Hong Kong Stock IPO丨Recon Technology: The First Embodied Visual Intelligence Stock in Hong Kong Stock Market Launches Offering Without Cornerstones or Green Shoe Option

07/01 2026

07/01 2026

423

423

Designer 丨 Tian

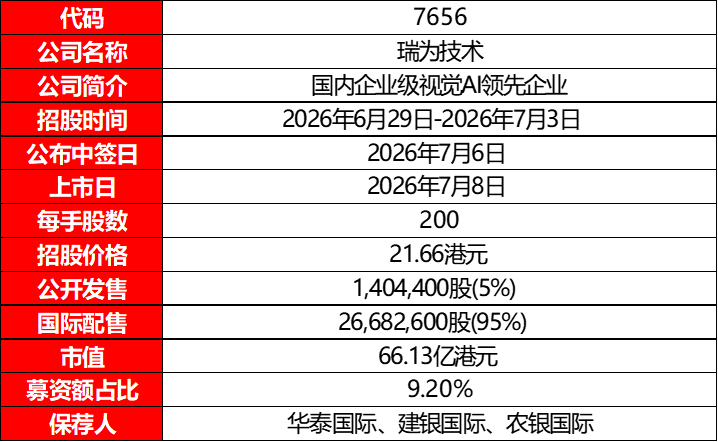

Offering Details

Source: Prospectus

Source: Prospectus

Financial Situation

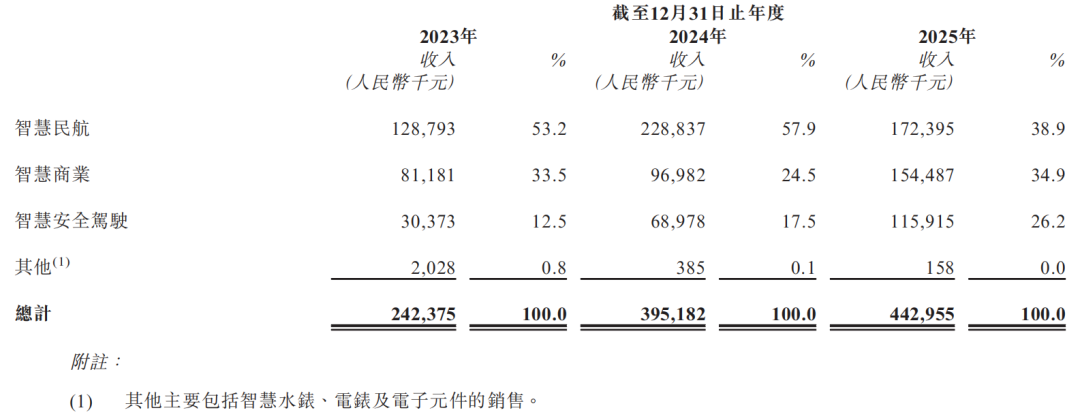

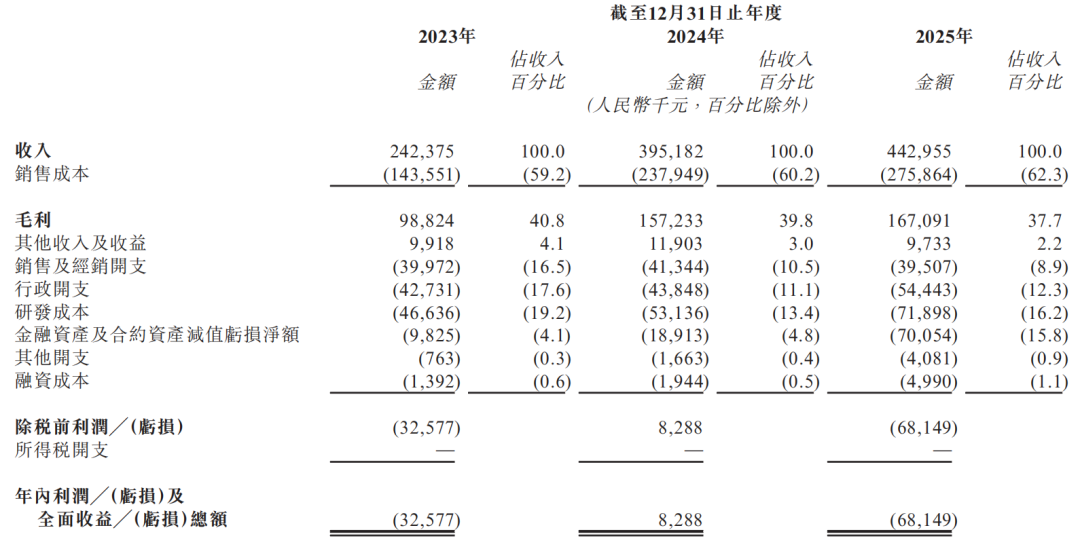

Recon Technology achieved revenues of RMB 242 million, RMB 395 million, and RMB 443 million in 2023, 2024, and 2025, respectively. In 2024, it experienced a 63% surge in growth driven by the concentrate delivery (centralized delivery) of smart civil aviation projects. However, growth significantly slowed to 12% in 2025, indicating a marked decline in momentum. The revenue structure underwent significant shifts over the three years. The revenue share from its foundational smart civil aviation business dropped from 53.2% to 38.9%, with an absolute revenue decline of nearly 25% in 2025, signaling a contraction in its traditional