Doubao Charges Fees: Zhang Yiming Helps Zhang Xiaolong Explore the Path

06/29 2026

06/29 2026

424

424

The key to future AI application competition lies not in choosing between B end and C end, but in whether one can excel in "AI foundation, traffic arena, and scenario hooks"—a robust technological base, a sufficiently large user base, and a deeply integrated scenario ecosystem.

Reported by Wan Tiannan

Edited by Chen Jiying

At a turning point for the monetization of domestic large models, Doubao, a ByteDance subsidiary, has taken the lead in exploring a paid model.

Anthropic has surged ahead, validating the monetization value of large models in the B end market. However, the viability of C end AI business models remains uncertain.

Even someone as bold as Elon Musk remains relatively cautious about C end AI. He predicts that C end membership subscriptions and advertising revenue will total just $1.36 trillion, accounting for less than 5% of the global AI market.

Nevertheless, Anthropic, which has thrived in the B end market, is now eyeing the consumer market. Since late last year, Anthropic has required its employees to enhance Claude's ability to handle daily inquiries related to health, travel, recipes, etc., and continuously improve the performance, completeness, and response speed of its chatbot.

Doubao, with 345 million monthly active users, is testing a paid model and also paving the way for WeChat, which boasts 1.4 billion users.

For Tencent, which has been slower to start, its biggest trump card for catching up in AI is WeChat. If Doubao can make it work, WeChat can too.

I. Doubao Charges Fees, Validating To C Monetization

As early as May, Doubao clarified its pricing: Standard version at 68 yuan/month, Enhanced version at 200 yuan/month, and Premium version at 500 yuan/month, with basic functions permanently free.

Paid users can experience more powerful models and gain additional usage quotas, including the office task mode powered by the latest Doubao 2.1 Pro, the expert mode with Doubao 2.1 Turbo, and high-computing functions such as AI PPT/spreadsheets, in-depth research, voice calls, and recording summaries, along with priority access during peak periods.

Compared horizontally, Doubao's pricing is not expensive. Competitors like Kimi, Zhipu, and MiniMax offer membership fees ranging from 49 to 79 yuan.

Doubao charges fees because it can no longer afford to burn money. ByteDance's capital expenditures in 2026 are expected to exceed 200 billion yuan, a 25% increase from previous plans, with the majority allocated to AI infrastructure construction. Calculations by Guolian Minsheng Securities show that, based on the cheapest Doubao model, the cost of providing one day of free AI services ranges from 132 million to 240 million yuan.

High investment, low return. According to LatePost, Doubao, with 200 million DAU in the first half of the year, generated less than 1 million yuan in daily revenue, while computing and operational costs could reach tens of millions of yuan per day.

Therefore, for Doubao, exploring commercialization is a necessary step.

Caijing Story purchased Doubao's 68 yuan standard service to try creating PPTs and building applications. The overall experience was that Doubao could efficiently build basic frameworks, but details were somewhat rough (rough), hallucinations persisted, and data was not precise enough.

We first gave Doubao instructions in free mode—"I am an industry analyst. Help me generate a PPT on the competitive analysis of mainstream AI large models in China."

The PPT generated by Doubao exhibited obvious hallucinations, such as humbly excluding ByteDance and claiming that "Alibaba and Baidu each dominate half of the market."

Under the standard paid office mode, Caijing Story generated another PPT on the same topic. This version had relatively accurate data, such as clarifying that Doubao has 345 million monthly active users.

In summary, both PPT versions had clear structures and beautiful visuals, but the data still required manual correction. Doubao's performance in application development and plan formulation was commendable, although human oversight remained essential.

Given this, the 68 yuan pricing is not expensive. Building a PPT framework alone can justify the membership fee.

Although the product system still has room for optimization and user willingness to pay is not fully mature, in the long run, model capabilities will continue to evolve, and these shortcomings will eventually be addressed.

Doubao's C end paid business primarily targets productivity tool value, covering high-frequency and efficient office scenarios such as intelligent PPT generation, batch data analysis, short video and film production, copy editing, and office automation.

These scenarios, distinct from ordinary casual conversations, offer strong practicality, efficiency gains, and clear ROI. User motivation to pay is purer, and willingness to pay is more stable, making it a shortcut for C end AI commercialization.

Previously, Kimi and MiniMax adopted a dual commercialization strategy targeting both B and C ends, catering to both enterprise services and individual users.

However, Doubao's fee charging holds different significance because its user base far exceeds that of Kimi and MiniMax, making it a national-level AI application. It is driving the AI large model industry from the wild "traffic acquisition" phase to a refined "value realization" phase.

Despite initiating fee charging attempts, Doubao has not abandoned its free basic services, thereby consolidating its massive C end user base.

This "basic free + advanced paid" model precisely aligns with the current user stratification characteristics of the domestic AI market: using free features to cultivate AI usage habits among the general public and paid features to screen high-value users and realize product value.

