Hot Topic丨Google [Changes the Game] to Secure Apple's Business, Annual $1 Billion [Hybrid Siri] Deal Finally Sealed

01/19 2026

01/19 2026

759

759

Preface:

Apple and Google have officially unveiled a multi-year, in-depth collaboration, with the next-generation Siri and Apple Intelligence to be powered by Google's Gemini model and cloud infrastructure.

These longstanding smartphone rivals, who have been at loggerheads for over a decade, have suddenly formed an alliance in the AI era. This strategic move not only propels Google's market value to surpass $4 trillion for the first time but also heralds a new phase in the global AI race, where ecosystems vie for dominance.

Image Source | Network

Rivals Unite: A Win-Win AI Partnership

The collaboration between Apple and Google has been nothing short of dramatic. These two tech giants, fierce competitors in the smartphone arena with over a decade of iOS vs. Android ecosystem rivalry, have opted for deep integration in the AI space.

According to their joint announcement, Apple will leverage a tailored version of the 1.2 trillion-parameter Gemini model to revamp Siri and bolster the Apple Intelligence platform. Meanwhile, Google will achieve widespread deployment of its AI technology through Apple's global user base of over 2 billion active devices.

At the heart of this partnership lies a 'white-label' soul transplant. Users interacting with Siri will see no Google branding or be required to link a Google account. The interface and experience remain distinctly 'Apple-esque,' yet the underlying intelligent core has been replaced with Gemini.

Apple's rationale for this collaboration model is to preserve the integrity of its ecosystem and address user privacy concerns.

Data privacy is paramount in this alliance. Apple insists that user data must never exit its ecosystem, adopting a 'hybrid processing model.'

Simple tasks, such as checking the weather or setting alarms, are still handled by Apple's on-device small models, with data never leaving the device. More complex tasks, like summarizing PDFs or planning trips, are processed by the Gemini model deployed in Apple's private cloud.

Crucially, user queries pass through a 'privacy buffer layer' that strips personal identifying information, processing data anonymously and discarding it immediately afterward. Google cannot access the raw data or use it to train its models.

External estimates suggest Apple will pay Google around $1 billion annually in licensing fees, creating an intriguing contrast with the $15-20 billion Google pays Apple each year to remain the default search engine on iPhones.

What was once a one-way financial stream has now become a two-way value exchange.

For Google, this deal not only brings stable revenue but also grants the Gemini model access to the world's most premium consumer-facing scenarios.

For Apple, this is a pragmatic move to address its AI shortcomings, enabling it to launch competitive products in the short term.

Google's Resurgence: From Crisis to $4 Trillion Market Cap

Who could have foreseen that Google, which sounded internal 'red alerts' three years ago due to ChatGPT's emergence, would now become Apple's AI partner and propel its market value beyond $4 trillion through this collaboration?

Google's AI turnaround has been remarkable. When ChatGPT took the world by storm in late 2022, Google faced criticism for transitioning from an industry pioneer to a follower. Its initial Bard model underperformed, leading Wall Street to nearly issue a 'death sentence.'

Under pressure, Google launched a full-scale counterattack. Gemini 1.5 became the key to its resurgence, securing Google's ticket to the AI era.

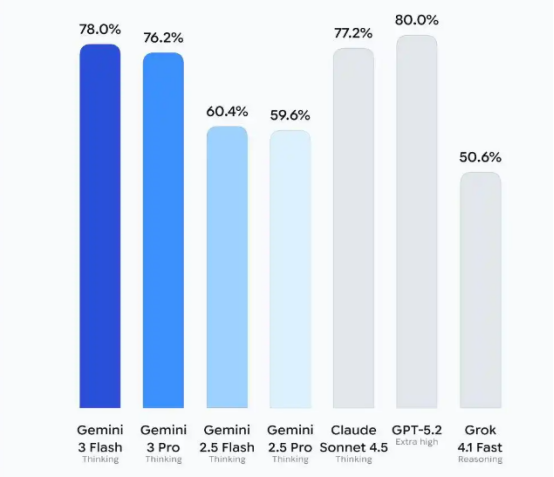

Gemini 2 and 2.5 continued to regain lost ground, while the November 2025 release of Gemini 3 marked a decisive turning point. Its multimodal capabilities and reasoning cost control reached world-class levels, placing it on par with OpenAI.

The launch of Gemini 3 Flash further addressed Apple's cost concerns by delivering near-Gemini 3 Pro performance at a lower price.

This technological edge quickly translated into commercial success. The Gemini APP's monthly active users surged from 450 million last summer to 650 million. Including core Google users utilizing Gemini functions, the total exceeds 1 billion.

Google's business ecosystem also formed a virtuous cycle with AI. In Q3 2025, Google Cloud signed more than $1 billion in deals, surpassing the total of the previous two years. Advertising revenue recovered strongly, with Q4 revenue nearing $80 billion.

Capital markets have highly recognized Google's AI transformation. Berkshire Hathaway established a 17.8 million-share position in Google stock in Q3 2025, valued at over $4.3 billion, further driving up the stock price.

From panic in 2022 to a market cap peak in 2026, Google completed an AI resurgence in three years, proving the adjustment capabilities of tech giants in times of crisis.

Apple's Dilemma: The Latecomer in the AI Era

Apple's decision to collaborate with Google stems from its long-standing challenges in the AI field.

Over the past decade, Siri's design logic has centered on three principles: localization, privacy-first, and rule-driven. This was advantageous in the 'command-based assistant' era but became a limitation in the large model era.

