WeiYi Zhizao Reports Revenue Growth Amid Net Profit Volatility, with Rising Debt Ratio as Baidu Exits

07/01 2026

07/01 2026

492

492

By Gangwan Business Observer, Shi Zifu

Changzhou WeiYi Zhizao Technology Co., Ltd. (hereinafter referred to as "WeiYi Zhizao") recently submitted its application to list on the Hong Kong Stock Exchange, aiming for a main board listing with Orient Securities International as its sponsor. The company initially filed its application in September 2025.

On November 14, 2025, the China Securities Regulatory Commission (CSRC) requested supplementary materials for WeiYi Zhizao's overseas listing application, demanding clarifications on eight key issues: the identification of controlling shareholders, the progress of state-owned asset management procedures, the pricing rationale for new shareholders' equity stakes, the reasons for inconsistencies in the listing plan, details of equity incentives, the business operation model, the actual conduct and specifics of advertising operations, and whether the shares proposed for "full circulation" are subject to pledges, freezes, or other rights restrictions.

For this initial public offering (IPO), WeiYi Zhizao plans to allocate the raised funds primarily towards the research and development (R&D) of core technologies, establishing localized overseas sales and service networks, strategic investments and acquisitions, expanding production capacity, and for working capital and other general corporate purposes.

1. Sustained Revenue Growth Amid Significant Net Profit Fluctuations

Founded in 2018, WeiYi Zhizao is a leading enterprise in the industrial embodied intelligent robot (EIIR) sector, committed to transforming manufacturing through cutting-edge technologies and shaping the future of the global workforce. The company offers globally deployable and highly flexible EIIR products and solutions. Leveraging its self-developed full-stack software and hardware systems and comprehensive systems engineering capabilities, WeiYi Zhizao has successfully developed EIIR products capable of autonomous perception, learning, decision-making, and execution of complex tasks.

During the performance record period, WeiYi Zhizao's revenue primarily came from the sales of EIIR and AI-enabled intelligent and modular products.

From 2023 to 2025 (hereinafter referred to as the "reporting period"), revenue from EIIR products amounted to RMB 114 million, RMB 272 million, and RMB 453 million, accounting for 26.3%, 45.3%, and 57.0% of total revenue, respectively. Revenue from AI-enabled intelligent products was RMB 203 million, RMB 205 million, and RMB 209 million, representing 46.9%, 34.1%, and 26.3% of total revenue, respectively. Revenue from modular products reached RMB 96.457 million, RMB 112 million, and RMB 127 million, accounting for 22.2%, 18.7%, and 16.0% of total revenue, respectively.

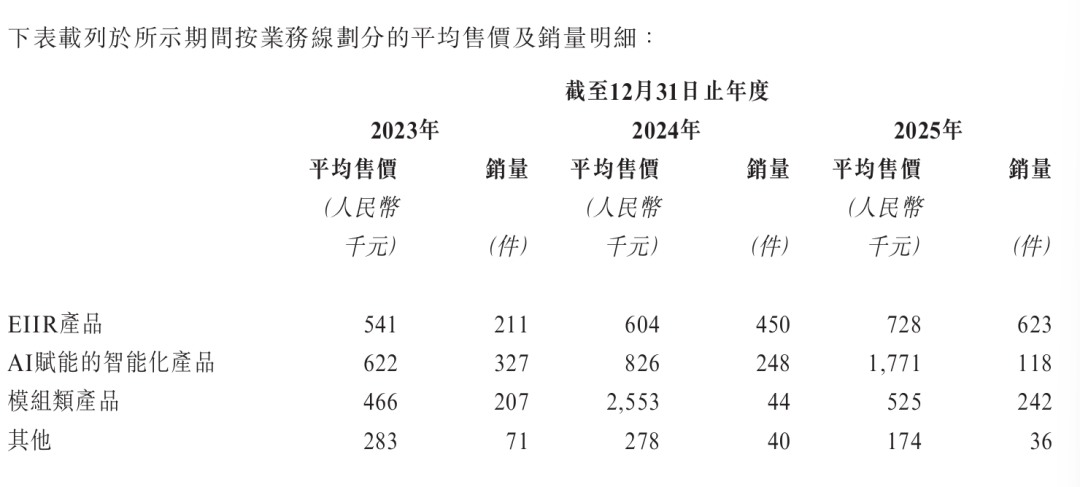

By business line, during the reporting period, the average selling price (ASP) of EIIR products was RMB 541,000, RMB 604,000, and RMB 728,000, with sales volumes of 211, 450, and 623 units, respectively. The ASP of AI-enabled intelligent products was RMB 622,000, RMB 826,000, and RMB 1.771 million, with sales volumes of 327, 248, and 118 units, respectively, showing a continuous decline in sales despite price increases.

