SpaceX: Is AI a Money-Burning Machine, or is 'Space Computing Hegemony' the Ultimate Game-Changer?

07/01 2026

07/01 2026

500

500

In 'From Daydreams to Fortunes: Is SpaceX Really That 'Sci-Fi'?', Dolphin Research discussed how, among SpaceX's three main business segments (rocket launches, Starlink, and AI), the AI business is the most cash-intensive but also offers the greatest valuation potential.

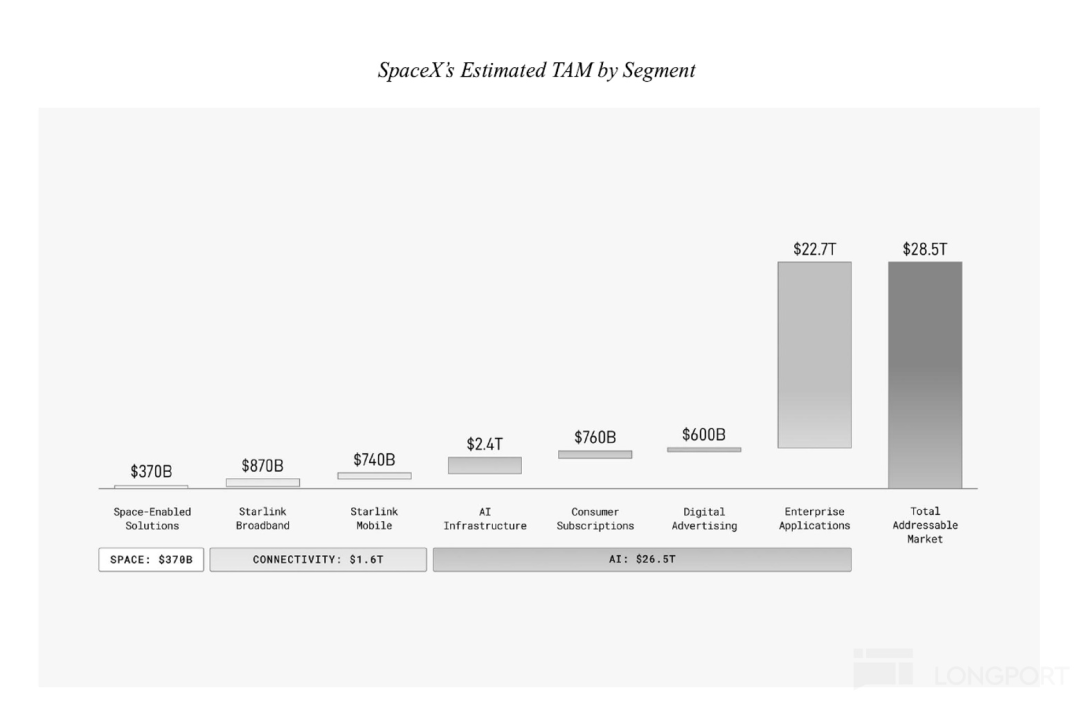

It not only represents SpaceX's core narrative of transitioning from a 'hardcore space infrastructure giant' to a 'platform-level intelligent service provider' but also serves as the absolute cornerstone supporting its massive total addressable market (TAM) of $28.5 trillion—with AI accounting for 93% of the total TAM, and enterprise applications contributing nearly 80% of the market space.

In this piece, Dolphin Research will conduct an in-depth analysis of the AI segment, focusing on the following core questions:

1. What are the core modules that constitute SpaceX's AI asset landscape?

2. Why has advertising revenue on the X platform, as the underlying data source, continued to decline under pressure?

3. What is the current progress in terms of intelligence and commercialization of the highly anticipated Grok large model?

4. Computing power leasing business: How long can this unexpected 'cash flow feast' last?

5. Space data centers: Is the transition from ground-based operations to 'space-based computing hegemony' a interstellar sci-fi fantasy or a dimensional strike?

Below is a detailed analysis.

1. What are the core modules of SpaceX's AI assets?

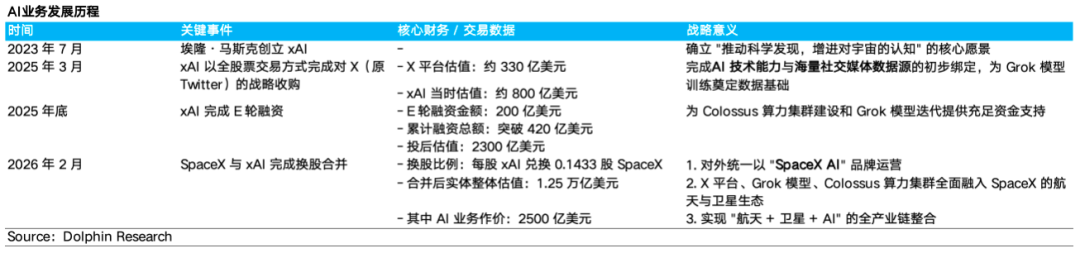

SpaceX's AI business officially took shape after the wholly-owned acquisition of xAI in February 2026. Its development trajectory is as follows:

Elon Musk founded xAI in July 2023 with the vision of 'advancing scientific discovery and enhancing understanding of the universe.' In March 2025, xAI completed the strategic acquisition of the X (formerly Twitter) social platform through an all-stock transaction. At that time, the X platform was valued at approximately $33 billion, while xAI was valued at around $80 billion, achieving an initial binding of data sources and AI operations. By the end of 2025, xAI completed a $20 billion Series E financing, reaching a post-money valuation of $230 billion.

In February 2026, SpaceX and xAI completed a share-swap merger, with the combined entity valued at $1.25 trillion (including $250 billion for the AI business) and operating under the unified brand 'SpaceX AI.' Since then, the X platform, Grok model, and Colossus computing cluster have been fully integrated into SpaceX's aerospace and satellite ecosystem.

Accompanying this integration, significant adjustments were made to the original xAI executive team. Michael Nicolls, a senior SpaceX Starlink engineering executive, was appointed as President of the AI division, marking the strategic commencement of a new era of deep integration between 'space edge computing and spatial AI.'

From the perspective of SpaceX AI's revenue composition, its income is derived from two main segments: advertising revenue and AI solutions and infrastructure revenue.

Advertising revenue primarily comes from the X platform, while AI solutions and infrastructure revenue mainly includes: 1) Subscription and data licensing services revenue from the X platform; 2) Subscription and API access services revenue from the Grok large model; 3) Leasing revenue from computing infrastructure (Colossus cluster), which significantly increased starting in 2026.

