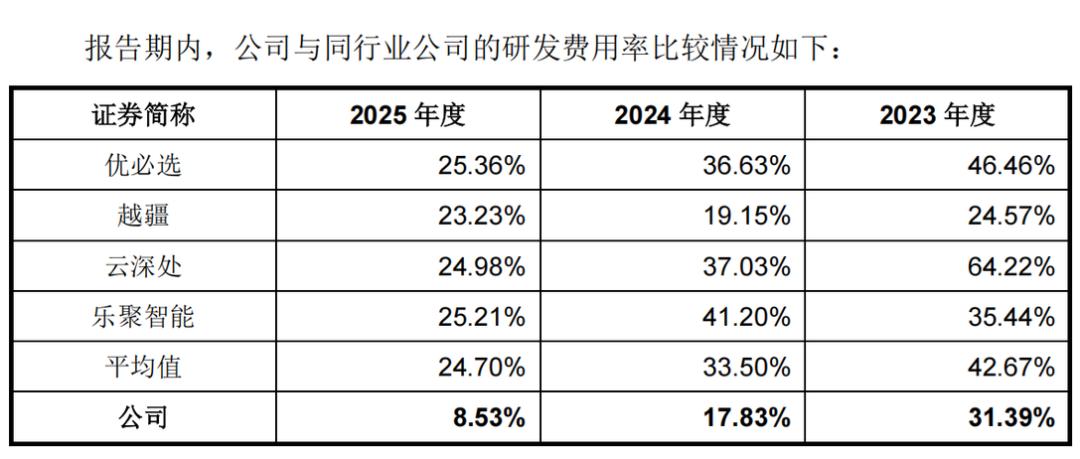

However, full-stack development is costly. UBTECH's 2025 R&D expenses reached RMB 507 million, with a significantly higher R&D-to-revenue ratio than peers, hinting at financial pressures.

(Source: Unitree Technology prospectus)

Strategy and approach are reflected in order structures and business logic.

UBTECH's orders fall into two categories: "embodied intelligent data collection center" projects led by local governments or state-owned enterprises, and industrial procurement orders. Zhou predicts more mass purchases from manufacturing giants in 2026.

Both factory deployments and data center roles allow robots to gather high-quality multimodal data from the physical world. This data feeds back into "brain" large models, improving generalization and enabling deployment in more scenarios, creating a "data-model-application" flywheel.

This long-term strategy of feeding large models with real-world data requires sufficient terminals to capture data.

The first type of customer buys robots primarily to collect real-world data and build testing infrastructure, not for immediate ROI on production lines. Transitioning from data infrastructure to practical applications takes time, meaning these orders are often project-based with long acceptance cycles, slowing UBTECH's cash flow—a point detailed later.

For B-end manufacturing to adopt humanoid robots at scale, ROI must be clear. Whether robots can perform tasks effectively, efficiently, and economically determines their commercial value.

In industrial settings, UBTECH's robots achieve 99% success rates in single tasks like intelligent handling and loading/unloading.

In early 2025, UBTECH's humanoid robots operated at about 30% of a human worker's efficiency in factories, improving to 45% by year-end and expected to exceed 60% in 2026. This means a robot working 12 hours roughly equals a human working 8 hours.

Industry estimates suggest a robot must replace a worker earning RMB 80,000–100,000 annually, with procurement costs under RMB 150,000 and controllable total ownership costs (including maintenance, downtime, and parts replacement), to be economically viable. Hidden costs after deployment often push the true economic threshold higher than the RMB 150,000 procurement price.

Thus, manufacturers must continue lowering prices to boost sales volumes.

Customer structure deeply impacts financial structure.