During the same period, the ASP of modular products was RMB 466,000, RMB 2.553 million, and RMB 525,000, with sales volumes of 207, 44, and 242 units, respectively, exhibiting significant fluctuations in both ASP and sales volume.

From a gross profit margin perspective, EIIR and AI-enabled intelligent products saw significant improvements during the period. The gross profit margin for EIIR products was 47.9%, 55.1%, and 53.5%, respectively, while that for AI-enabled intelligent products was 35.2%, 47.5%, and 44.4%, respectively. WeiYi Zhizao attributed the improvement in gross profit margins of its main products to product mix optimization and enhanced operational efficiency from proprietary technology upgrades.

During the reporting period, WeiYi Zhizao's gross profit was RMB 184 million, RMB 287 million, and RMB 385 million, with gross profit margins of 42.4%, 47.9%, and 48.4%, respectively, showing an overall upward trend.

Due to improvements in gross profit and margins, as well as enhanced operational efficiency from product mix optimization and proprietary technology upgrades, WeiYi Zhizao's net profit turned from negative to positive during the period. The company reported revenues of RMB 434 million, RMB 600 million, and RMB 796 million, with total comprehensive income for the year of RMB -114 million, RMB 15.612 million, and RMB 5.052 million, respectively. Adjusted net profit (non-IFRS measure) was RMB -28.112 million, RMB 44.146 million, and RMB 48.726 million, respectively.

In 2023, WeiYi Zhizao incurred a loss of RMB 114 million, primarily due to high R&D investment of RMB 178.3 million (41% of revenue) focused on developing its core full-stack software and hardware systems.

The company returned to profitability in 2024. In 2025, net profit decreased to RMB 5.1 million, mainly due to increased investment in high-performance computing resources and R&D personnel to support large model development, leading to sustained growth in R&D expenditure.

In terms of specific expenses, during the reporting period, WeiYi Zhizao's R&D expenditure was RMB 178 million, RMB 165 million, and RMB 235 million, accounting for 41.01%, 27.5%, and 29.52% of revenue, respectively. Selling expenses were RMB 49.756 million, RMB 31.314 million, and RMB 38.791 million, representing 11.47%, 5.22%, and 4.87% of revenue, respectively. General and administrative expenses were RMB 60.733 million, RMB 42.032 million, and RMB 80.32 million, accounting for 14%, 7.01%, and 10.09% of revenue, respectively.

During the performance record period, WeiYi Zhizao's R&D expenditure included employee benefits and share-based compensation for R&D personnel, computing costs, depreciation expenses, raw material consumption, and other expenses. In 2023 and 2024, R&D expenditure increased by -7.5% and 42.8% year-on-year, respectively. The decline in the 2023 R&D expense ratio was due to team restructuring and a RMB 33.5 million reduction in share-based compensation, partially offset by a RMB 23.5 million increase in computing costs to support continued in-depth R&D in embodied intelligence. The 2024 increase was mainly due to enhanced R&D in high-speed visual servo systems and integrated visual inspection platforms for industrial robots.

Regarding the sustainability of profitability, WeiYi Zhizao stated in its prospectus that it may continue to incur net losses in the short term as it is in the business expansion and operational phase of rapid growth in the industrial intelligent robot sector, with ongoing R&D investments. The company believes future revenue growth will depend on its ability to develop new technologies, enhance customer experience, establish effective commercialization strategies, compete effectively, and develop new products and solutions. As the company continues to expand its business and operations and invest in R&D activities, its costs and expenses may continue to rise in the future.