core business. Smart commercial and smart safety driving segments emerged as the primary growth drivers, with their revenue shares increasing to 34.9% and 26.2%, respectively. The safety driving business nearly doubled in compound annual growth over three years, yet its scale remains insufficient to fully offset the decline in civil aviation revenue.

Source: Prospectus

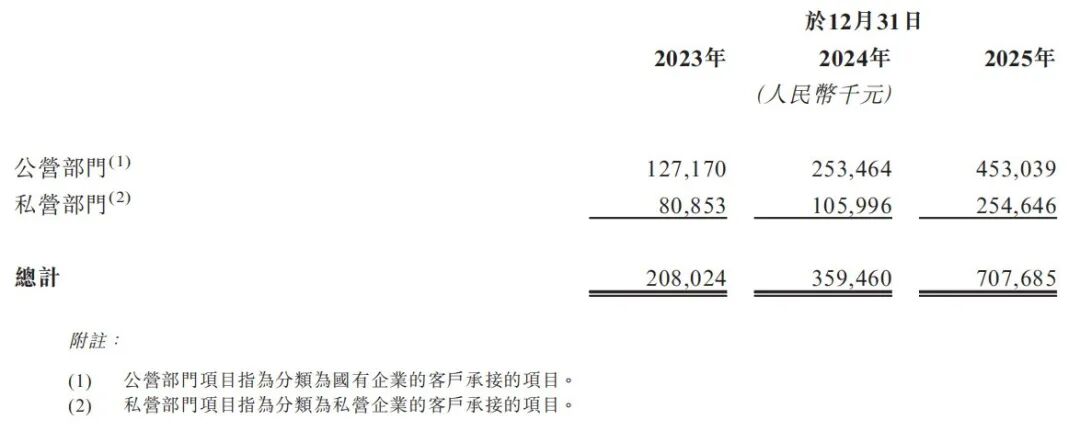

The company exhibits extremely high customer concentration, with the top five customers accounting for 59.1%, 73.5%, and 60.3% of revenue in 2023, 2024, and 2025, respectively. In 2024, there was a pronounced reliance on a single major customer, which improved in 2025 due to business diversification, with the revenue share from the largest customer dropping from 31.7% to 14.4%. The prolonged payment approval processes and slow settlement cycles characteristic of downstream public sector and state-owned enterprise clients directly impacted the company's operational cash flow, being the primary reason for extended payment collection periods.

Source: Prospectus

The overall gross profit margin showed a consistent downward trend, decreasing from 40.8% in 2023 to 37.7% in 2025. This decline was not primarily driven by a drop in product profitability but rather by shifts in the business mix. The revenue share of the high-margin smart civil aviation business continued to shrink, while the rapidly expanding intelligent safety driving business, with a low gross margin of only 16.4%, increased its share, continuously pulling down the company's overall profitability.

Source: Prospectus

Expense trends were divergent, with the sales expense ratio continuously optimizing from 16.5% in 2023 to 8.9% in 2025, reflecting improved channel efficiency and deeper customer engagement. However, R&D and administrative expense ratios rose simultaneously, reaching 16.2% and 12.3% in 2025, respectively. The company's profitability was highly volatile, achieving a brief small profit in 2024 before expanding to a net loss of RMB 68.15 million in 2025. The core driver of the loss was not a deterioration in core business operations but rather a RMB 70.05 million impairment loss on financial assets (primarily provisions for expected credit losses on trade and other receivables, net of any reversals, under the expected credit loss model) in that year, accounting for 15.8% of revenue. The concentrated release of accounts receivable bad debt risks directly eroded current profits. Even after excluding non-recurring items such as share-based payments and listing expenses, the adjusted net loss still approached RMB 49 million.

Source: Prospectus

The core operational risk lies in accounts receivable. As of the end of 2025, the company's trade receivables balance reached RMB 587 million, 1.32 times the annual revenue. The trade receivables turnover days surged from 200 days in 2023 to 440 days, with an average payment collection period exceeding 14 months. The continuously lengthening payment terms and receivables scale far exceeding revenue scale suggest a potential for further bad debt risks. In contrast, inventory management efficiency continuously improved, with inventory turnover days dropping significantly from 174 days to 45 days. However, the efficiency gains in inventory were entirely offset by the deterioration in accounts receivable, causing the company's cash conversion cycle to increase from 150 days in 2024 to 161 days, with overall working capital occupancy remaining high.