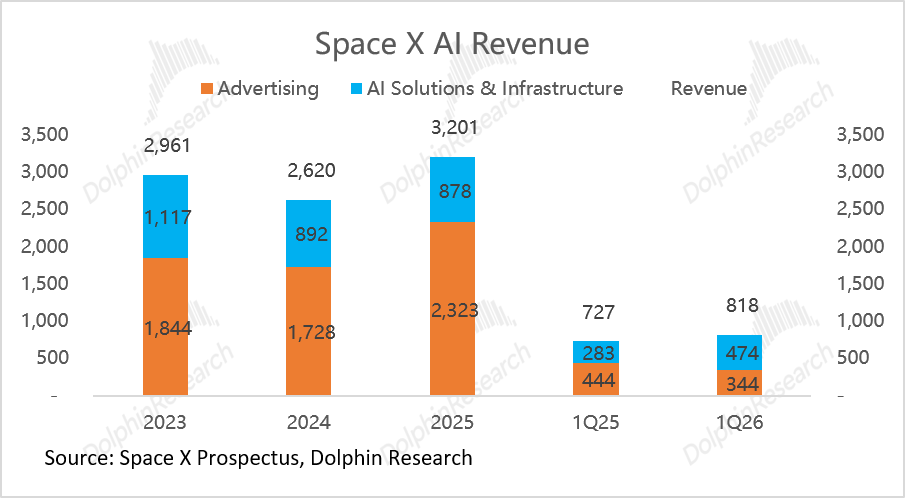

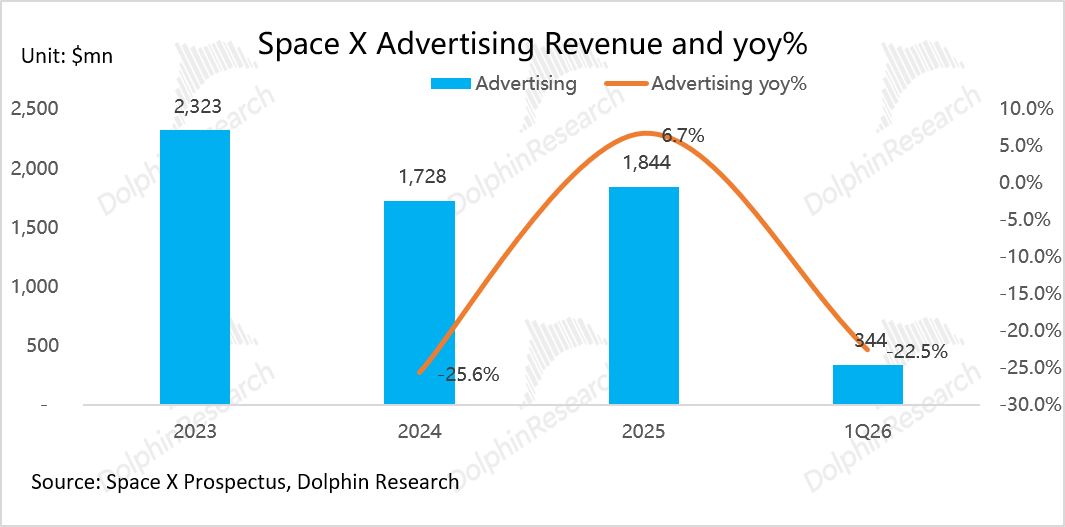

Between 2023 and 2025, SpaceX's AI business revenue grew relatively slowly, increasing from $2.96 billion to $3.20 billion, with a two-year compound annual growth rate (CAGR) of only 4%.

The growth contribution mainly came from AI solutions and infrastructure services revenue, which rose from $640 million in 2023 to $1.36 billion in 2025, with a two-year CAGR of 46%. In contrast, advertising revenue from the X platform continued to decline, dropping from $2.32 billion in 2023 to $1.84 billion in 2025, with an average annual decline of approximately 11%.

Let's examine the four core segments of SpaceX's AI business in order: 1) X platform; 2) Grok large model; 3) Computing power leasing business (Colossus cluster); 4) Space computing business.

2. Why has advertising revenue on the X platform, as the underlying data source, continued to decline under pressure?

The X platform (formerly Twitter), acquired by Musk for $44 billion at the end of 2022, underwent a fundamental transformation. Its role shifted from a social media platform to xAI's 'data granary' and 'distribution channel':

On the data side, its daily 350 million real-time posts provide exclusive, high-timeliness training data for the Grok large model. On the distribution side, with 550 million monthly active users, the X platform serves as a natural, zero-cost traffic entry point—currently, approximately 117 million users have accessed and used Grok's AI features, with the overall X platform having 4.4 million paying users and a paid penetration rate of about 0.8%.

However, the X platform's advertising revenue has been declining since peaking in 2022. Dolphin Research believes this decline results from a combination of industry structural trends and internal strategic contractions:

1. Brand advertising's struggle against 'performance-driven' competition

The X platform (since its Twitter days) has traditionally focused on brand advertising (Brand Awareness), emphasizing brand exposure and topic marketing. However, overall brand advertising budgets are under sustained pressure due to geopolitical and macroeconomic uncertainties. In a budget-constrained environment, advertisers increasingly prioritize quantifiable ROI, shifting funds from 'exposure-oriented' platforms to 'conversion-oriented' ones.

In comparison, the X platform's competitors hold irreplaceable advantages in 'conversion effectiveness':

a. TikTok: Built a highly engaging advertising system through its dominant user time spent.

b. Google Search: Holds the clearest 'purchase intent'—every user search term directly expresses commercial demand.

c. Amazon: Possesses the most direct 'purchase behavior' data, enabling highly cost-competitive performance advertising products.

d. Meta: Established industry-leading conversion tracking and attribution capabilities through AI-driven advanced advertising technologies (such as Advantage+ and GEM recommendation models).

In contrast, the X platform has consistently lagged significantly behind these four competitors in terms of full-funnel effectiveness from 'viewing ads → placing orders.' As the company heavily allocated computing power and R&D resources to the development of general-purpose large models like Grok, iterations in advertising AI algorithms were further delayed (insufficient ad targeting precision).

2. Strategic contraction-induced 'brand exodus'

In 2023, Musk implemented a large-scale strategic contraction on the X platform, redirecting resources to core areas like AI. Massive layoffs (especially the dismantling of content moderation teams) and relaxed speech standards directly crossed large advertisers' 'brand safety' red lines, triggering a 'brand exodus'—many mainstream advertisers paused or withdrew their spending due to concerns over brand content security.

This not only led to a 26% year-over-year decline in the X platform's advertising revenue to $1.7 billion in 2024 but also, combined with the user perception disconnection and brand equity loss caused by the abrupt rebranding to 'X,' ultimately resulted in the company recognizing $3.8 billion in goodwill and intangible asset impairment losses in 2023. Although the platform subsequently attempted to repair relationships with advertisers by improving content controls and launching new ad formats, rebuilding commercial trust is a lengthy process.

3. Short-term growing pains from proactive advertising platform transformations

Entering Q1 2026, the X platform undertook a comprehensive overhaul of its underlying AI advertising infrastructure to reverse technological disadvantages, focusing on deploying: fully automated ad placement systems, AI probabilistic attribution tracking, Grok-driven real-time brand safety risk control, and deep integration of advertising and recommendation flow algorithms.

However, this aggressive transformation inevitably disrupted sales rhythms in the short term, causing advertising revenue to decline by approximately $100 million year-over-year (yoy -22.6%) to $340 million in the quarter. Whether this overhaul can truly recover lost advertiser budgets remains to be continuously observed.

Musk's ultimate vision for the X platform is to transform it into an 'Everything App'—a super portal integrating AI, payments, communications, content, and commerce, essentially upgrading from single ad dependency to an 'AI service-driven' diversification (diversified) monetization engine (subscriptions, advertising, payments, commerce). By running the Grok model through all links, a self-reinforcing closed loop (closed loop) of data → model → monetization → users is formed.

However, in reality, the X platform is currently trapped in the dilemma of being 'the American version of Weibo': while still a center of public opinion (hub of public opinion) during major outbreak (breaking) events, its daily commercial traffic and user engagement are being systematically eroded by competitors, with market share under sustained pressure.

3. What is the current progress in terms of intelligence and commercialization of the highly anticipated Grok large model?

Grok is a large language model series independently developed by xAI. Its most differentiated core advantage lies in exclusive access to approximately 350 million daily real-time posts on the X platform (formerly Twitter). Unlike ChatGPT, which relies on external non-exclusive partnerships (such as with Reddit) or web scraping, the X platform serves as the 'first scene' for global breaking news.

This 'second-level timeliness + exclusive monopoly' of dynamic corpus input endows Grok with stronger data real-time capabilities compared to other large models.

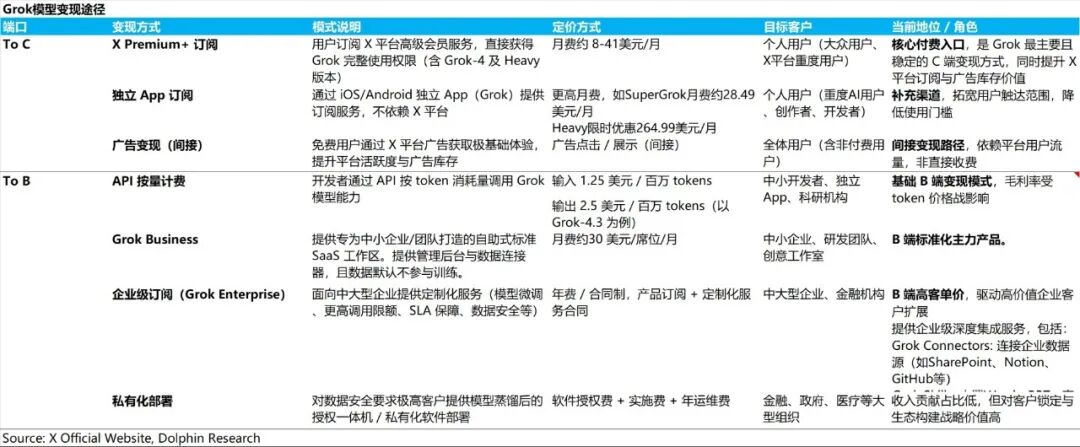

Since its launch, Grok has built a 'multi-track parallel' commercialization matrix:

To C (Consumer): Meeting the needs of different individual users by bundling with X platform memberships (Premium/Premium+) and offering standalone SuperGrok tiered packages (Lite/Standard/Heavy); simultaneously, using the free version to drive traffic and enhance the X platform's advertising value.

To D (Developers): Providing industry-standard compatible Grok APIs, offering flexible model calling services to developers and startups through a pay-as-you-go model.

To B (Enterprises):

- For small and medium-sized teams: Providing standardized SaaS services (Grok Business) with online self-service and per-seat pricing.

- For large and medium-sized enterprises and compliance institutions: Offering contract-based exclusive suites (Grok Enterprise) and private cloud/on-premises deployments to meet deep needs such as private data access, compliance, and customized fine-tuning.

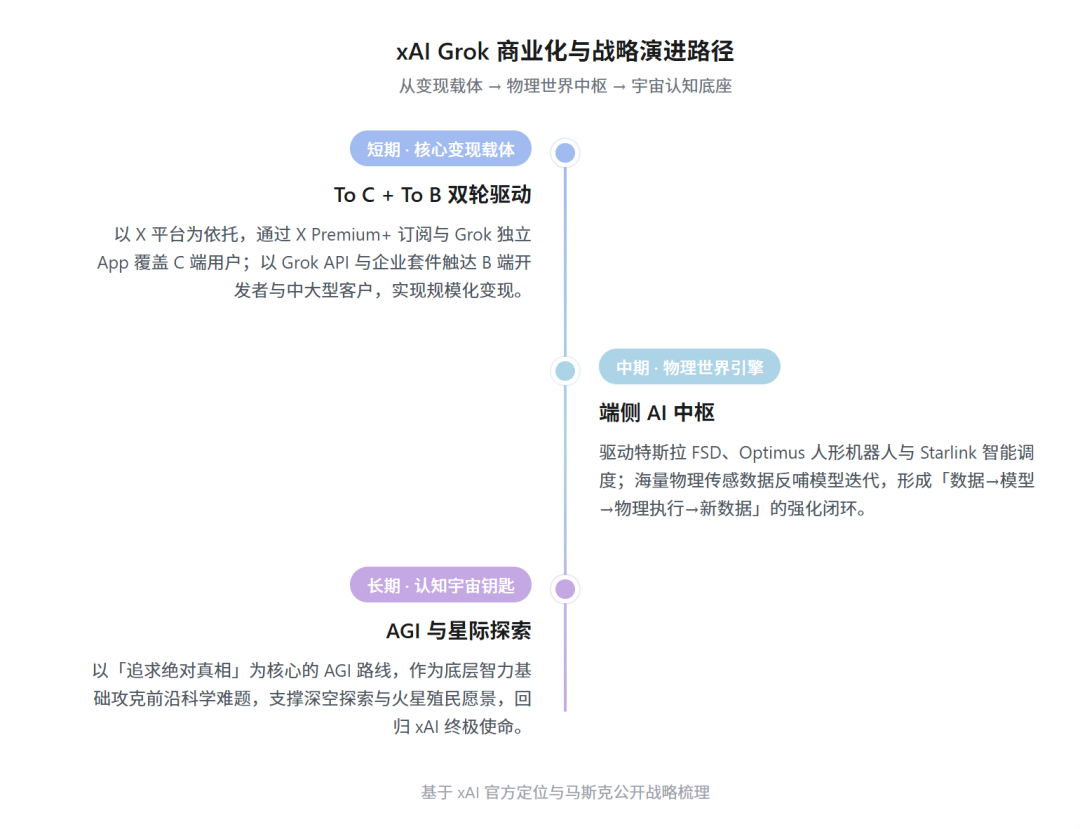

Within Musk's grand commercial blueprint, Grok serves as the most imaginative medium- to long-term business hub. It is envisioned as the 'central brain' connecting Tesla, SpaceX, X, Optimus, and Neuralink, with strategic deployments as follows:

In the short term, leveraging the X platform to achieve To C coverage through X Premium+ subscriptions and Grok standalone app subscriptions, while reaching B-end developers and medium-to-large clients through Grok APIs and Grok Enterprise suites. In the medium term, serving as the hub for edge AI to drive intelligent scheduling for Tesla's FSD system, Optimus humanoid robots, and Starlink's satellite network.

