"Fruit Chain Brother No.1" Plummets Below Issue Price on Debut Trading Day! Chaoshan's Wealthiest Woman Stakes HK$24 Billion on AI

07/13 2026

07/13 2026

359

359

For the wealthiest woman from Chaoshan, the hurdles have only just begun.

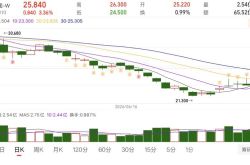

On July 9th, Luxshare Precision, dubbed the "Fruit Chain Brother No.1," made its official debut on the Hong Kong Stock Exchange. Its shares nosedived upon opening, plummeting over 9% at one point during intraday trading, and ultimately closed 1.55% lower, signaling a break below the issue price. Retail investors who subscribed to the IPO incurred a paper loss of nearly HK$300 per lot. Although the stock rebounded to close 1.12% higher on July 10th, it still remained below the issue price.

Behind Luxshare Precision's lackluster debut lies the halo of being the "largest Hong Kong IPO of the year" and a stellar lineup of global cornerstone investors, yet the market remained unimpressed. The reason may stem from the fact that Wang Laichun, the wealthiest woman from Chaoshan, built a commercial empire worth hundreds of billions by relying on Apple, but now aims to shed the "Fruit Chain OEM" label—a transformation that promises to be a long and arduous journey.

According to the Hurun Research Institute's "2026 Hurun Global Self-Made Women Billionaires List," Wang Laichun ranked fourth globally and second domestically, with a wealth of RMB 91 billion, making her the wealthiest female entrepreneur in Shenzhen. The "2026 Hurun Global Rich List" further positions Wang Laichun at 232nd globally, with the same wealth figure.

"Fruit Chain Brother No.1" Plummets Below Issue Price on Debut Trading Day

During this Hong Kong IPO, Luxshare Precision encountered an extreme divergence where long-term institutional investors bought in while short-term funds exited.

A total of 383 million shares were offered globally, with 90% allocated to international placement and oversubscribed nearly 10 times. Twenty-six top-tier institutions locked in nearly half of the offered shares, with three global sovereign wealth funds simultaneously participating, binding HK$1.5 billion in long-term capital. In this year's Hong Kong IPO market, this cornerstone investor lineup is considered top-notch.

The core conflict revolves around pricing. Luxshare Precision directly opted to price at the upper limit of the offering range, equating to just a 13% discount relative to its A-shares.

A review of the data reveals that in recent years, leading A-share companies listing in Hong Kong have typically offered a 20%-30% discount. Luxshare Precision's near-parity pricing with its A-shares left little room for safety in the Hong Kong secondary market.

From an operational standpoint, although Luxshare Precision has been downplaying its reliance on Apple, over half of its revenue still comes from a single major customer.

In the capital market's valuation framework, consumer electronics OEMs have always had to work hard for their money, typically being valued as manufacturing companies rather than pure tech growth stocks.

Therefore, short-term funds in the Hong Kong market focus solely on current fundamentals—as long as the "Apple dependency" remains unresolved, even the most ambitious transformation narratives will struggle to support a high valuation.

No discussion of Luxshare Precision would be complete without mentioning its founder, Wang Laichun, the legendary wealthiest woman from Chaoshan.

Early in her career, she rose from a frontline worker to an executive at Foxconn, mastering the entire precision manufacturing process for consumer electronics. In 2004, she returned home to start her own business, betting on the Apple supply chain boom. Relying on stable quality control and unparalleled delivery capabilities, she steadily secured core orders for Apple cables, assembly, and structural components, transforming a small OEM factory into the world's second-largest Fruit Chain supplier.

Over the past decade, Apple has consistently accounted for 70% of Luxshare Precision's revenue, serving as the bedrock for the company's growth and the key to Wang Laichun's ascent to a net worth exceeding RMB 100 billion.

In 2025, the consumer electronics segment contributed RMB 264.2 billion in revenue, accounting for nearly 80% of the company's total revenue, with Apple remaining the single largest customer.

The global Fruit Chain supply chain continues to restructure, bringing risks: Apple persistently reduces unit prices for component procurement, mid-range production capacity shifts to India and Vietnam, and overseas factory construction incurs higher labor costs and compliance risks, with geopolitical fluctuations always posing threats to the company's foundation.

As long as consumer electronics account for 80% of revenue, Luxshare Precision cannot escape the low valuation associated with "low-end OEM manufacturing," a core concern that prevents funds from offering a premium.