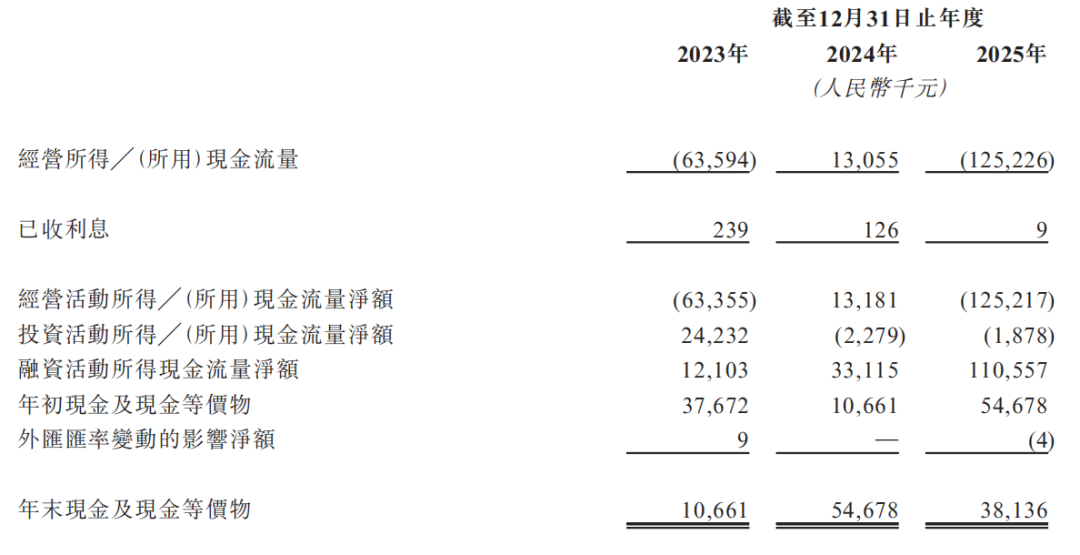

Cash flow and liquidity pressures represent the company's most prominent financial weaknesses. Operating cash flow has been significantly negative for two consecutive years, with a net outflow of RMB 125 million in 2025, severely diverging from reported profits. This is inherently tied to the business model of "financing projects upfront," where revenue growth primarily manifests as an accumulation of accounts receivable rather than genuine cash inflows. Liquidity constraints are even more pressing. As of the end of 2025, the company's cash and cash equivalents stood at just over RMB 38 million, while short-term interest-bearing borrowings reached RMB 151 million. Cash reserves were insufficient to cover short-term debt, leaving daily operations highly dependent on external financing. A significant portion of this IPO's proceeds will be used to supplement liquidity and alleviate funding pressures.

Source: Prospectus

Comprehensive Assessment

Market Capitalization

HKD 6.613 billion.

Valuation

Based on business model, financial metrics, and industry positioning, this analysis selects Maxvision Technology, Rongming Technology, and Cloudwalk Technology as comparable companies for Recon Technology.

Maxvision Technology

A leading domestic enterprise in the smart port sector, with over two decades of expertise in port intelligence. It primarily provides integrated smart port inspection system solutions, covering all types of ports—air, land, and water. Its product range includes passenger self-service inspection channels, intelligent vehicle supervision systems, customs quarantine equipment, and intelligent inspection robots. It deeply serves the General Administration of Customs, border inspection agencies, and major airport groups across China, being a core supplier for intelligent transformations at domestic airport ports. The company has also extended its layout (layout) into smart airports, intelligent transportation, and commercial robotics, with products deployed in multiple overseas ports, boasting strong barriers to entry in terms of scenario-specific qualifications.

Rongming Technology

A globally leading provider of visual AI solutions for commercial vehicles, focusing on enhancing safety and operational efficiency. Its product portfolio includes three main matrices: in-vehicle video surveillance equipment, AI-assisted driving systems, and fleet risk control management platforms, covering functions such as driver state monitoring, blind spot warnings, and driving trajectory control. These solutions are applied in freight logistics, public transportation, school buses, mining vehicles, and other scenarios. The company holds a leading market share in global commercial vehicle video equipment, with business operations spanning over a hundred countries and regions, and overseas markets being a significant revenue source.

Cloudwalk Technology

A top domestic AI platform company and one of the "Four Little Dragons of AI." It independently develops a human-machine collaboration operating system and the Congrong large model, using computer vision as its core technological foundation to provide full-stack AI solutions across smart finance, smart cities, smart transportation, and smart commerce. In the smart transportation sector, it covers over a hundred domestic civil airports, offering intelligent solutions for security screenings, passenger services, and security control. It is a key benchmarking company for Recon Technology in the civil aviation sector while continuously advancing the implementation of multimodal large models and embodied intelligence technologies.

Source: iFinD, Zhenyan Factory

Source: iFinD, Zhenyan Factory

Note: 1 HKD = 0.8624 RMB

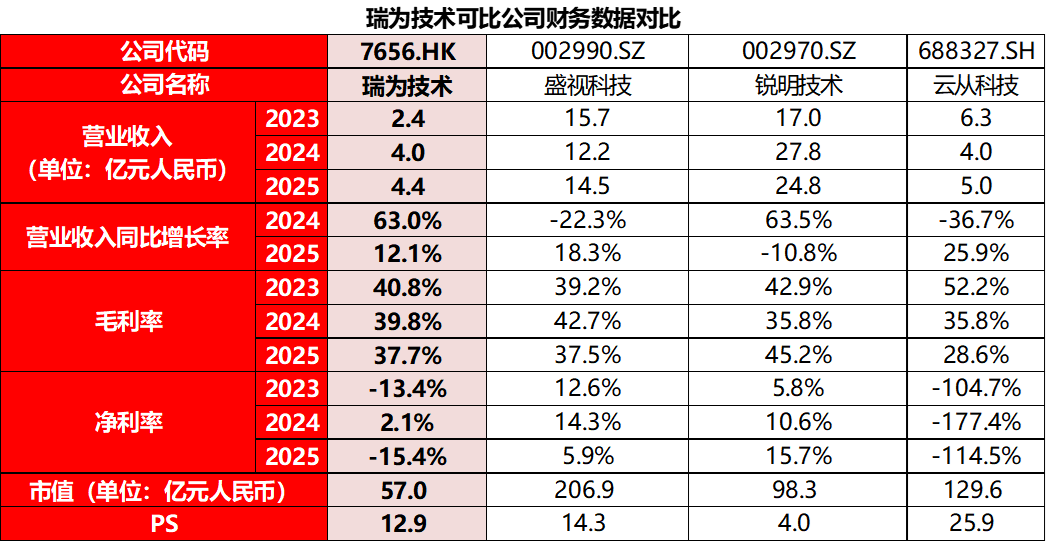

Recon Technology has the smallest revenue scale among the four comparable companies, positioning it as a small-to-medium-sized growth player in a niche segment. In terms of growth, the revenue growth rates of the four companies reflect distinct industry cycle misalignments. In 2024, Recon Technology and Rongming Technology both achieved approximately 63% high growth, with the former benefiting from the Centralized delivery (centralized delivery) of smart civil aviation airport projects and the latter from the recovery of the commercial vehicle industry and overseas market expansion. Meanwhile, Maxvision Technology and Cloudwalk Technology saw revenue declines, dragged down by lulls in port construction projects and budget cuts from government and enterprise clients, respectively. In 2025, the growth landscape reversed, with Maxvision and Cloudwalk rebounding to positive growth of 18.3% and 25.9%, respectively, corresponding to the restart of port bidding cycles and demand recovery driven by large model implementations. Recon Technology's growth slowed to 12.1%, primarily due to revenue contraction in its civil aviation core business, with new businesses insufficient to offset the decline. Rongming Technology saw a negative growth of 10.8%, affected by the downturn in the commercial vehicle cycle. This misalignment fundamentally stems from the asynchronous industry cycles of each company's core businesses, with companies in more project-driven sectors experiencing sharper revenue volatility.

Recon Technology's overall gross profit margin of 37.7% in 2025 places it in the mid-range among comparable companies, roughly on par with Maxvision Technology, lower than Rongming Technology, and higher than Cloudwalk Technology. The margin differences are inherently determined by business structure and competitive landscape. Rongming Technology's high margins stem from its channel barriers and product premiums in overseas commercial vehicle markets, where competition is less intense than in domestic markets, and economies of scale continue to unfold. Cloudwalk Technology's margins have been declining annually as its compute infrastructure business rapidly scales up in 2025. This business, still in its early market expansion phase, has relatively low margins, compounded by rising hardware procurement costs, dragging down the overall margin. The similar margins between Recon Technology and Maxvision Technology reflect their shared focus on high-barrier civil aviation/port scenarios, where project-based deliveries inherently carry high margins. However, Recon Technology's margins have been trending downward due to the rising revenue share of its low-margin smart safety driving business, which structurally pulls down overall profitability.

Recon Technology exhibits extreme net profit margin volatility, with profit stability significantly weaker than that of Maxvision Technology and Rongming Technology, though its loss magnitude is smaller than that of Cloudwalk Technology. Maxvision and Rongming have achieved consistent and stable profitability, thanks to their mature business models, well-established supply chain and channel systems, and relatively controllable impairment pressures on accounts receivable. Cloudwalk Technology's substantial losses stem from the high R&D investments and personnel costs inherent to general-purpose AI platforms, a characteristic phase for technology platform companies. Recon Technology's losses are not due to unprofitable core operations but rather to significant impairment losses on accounts receivable in a given year, reflecting the concentrated release of bad debt risks from its high proportion of downstream public sector clients and project financing models. Its core business margins can generally cover period expenses.

Recon Technology's offering price corresponds to a price-to-sales (PS) ratio of 12.9x, lower than Cloudwalk Technology's 25.9x and Maxvision Technology's 14.3x but higher than Rongming Technology's 4.0x. Rongming Technology's 4x PS ratio represents a typical valuation for mature hardware manufacturing, with market discounts reflecting the strong cyclicality and growth ceilings of the commercial vehicle sector. Cloudwalk Technology's high PS valuation incorporates a growth premium for its general-purpose large models and full-scenario AI platform, pricing in long-term technological potential. Recon Technology's 12.9x PS ratio falls between hardware and pure AI players, enjoying a growth premium from its visual AI and embodied intelligence layout (layout) while also facing discounts due to high profitability volatility, significant payment collection risks, and relatively small scale. Subsequent valuation flexibility will depend on factors such as the pace of fundamental recovery and the commercialization progress of new businesses.

Listing Team

Source: Prospectus

The company's listing sponsors are Huatai International, CCB International, and ABC International.

Huatai International has historically sponsored 77 listed projects, with 43 gaining, 31 declining, and 3 remaining flat in the gray market (grey market); the break rate was 40.26%. On the first day (listing day), there were 40 gains, 29 declines, and 8 flats, with a break rate of 37.66%.

Source: Chitose Trading Pro

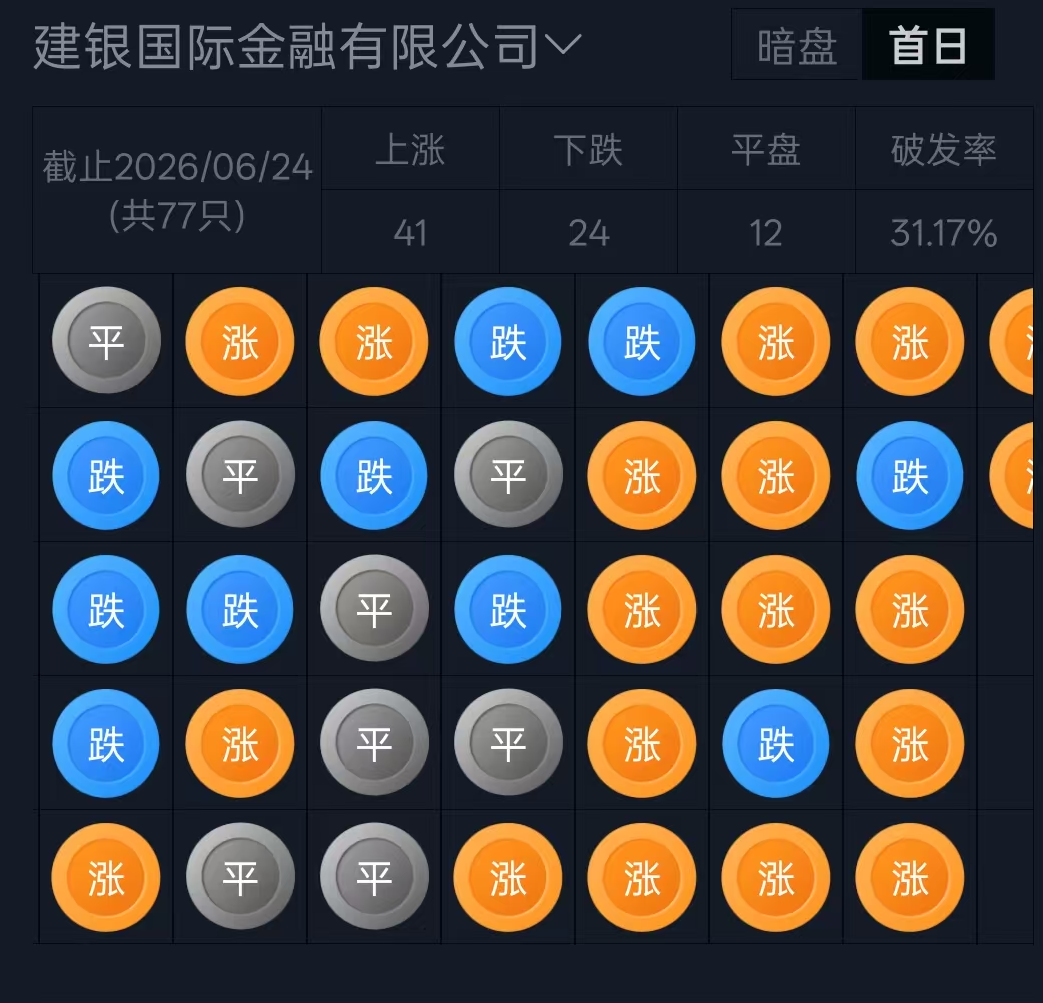