Song Xiangqing, Vice President of the China Business Economics Society, stated that WeiYi Zhizao's profitability and cash flow challenges are typical of hard-tech startups characterized by high investment, long cycles, and strong expansion, with the core issue being the lag in large-scale implementation (scaled deployment) compared to upfront investments. Net profit fluctuated from a loss of RMB 114 million in 2023 to a profit of RMB 15.739 million in 2024, then fell to RMB 5.066 million in 2025, driven by sustained high R&D investment, continuous spending on embodied intelligence technology iteration and scenario deployment, resulting in inherently fragile profitability.

2. Improvement in Operating Cash Flow, Rising Debt Ratio

During its business development, WeiYi Zhizao also faced high concentration in its upstream and downstream sectors.

During the reporting period, revenue from WeiYi Zhizao's top five customers was RMB 227 million, RMB 169 million, and RMB 303 million, accounting for 52.4%, 28.3%, and 38.1% of total revenue, respectively. Revenue from its largest customer was RMB 58.6 million, RMB 42 million, and RMB 74.6 million, representing 13.5%, 7.0%, and 9.4% of total revenue, respectively.

During the same period, the company's purchases from its top five suppliers amounted to RMB 203 million, RMB 186 million, and RMB 362 million, accounting for 64.1%, 46.6%, and 42.4% of total purchases, respectively. Purchases from its largest supplier were RMB 51.9 million, RMB 50.3 million, and RMB 105 million, representing 16.4%, 12.6%, and 12.2% of total purchases, respectively.

While facing high customer concentration, WeiYi Zhizao also encountered credit risks associated with delayed payments and defaults from customers, distributors, or related parties. As of the end of each reporting period, the company's trade receivables and bills receivable were RMB 387 million, RMB 615 million, and RMB 464 million, respectively.

As of the end of each reporting period, the company's inventories were RMB 45.743 million, RMB 77.553 million, and RMB 110 million, respectively, with inventory turnover days of 43, 72, and 83 days, and inventory turnover ratios of 8.5, 5.1, and 4.4, respectively.

As of the end of each reporting period, net cash flow from operating activities was RMB -105 million, RMB -154 million, and RMB 141 million, respectively. The company recorded cash outflows for two consecutive years in 2023-2024, followed by cash inflows in 2025.

Regarding the cash inflows in 2025, the company stated that the net change in working capital was primarily due to a RMB 124.2 million decrease in trade receivables and bills receivable, other receivables, and prepayments; a RMB 97.3 million increase in trade payables and bills payable, other payables, and accrued expenses; and a RMB 35.5 million increase in contract liabilities.

Song Xiangqing noted that in terms of cash flow, operating cash flow showed continuous net outflows in 2023-2024 (RMB -105 million, RMB -154 million), mainly due to a surge in credit sales amid business expansion, with trade receivables exceeding RMB 1.46 billion over three years, coupled with slowed inventory turnover, resulting in significant capital occupation by upstream and downstream parties, trapping the company in a cycle of "revenue growth—credit sales expansion—cash flow pressure." Operating cash flow turned positive to RMB 141 million in 2025, indicating initial success in scaled product deployment, but profit quality and cash flow stability remain to be verified. Its IPO essentially aims to alleviate capital pressure through the capital market to support technological iteration and market expansion. Investors should closely monitor improvements in subsequent receivables recovery, gross profit margin stability, and R&D investment return ratios.

In terms of solvency, as of the end of each reporting period, the company's current ratio was 0.9, 1.1, and 1.2, respectively, with quick ratios of 0.8, 1.0, and 0.6, and debt-to-asset ratios of -21.9%, 40.8%, and 56.4%, respectively.

Other financial data showed interest coverage ratios of -3.3%, 1.6%, and 1.1%, debt-to-equity ratios of -40.9%, 75.3%, and 0.6%, and net debt-to-equity ratios of -39.2%, 73.8%, and 0.4%, respectively, during the reporting period.

3. Potential Goodwill Risk, Baidu Cashes Out

As of the last practicable date, Zhang Zhiqi and Pan Zhengyi, acting in concert, collectively held approximately 31.78% of the shares, serving as the company's actual controllers.

Since its establishment in 2018, WeiYi Zhizao has completed several rounds of financing, including Series A, Series B, acquisition of Jiangsu Zhiyun Tiangong, financings in April-May 2024, December 2024, and April 2025. The company issued ordinary shares to investors and entered into separate agreements with shareholders, granting them redemption rights, anti-dilution rights, liquidation preferences, and other rights (collectively referred to as "redeemable rights").

Regarding the acquisition of Jiangsu Zhiyun Tiangong, which occurred in December 2022, WeiYi Zhizao's product mix underwent significant changes post-acquisition. Before the acquisition, revenue primarily came from AI-enabled intelligent products; after the acquisition, the company strategically expanded into EIIR products, which became an increasingly important contributor to total revenue.

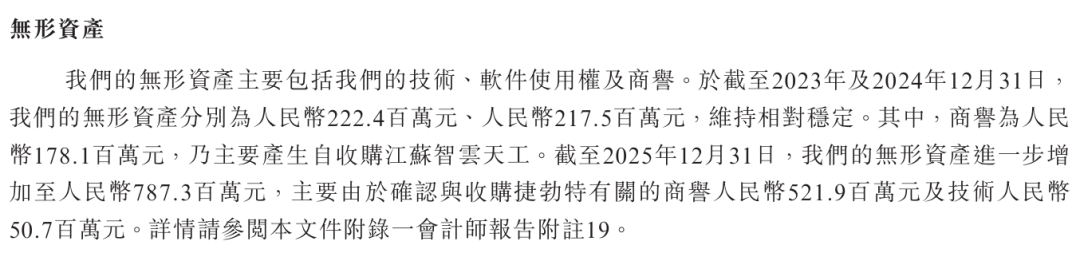

Due to the acquisition of Jiangsu Zhiyun Tiangong, WeiYi Zhizao also incurred significant goodwill impairment. As of the end of 2023 and 2024, the company's intangible assets were RMB 222 million and RMB 218 million, respectively, with goodwill of RMB 178 million in 2023, primarily from the acquisition of Jiangsu Zhiyun Tiangong. As of the end of 2025, WeiYi Zhizao's intangible assets further increased to RMB 787 million, mainly due to the recognition of RMB 521.9 million in goodwill and RMB 50.7 million in technology related to the acquisition of Jiebote.

Given the high level of goodwill, there is a risk of goodwill impairment if the acquired assets underperform.

In addition to its own goodwill, WeiYi Zhizao's related-party transactions with Jiangsu Zhiyun Tiangong also drew external concern. In 2022, Jiangsu Zhiyun Tiangong was WeiYi Zhizao's largest customer, contributing 20.9% of total revenue.

Moreover, during WeiYi Zhizao's previous financing rounds, Baidu, a prominent capital provider, was undoubtedly a focal point. Baidu's full exit on the eve of this IPO sparked widespread discussion.

On October 31, 2019, Baidu Online subscribed to RMB 3.0899 million in additional registered capital for RMB 25.3 million in Series A financing. On July 8, 2022, Baidu Online transferred 3% and

-

![]()

Big Company HR Departments Are Overwhelmed: Young Job Seekers Harness Agents, AI-Assisted Interviews Spark Controversy

-

![]()

SAIC MG General Manager Overwhelmed by Online Backlash, Ends Livestream Prematurely: A Blend of Unfairness and Fairness

-

![]()

Hong Kong Stock IPO丨Recon Technology: The First Embodied Visual Intelligence Stock in Hong Kong Stock Market Launches Offering Without Cornerstones or Green Shoe Option

-

![]()

Avita Reapplies for Listing: Reports 25.6 Billion Yuan in Revenue and 3.49 Billion Yuan in Net Loss for the Previous Year, with 182 Million Yuan in Dividends from Yinwang | MIRROR Pro

-

![]()

DataStory's Controversial Hong Kong IPO: 5 Billion Valuation Hangs in the Balance Amid 866 Million Debt Pressure

-

![]()

Apple’s Prices Skyrocket Up to 3,500 Yuan! Who Empowered Cook to Hike Prices?

-

![]()

ByteDance Executives Go Viral!

-

![]()

ByteDance Executives Dominate Headlines!