A HK$24 Billion Gamble

In this Hong Kong listing, Luxshare Precision raised HK$24 billion, making it the largest IPO in Hong Kong in 2026.

According to the prospectus, 35% of the funds will be used for global capacity expansion and upgrading overseas bases to accommodate automotive and computing hardware production; 30% will be invested in R&D, focusing on high-end sectors such as high-speed optical interconnects, automotive precision manufacturing, and liquid cooling.

It is clear that Wang Laichun aims to leverage the A+H dual-listing platform to completely restructure the business and shed the heavy "Fruit Chain" label.

In recent years, Luxshare Precision has gone all-in on two new sectors: automotive electronics and AI computing hardware, attempting to break free from Apple's grip.

Unfortunately, the ideal is ambitious, but the reality is challenging. Luxshare Precision's new businesses are still too small to support the company's valuation in the short term.

Financial reports show that in 2025, automotive electronics revenue reached RMB 39.255 billion, a significant year-on-year increase of 185.34%, with its revenue share rising from 5% to 11.81%. However, this is still several times smaller than the consumer electronics base and can only serve as incremental growth in the short term, unable to offset potential fluctuations in Apple's business.

Additionally, while Luxshare Precision's AI computing hardware narrative is compelling, performance realization is at least two years away. Computing power is currently the hottest sector in the capital market, and Luxshare Precision has made early moves: high-speed connectors are supplied in bulk to NVIDIA's MGX servers, liquid cooling has entered NVIDIA's supply chain, and 800G optical modules have achieved small-scale deliveries.

Financial reports show that in 2025, Luxshare Precision's communications and data center segment contributed RMB 24.5 billion in revenue, accounting for less than 7.4% of total revenue. Optical modules and high-speed connectors are still in the early stages of capacity ramp-up.

Multiple foreign institutions consistently estimate that Luxshare Precision's 800G and 1.6T optical modules will see mass-scale volume production in the second half of 2027. By 2027, the computing power business will contribute only 10% of profits, rising to 16% by 2028.

This means that Luxshare Precision's AI computing-related businesses will take at least 1-2 years to make a substantial contribution to earnings, leaving the company's revenue structure unchanged in the short term.

The debut below the issue price in Hong Kong essentially reflects the secondary market's negative pricing of the "excessively long transformation cycle."

The logic of the capital market is always pragmatic: while long-term narratives can command valuation premiums, the premise is consistently delivering incremental earnings. Currently, Luxshare Precision's core revenue and profits remain tied to Apple, with transformation businesses too small in scale and their payoff cycles too long for funds to justify paying a premium for earnings two or three years down the line.

Conclusion

From a Foxconn factory worker to the helm of a company with a market capitalization exceeding RMB 100 billion, Wang Laichun achieved class mobility through the Apple supply chain but is equally constrained by the valuation ceiling imposed by a single customer.

While Apple's revenue share has declined from 70% to 50%, signaling initial success in "de-Applefication," nearly 80% of revenue still depends on consumer electronics, with emerging businesses accounting for less than 20%. The transformation is far from complete.

With HK$24.2 billion in proceeds now secured, Luxshare Precision is simultaneously advancing in automotive electronics and AI computing power, but capacity ramp-up, customer certification, and order volume growth will take time.

The debut below the issue price in Hong Kong is not a denial of Luxshare Precision's manufacturing capabilities but a reminder to Wang Laichun: to completely break free from the Fruit Chain valuation shackles and no longer be swayed by "Apple dependency" in the company's stock price, at least another 2-3 years of arduous business scaling lie ahead.

Luxshare Precision's "de-Applefication" Long March has only just reached its midpoint.

-

![]()

Weekly Stock Review | Who Dominates the Market: Hedge Funds, Quant Traders, Institutions, or Hot Money?

-

![]()

Sales Slump Again: Why Are Affluent Buyers No Longer Exclusively Opting for Porsche?

-

![]()

Xiaomi’s New Auto Brand Launch Sparks Stock Rebound: Is a Trend Reversal on the Horizon?

-

![]()

Seres Mid-Year Report Catastrophe: Projected Losses Surpass 1.5 Billion Yuan!

-

![]()

"Fruit Chain Brother No.1" Plummets Below Issue Price on Debut Trading Day! Chaoshan's Wealthiest Woman Stakes HK$24 Billion on AI

-

![]()

Auto Market Undergoes Major Shake-Up: Winners and Losers Revealed

-

![]()

The Successful Recovery of the First Stage of the Long March 10B: What Does It Mean for China's Commercial Space Industry?

-

![]()

Xiaomi Pengcheng: Crafting the Future of Mobility