In the longer term, using the Grok model as the underlying intelligence foundation to tackle complex frontier scientific challenges and support the grand visions of deep space exploration and Mars colonization—the 'ultimate mission' set by Musk for Grok.

While the long-term vision is grand, and Grok plays the most central role as the software intelligence engine in Musk's AI ecosystem, its actual performance still lags about one tier behind leading competitors like Anthropic and OpenAI in comprehensive metrics, remaining a 'chaser.'

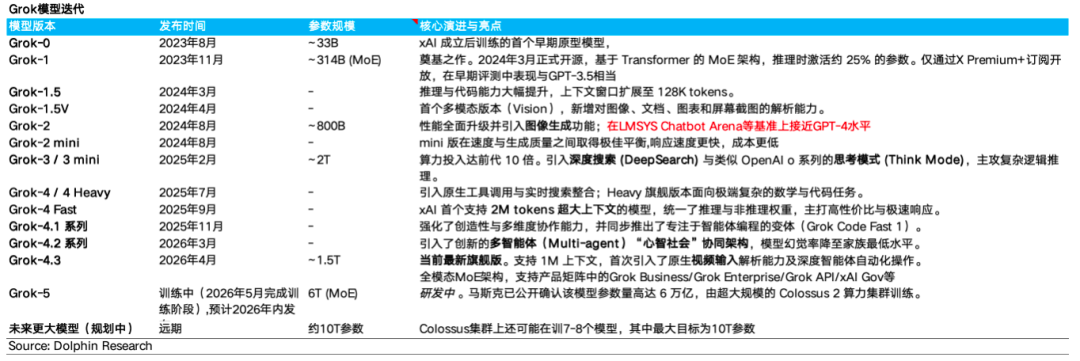

Since xAI's founding in July 2023, Grok has undergone rapid iteration from Grok1 to Grok4.3 in less than three years, with an iteration speed (4-5 months per major version) relatively fast in the industry. However, rapid model iteration does not equate to leadership:

Significant lag in foundational intelligence: Grok 4.3's intelligence score (38 points) lags far behind the first tier (Claude Fable 5, GPT-5.5) and has been surpassed by competitors known for 'high cost-performance' such as GLM-5.2 and DeepSeek V4 Pro, revealing a stagnation in the iteration of foundational capabilities.

Shortcomings in code and agent capabilities constrain enterprise-level monetization: Despite strong performance in specific vertical domains (e.g., Telecom τ²Bench), its overall coding index (42.2) and agent index (24.1) significantly trail leading competitors (both above 74 and 45 points), showing weakness in autonomous planning and executing complex tasks.

This undermines its deployment capabilities in high-value enterprise AI applications (automated workflows, intelligent customer service, code development assistants), falling significantly behind the commercialization pace of OpenAI and Anthropic.

Core Strengths: Ultra-Fast Response and Cost-Effectiveness

With extremely low inference latency (first-character latency of just 13.7 milliseconds, end-to-end speed far exceeding GPT-5.5's 82 seconds) and moderate API pricing ($1.25-$3 per million tokens), Grok remains highly competitive in real-time interaction scenarios due to its strong 'cost-performance' appeal.

Thus, at its current stage, Grok is positioned not as a pure research benchmark pushing AGI limits but as a more pragmatic 'engineering-focused model.' Leveraging its extremely high response speed and cost-effectiveness, Grok performs smoothly in C-side interactions and lightweight B-side scenarios (e.g., basic Q&A, simple summarization); however, in-depth areas such as complex code engineering, multimodal generation, and enterprise-level end-to-end automation still exhibit quantifiable capability gaps compared to leading all-round competitors.

However, for model vendors, the B-side market offers immense value and higher barriers: B-side clients not only have higher average contract values and substantial token consumption but also face extremely high migration costs once models are embedded into core enterprise workflows. Unlike price-sensitive C-side users, enterprises will not easily (replace base models) solely due to 'lower cost or faster response.'

Mismatch between Grok's capabilities and B-side needs: B-side clients prioritize 'low hallucination, high precision, and high auditability.' Grok's shortcomings in foundational intelligence and code capabilities directly restrict its deployment in core high-value scenarios like automated development.

The labor substitution and efficiency gains from top-tier models far outweigh the cost differentials in model procurement. Therefore, B-side clients consistently prefer paying a premium for 'extreme intelligence.'

This raises the question: Why haven't Grok's abundant AI operational compute resources (1GW+ GPU clusters) and data advantages (X platform) translated into model leadership? Dolphin Research suggests potential gaps in foundational algorithms, data structures, and organizational culture:

a. 'Pure compute stacking' hits bottlenecks, reinforcement learning (RL) becomes inefficient:

Grok's shortcomings in complex code tasks indicate that compute has reached its ceiling. It allocates half of its compute to RL, but due to subjective code quality and lack of automated scoring mechanisms, ambiguous reward signals cause compute to spin inefficiently in 'trial-and-error' mode, far less efficient than supervised fine-tuning (SFT).

Yet compute cannot generate high-quality supervised signals. To break through intelligence limits, xAI must upgrade its algorithms:

Hybrid SFT+RL training: Use human expert data (SFT) as a foundation to drastically reduce RL's cost of blind trial-and-error.

Quantitative metrics + RLHF guidance: Transform subjective code evaluations into 'hard metrics' like memory usage, latency, and compilation rates, combined with human feedback (RLHF) to provide clear and precise reward signals for model evolution.

b. X platform data is inherently 'biased,' lacking B-side professional corpora:

X platform tweets and conversation data excel in C-side trend tracking but severely lack high-quality code, complex reasoning, and structured knowledge (e.g., StackOverflow, arXiv), offering limited training benefits for B-side core capabilities.

High-quality AI coding relies on a 'generate → run → feedback → refine' loop. Compared to competitors (e.g., Anthropic) that accumulate high-frequency interaction data through proprietary development tools and form a 'flywheel effect' for capability evolution, Grok's late layout (deployment) in programming tools has left it lacking continuous feedback from real programming data.

c. Organizational culture: Engineering-dominated

Grok's intelligence lag may stem not just from R&D bottlenecks but also from organizational turmoil. Since February 2026, half of xAI's founding members and core training experts have departed, objectively disrupting the iteration rhythm of cutting-edge models.

Meanwhile, as Starlink-background executives take over the AI division, SpaceX's dominant 'engineering culture' is deeply shaping xAI's R&D direction—while significantly boosting model deployment efficiency and cost-effectiveness, this may also somewhat undermine the exploratory freedom needed for frontier AGI research.

