Apple’s Performance and Market Value Soar to New Heights: Unveiling the Driving Forces

05/15 2026

05/15 2026

613

613

Introduction: Under the astute leadership of Tim Cook, Apple has undergone a remarkable metamorphosis, evolving from a mere 'hardware vendor' into a sophisticated 'user operator'.

By Li Ping / Author, Lishi Business Review / Producer

1. Historical Quarterly Performance

'We’ve just delivered our best March quarter (second fiscal quarter) results ever, with double-digit growth across all regions,' Tim Cook announced at Apple’s recent financial results briefing.

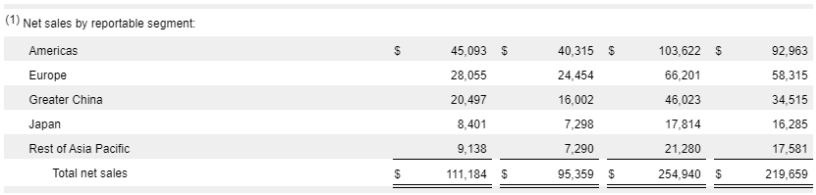

According to the financial report, in the second quarter of FY2026 (ending March 28, 2026), Apple’s total revenue soared to $111.184 billion, marking a 17% year-on-year increase. Net profit reached $29.6 billion, up 19.4%, while diluted earnings per share stood at $2.01, a 22% rise year-on-year. All these figures surpassed market expectations, setting new records for the second quarter.

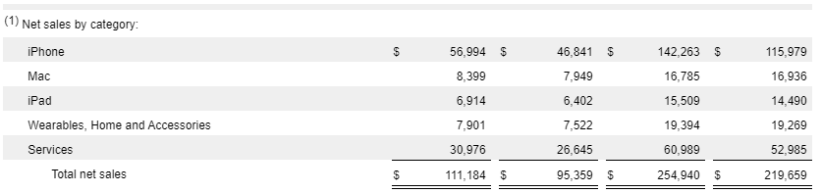

Analyzing the business segments, Apple’s hardware revenue totaled $81.206 billion, up 16.7% year-on-year. Driven by robust demand for the iPhone 17 series, iPhone revenue surged to $56.99 billion, a 21.7% increase, becoming the cornerstone of hardware growth. The strategy of offering 'more storage at the same price' was pivotal to the global success of the iPhone 17 series. The new iPhone 17 models now start with 256GB of storage, maintaining the price at 5,999 yuan, and have become eligible for government subsidies in China.

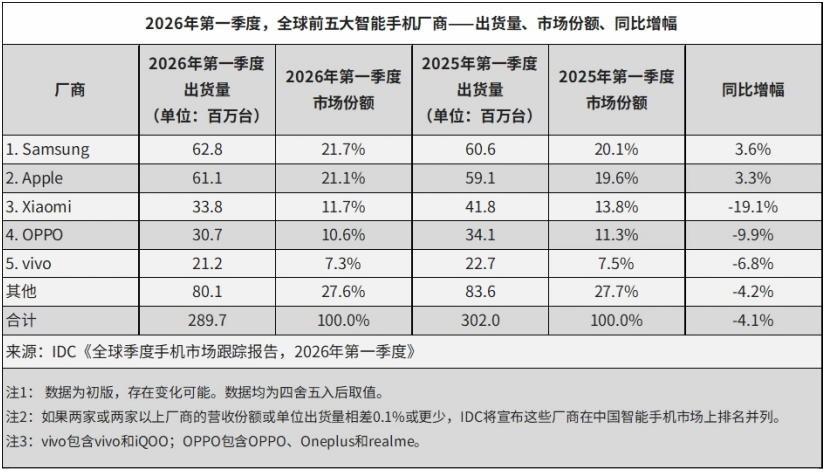

IDC data reveals that in Q1 2026, global smartphone shipments reached 289.7 million units, down 4.1% year-on-year, breaking a ten-quarter growth streak since mid-2023. This decline was primarily attributed to shortages and escalating costs of DRAM and NAND storage chips. Despite this, Apple’s global market share stood at 21.1%, up 1.5 percentage points year-on-year. Regionally, China’s smartphone shipments in Q1 were approximately 69.01 million units, down 3.3% year-on-year. However, Apple shipped 13.1 million units, up 33.3%, leading the market in growth.

Beyond the iPhone series, other Apple hardware products also witnessed positive growth. Mac revenue reached $8.4 billion, up 6% year-on-year, driven by the launch of the MacBook Air, MacBook Pro, and the more affordable MacBook Neo this fiscal quarter. iPad revenue hit $6.91 billion, up 8% year-on-year, thanks to increased sales of the M5 Pro and A16 models.

Compared to traditional hardware, Apple’s software services performed even more impressively. Revenue from software services reached $31 billion, up 16% year-on-year, marking the second consecutive quarter exceeding $30 billion. In a sense, even without considering its vast hardware empire, Apple has emerged as one of the world’s largest software companies.

Buoyed by strong iPhone 17 series sales, Apple resumed double-digit growth in the Chinese market, alleviating concerns about a 'market slide' in China. Data shows revenue in Greater China reached $20.497 billion, up 28.09% year-on-year, setting a new record for the second fiscal quarter and far exceeding market expectations.

Beyond China, Apple’s sales in other regions also shone. Revenue in the Americas reached $45.093 billion, up 11.85% year-on-year, accounting for over 40% of total revenue, with the U.S. remaining Apple’s largest market. Europe generated $28.055 billion, up 15% year-on-year, accounting for 25.2%, reflecting the popularity of the iPhone 17 series in Europe. Additionally, other Asia-Pacific regions and Japan saw year-on-year growth rates of 25% and 15%, respectively.