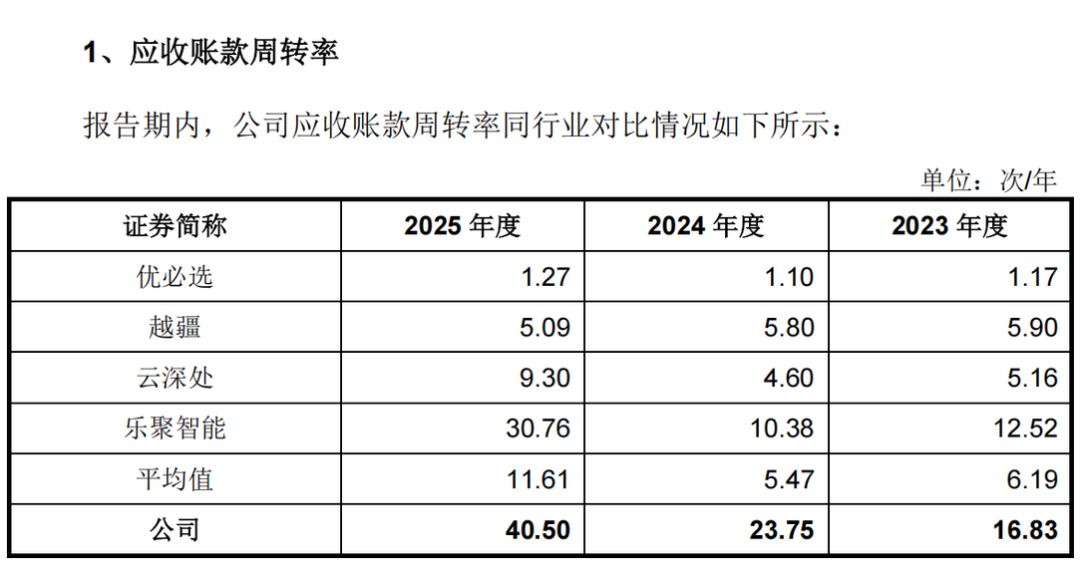

With a significant share of orders from government entities, UBTECH's cash collection is sluggish. In 2025, revenue reached RMB 2.001 billion, but accounts receivable hit RMB 1.3 billion, with collection cycles much slower than industry peers.

By year-end 2025, over 40% of receivables were over a year old, and those over three years surged more than threefold year-on-year.

(Source: Unitree Technology prospectus)

UBTECH has also been consistently unprofitable, reporting net losses attributable to parents of RMB 1.234 billion, RMB 1.124 billion, and RMB 703 million in 2023–2025.

Slow collections and profit pressures have kept UBTECH's operating cash flow negative, at RMB 1 billion, RMB 880 million, and RMB 780 million net outflows in 2023–2025.

The industry widely expects a shakeout in humanoid robots soon. Even without one, the race to scale will intensify funding demands.

Despite bleeding profits and cash, UBTECH appears financially stable. As of late 2025, it held RMB 4.888 billion in cash, largely from capital markets—RMB 6.3 billion raised through three 2025 private placements alone.

However, frequent discounted placements within two years of listing have diluted shareholder equity, sparking concerns about over-reliance on financing and accusations of "raising funds to stay afloat."

In other words, UBTECH's "cash-rich" status stems from strong financing ability, but its "cash-poor" reality reflects its business model.

The roots of its losses lie in two areas: insufficient shipment volumes to spread manufacturing costs and R&D expenses far exceeding peers.

Yet, another financial variable affects UBTECH's losses.

In 2025, UBTECH's construction in progress (CIP) stood at RMB 1.742 billion, with about RMB 1.22 billion allocated to office buildings. Less than RMB 60 million was added to this project all year, and none was transferred to fixed assets.

Moreover, UBTECH's CIP was over seven times larger than its fixed assets by late 2025.

Under accounting rules, CIP incurs no depreciation until ready for use, and some loan interest can be capitalized, avoiding immediate profit impact. Once transferred to fixed assets, depreciation and capitalized interest become financial expenses, directly reducing profits.

It's unclear whether the headquarters buildings meet operational criteria, but this approach raises questions about potential accounting gray areas. Future transfers to fixed assets will add predictable expenses to an already fragile profit statement.

Humanoid robots are still early-stage, with divergent technical and commercial paths.

The endgame remains unclear: Should firms first capture terminals with low barriers and then upgrade "brains," or first master industrial scenarios with robust "brains," using real-world data to build barriers before scaling?

Different paths imply different financial models. The former prioritizes asset-light operations, high turnover, and self-sufficiency, bolstering market confidence with nearer profit timelines. The latter is burdened by heavy assets and persistent losses.

UBTECH has set its finish line farther away. It must prove not just technical feasibility but also economic viability.

-

![]()

Weighing the Pros and Cons of In-House Chip Development: Most Automakers Shouldn't Feel Compelled to Pursue It

-

![]()

Can the Leapmotor D99 Gracefully Ascend into the Premium MPV Market as the Brand Climbs Higher?

-

Midea Bets 1 Billion Yuan on Liquid Cooling, Targeting AI Computing Power Market with 2027 Production Launch

-

Amidst Declining Profit Margins, Can Anwen Technology Sustain Its Edge in Automotive Cockpits?

-

![]()

5,000 Companion Robots Sold: Can UBTECH Breathe a Sigh of Relief?

-

![]()

NIO Maintains Brand Premium: Onvo Sets Minimum Price at 150,000 Yuan, Avoids Direct Competition with Leapmotor and BYD | MJ Pro

-

![]()

“From a 5-minute escape window to a zero-fire baseline, I finally feel confident driving an electric vehicle”

-

![]()

Profits Skyrocket! From Leasing to Construction: A Storage Enterprise with Hundred-Billion-Yuan Revenue Plans 1.175 Billion Yuan Investment in New Headquarters