Training frontier large models requires immense human and compute investments, trapping global firms in a 'diseconomy of scale': Each model generation costs hundreds of millions of dollars, with a revenue window of perhaps just one year, while next-gen costs often double. Take SpaceX's AI business as an example:

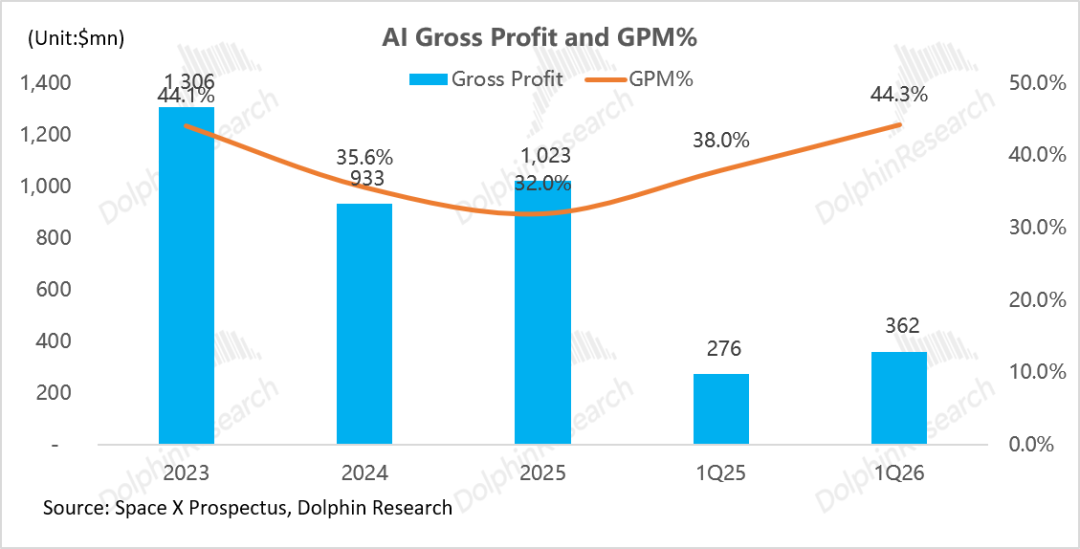

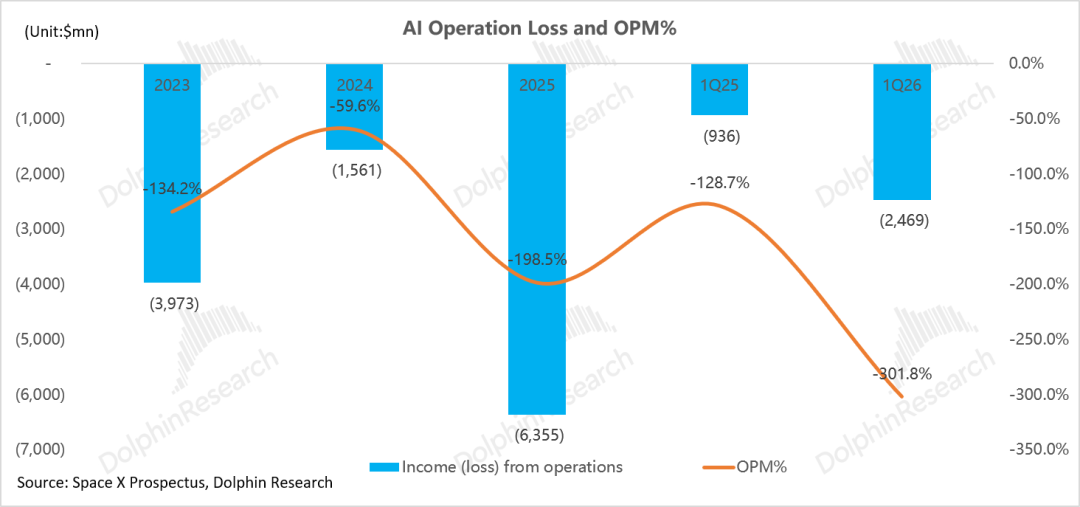

Severe operational profit pressure: In 2025, the AI division's total revenue was just ~$3.2 billion, while R&D spending alone reached $5.1 billion (1.6x revenue). High R&D and operational expenses directly resulted in an annual operating loss of nearly $6.4 billion, a loss rate of ~-200%.

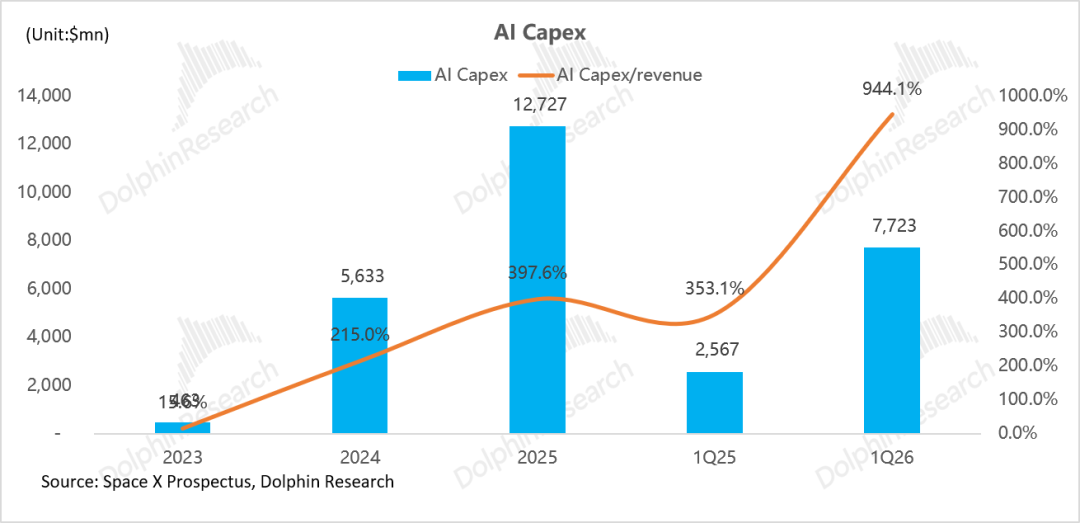

Cash flow strain from compute investments: In 2025, AI division capital expenditures reached $12.73 billion (61.4% of SpaceX's total capex), nearly 4x revenue.

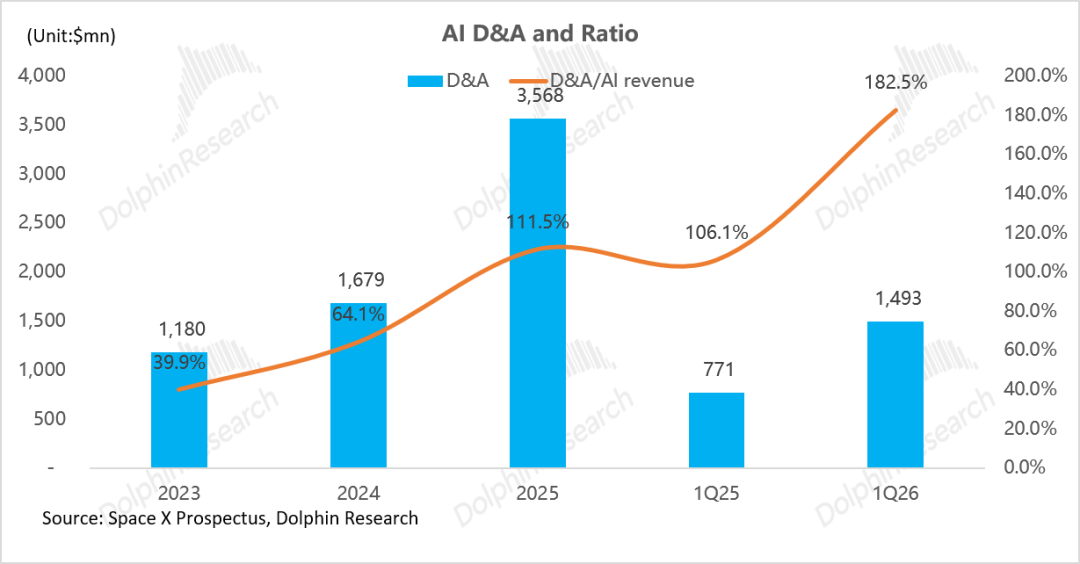

Simultaneously, depreciation and amortization expenses hit $3.6 billion—meaning current AI revenue ($3.2 billion) cannot even cover depreciation costs. The AI business relied entirely on SpaceX's other segments (primarily Starlink's $4.4 billion profit) and external financing in 2025.

The root cause of financial pressure lies in Grok's monetization progress failing to match investment scale:

C-side scale disparity and low pure-AI payment ratio: As of March 2026, Grok's ecosystem had 6.3 million paying users. However, ~4.4 million were X platform social subscribers (Grok as a value-added service), with only ~1.9 million truly paying for standalone AI features (SuperGrok), contributing just ~$1 billion in annualized revenue (ARR).

In contrast, OpenAI, also C-side-focused, has over 50 million paying users and ARR exceeding $25 billion, a massive gap.

Late B-side ecosystem entry: Grok's B-side API business (Enterprise tier) only launched in late 2025, far behind OpenAI and Anthropic's mature enterprise ecosystems.

Facing the massive gap between 'huge investments' and 'lagging monetization,' xAI has not passively waited for model commercialization to improve but proactively shifted its strategy from single-model R&D to a 'model monetization + compute leasing' dual-drive model:

IV. Compute Leasing Business: How Long Can This Unexpected 'Cash Flow Bonanza' Last?

xAI's compute leasing business was not a planned core operation but an 'unexpected gain' from technical predicament s and Grok's model lag:

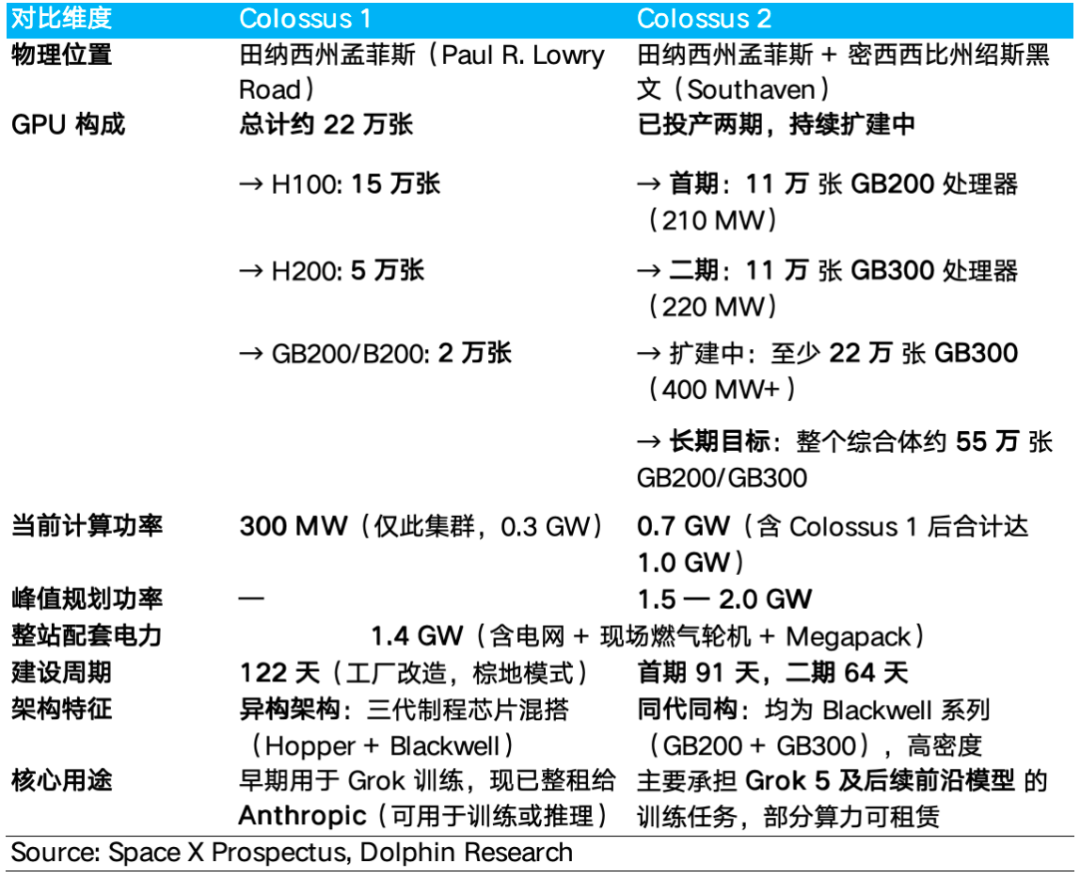

xAI's core compute asset is the Colossus supercomputing cluster deployed in Memphis. By Q1 2026, its pure compute power consumption (GPU and rack systems only, excluding cooling, power distribution, etc.) reached 1.0 GW, making it one of the world's largest single AI training data center clusters, composed of two sub-clusters:

Colossus 1: A heterogeneous cluster with ~150,000 H100s, 50,000 H200s, and 20,000 GB200s, totaling over 220,000 GPUs. Its total compute power consumption is ~300 MW (pure GPU chip TDP sums to ~164 MW, rising to 300 MW after adding server platforms, networking, and rack components).

Colossus 1 was initially used for Grok model training but faced severe 'bottleneck effects' in distributed training due to mixed chip generations, resulting in just 11% GPU utilization (MFU)—far below industry leaders (>40%)—and inability to support training for Grok 5, a 6T-parameter ultra-large model.

Facing this, xAI migrated core training tasks to the homogeneous Colossus 2 cluster and leased Colossus 1's full capacity and part of Colossus 2's capacity to Anthropic, presumably for inference workloads.

On one hand, inference tasks require far less real-time chip synchronization than training, aligning with heterogeneous clusters' weaknesses; on the other hand, this was a pragmatic choice after Grok's model progress lagged and its own inference demand fell short.

Colossus 2: A highly homogeneous compute cluster built in phases: Phase 1 deployed ~110,000 GB200s (~210 MW, completed far faster than industry benchmarks), Phase 2 deployed ~110,000 GB300s (~220 MW), with plans for further expansion. By Q1 2026, Colossus 2's total compute power consumption was ~700 MW.

Colossus 2's long-term goal is to deploy over 550,000 GB200/GB300 chips. Currently, it primarily trains Grok 5 (xAI's next-gen model, expected in June-July) and subsequent frontier models.

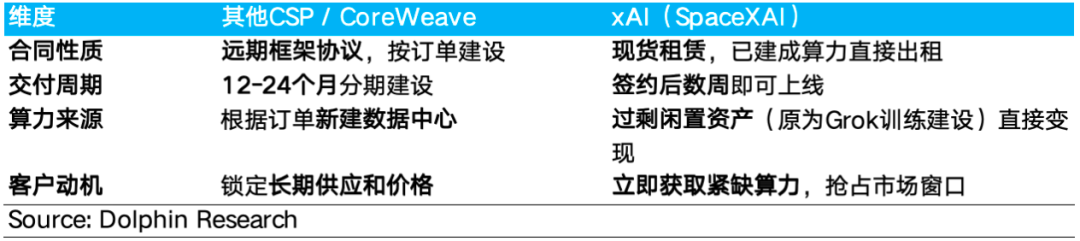

From Colossus's client base, SpaceX's compute leasing avoids traditional cloud vendors' 'massive small clients' approach, focusing instead on a 'few ultra-large clients' in ultra-large single-tenant mode:

① Anthropic (annualized $15 billion): Signed in May 2026, totaling ~$45 billion, leasing ~300 MW of Colossus 1's compute (presumably for inference) through May 2029. This forms xAI's revenue core.

② Google (annualized $11 billion): Signed in June 2026, totaling ~$30.4 billion, gaining access to ~110,000 GPUs (likely GB200/GB300) to support its AI services.

③ Reflection AI (annualized $1.8 billion): Signed in June 2026, totaling $6.3 billion, securing right of use of Colossus 2's GB300 chips.

These three contracts alone contribute $27.8 billion in ARR to SpaceX's AI business, compared to just $3.2 billion in total AI revenue in 2025 (60% from X platform ads, only ~$1.3 billion from true AI solutions and infrastructure). This means AI compute leasing, with just three major clients, has propelled the AI segment to become SpaceX's fastest-growing, highest-revenue-share core business in 2026.

While xAI has not disclosed detailed compute leasing pricing, Dolphin Research's extrapolation from contracts with Anthropic and Google reveals significant counterintuitive premiums:

a. GW-scale annualized revenue far exceeds industry averages

Extrapolating from xAI's Anthropic contract: At $15 billion annualized revenue for ~330 MW leased—first, clarify power metrics: The 330 MW refers to pure IT load (server and rack net power, excluding cooling and power distribution losses). Given Colossus 1's reliance on air-cooled chips like H100/H200, typical PUE ranges from 1.3-1.5, implying total facility power of ~430-495 MW.

This means that the actual annualized revenue per GW of total facility power is approximately US$30-35 billion. It should be noted that the contract also involves leasing a portion of the computing power of Colossus 2, so the assumptions and estimates above may be on the high side.

Cross-validation: xAI and Google Contract:

The Google contract explicitly leases 110,000 NVIDIA GPUs (GB200 or GB300), with the assumption that GB300 chips are the primary focus. Based on a power consumption of 1,400W per chip, the IT load for 110,000 GB300 chips is approximately 220MW. Considering that GB300 adopts an L2L liquid cooling architecture with a PUE value of 1.1-1.2, the total facility power is approximately 242-264MW, corresponding to an annualized revenue of approximately US$41.6-45.5 billion per GW.

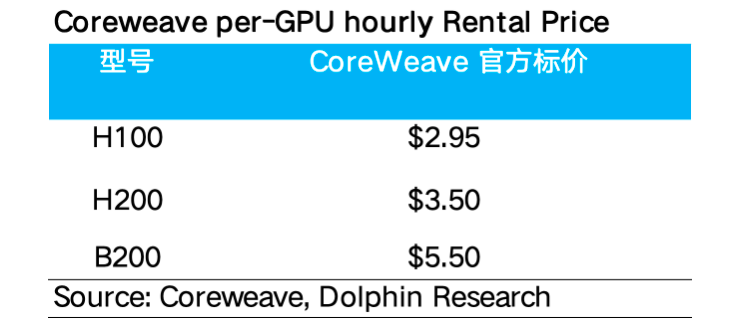

For comparison, according to industry research, the price for leading Neocloud (primarily bare-metal leasing) is approximately US$10 billion/GW, while the price for comprehensive cloud service providers (CSPs) offering a rich software and hardware ecosystem is approximately US$15 billion/GW.

Therefore, regardless of the metric used, the pricing of xAI's computing power leasing is significantly higher than the industry average.

Dolphin Research believes that given that both Anthropic and Google possess extremely strong self-developed software stacks, the services provided by xAI are essentially pure Bare Metal underlying computing power and do not include high-value-added software ecosystems.

At the same time, Colossus 1 is primarily composed of previous-generation chips such as H100/H200. Pure bare metal + previous-generation hardware should not, by common sense, command such a high premium. Dolphin Research speculates that the main reasons for this premium are as follows:

① A small number of available hyperscale inference clusters

Colossus is one of the few GW-scale AI computing clusters in operation globally. Inference for cutting-edge large models places extremely high demands on low latency and high throughput, and cross-regional small and medium-sized clusters are highly prone to network bottlenecks;

Colossus 1, with its super network topology (InfiniBand/Spectrum-X) within a single campus, successfully resolves the network storms of a hundred-megawatt power supply and tens of thousands of nodes, becoming an extremely scarce high-quality asset in the market.

② Time premium: Immediate computing power vs. forward futures

In the race to secure positions in AI applications, the speed of computing power delivery is a lifeline:

Securing market advantage: Traditional cloud service providers require 12-24 months to build facilities after signing a contract, while Colossus 1 is a ready-made asset that can be put into production immediately upon signing. Customers pay a premium for a ticket to enter 6-12 months earlier. For example, after signing the contract, Anthropic immediately doubled the usage limit of Claude Code and comprehensively relaxed the peak traffic limiting and API call rate limits for the Claude Opus model.

Supply certainty: xAI possesses an industry-disrupting facility construction speed (Colossus 1 took only 122 days, and the first phase of Colossus 2 went online in just 91 days, far faster than the industry benchmark of 1-2 years). This "deliver as promised" speed provides customers with extremely valuable "certainty premium" for subsequent capacity expansion needs—which is highly valuable in a market where computing power is in extremely short supply.

③ Risk transfer premium: The cost behind the 90-day termination clause

Industry-typical long-term locked-in contracts (e.g., 3-5 years non-cancelable, with substantial upfront payments) place the tail risk of hardware depreciation and technological obsolescence entirely on the customer. In contrast, the contracts signed by Anthropic/Google and xAI include a clause allowing either party to terminate with 90 days' notice, meaning that customers fully transfer the risk of "asset depreciation after GPU generational iteration" to xAI.