The issue isn't that Siri's engineering team isn't working hard but that large models inherently require cloud computing power, continuous training, and rapid iteration—all conflicting with Apple's traditional philosophy.

Apple isn't incapable of building models but struggles with 'cost-benefit analysis.' It can develop its foundational models, but the cost is exorbitant, and most critically, it cannot directly command hardware premiums.

With global hardware growth slowing, Apple cannot afford to refactor (restructure) its entire cost structure just to 'chase AI hype.' Thus, the 'hybrid approach' became the most rational choice.

As the pioneer of the mobile internet era, Apple has clearly lagged in the AI wave. This collaboration feels more like a strategic compromise forced by circumstances.

Apple's AI shortcomings have been evident. Since the 2024 release of Apple Intelligence, core feature rollouts have been repeatedly delayed, and Siri's AI upgrades have been postponed three times.

The new Siri, initially planned for release with iOS 18 in fall 2024, only launched with basic features like notification summaries and writing rewrites. In 2025, the Siri upgrade was delayed again to 2026 due to 'high implementation difficulty and subpar results.'

Talent drain exacerbated Apple's AI woes. In July 2025, Pang Ruoming, head of Apple's foundational model team, left with key deputy Tom Gunter and several senior researchers to join Meta.

John Giannandrea, SVP of AI and Machine Learning, announced his retirement in spring 2026, with core members from multiple sub-teams defecting to competitors like OpenAI and Anthropic.

In 2025, Apple restructured its AI reporting lines, merging projects like Apple Intelligence into the software engineering department and consolidating some independent AI functions into the OS development organization.

Apple's AI lag stems from strategic conservatism. While Google, Microsoft, and others were investing heavily in AI deployment, Apple chose to 'sit tight,' with severely inadequate investment in computing infrastructure and large model training over the past three years.

As a supply chain management expert, Tim Cook excels at cost control but lacks the resolve to invest in emerging technologies at critical moments.

As industry analysts note, if Steve Jobs were still alive, he likely would have gone all-in on self-developed large models when ChatGPT emerged in 2022. Cook's caution caused Apple to miss the golden window for AI development.

With self-development hindered, Apple considered various external collaboration options: continuing to trust OpenAI, partnering with startups like Anthropic or xAI, accelerating self-development, or collaborating with Google.

However, OpenAI's model quality was criticized for declining, and its shift toward consumer AI hardware posed future competition risks.

Anthropic's Claude had safety advantages but came with high pricing. Startups like xAI lacked foundational strength and ecosystem completeness, posing excessive risks.

Ultimately, Google Gemini's strong performance, mature ecosystem, and cost advantages made it Apple's best option.

Nevertheless, Apple hasn't abandoned its ambition for self-developed AI. Analysts generally believe this collaboration with Google is a strategic short-term choice, with Apple quietly advancing its AI deployment.

It has invested billions in GPUs, assembled teams, and is developing a trillion-parameter self-developed model targeting a 2027 launch. Its self-developed ASIC chip, Baltra, is expected to deliver in 2028, entering the tape-out phase in H1 2026.

Reshaping the Landscape: AI Ecosystem Competition and Monopoly Controversies

Through collaborations with Apple and Samsung, Google nearly covers both major mobile ecosystems—Android and iOS—achieving a quantum leap in Gemini model distribution.

OpenAI now faces immense pressure, with its largest consumer-side imagination space evaporating.

Despite retaining 1.2-1.5 billion monthly active users, 30-40 million paying users, and over 1 million developers, Google's advantages in resources, ecosystems, and hardware integration capabilities are more pronounced.

To counter challenges, OpenAI has resorted to 'attacking through defense' by heavily investing in computing infrastructure and signing partners, but with limited effect.

Anthropic has more enterprise collaborations but lacks consumer platform integration. xAI's Grok is confined to the X and Tesla ecosystems, struggling to achieve scale.

Apple and Google's collaboration is essentially a battle for the next-generation gateway, no less significant than the default search agreements of the past.

In the future, ecosystem integration around AI assistants will become the core of competition. Whoever controls the gateway and orchestrates the service ecosystem will dominate.

This competitive landscape takes on a different form in the domestic market. Unlike Apple's external collaboration, domestic smartphone makers like Honor and Vivo prefer self-developed models or multi-model collaborations to maintain ecosystem control.

Meanwhile, model providers like Doubao and Tongyi Qianwen vie for 'on-device' opportunities, seeking scaling (scale) distribution through pre-installations.

The domestic market's uniqueness lies in its highly fragmented service ecosystem, where cross-App execution faces permission, ecosystem, and liability challenges. This makes the domestic AI gateway battle more complex, potentially spawning new collaboration models and ecosystem alliances.

Conclusion:

From a broader perspective, the significance of this collaboration lies in how platforms are no longer closed kingdoms but capability assemblies.

Operating systems no longer need the strongest intelligence, and terminal manufacturers need not develop everything in-house.

AI is becoming a 'pluggable capability.' Future competition won't be about 'who owns everything' but who can better integrate external capabilities and control the ultimate user experience.

Partial Source References: Tencent Technology: 'Privacy, Monopoly: Five Key Questions About Apple's [Hybrid Siri],' 51CTO Tech Stack: 'Apple × Google: AI Century Alliance Officially Announced, Google's Market Cap Surges Past $4 Trillion Overnight,' Meitou Investing: 'Google Officially Integrates into Apple's Ecosystem,' Photon Planet: 'Google Has Taken Apple's [Soul].'

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan