The AI Industry Chain: A Tale of Fire and Ice - Upstream Thrives, Downstream Struggles

07/03 2026

07/03 2026

383

383

Who's Making All the Money in AI?

The AI industry chain suffers from a severe imbalance in profit distribution.

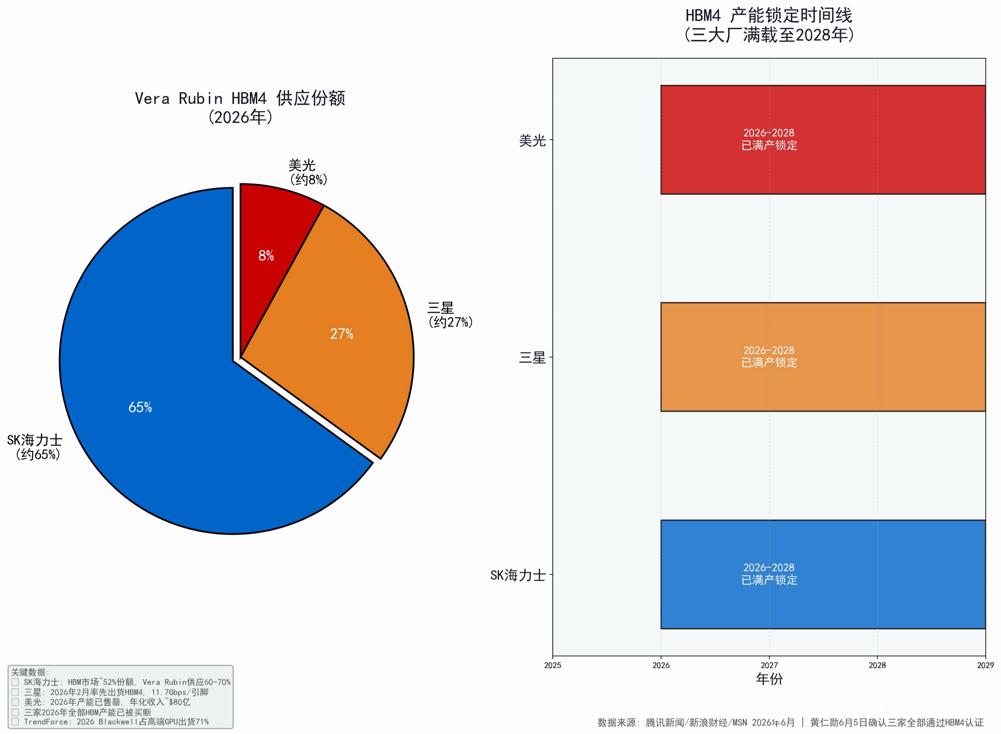

On June 25, Samsung, SK Hynix, and Micron were collectively sued in a U.S. federal court, accused of raising memory prices sevenfold over four years.

Two days later, the Financial Times reported that Tim Cook was lobbying the U.S. government for permission to purchase DRAM from China's ChangXin Memory Technologies, as the top three memory giants had allocated 85% of their HBM (high-bandwidth memory) capacity to cloud providers willing to pay billions upfront, demoting Apple—the world's largest consumer electronics buyer—to a "marginal customer."

Around the same time, OpenAI was reported to have delayed its IPO due to market reluctance to meet Sam Altman's $1 trillion valuation, demanding a discount for listing.

On June 29, the South Korean government announced an 800 trillion won investment to build four new wafer fabs, betting heavily on memory.

Within a week, the strongest upstream players were expanding production, the strongest downstream players were scrambling to survive, sandwiched between a Cross border litigation (transnational lawsuit) and a delayed IPO.

SK Hynix's operating profit margin reached 72% in Q1 2026. NVIDIA's was 65%, and TSMC's 58%. A memory company outearned the GPU king and the world's most advanced foundry, setting a semiconductor industry record.

At 72%, for every $100 in memory chip sales, only $28 covers costs. Memory has long been seen as a cyclical, low-margin business—20-30% profit margins were once considered a good year.

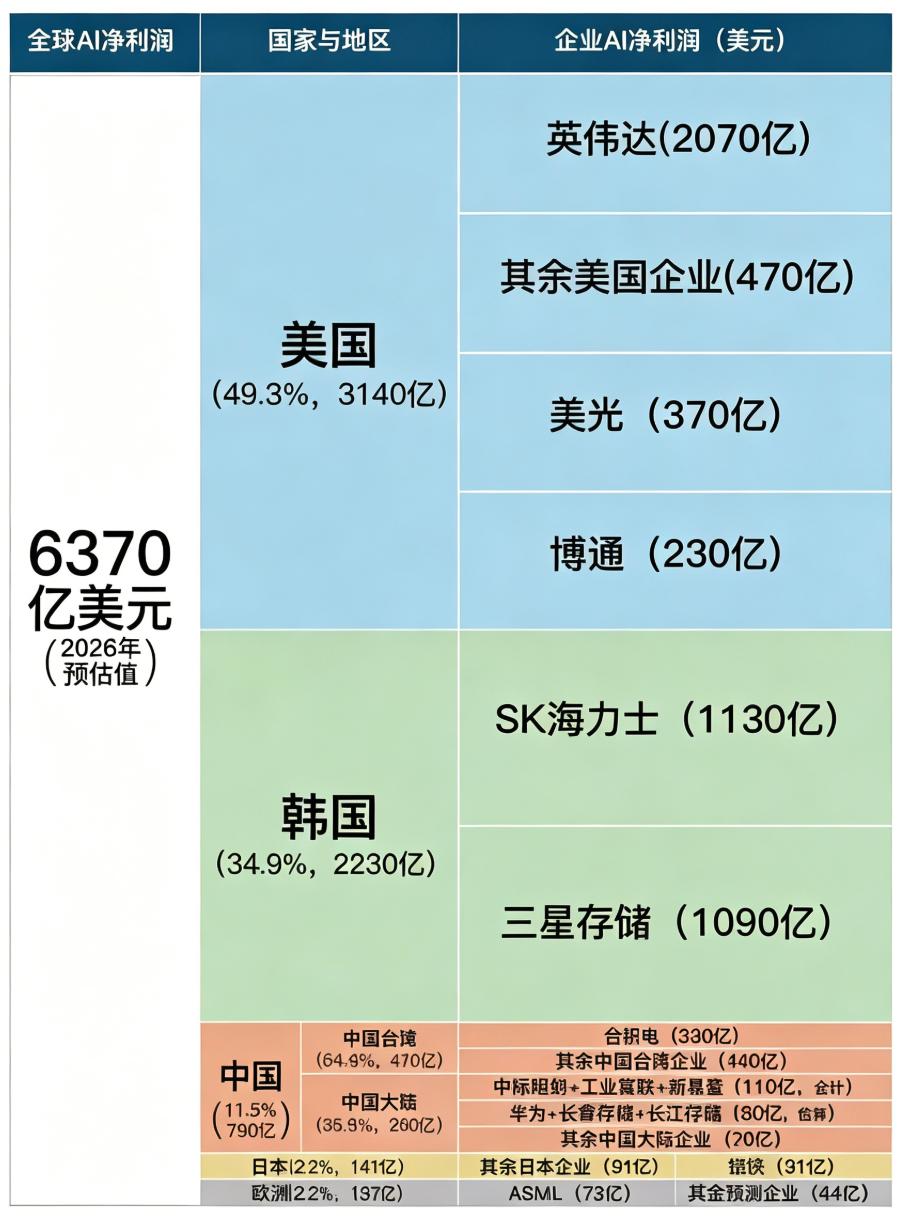

72% isn't just a good year; it's a paradigm shift. Altimeter estimates the 2026 global AI net profit pool at $637 billion, with the U.S. and South Korea taking 84%. NVIDIA alone accounts for $207 billion, while Samsung and SK Hynix combined take $222 billion. In AI, a few companies from two countries dominate.

Upstream players maintain these profits because even the most powerful GPUs rely on HBM for data. Without HBM, GPUs spin idly. Only three companies globally can mass-produce HBM: SK Hynix, Samsung, and Micron. Any company training models, running inference, or deploying agents must first buy from these three. OpenAI buys, Anthropic buys, Meta buys, ByteDance buys, and DeepSeek buys.

Moreover, this round of "shovels" isn't a one-time purchase. Every training run, every inference, every conversation requires ongoing payments upstream. Upstream revenue is downstream's persistent cost.

Downstream players fall into two camps: large model companies (OpenAI, Anthropic, and domestic players like Zhipu, MiniMax, and Moonshot AI) and super platforms at the application layer (Microsoft, Meta, Google, ByteDance, Tencent). The former bleed money; the latter invest heavily but remain profitable overall due to diversified businesses.

Consider the heavy bleeders. According to The New York Times, citing insiders, OpenAI's 2025 revenue reached ~$13 billion, with monthly revenue around $2 billion.

In Q1 2026, OpenAI reported $9.3 billion in operating losses and $3.7 billion in cash burn. Revenue tripled year-over-year to $5.7 billion, but costs expanded nearly as much. The company's shareholder documents project $25 billion in cash burn for 2026, escalating to $57 billion in 2027, with long-term compute procurement commitments exceeding $660 billion. Positive cash flow isn't expected until 2029-2030.

Perhaps due to persistent unprofitability, the market balked at a $1 trillion valuation, forcing OpenAI to delay its IPO to 2027.

Domestically, Zhipu's prospectus revealed $190 million in H1 2025 revenue and $236 million in net losses—$12 lost for every $1 earned. Zhipu explicitly stated in its prospectus that net losses would widen further in 2025.

Why the losses? Many blame "expensive model training." But training is a one-time cost that amortizes—not the core issue. The real problem is inference: every user interaction costs real money upstream. More users mean bigger bills.

OpenAI's 2025 revenue more than tripled from 2024, soaring from $3.7 billion to $13 billion. Service costs, however, nearly tripled from $2.65 billion to $7.5 billion. Tripling scale meant tripling direct costs, with no amortization. Zhipu faced the same issue: of its $159.5 million in H1 2025 R&D spending, $114.5 million went to compute services—variable costs incurred per call, not fixed assets that amortize with scale.

Thus, large model companies' losses aren't temporary but structural: stopping means death, continuing means persistent losses.

Microsoft has monetized AI by adding premiums to Azure and Office subscriptions. Copilot leveraged Office's existing customer base, growing paid seats from 15 million to 20 million in nine months. Users didn't pay for AI; they paid $30 extra monthly for Office. Combined with Azure, Microsoft's AI business ARR exceeded $37 billion in FY26 Q3, up 123% YoY, surpassing OpenAI and Anthropic's combined revenue.

Meta used AI recommendations to sell old ad inventory at higher prices. In Q1 2026, ad impressions rose 19%, prices 12%, and Reels user time increased 10% due to AI-driven sorting. Without launching new products, Meta purely accelerated old algorithms with AI, driving Q1 ad revenue to $55.3 billion (+33% YoY). ByteDance's AI content distribution and Tencent's AI customer service/coding assistants follow the same logic.

The fundamental difference? These companies monetize AI by transforming existing businesses. Microsoft isn't an "AI company" but an OS and enterprise software company—AI lets it raise prices on old products. Meta isn't an "AI company" but an ad company—AI lets it charge more for ad slots. ByteDance isn't an "AI company" but a content distributor—AI adds leverage to its recommendation algorithms.

They have existing business models to carry AI's efficiency gains. Users, traffic, enterprise clients, pricing power, and channels already exist; AI just boosts margins. They don't need to ask if users will pay for AI—users already pay them.

Large model companies lack this luxury. ChatGPT Plus and Claude Pro cost $20/month but can't cover quarterly inference bills in the billions. Enterprise API revenue grows, but pure B2B clients face low switching costs, and competitors like DeepSeek undercut prices by half—a few code changes might suffice to switch.

The difference between profitable and unprofitable downstream players lies in having a non-AI-dependent business model to capture AI's efficiency gains. Those with it profit; those without struggle.

Apple earned $112 billion in FY2025 ($2 billion daily), the most complete downstream player globally. It has devices, brand, pricing power, and the world's largest procurement scale.

Yet even Apple, to cut memory costs, risked political backlash from the U.S. government by seeking a Chinese supplier in an export-controlled sensitive area.

The top three memory giants prioritized 85% of HBM capacity for cloud providers willing to pay billions upfront, demoting Apple—once their "top client"—to a "marginal customer."

Micron's CEO publicly accused Apple of "buying chips cheap for a decade, then marking up devices by hundreds of dollars"—the point isn't the verbal sparring but his boldness. A decade ago, Apple was the golden client; such remarks would never leave Micron's execs' mouths. Now, supply-demand dynamics reversed, and he spoke openly.

If even Apple faces upstream pricing power, imagine the plight of middle layers without devices, brands, or pricing control.

Upstream profits and downstream struggles aren't unique to AI. In every tech revolution, money first flows to "shovel sellers."

During the 1990s internet boom, Cisco dominated by selling routers, peaking at a $500+ billion valuation—then the world's highest.

Today's Amazon saw its market capitalization (market cap) evaporate by 90% in 2000, with a 50% loss rate, until recovery began in 2001. Its upstream cloud business, AWS, remains its profit engine—among Amazon's three segments, AWS leads with a 37.7% operating margin, contributing nearly 60% of total operating profits.

In the 19th-century railway era, companies selling rails, locomotives, and ties profited first, while railway operators waited decades for returns.

The pattern holds: regardless of downstream winners, upstream players cash in first.

This AI cycle follows the same script. SK Hynix's 72% margin, NVIDIA's market cap leadership, and South Korea's 800 trillion won bet on memory reflect upstream stability. Whether OpenAI, Anthropic, ByteDance, or DeepSeek wins, payments to upstream players are inevitable.

This certainty has led the U.S. and South Korea to bet their futures on it.

Large model companies face a different reality. Their primary cost—compute—scales with revenue. OpenAI's 2025 revenue tripled, but service costs tripled too, with no amortization. They must pay upstream while lacking a massive, stable paying user base—costs rise rigidly, but monetization lags.

Downstream players have split. Microsoft's Copilot, Meta's ad recommendations, and ByteDance's content distribution earn by enhancing existing businesses with AI. They leverage users, traffic, pricing power, and channels—AI flows into old ledgers as profit. Companies relying on "AI to open new businesses" face the same struggles as large model firms, lacking proven models.

Upstream players earn certain money; downstream giants earn by adding AI leverage to old models; large model companies chase future narratives. The first two are cashing in; the third awaits a delayed validation moment.

History doesn't repeat, but it rhymes. Cisco and Amazon, rails and railways, NVIDIA and OpenAI—every tech revolution begins this way.

Money bypasses the loudest frontstage companies, flowing to the silent profit machines.

-

![]()

Laifen Seeks to Escape 'Budget Dyson' Label but Falls Short of Dyson's Prestige

-

![]()

Who is Holding Back the Development of Dexterous Hands?

-

![]()

How do Autonomous Driving Physical AI and End-to-End Systems Work Together?

-

![]()

June's New Energy Vehicle Sales Rankings Unveiled! Leapmotor Surpasses Tesla in a Stunning Comeback, Marking the Start of the Automakers' Knockout Phase

-

![]()

Global Agents Embrace 'Loop Engineering': AI's Self-Sufficient Work, Supervision, and Revision

-

Post-90s Straight-A CEO Propels Jihao Technology Toward IPO, Despite Over 90% Revenue Reliance on Smartphones

-

AI 'Dissolves' Visual China's Copyright Moat—What Story Can It Tell to List in Hong Kong?

-

![]()

The AI Industry Chain: A Tale of Fire and Ice - Upstream Thrives, Downstream Struggles