II. Zhang Yiming Paves the Way for Zhang Xiaolong

Doubao's foray into paid services signifies that domestic large model applications are bidding farewell to the era of pure traffic expansion and entering a new phase of value validation and paid conversion.

Previously, the core metrics of competition in the domestic AI industry focused on traffic dimensions such as DAU, monthly active users, user base, and traffic entry points. The free model lowered user barriers, quickly achieving market penetration and cultivating AI usage habits among the public.

However, as large models iterate and upgrade, high-order functions such as multimodal generation, complex logical reasoning, ultra-long text processing, and high-definition video generation incur exponentially increasing costs. Relying solely on free models, advertising monetization, and traffic subsidies cannot sustain long-term technological iteration and product optimization of large models.

C end AI pay (paid services) have become a global industry consensus. Domestic mainstream AI applications like Kimi and MiniMax have launched paid membership systems, while overseas leaders like OpenAI, Google, and Anthropic have fully implemented C end paid services.

If Doubao successfully monetizes, WeChat could be the biggest beneficiary—AI C end monetization positions WeChat as the largest potential king.

Both Doubao and WeChat boast massive user bases.

Leveraging ByteDance's ecosystem-wide traffic, Doubao's user base has exploded. According to QuestMobile, as of March 2026, domestic AI-native apps had 440 million monthly active users, with Doubao surpassing 345 million, far exceeding the combined total of the second-ranked Qianwen and third-ranked DeepSeek, leading by a wide margin.

WeChat, as a national-level app, boasts 1.4 billion users, covering users of all ages, scenarios, and circles, with nearly seamless scenario penetration.

However, their core strengths differ significantly.

Doubao's core strength lies in its AI-native user mindset. Users actively download and use AI products, with higher awareness, acceptance, and usage rates of AI functions than ordinary netizens, naturally aligning with AI paid conversion.

In short, Doubao represents pure AI-native traffic, while WeChat embeds AI capabilities into a super traffic arena, each with its pros and cons.

Domestically and internationally, the B end enterprise services business model has fully taken off, while the C end individual paid market remains fraught with uncertainty. Compared to mature paid mindsets among overseas users, domestic internet users have long been accustomed to free services and exhibit low willingness to pay for tool-based and AI-based products. C end commercialization has always been an industry-recognized challenge and the biggest hurdle for WeChat's AI ecosystem monetization.

Doubao's fee charging attempt represents a precise market test: while maintaining a free user base, it accurately screens high-value users willing to pay for efficiency and experience from the massive general user base, validating the land (implementation) of C end AI value.

This "cast a wide net, catch fish precisely" approach aligns with WeChat AI's monetization logic. "Initially, we provide free services and gradually generate revenue over time. In the AI field, we must find 'high-value users' and not just focus on daily active users," said a Tencent executive.

If Doubao successfully implements a domestic AI C end paid model, validating domestic users' AI paid mindset, payment threshold, and commercial sustainability, it will prove that WeChat AI, with its 1.4 billion users and full-scenario ecosystem, holds even greater commercial potential.

From this perspective, Zhang Yiming is essentially solving a proof problem for Zhang Xiaolong.