As compensation, xAI must charge a significantly higher unit price than the market to cover this risk exposure: If the contract lasts only 3 months instead of 3 years, xAI needs to recover most of its investment within this short period. Therefore, the high unit price is, in a sense, also an "insurance premium"—customers pay a higher price in exchange for the right to exit flexibly and peace of mind from being exempted from tail risk.

From the cost perspective, although SpaceX has not directly disclosed a detailed cost breakdown for a 1GW data center, we can verify its cost control capabilities from cumulative capital expenditures: The cumulative capital expenditures for the AI business from 2023 to Q1 2026 are approximately US$26.5-30 billion, corresponding to approximately 1GW of hybrid computing power deployed (including approximately 0.3GW of H100/H200 and approximately 0.7GW of GB200/GB300).

In comparison, building a new 1GW AI data center with the latest industry architecture (such as Vera Rubin or GB300) would require a total investment (including IT equipment) of approximately US$40-60 billion. Even considering architectural generational differences, xAI's computing power capital expenditures are still significantly lower than the latest deployment levels of the same scale in the industry, reflecting its significant cost advantages in chip procurement, infrastructure reuse, and large-scale deployment:

a. The "shell cost" of infrastructure is only one-third of the industry average: According to Oppenheimer, xAI's data center construction cost is only US$3 million/MW (approximately US$3 billion/GW), far lower than the industry average of over US$10 million/MW (approximately over US$10 billion/GW).

This significant advantage primarily stems from its unique construction strategy: brownfield repurposing (utilizing existing factories/buildings for transformation, avoiding the long cycles of new construction approvals and grid connections), Megapack energy storage solutions replacing diesel generators, vertical integration of self-built power supply/cooling/network full-link, and modular standard construction.

b. GPU chip procurement costs may be lower than the industry: SpaceX's close relationship with NVIDIA ensures its priority access to GPU supply and may secure discounts. SpaceX is one of the few companies globally capable of placing orders worth billions of dollars and rapidly deploying them, making it a priority customer for NVIDIA.

Although the discount amount has not been disclosed, given its enormous procurement volume and rapid delivery capabilities, xAI's unit cost at the chip level is likely lower than that of other CSPs and competitors.

In the short term, this is indeed a highly profitable business—completing computing power deployment with lower total industry investment while achieving pricing power 3-4 times the industry average and locking in profit margins far exceeding those of peers, thanks to scarce assets and risk clause advantages.

However, the sustainability of this profitability faces constraints: ① The 90-day termination clause means that super contracts may disappear at any time; ② Pricing premiums will be compressed after the supply and demand for computing power balance out after 2027/2028. Therefore, this is more of an "extremely short-term profit windfall" during a scarce window period rather than a perpetual business that can be linearly extrapolated.

V. Space Data Centers: From Ground Rehearsals to "Space-Based Computing Hegemony"—Is This Interstellar Sci-Fi or Dimensional Reduction Strike?

From a macro perspective on computing power capacity planning, SpaceX's strategy presents an ambitious dual-track approach: short-term ground data centers as the cornerstone, and long-term establishment of an industry-disrupting "space data center":

Short-term: Ground cornerstone centered on Colossus II

As the world's first GW-scale AI supercomputer, Colossus II commenced operations in January 2026. It plans to expand to 1.5GW within the year and aim for a 2GW target by the end of 2026 to 2027 (approximately 555,000 GPUs).

Operating a massive ground cluster is not only for leasing revenue but also a "mandatory course" for venturing into space. SpaceX has thereby established a full-chain engineering system for ultra-large power supply, extreme cooling, and tens of thousands of node network topologies, practicing Musk's core logic of "mastering GW-scale clusters on Earth to replicate them in space."

Long-term: Space-based computing center free from Earth's power grid constraints

Faced with the physical constraints of ground power resource shortages and land approvals, Musk views space as the best solution for achieving rapid computing power expansion within the next four years.

SpaceX has announced an aggressive deployment timeline:

The first-generation orbital AI satellites—"AI1"—with a wingspan of 70 meters, an average power consumption of 120kW, and a peak of 150kW—are expected to commence large-scale commercial networking in 2028.

2028-2030: Benefiting from Starship's ultra-high-frequency heavy-lift launches (the current V3 version can orbit 100 tons per launch, with a V4 target of 200 tons, and a long-term goal of producing 10,000 ships annually and launching 10,000 times per year), as well as the Texas Terafab chip factory (adopting a 2nm process, with a long-term goal of producing 1TW of computing power annually, approximately 80% of which will be used for space applications), SpaceX aims to transport approximately 1 million tons of computing power hardware to orbit annually. Based on 100kW per ton, this corresponds to an annual new deployment capacity of 100GW of space-based computing power (expected to be achieved in 4-5 years, i.e., by 2030-2031), with an ultimate long-term plan of 1TW (1,000GW).

For comparison, the current total installed AI computing power deployed by major global cloud service providers (CSPs) is approximately tens of GW (approximately 30-50GW). This means that SpaceX's annual increment in space-based computing power alone (100GW) is equivalent to building another "global cloud computing" capacity annually on top of the existing global AI computing stock—completely breaking through the growth ceilings of ground-based energy and land.

From being forced to lease computing power to recoup losses to attempting to reshape the global computing power landscape with hundreds of thousands of satellites, SpaceX is engaging in the most expensive gamble in history.

So, are space data centers technically and economically feasible? How exactly should one value this behemoth, SpaceX? Dolphin Research will continue to explore these questions in the next report—stay tuned!

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reproduction is permitted only with authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions expressed in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for or proposed for distribution to jurisdictions where distribution, publication, provision, or use of such information, tools, and materials would contravene applicable laws or regulations or result in Dolphin Research and/or its subsidiaries or affiliates being subject to any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other non-authorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Big Company HR Departments Are Overwhelmed: Young Job Seekers Harness Agents, AI-Assisted Interviews Spark Controversy

-

![]()

SAIC MG General Manager Overwhelmed by Online Backlash, Ends Livestream Prematurely: A Blend of Unfairness and Fairness

-

![]()

Hong Kong Stock IPO丨Recon Technology: The First Embodied Visual Intelligence Stock in Hong Kong Stock Market Launches Offering Without Cornerstones or Green Shoe Option

-

![]()

Avita Reapplies for Listing: Reports 25.6 Billion Yuan in Revenue and 3.49 Billion Yuan in Net Loss for the Previous Year, with 182 Million Yuan in Dividends from Yinwang | MIRROR Pro

-

![]()

DataStory's Controversial Hong Kong IPO: 5 Billion Valuation Hangs in the Balance Amid 866 Million Debt Pressure

-

![]()

Apple’s Prices Skyrocket Up to 3,500 Yuan! Who Empowered Cook to Hike Prices?

-

![]()

ByteDance Executives Go Viral!

-

![]()

ByteDance Executives Dominate Headlines!