Buoyed by strong financial results, Apple’s stock price rose 3.24% the day after the earnings release, with its market value surging by over $100 billion overnight. As of the latest trading day, Apple’s total market value closed at $4.3 trillion, another all-time high.

2. Gross Margin Reaches All-Time High

Since the second half of 2025, surging demand for AI and data centers has expanded the market for storage products, with prices for memory modules and hard drives soaring across the board. As the global shortage of memory chips continues to spread, consumer electronics like smartphones and PCs have been significantly impacted. Against this backdrop, Apple’s performance this fiscal quarter was not initially viewed favorably by the market, and its stock price had been on a downward trend since December 2025, losing its $4 trillion market cap.

However, concerns about Apple’s costs did not materialize. The financial report showed Apple’s gross margin reached a record high of 49.3%, up 2.2 percentage points year-on-year. Hardware gross margin stood at 38.7%, up 2.8 percentage points, while software services gross margin rose to 76.7%, up 1.4 percentage points.

Notably, amid rising memory costs across the consumer electronics industry, Apple’s hardware gross margin improved, thanks to economies of scale and product mix optimization. On one hand, the significant increase in iPhone shipments brought strong economies of scale, effectively diluting fixed costs per unit. On the other hand, Apple’s focus on the mid-to-high-end market meant the impact of rising storage costs was relatively smaller compared to competitors, while the increased share of high-margin products like the Pro series also boosted overall margins.

Additionally, Apple’s robust supply chain management was a key factor in its margin improvement. Under Tim Cook’s leadership, Apple successfully implemented a global supply chain layout, distributing core component production to cost-optimal regions and using stringent process management to minimize inventory cycles, greatly reducing capital tied up in inventory. At the same time, Cook pushed Apple to sign long-term exclusive agreements with key suppliers, even prepaying to secure upstream capacity, a crucial factor in Apple’s hardware margins remaining resilient to storage price hikes.

Nevertheless, the escalating memory price surge still poses potential cost risks for Apple in the future. Cook himself admitted during Apple’s Q2 2026 earnings call that Apple’s ability to maintain high profit margins in the previous two quarters (ending December 2025 and March 2026) was largely due to significant advance stockpiling, locking in lower memory costs. However, starting in June, this protection will gradually fade as inventory of DRAM and NAND flash memory runs out, forcing Apple to procure new components at current market prices.

By tradition, Apple will prepare for the mass production of the iPhone 18 series in the second half of the year, coinciding with the depletion of its memory inventory. There have been rumors that Apple will keep iPhone 18 pricing unchanged. However, given the storage chip shortage, the sustainability of this strategy remains questionable.

Some analysts believe that, based on the strong market performance of the iPhone 17 series, Apple may significantly adjust its product release schedule, with the most notable change being a substantial extension of the production cycle for the iPhone 17 standard model, while the iPhone 18 standard model, originally slated for a fall 2026 release, may be skipped.

3. Services: The 'Money Printing Machine' in Full Swing

Beyond supply chain advantages, the rising share of service software revenue has been a key driver of Apple’s sustained margin growth, thanks again to Cook’s leadership. Since 2014, Cook has, through a series of forward-looking strategic moves, successfully established services as Apple’s second growth engine.

In fact, during Steve Jobs’ tenure, he believed 'great products should be bought outright' and opposed subscription models to bind users. Thus, under Jobs, the Apple Store was merely a hardware supplement, aimed at improving the iOS ecosystem to make the iPhone more powerful and irreplaceable, rather than generating major revenue from app distribution.

Under Cook’s leadership, Apple successfully integrated services like Apple Music, iCloud, and AppleCare, building a comprehensive 'User Lifetime Value (LTV) system.' Based on this strategy, users continue to pay for music subscriptions, cloud storage, and in-app purchases after purchasing hardware, creating a new dual-wheel-driven business model where 'hardware drives services, and services feed back into hardware.'

Thus, through ecosystem synergy, Apple transformed low-frequency hardware sales into high-frequency, high-stickiness, and high-margin recurring service revenue, achieving a commercial transformation from 'selling devices' to 'operating users.'

Data shows that in FY2015, Apple’s services revenue was less than $20 billion. By FY2025, it had surged to $109.16 billion, surpassing $100 billion for the first time, accounting for about 26.2% of total revenue. Moreover, Apple’s services gross margin consistently exceeds 75%, more than double that of its hardware business.

In Q2 FY2026, Apple’s software services revenue reached $31 billion, up 16% year-on-year, accounting for 28% of total revenue, far exceeding market expectations. Meanwhile, as Apple’s global active device base continues to grow, its services gross margin rose to 76.7%, another record high. From a gross profit contribution perspective, while software services account for less than 30% of revenue, they contribute 43% of Apple’s gross margin, making services the 'ballast' of Apple’s profitability.

Notably, Apple is actively expanding its advertising business within its services ecosystem. It has added new ad slots in App Store search results and plans to launch local business-focused ads in Apple Maps in the U.S. and Canada this summer. Given the extremely high profit margins of advertising, its growing revenue share is expected to further boost Apple’s overall services margin, meaning Apple’s services business will continue to operate as a 'money printing machine.'

In April, Apple announced a leadership transition: current CEO Tim Cook will step down on September 1, becoming Executive Chairman, with Senior Vice President of Hardware Engineering John Ternus succeeding him as CEO. This marks the end of Tim Cook’s 15-year tenure at Apple’s helm.

Overall, Apple achieved 'full bloom' in both hardware and software businesses in the second fiscal quarter, with double-digit growth across all major markets, demonstrating that the company’s sales breakthroughs were driven by global demand resonance rather than reliance on a single market or product. For Cook, who is about to step down as CEO, this is undoubtedly a near-perfect farewell report.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action