CCB International has historically sponsored 77 listed projects, with 36 gaining, 20 declining, and 21 remaining flat in the grey market; the break rate was 25.97%. On the listing day, there were 41 gains, 24 declines, and 12 flats, with a break rate of 31.17%.

Source: Chitose Trading Pro

ABC International has historically sponsored 44 listed projects, with 24 gaining, 18 declining, and 2 remaining flat in the grey market; the break rate was 40.91%. On the listing day, there were 25 gains, 12 declines, and 7 flats, with a break rate of 27.27%.

Source: Chitose Trading Pro

Over-Allotment Option

This offering does not include a green shoe option.

Offering Size Adjustment Option

This offering does not include an offering size adjustment option.

Callback Mechanism

This IPO adopts Mechanism C for issuance.

Cornerstone Investors

There are no cornerstone investors for this issuance.

Pre-IPO Financing

Since its inception, the company has undergone multiple rounds of financing, involving investment institutions such as Intel Capital, China Merchants Capital, SAIF Partners, Greenland Financial Holdings, Shanghai Airport Hongyu Capital, CITIC Securities Investment, and other renowned domestic and international industrial capital and top-tier investment institutions. The total amount raised exceeds RMB 1 billion. After the final Series E financing round in 2025, the company's post-money valuation reached approximately RMB 3.55 billion.

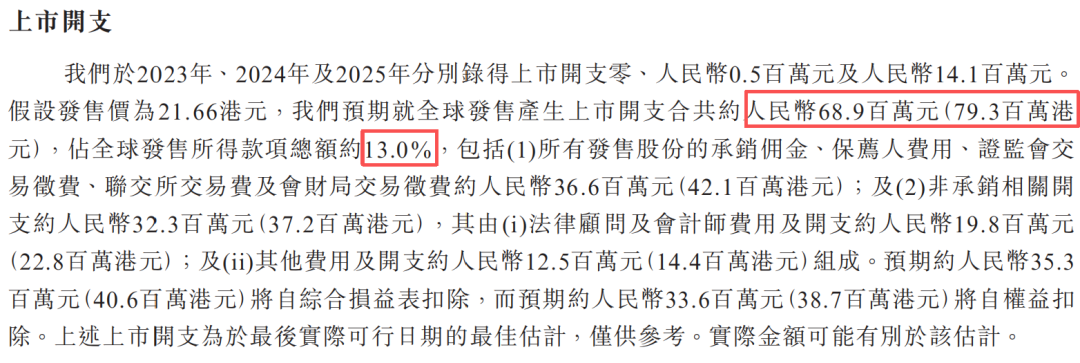

Listing Expenses

Based on the mid-price of the offering at HKD 21.66, the total estimated expenses for this issuance are approximately HKD 79.3 million, accounting for 13.0% of the total funds raised.