III. AI Foundation, Traffic Arena, Scenario Hooks

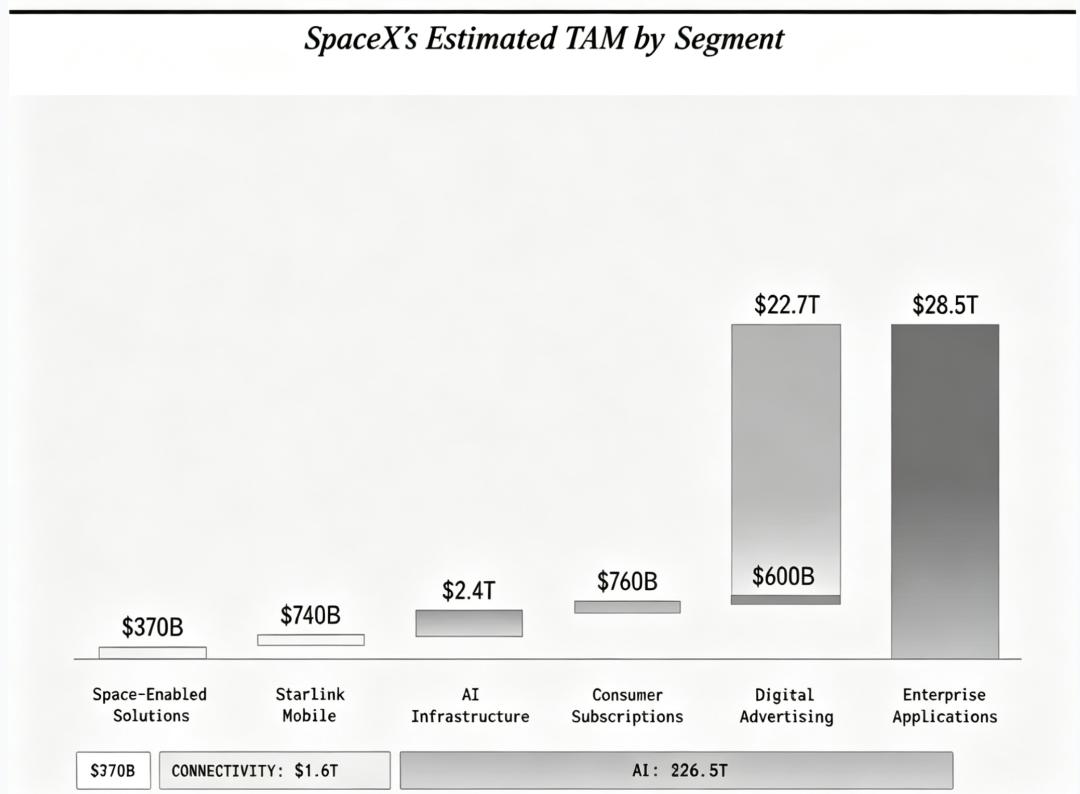

Elon Musk has publicly expressed pessimism about the commercial value of C end AI.

In SpaceX's prospectus, Musk predicted the global AI market: total market size will reach $28.5 trillion, with enterprise B end applications accounting for $22.7 trillion, AI infrastructure $2.4 trillion, and C end membership subscriptions and advertising revenue totaling just $1.36 trillion, far smaller than B end business.

However, this judgment appears somewhat hasty in the long run. Parallel To B and To C monetization may ultimately prevail.

The strategic layouts of global leading companies confirm this trend.

Anthropic initially targeted government and enterprise clients, providing professional B end AI services.

However, in the past six months, Anthropic has begun focusing on the C end consumer market.

Mike Krieger, co-lead of the company's lab team, publicly stated that since late 2025, Anthropic has required all employees to optimize Claude's C end service capabilities, focusing on refining life scenarios such as health consultations, travel planning, recipe recommendations, and daily companionship, continuously improving chat interaction quality, response speed, and problem-solving precision to enhance ordinary users' daily experience and fully capture the C end consumer market.

The growth of Anthropic's Claude Code also validates the value of B and C synergy—developers first use Claude Code to write daily code, which then enters enterprise teams' codebases, triggering company-wide unified procurement, permission configuration, and security compliance access. Personal usage habits transform into organizational processes, naturally permeating from To C to To B, establishing a conversion path from individual users to enterprise procurement.

The same logic applies to Doubao. If multiple employees within a company spontaneously use Doubao Pro, it could lead to organizational procurement at the enterprise level.

OpenAI is also pursuing a dual B and C integration strategy. On one hand, it relies on ChatGPT to firmly dominate the global C end AI market; on the other hand, it continues to ramp up B end enterprise services. According to the AI Index report released by third-party agency Ramp, in April 2026, 34.4% of enterprises were paying for Anthropic's products, while 32.3% were paying for OpenAI's.

In the future, B end professionalization and C end universalization will converge, becoming the core narrative of the AI industry.

C end massive users can continuously refine model general capabilities, optimize product interaction experiences, accumulate user data, and screen high-value paid users; while B end advanced technologies, professional computing power, and industry implementation experience can feed back into C end product upgrades, enhancing ordinary users' efficiency and service quality.

The key to future AI application competition lies not in choosing between B end and C end, but in whether one can excel in "AI foundation, traffic arena, and scenario hooks"—a robust technological base, a sufficiently large user base, and a deeply integrated scenario ecosystem.

Doubao's fee charging this time sets a price anchor, probing the overall commercialization temperature of China's AI large models. If the water is warm, ByteDance won't be the only one diving in—WeChat represents the biggest variable.

-

'Computing Power Leather' Surges 77% in 9 Days, NIO Supplier Also Chases the 'Light'

-

![]()

Storage and Computing Power Becoming Scarcer: Google Initiates Exploration of Using Old Smartphones to Build AI Servers

-

![]()

Storage Computing Power Grows Scarcer: Google Explores Using Old Smartphones for AI Servers

-

![]()

Huawei Imposes a $0.5 Patent Fee Per Device: Is It Time for Huawei to Reap Global Patent Royalties?

-

![]()

Geely Invests 1.8 Billion Yuan Post-Acquisition: The Launch of Flyme Auto 3.0 Sparks Questions on Meizu’s Enduring Influence

-

![]()

MBBF 2026 on the Bund in Shanghai: Deciphering Mobile AI's Future Trajectory

-

![]()

Commercialization of ASIC: The Turning Point Has Arrived

-

![]()

Doubao Charges Fees: Zhang Yiming Helps Zhang Xiaolong Explore the Path