Source: Prospectus

Analysis on Whether to Subscribe

From a fundamental perspective, Reware Technology is a leader in China's enterprise-level visual AI civil aviation niche market. Its core strengths lie in the strong barriers of civil aviation scenarios and the cross-scenario reuse capabilities of its full-stack technology. The nearly 60% gross margin in its civil aviation business forms a solid foundation for profitability. Building on this, the company has successfully expanded into two major growth areas: smart commerce and smart safety driving. Its revenue structure has shifted from reliance on a single civil aviation segment to a tripartite balance, with the proportion of non-civil aviation business increasing by over 14 percentage points in three years, demonstrating strong scenario replication capabilities. Technologically, the company has independently developed visual large models and VTFLA embodied large models, pioneering the commercialization of products such as baggage transfer robots. It holds a first-mover advantage in the industry trend of AI transitioning from perception to execution. However, the company's financial quality and operational risks also warrant attention: profitability is highly volatile, with a swing from profit to loss in 2025 due to significant provisions for impairment of accounts receivable. The 440-day turnover period suggests further potential for bad debt risks to materialize. Cash flow pressures are even more pronounced, with consecutive large net outflows in operating cash flow. The company holds less than RMB 40 million in cash on hand while carrying RMB 150 million in short-term borrowings, making liquidity highly dependent on external financing. Additionally, issues such as high customer concentration and the rising proportion of low-margin businesses also constrain improvements in profit quality.

From a structural perspective, this IPO is jointly sponsored by Huatai, CCB International, and ABC International, with no cornerstone investors or green shoe option. Post-listing, there will be neither institutional lock-up support nor underwriter price stabilization buffers, resulting in higher stock price volatility risks. Issued under Chapter 18C with a 20% clawback, the public offering comprises 28,088 lots, representing a relatively small supply. With an issued H-share market capitalization of HKD 5.929 billion, a 71.3% increase would be required to reach the Stock Connect threshold of HKD 10.156 billion (data from Live Reports).

From a market sentiment perspective, 16 new listings are currently open for subscription, with 6 overlapping with Reware Technology's subscription period, leading to significant capital diversion. As the 'first visual embodied AI stock listed in Hong Kong,' Reware Technology benefits from the overall heat of the AI sector and has certain potential for speculative trading. However, the company's lack of cornerstone investors and green shoe option, combined with fundamental flaws such as volatile profitability, high accounts receivable, and cash flow pressures, suggest significant post-listing stock price volatility. As of 18:00 on June 30, 2026, the public offering was oversubscribed by 154.21 times. Interested investors may continue to monitor the project's subscription enthusiasm and listing performance.

Disclaimer:

1. This article is compiled solely based on publicly available information and aims to provide factual observations and industry research references. It does not constitute any form of investment advice or offer to buy or sell securities. Data related to companies, stock prices, valuations, market shares, etc., mentioned herein are sourced from publicly disclosed documents by the issuer, HKEX's Disclosure Easy, public news reports, and third-party research. This account makes no explicit or implicit guarantees regarding their completeness or accuracy.

2. Any investment decisions made by readers based on this information are at their own risk and consequence. Regulatory requirements differ between the Hong Kong and mainland markets, and cross-border investments require attention to policy, exchange rate, liquidity, and compliance risks.

3. Investment involves risks; decisions should be made with caution.

-

![]()

The imaging capabilities of smartphones are continuously improving, but why are there more and more 'add-ons' for shooting?

-

![]()

Alibaba's AI 'Crucible': Navigating Overseas Blockades, Organizational Upheaval, and the Lag in Commercialization

-

![]()

Global Electric Vehicles Enter the '23 Million Unit Era': China Maintains Edge, Emerging Markets as New Growth Pole

-

Meituan Triumphs with Domestic Computing Power: Running a Trillion-Parameter Model, Exploration Initiated in 2023

-

![]()

Embodied Intelligence and Mobile Robots: Why the Intensified Focus on Factories This Year

-

"Chip" Radiance Persists: Is the Semiconductor Sector Still a Magnet for Investors?

-

![]()

Robots Embark on 200-Hour Factory Trials: Is AI Truly Ready for Industrial Deployment?

-

![]()

Another Bionic Robot Company Secures $7 Million in Funding